The rate at which rents are rising in Auckland is slowing, according to Barfoot & Thompson.

The agency manages nearly 6,000 residential rental properties in Auckland and says the cost of renting a three bedroom house was $19 a week more in the second quarter of this year than in the second quarter of last year, an increase of 3.5%.

"This is the smallest percentage increase in weekly rents that we have observed in at least the last two years and is also the first time the average increase has dropped below $20 per week," Barfoot & Thompson Director Kiri Barfoot said.

During 2017 rents had been increasing at the rate of about 4.3% a year and during 2015 and 2016 rents had been rising by about 5%.

Barfoot said that a year ago the average rent on a three bedroom house had increased by $22 a week compared to a year earlier and in the second quarter of 2016 the annual increase was as high as $24 a week.

Average rent increases were edging down for all housing types except one bedroom properties, which bucked the trend and were up by 4.6% in the second quarter compared to a year earlier, while all other properties increased by less than 4%.

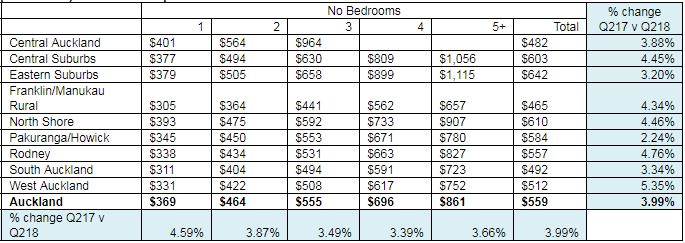

The areas with the lowest annual rent increases were Pakuranga/Howick (+2.2%) and Eastern Suburbs (+3.2%) while the highest increases were in West Auckland (+5.35%) and Rodney (+4.76%).

"We are likely seeing the beginning of a new normal in rental price trends as landlords strike a fine balance in their pricing in the face of rising operating and compliance costs," Barfoot said.

Average Rents in Properties Managed by Barfoot & Thompson June 2018

62 Comments

Auckland renters should start to negotiate down their rents in this market. If you're paying $600/week for a 2-bedroom flat, try $450/week. All the best.

First Carlos67 and now you. Is it something in the water?

Double GZ has now sold out of the Auckland market and re-positioned himself as a bear... Either that or he's part of the PRC's 'pump and dump' New Zealand housing scheme, to see how cheap our assets become after the crash

I see the Chinese have been keeping profits up at Sky City as well... love a good gamble.

Nic, all fleeing speculords should practice common sense and consult with IRD. Under the "intent provision" they're risking a future surprise if, by choice, they exited with a gain. DGZ would not want to risk having to pay this tax. It's doubtful he's sold out unless a change in circumstances forced it.

It would be pretty hard for him to sell his parents basement, without their knowledge.

Unless his parents don't live here.

with 4700 Auckland properties for rent on trade me ATM, if you have a history of long tenancy there will be plenty of room for negotiation.

I wonder what the average tenancy and days vacant per year are...???

Your spruiking form leaves much to be desired lately...

Double GZ - The first of the spruikers to leave the HMS Auckland.

https://parterre.com/wp-content/uploads/2011/06/nyco_rats.jpg

{kind=link}

BuyLowSellHigh, we are still waiting on your factual reasoning behind forecasting 5%pa house prices increases from 2021. What will be the key drivers behind this strength?

Demand exceeding supply :)

My prediction was actually that the upward phase of the cycle will begin in 2021 or 2022. Also, that YoY gain in Feb 2023 for the REINZ stratified index would be over 5%, probably closer to 7%.

I hope so. Can't wait for the cycle to move on up again.

BuyLowSellHigh, I'm trying to be open minded here but your response provides little in the way of specifics. Demand for affordably priced housing exceeds supply now. What specific driving factors do you believe will come into play between now and 2021/2022?

Glad to hear you're trying to be open minded.

You say that demand for affordably priced housing exceeds supply now. In economic terms, the word "demand" has a very specific meaning. For demand to exist, the consumer must be both willing and able to purchase the product. When demand exceeds supply, prices rise until a new equilibrium is reached.

The market for lower quartile houses is flat, so demand (in the economic sense of the word) does not exceed supply. Demand means willing and able - affordability constraints (in the form of incomes and cautious bank lending) may be impacting the able part of this equation, while market uncertainty may be impacting the willing part of this equation.

What do you mean when you say affordable houses? Do you bean small, no frills units? Lower quartile units? Demand for $100 houses will always exceed supply. Do you see why it isn't quite fair to refer to demand for "cheap" houses when talking about how supply and demand affect prices?

