The downturn in the Australian housing market is being closely followed on this side of the Tasman, with many people believing Auckland's housing market will follow the Australian market and head into a slump next year.

However Auckland Council's chief economist David Norman doesn't think so.

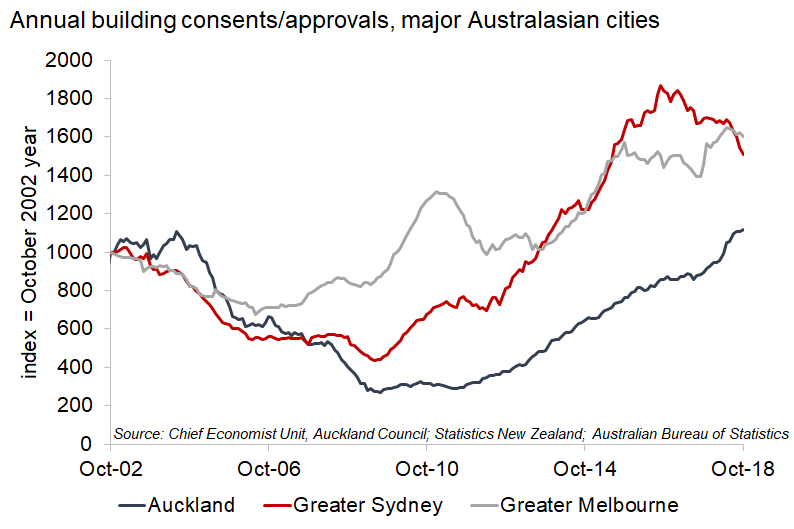

In a LinkedIn post, Norman said Auckland's housing market was unlikely to follow trends in Sydney and Melbourne.

"Suggestions that the Auckland housing market will follow those of the Australian eastern seaboard seem baseless," he said.

"Sydney and Melbourne are in a very different position, having not systematically under-built the way Auckland did, and thus having no significant shortfall.

"Auckland's shortfall is around 46,000 dwellings.

"Our trans-Tasman cousins' two largest cities have an oversupply of apartments, largely the result of building for the foreign investor market that is not as buoyant any more (the way Auckland overbuilt for overseas students in the early 2000s).

"This has concerned some of the banks in Australia for years and explains some of their nervousness about lending for apartment projects in NZ.

"Hopefully this chart [See below] will dispel some of their fears!"

"We need to keep building for a very long time at current rates and faster to eliminate our shortfall," Norman said.

Readers may also be interested in this video interview with ANZ's chief Australian economist David Plank discussing that country's housing market downturn, and in this article on Auckland's housing shortfall.

98 Comments

The funny thing about Sydney and Melbourne is a lot of economists got it wrong also. Check out these predictions all of 10 weeks before the Australian property decline:

https://www.domain.com.au/news/what-now-for-sydney-property-prices-five…

https://www.domain.com.au/news/melbourne-property-prices-will-they-cont…

I disagree with David Norman. If theres such a housing shortage why is there close to 7 months of stock on the Auckland property market?

This presentation was bought to you by the numbers 2, 0, 1 and 9, and the word AFFORDABILITY.

A shortage of houses would imply that there are desperate buyers out there who simply cannot find a house to buy for love or money. However, the number of listings and the days on market suggest that this is not the case. There is an ample supply of houses to purchase - but not enough buyers who can afford to buy them. This whole "supply" argument is completely bogus. People are not forced to buy houses - they can continue living in their current home, be renting, flatting with others, or continue living at home with their parents.

Property prices are falling in Sydney and Melbourne due to a credit crisis. Bank customers can't refinance easily and new lending is much, much more difficult to get.

Some off-the-plan buyers are having to walk away from their initial 10% deposits now because they are unable to get financing to settle.

Supply and demand hasn't changed, just the demand side doesn't have access to easy money anymore. Same is beginning to happen in Auckland. This factor has been ignored in this article.

Simo, I agree with your comment that credit availability in OZ is hurting but I still think oversupply in Syd & Mel is an important cause because other cities in OZ (that are subject to the same credit tightening) are not going down in value.

Also I wonder why you claim that it's harder to get access to money in Auckland? It's the same for all of NZ and the latest move has been to relax the LVR rules, so to make credit availability a little easier

Its important to remember the greatest contributor to house price movements, both up and down, is availability of credit. Banks make lending decisions based on risk. That may be by customer, suburb, city or region etc.