BuyLowSellHigh, what a load of waffle. I suspected your response might lack specific future events/policies to substantiate your prediction. Who knows, after lucking it with skellerup, maybe a second trick is in the offing. Although I seriously doubt it.

I'll always remain open minded ideas presented by people, who I believe to be well versed in relevant subject matter. On this occasion, not you.

I just want to make sure that you understand the basics of supply and demand, as your initial statement suggests you don't. I'd be better off talking to a brick wall if you don't.

Edit:

Price of lower-end houses is flat currently, so demand (in the economic sense of the word) does not exceed supply. Your statement about demand exceeding supply, despite prices being flat, is factually incorrect.

Anyway, I'll assume for now you agree that demand comprises both the ability and willingness to purchase, and that prices rise when demand exceeds supply. Looking at how NZ's property cycle has turned over historically gives a reasonably good idea of when upswings will occur. Data now shows that the market peaked in 2016, so upswing phase of the cycle can be expected in about 2021/22. In terms of what combination of factors will affect the demand side of the equation - less restrictive lending by banks, higher incomes, more consumer confidence in the market, immigration starting to rise again. In terms of supply - we still won't be building enough.

Can we get some stats on tenancy rent arrears/defaults?

Given that yields (as per interest.co survey) are well south of 5% in Auckland - less outgoings including rates, insurance, r&m, bad debts, and periods of non-occupancy - plus at best a fairly flat market, this doesn't bode well for rental properties being an attractive proposition for some time.

(And a P.S.; If you are an existing landlord, calculate your yield on the current value of your property and not what you purchased to get the true current return on your investment; then compare it to Term Deposits rates especially knowing that there is little upside as it would seem there is neither increasing property values nor increasing rents)

The problem there is that most investors know that they are not smart enough to call tops and bottoms and instead just cream massive profits over long periods of time... suckers...

Ok, well, if Auckland is at 9x income and yields are at less than 3% or less, I’m going to call that the “top”. That wasn’t so hard, was it? Is that really so difficult to time?

Agreed, However, they have so far proved to be a safe long term investment providing "Total returns" which are as good as investing in the share market for 10+ years, and certainly have left TD in their dust.

TD is eroded by tax and inflation, where rentals have CG, inflation adjusted, and claimable expenses, so less tax.

TD is great for people looking for low risk,piece of mind, and happy with small and minute returns.

total yields become positive when realised equity is invested high return classes like shares or commercial properties.

Investment is based on assurance and confidence , there are many good reasons why total $$ value invested in the share market is only 10% of what is invested in Property.

For more than a decade, property investment ( in main centres) was not treated or viewed as an additional income carrying positive yields up front.. they were rather looked at as 10+ investment and saving plans to provide future income. ... so instant yields are not important as long as running costs are under control. and so far they are returning an average of 10% pa in Auckland in CG alone.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11…

Hi Eco Bird,

You are correct in your comments about bank term deposits.

The banks market term deposits as being "investments"........ but, in reality, they are glorified savings accounts.

Astute investors know well that it's the banks that make money from term deposits - not the depositors.

Even during relatively flat property market conditions, few people are prepared to liquidate their property holdings into bank deposits.

TTP

TTP :), sorry, but your comment is unthought and misleading. In 2007, banks sourced about 35% of their funding from domestic households. Today, its risen to close to 46%. Why is that I wonder? I guess there are many households that just don't agree with your myopic investment theories. I understand banks source about 20% of their funding offshore.

https://www.interest.co.nz/news/86326/we-look-detail-where-banks-source…

Did you notice the article was put up by David Chaston. Obviously you didn't read it.

I'd say that lots of term dep money is from kiwisaver accounts.

Uninterested, I think that's under NZ Finance/Business accounts. Thats an additional 30%, also sourced locally.

Hi R-P,

Consumers/households who invest in term deposits reap relatively low returns...... As I noted above, it's the banks that make the big money from term deposits. And they are very big winners. Look at their profits in this country.

You should note that NZers have vastly more money invested in real estate - than in term deposits.

Further, since 2007 growth in the aggregate value of real estate assets in this country has far exceeded growth in the aggregate value of term deposits (and certainly the growth of domestic households' share of term deposits).

For the record, the total value of houses in NZ is now about $1trillion (yes, one trillion dollars). In Auckland alone, the figure is about $470billion (or getting on for half a trillion dollars). The figures have about doubled in the last 10 years.

Obviously, New Zealanders favour real estate investment over term deposits - by a very large margin.

Thus, Retired-Poppy, it's not me who's misleading anyone - but you. What's new??