Auckland prices have followed a similar pattern up just like Syd and Melb, and now sales especially auctions clearance rates have fallen below 30%. Supply of unsold houses and days on-market have risen etc. NZ Banks will be adjusting their lending decisions to reflect this increased market risk in Auckland. Other places in NZ will have a different risk profile and bank lending will will reflect this risk.

"Supply of unsold houses have risen", this is incorrect as it was under 12'000 for Auckland last Friday and used to be around 13'500 in November. I also doubt your claim that banks have different lending rules depending on which region you want to buy a house. What the banks are interested in is a customers ability to service the loan and the collateral, not the location of the house

Just because listings have been removed doesnt mean they have been sold. As is happening in Australia, lots of unsold houses have been pulled from the market and placed up for rent (driving up the vacancy rate and lowering rents) or simply taken off market over the Xmas holiday period, in which case they will return to the market in the New Year.

Banks definately have different criteria for different areas and postcodes. A quick google of NAB and postcodes at high risk will lead you to many well published articles on this. The NAB list was leaked out. Banks never publish this information.

Here is one example: High Risk and Blacklisted Suburbs. https://www.canstar.com.au/home-loans/getting-loan-blacklisted-suburb

TB, I was talking about New Zealand, not other countries, I made it quite clear when I said in my earlier comment: "It's the same for all of NZ"

NAB owns BNZ. Pretty good chance the same practice will be driven into the NZ market given half a chance.

I'd also like to see David Norman argue that Sydney, Melbourne and Auckland don't share one thing in common - a glut of un-affordably priced homes. There's always a shortage on the ride up. Selling starts, suddenly there's ya surplus!

Quit dreaming David Norman.

And if it does, he should be fired from his job. Guys like him make these statements knowing there are no repercussions. .

Whereas your prediction of the NZ property prices of the last 8 1/2 years is more accurate?

Yes, when I first created my profile they were falling. .. and now they are starting to again. . Too bad for you. .

Between the date you created your username and today, have property prices fallen or risen astronomically? And do you think the median house price will ever again be as low as the day you made your username?

Simple reason for his opinion; it's not in Auckland Council's interest to have a housing crash. This statement is no different from tobacco companies saying that there is no link between smoking and lung cancer.

Why would Auckland Council not want a housing crash?

Why would Auckland Council not want a housing crash?

Pretty obvious

Not to me, please enlighten me?

You would never understand. . So take put you through the pain

Thanks for your great explanation PP2F, it clearly shows your knowledge

The higher the RV, the more the council can collect in rates is just one example.

In the denial phase already

Right. So David Norman chose one very specific thing (oversupply of apartments) and completely ignored all other factors? Like who's gonna buy all these overpriced Auckland houses now that Chinese money is gone? Great thinking, David Norman!

You make an interesting comment - there is an oversupply of apartments and I assume not of other types of housing. Then the question becomes are all types of housing dropping - if so then the oversupply of apartments - maybe, just maybe - a red herring....

Mr Norman is obviously unaware of the fact that Auckland is Sydney is Beijing is Buenos Aires is Timbuktu. And economic headwinds experienced by any country anywhere are felt ten times harder by the Auckland property market than in that country itself.

BLSH, when invited to make your predictions for Auckland house prices to December 2019, you declined on grounds you wanted to see what others would predict. By what percentage do you predict Auckland house prices will have declined by December 2019?

Don't be afraid, step up and make your prediction.

You have addressed him incorrectly

Merry Christmas Poppy, although you strike me as the type of miserable fellow that would put coal in their grandchild's stocking in order to acclimatise them for supposed tough times ahead.

At no point did I not acknowledged global risk - I just never exaggerated it. I declined to tell you my 2019 prediction because I don't want to ruin the surprise when we are asked for predictions in a few days time. You're obviously on tenterhooks awaiting my insights, but you'll just need to be patient.

Oh dear, a weak excuse and a sideshow. It seems for you it was an Auckland-Sydney marriage on the ride up, divorce on the way down. Speaks volumes about you ;-)

Why can't you make a decline prediction right now and own it?

Hi R-P,

Rest assured that whatever predictions people happen to make here, none of them are likely to fall as wide of the mark as the ones you've made.

In terms of accuracy, I know of no predictions here that have proven as unreliable as yours.

If I was you, I'd refrain from making any further predictions - mounting evidence shows predictions just aren't your strong-point.

Go enjoy Christmas instead!

TTP

Agent TTP, I will certainly be enjoying Christmas with family and friends;-) Again, my invitation still stands for you to reveal your facts that mitigate the current and growing risks.