TTP

TTP, since we're both on record as agreeing with Olly Newlands forecast of a 10 year house price stagnation (subject to no there being nil external shocks), its hypocritical for you to conveniently enrich your narrative and compare past house price increases to present term deposit yields. At 4.20%, over this longer term, it's the place to be for now.

TTP, skilled RE agents can still earn commissions in a market experiencing weak turnover. What's really the issue here?

Hi Retired-Poppy,

Sorry - but you're wrong yet again........

I have never thought (or stated) that there will be a 10 year house price stagnation.

I certainly do NOT believe the current flat period will last as long as 10 years.

I have said the market seems likely to remain flat for the "foreseeable future". I very much doubt that will extend to 10 years.

Please do not misquote or misrepresent what I state in this blog.

TTP

TTP, so NOW your backing away from Olly Newlands forecast. I'll allow you a little time to rethink the comment you just posted....

You know why? Because wage growth has been sluggish and it has not been keeping up with the rising cost of property, rents or cost of living in NZ. We now have record household debt, negative household savings and people are hitting their affordability limits. All this happening while we are supposedly meant to be having a so called housing shortage. This is not sustainable and its already starting to impact the economy as the consumer spends less as they feel the squeeze. Something has to give.

Even now it is not easy to find rental specially in the school zone. Also many overseas investors do not let out the property but keep it vacant.

OVERSEAS INVESTEMENT AMENDEMENT BILL

Can anyone still deny that the government is not trying to delay the overseas amendment bill (Though would like to scrap it but as cannot avoid it are delaying). It was under discussion on 02 July (Committee stage) and was supposed to be discussed in next sitting that is yesterday but was put last on the agenda and even today seems doubt that will be taken up as is way down the agenda ( https://www.parliament.nz/resource/en-NZ/OrderPaper_20180808/32cc828953… ). May be it will be taken up tomorrow towards the end of the day to again push for next week and then can be delayed by a month.

This is correct to say (Many are saying) that government is having cold feet and is now trying to delay and dilute (Of what is left).

Rightly said wait and watch

Flagship promise but government forgets that in today’s time where social media is active it is hard to hide or lie. See what happened to National, they should have been in power but they denied, lied and manipulated the housing problem, foreign buyer data beside other issues and see what happened to them despite winning (It is not WP but they themelves to be blamed for being out of power).

Current Labour Government may be a One term Wonder

One term disappointment.. following on from a three term disappointment. Maybe Gayford better get the Mrs knocked up again in time for next election so she has an excuse to step down before the train wreck.

lol, that was a good piece of advice ...hope he is reading this ...

But seriously, now that you sampled the current CoLs, which " disappointed " would you like to have in 2020 ?

I fancy a team who listens and executes, make money and spend money, not spend money, piss the money makers and tax for more ... I would like National come back to teach these noobs a lesson and send them home to do some serious homework maybe they get better prepared next time.

Eco Bird, I think many Labour supporters will agree with you and surprisingly it has happened in less than a year and just imagine what will happen in next 2 years by election.

Hi Stuart & Eco Bird,

Labour really has very little to show for its first 11 months in office......

And things may well be about to get a whole lot tougher.

TTP

Indeed gents,

I guess a lot of people do not find the word " disappointment " strong enough to express their sentiments.

everyone is surprised how this lot showed so much incompetence so soon in the piece ...

But, now that the patient is told about his terminal illness , he went into denial stage and will pull all stops to show that he will survive the inevitable bitter end.

Agree.

Negative counting has started for Labour.

I didn't want either set last time... Can't see me wanting either lot next time.

However, you will end up with one of them next time whether you liked it or not - they are the two biggest parties and cannot shoved aside... I see why you are and will be continuously disappointed.

they are slightly different variations on populism. Neither party has the inclination or balls to do the best for NZ's future.

Ah yes, how dare I actually hold out hope for politicians that will actually do a decent job. But if push comes to shove I'll vote Labour before the Nats.

No one holds out hope for the perfect poly who can do a perfect job,

they all are as good as the advice they take and as good as they listen to the public and drivers of society.

The smart ones will judge by logic and sense before ideology and own believes ... like any manager in any leading position - there are good ones and bad ones - clever and short sighted, astute and noob, productive and self serving.

The brand doesn't make much difference as they will all eventually toe the same line , the only distinction is the amount of damage they would leave behind when it is time to go.

Hi richard 1965,

You're absolutely correct.

The government is running scared of the Bill...... and for very good reason.

If passed, it knows there will be another PLUNGE in business confidence.

The Bill has been much watered down and is a mere shadow of its original incarnation. Thus, its impact would be slight - and not worth the wider costs to the government.

In fact, it's as big a can of worms as KiwiBuild. Both are election campaign bribes that have far-outlived that purpose. They have now become LIABILITIES of the government.......

Collectively, they might be thought of as a twin-headed monster.

TTP

Yeah. All Labour supporters have been taken for a ride :)

Than National was no different but it seems that Labour will be out of power and WP who makes more noise when in opposistion will find it hard to reach 5% treshold.

Yeah. All Labour supporters have been taken for a ride :)

Than National was no different but it seems that Labour will be out of power and WP who makes more noise when in opposistion will find it hard to reach 5% treshold.

Rent reviews are not a matter of pure science or economics theory for most Landlords ... it has very little to do with tenants wage growth or personal debt in a market where demand exceeds supply. Most of the Increased running cost of property needs to be met by the user.

However, rent rises in the range of 2.5 - 3.5% pa in Auckland ( mine were around 1.9% last year) remains reasonable for both sides ... I personally don't think that it should linearly track property prices because realised CG usually compensates for any loss in yield until rents catch up a bit later.

Having said that, tenants should pay their fare share of the increase in cost of living & outgoings and rent is part of that ( just like they would incur these expenses if they owned the house).

There is always a balance to stick between the human touch and business realities and requirements ... I personally wouldn't like my rent to go by 5% pa if I was a tenant on steady income, but these are just unavoidable expenses like fuel tax or car insurance increase -- unfortunately, they are user paid,

Eco Bird, rents are falling in Newmarket, Northcote, Oceanview, Harbourside, Grey Lynn West, St Lukes, Kingsland, One Tree Hill, Epsom, Mount Eden East, Balmoral and Seacliffe. Rents have stalled in a number of areas yet some have still increased. A large number of apartments nearing completion, there's a question mark over immigration/student numbers and Kiwibuild is sure to empty out some rentals. I think it's slowly turning into a renters market to be honest. A growing number of Landlords are struggling to pass on costs - period.

https://insights.nzherald.co.nz/article/rental-bonds-2018Q2/

hahahahah .. thank you for making my dull day RP

please keep feeding us with your excellent first hand news. I am sure someone will eventually believe you ..lol

Better get something stronger to warm me up after your " chilling " news

period !! ... lollololol

Eco Bird, that's a lot of nervous laughter you've stuffed into one comment there ;-)

Hahah, I am still laughing RP ... did you see the table above before writing your comments? .. do you see anything falling or negative numbers...?

if not go to specsavers ..

Is that all you're doing during the day?, stir the shit in hope that someone will pay attention lolololol? ...

But hey, as shameless as you are, you don't care if you are wrong .. you have tried anyway ...hahahaha

Hi Eco Bird,

I agree that Retired-Poppy ought to head to SpecSavers.......

But to get his eyes tested, he might have to cash in one of his term deposits - which would hurt him too much.......

Oh, the pain!

TTP

Tenants should re-negotiate their rent with landlord. Failing that they can get some more people in to share the cost.

I love how you make decisions for others and dish out " productive and practical " advice ...:)

Maybe tents in the backyard, sublet the garage. Lots of options.

Huge demand for these types of accommodation from all the cheap immigration we are letting in for scrubbing our pots and driving ubers.

One of the problems affecting supply of available rental housing is the strange phenomena of Ghost Houses & Ghost Apartments.Nothing spooky about the property. Much to do with property flippers awaiting an opportune moment to unload but spooked by hassle of tenancies.Hopefully some of Labour's measures in the pipeline to address housing ownership etc would alleviate this phenomena & add to rental stock. Would it impact upon rents?? Case of Supply vs Demand.

I love the words like "Only 2.5% or a 3.5% increase" the problem is your wages are not doing the same. Even what people call "Small increases" like this are actually huge increases YOY. Try getting a 4% pay increase every year to cover it and this only stops you going backwards, good luck with that.

Its okay, this lot in govt will crank up the accomodation supplement for working class stiffs. Soon paying $600/week in rent while earning a 6 figure household income will be subsidised to the point where no-one will care.. then they'll crank taxes up to pay for it.

But what's crazy is that both our major parties were campaigning on increasing WFF and the Accommodation Supplement.

Yeah, thats effectively tax funded state housing without HNZ being involved.

Yeah...and without the boosted supply of previous decades. All it does is raise everyone's rents and depress everyone's wages.

Greed has turned NZ into a place where you cannot live. Middle class no longer exists- just the haves and the have nothings...thats why NZ has the highest homelessness rates in the World. $860 to house a large family ...bloody hell. In Perth for an amazingly huge and near new house of 7 bedrooms with a pool...my family pays $595 and the wages are double. The NZ economy and property market is in a World of trouble.... and the little people will suffer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.