First time buyers, this is a time to be a member of the audience. Before your eyes it will all unravel.

RP: "Why can't you make a decline prediction right now and own it?"

Because BLSH doesn't want to look like a fool, like when you predicted Auckland prices to be down by 5% year-on year by this Christmas

Yvil, huh? but I don't feel foolish. Anyway, its an anonymous forum! Perhaps, instead of being consumed panning the forecasts of others, have the courage to make a forecast yourself - and own it. Put some of those skills you profess to have on display. Besides, Auckland prices have registered a small decline overall, some areas by more than 5%. The downturn is still in front of us, not behind us.

You've already acknowledged they will decline throughout 2019 but created a sideshow when pressed for a percentage. Like BLSH, are you also afraid of feeling foolish?

Step up Yvil!

“Like BLSH, are you also afraid of feeling foolish?”

You’ll find most people have an aversion to looking foolish Poppy - a characteristic you evidently do not have at all.

Ooooh, BLSH is getting a little titchy. Why is that? Step up and put your forsight on display. Don't wait to see what others are forecasting. Are you the Papamoa Beach based property Oracle or not?

Okay, I guess in conclusion, in fear of looking foolish on an anonymous forum, the resident Spruikers aren't prepared to forecast the extent of Auckland's house price decline in 2019.

I predict they will spend the entirety of 2019 panning the forecasts of others!

I’ll be forecasting plenty in a few days time. I said that I have a property in sunny Papamoa Beach, not that I’m based there myself.

BLSH waiting to see what others forecast first. How incredibly insightful........

Whatever you say Poppy.

Overall maybe not down 5%, but there are plenty of locations down 5-10% - so not that wide of the mark

I'm prepared to repeat my prediction of a -5% overall adjustment for Auckland house prices for 2019. I was certainly premature in forecasting this for 2018. They fell a small amount however, the downturn influenced by events beyond our shores, is still in front of us.

There are locations up by that much as well. You can cherry pick whatever result you want, but that’s not how it works.

How long do you expect Auckland to stay as expensive as Silicon Valley or Melbourne?

I really can't bring myself to bearish on this market when I compare Auckland prices with real world class cities. And it's not like it's a Luanda situation.

"We know there's a housing shortage here, because we worked damn hard to make sure no one could address it"

All too true.

is this a joke

Falling mortgage interest rates should keep Auckland property propped up for a while.

If that happens... will be an interesting dilemma - downward OCR predictions but upward capital requirements = fighting over deposits, so potentially, this time, borrowers might pay the piper not depositors.

Plenty of reasons why Auckland could follow. Less money chasing the same amount of stock (hot money from overseas - same thing that drove Sydney funnily enough). Migration away from Auckland to the suburbs - or Sydney / Melbourne as they become more affordable. A recession. Etc.

The next Global downturn has started and boy are we in for some trouble. It doesn't matter where you are on this planet, Asset values across the board will be getting readjusted. Even with an ok economy, high migration, record low interest rates and an undersupply the Auckland market here is flat and starting to dip in some areas. That is a telling sign in itself. It all comes down to affordability, peoples appetite for debt risk and the supply of credit. How many first home buyers do you know that will be taking out a mortgage if there is job uncertainty? It all comes down to sentiment and when the jobs start getting culled less people will be willing to step up and take on the large mortgages to keep the Auckland debt bubble going. Credit availability will also be tighter in this next downturn and this will have a major impact on prices as well.

Hi Adam, have a good X-mas, hope to catch up with you on NYE since you didn't make it to R&R's

Looking forward to partying with you my man!

Lets go back a couple of years to Sydney's "undersupply of housing means no bust" just for LOLs

https://www.domain.com.au/news/sydney-property-undersupply-a-myth-says-…

true, and they are forgetting that if supply remains the same then price could still drop if demand falls. this is possible in this global downturn

"Despite the widely held belief that Sydney has too few properties, he said there would be more than enough property to go around, if it weren’t for investors"

"This sounds all too familiar"

You should get into politics AdamB. Word on the street is you really know how to create a successful party ;-)

some people just can't accept the fact that nothing lasts forever, price can't just go up and up

a delay until the same property downturn does this side of the Tasman the same

why is AKL council wading in here? are they trying to talk up the ponzy?

I’ve heard from several experts in the property sector that it is a myth that we have an undersupply. In fact, I have heard on numerous occasions that we have it about right.

Maybe there is a realisation within council that if construction stalls, then they may have to instigate a mass layoff, and find some revenue elsewhere to fund Goff’s monuments

Belt tightening in Goff’s language may be unpalatable

I'm reminded (yes, I'm That old) of the famous quote in the Profumo Affair trial, from Mandy Rice-Davies:

Well (giggle) he would, wouldn’t he?

Economists have put together a visualization of where the New Zealand housing market is likely to be going. I found this quite fascinating.

According to the "CoreLogic Home Property Value Index" fall in apartment price in Melbourne YoY was 1.71% and whooping 7.6% for the houses. Similar trend for Sydney too.

So, what oversupply of apartments are you talking, if prices did not fell for units as much as for the houses?

Better resign, David!

Simplistic economics at its best! Well done David and Auckland Council!

Yep, "supply and demand" what a crazy, untested economic model

Supply and demand is great, even better when the whole picture is considered not just one factor. Which is what I assume Fritz is getting at.

Yes

Unfortunately you wouldn't understand an economic model. .

Bulls leaverage up...oh you cant if your alread on minimum equity (like most). Bears...sit back and continue to eat popcorn.

Unless Govt unleashes immigration tidal wave times are a changing. If they do Govt will change next time around as NZ wont take both socialist BS and lies. Nat were just lies.

Eating popcorn has never made anyone rich ; )

Hi Yvil

George Soros apparently ate popcorn whilst shorting the pound in the early 90's... No fat, low calories and kept him occupied during a crash

I think when Averageman says: "sit back and continue to eat popcorn" he means take no action, clearly Soros and other successful people take action.

Nah. Waiting for reality to hit having cleared debt. Working on building a business with recession proof income and adding to a vulture fund to pick over the impending specuvestor collapse. So...not doing nothing, just waiting, also known as timing.

Now have you tried ham with popcorn...?

Economists are not known for their accuracy when it comes to predictions.

Now, one working at the council? Bwwaaahhhhahaaha.

Don't insult evil, he's backing the council economist all the way

look at the contrast:

the urban planners are making them look good!

Where is Gordon?

Hope all is well and he has a great Xmas or is he really Retired Poppy??

Gordon, Another year gone by and you haven’t taken up the challenge, but then we all know that The Man never tells porkies, and predictions are always correct!!

Ha-ha-ha :) Nah, I'm not Gordon and he isn't me :)

Merry Christmas TM2.

Are you having withdrawal symptoms without Gordon

Wouldn’t say withdrawal symptoms, more just concern that he is ok!

Also wouldn’t mind him taking me on with the challenge that he has been offered for a long time, but he hasn’t even mentioned ever whether he will take it up or not!

All depends on the immigration rate. Australia's has not dropped off yet, whereas NZ's is reducing.

Auckland = rate of increasing demand slowing & substantial undersupply of houses

Sydney/Melbourne = constant excess demand and less undersupply of housing

Just think how many Kiwi's are going to be leaving when Sydney house prices are cheaper than Auckland, while salaries are twice the NZ rate LOL. Better pray that Auckland house prices drop, or there will be no-one left there but a few foreign migrants sharing bunk beds in flats who didn't get an Aussie visa so they'll use the NZ backdoor.

check the maths.

mortgage growth.

Change in the rate of change in new credit - new mortgages.

- its a big thing:

as someone said, its in the hands of those new borrowers that want to "step-up"

Come on!

Akld council has a lot of debt.

If housing crashes, new builds disappear and that is a big revenue stream.

Also the rely on rate increases and its hard o push up rates when values are sliding and people are feeling jittery about their wealth.

It seems that Govt and banks alike are committed to the same narrative of plateauing market withbthe pipe dream that wages will catch up.

The Sydney and Melbourne markets are declining due to changes to credit availability so quite different to Auckland but never the less the Auckland market is teetering on the edge and there is no upside and a lot of downside pressures with credit availability being one of those,

So lets see how she goes

Too many people on this site just sitting on the sideline "Seeing how it goes".

Jim Lovell Quotes. There are people who make things happen, there are people who watch things happen, and there are people who wonder what happened. To be successful, you need to be a person who makes things happen.

Indeed, far too many "popcorn eaters" on this site, lol

Mmmmmm...popcorn.

Honey and popcorn....probably has nothing to do with lending decisions. In the same breath why wouldnt you sit and wait out another 6-12 months to see what the overswas debt chaos storm delivers.

But if they sit around long enough then someone else might make things happen for them.

Yeah true if you just sit round long enough shit happens for them.

People like me (and i can tell you right now that I would be deemed as upper middle class) have not a shit show in hell, getting a mortgage in NZ. $800k mortgage with a deposit of $160k... no wonder I like many others have crossed the ditch for much better treatment. But heres my prediction... property down over 12% by Jan 2020 in Auckland.

Know several in this boat. But hay its more important to look after banks and debt farmers than keep our best and brightest in NZ. Its ok Aussie will still send their tax to NZ....tui

Just saying where NZ sits in the scheme of things.

https://www.huffingtonpost.ca/2018/09/15/riskiest-housing-markets-canad…

I don’t really care what the AKL housing market does as I don’t live there anymore and never would want to again but I believe there will be a hell of a correction. I’d encourage many an Aucklander to go on a few trips to 3rd world Asia and have a look at the standard of living in those cities as that is exactly how AKL will turn out to be like. Most Aucklanders know thats the case so are packing up and leaving to far nicer places like Tauranga, Napier and Nelson if they are lucky enough to find a reasonable job. THe ones that are left can either earn average money slugging it out in Aucklands fast deteriorating standard of living never leaving the rat race or they can move to an Australian city which offers far superior earning capabilities and a better standard of living. Auckland is a sinking ship it has no attraction whatsoever unless you’re a 3rd worlder.

Markets with inelastic supply (like Auckland housing) traditionally have much bigger declines when demand recedes. Auckland is going to perform much worse than Melbourne or Sydney, because of the housing crisis.

Economists focus on the supply from a primary market perspective (i.e new houses being built to meet underlying demand). They focus on underlying demand and underlying supply for housing and not effective demand and effective supply for housing. This is how they can get caught out with respect to their property price forecasts. The article above focuses only on underlying demand and supply.

However, anyone who understands prices in any free market realises that prices are set at the margin and these can be largely determined in the secondary market - i.e by the marginal buyer and marginal seller of an existing house. This is the effective supply and demand in the property market.

If there is a desperate, time constrained marginal seller, and the seller is willing to accept a lower price from the buyer, then this becomes the new market price.

Now imagine that there are economic conditions which result in a large number of desperate, time constrained or financially stressed highly leveraged property owners. And as prices trend downwards (and this is more commonly reported in the mainstream media), potential buyers extrapolate this downward price trend and have changed future price expectations - they then decide to wait for lower prices before buying - this results in fewer buyers at current price levels. If you recall, when property prices were rising rapidly, buyers extrapolated this price trend to determine their future price expectations and there was a fear of missing out, and hence the rush to buy.

That is how free markets can result in a supply / demand imbalance with price being the variable that changes and brings effective supply and effective demand back into equilibrium ...

For those who don't know, the difference between underlying demand and effective demand - from MBIE

A 2009 / 2010 report by the Dept of Building and Housing recognises two types of demand

1) underlying housing demand

2) effective housing demand

1) Underlying housing demand

‘Underlying demand’ refers to the number of houses needed to accommodate households in the population. Population increase in the age range of 20–40 (which is when people tend to form independent households) leads to smaller household sizes and more single-person households. Further, positive net migration increases underlying demand for housing. A ‘household’ means either one person who usually lives alone, or two or more people who usually live together and share facilities in a private dwelling.

Natural population growth rates, internal migration, housing preferences and household formation rates all tend to change relatively slowly, and therefore changes in underlying demand caused by these factors are reasonably predictable. By contrast, the level of external migration depends on policy rules and incentives, as well as on wider domestic and international economic conditions, and it therefore tends to have a more volatile, less predictable impact on underlying housing demand

2) Effective housing demand

Effective housing demand is the combined effect of both 1) the desire to rent or buy a house, and 2) the financial ability to rent or buy a house. This aspect of demand is what shows up in the housing market statistics for sales, prices and construction. It also largely accounts for the changes in housing and tenure choices over time.

The New Zealand housing market has not only experienced increased underlying demand from population growth and higher net immigration; it has also (until the recent global financial crisis) experienced an increase in effective demand as a result of higher incomes, lower unemployment, cheaper and easier access to credit, and the preference of New Zealanders, for various reasons, to invest in housing over other forms of investment.

The difference between underlying and effective demand is a function of:

• buyer wealth and income

• the cost and availability of finance

• the state of the economy

• individual consumer preferences (for example, location, or between renting and owning)

• the attractiveness of housing as an investment good.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.