By Greg Ninness

Rents are rising more slowly in Auckland and Tauranga than they are in most of the rest of the country, according to interest.co.nz's latest quarterly analysis of rental bond data.

It found that the average rent for all new bonds received by Tenancy Services in the fourth quarter (Q4) of last year was $456 a week, up $24 (5.5%) a week compared to the Q4 2017.

That compares with a rise of 4.1% in Q4 2017 from Q4 2016, suggesting rents throughout the country rose at a faster rate in 2018 than they did in 2017.

However there were also major regional differences.

Average rents in Whangarei, Auckland, Tauranga and Canterbury rose at a much lower rate than most other parts of the country (see table below).

In the Auckland region, the average rent increased by $19 a week between Q4 2017 and Q4 2018.

That's an increase of 3.6%, unchanged from a year earlier, suggesting the rate of increase in Auckland was flat.

Within the Auckland region, four districts (Rodney, Waitakere, North Shore and Franklin), posted lower percentage increases last year than they did in 2017, while the other three districts (Central Auckland, Manukau and Papakura) posted percentage increases that were up compared to 2017.

The biggest increase in Auckland, in both dollar and percentage terms, was in Papakura where the average rent increased by $31 a week, from $483 in Q4 2017 to $514 in Q4 2018.

The smallest increase in Auckland was in Franklin where the average rent was up by just $6 a week (1.2%) followed by Waitakere with an average increase of $11 a week (2.2%).

The average rent increase was also modest in Christchurch where it was up by $10 a week (2.6%) but that was a substantial rise on the previous year when the average rent increase was just one dollar.

Selwyn was the only district monitored to show a decrease, with the average rent in Q4 2018 down by $2 a week (-0.5%) compared to Q4 2017.

In all of Canterbury, average rents were up by $8 a week (2.3%) compared to just $3 a week (0.7%) for the same period of 2017.

Rental growth was also weak in Dunedin, where the average rent increased by $4 a week (1.1%) between Q4 2017 and Q4 2018.

That could be a danger signal for residential property investors in the city because Dunedin has experienced significant investor activity over the last few years and the low rate of rental growth may suggest that they increase in rental stock is starting to outpace the growth in demand from tenants for rental properties.

If a surplus of rental properties in Dunedin eventuated, that could result in falling rents and higher vacancy rates, which would likely flow through to lower capital values for rental properties.

However many parts of the country posted very high growth in rents in Q4 2018 compared to Q4 2017, led by Hastings 20.7%, with Napier, Whanganui, Kapiti, Porirua, Upper Hutt and Queenstown-Lakes all posting double digit growth in average rents.

The Wellington region had the highest rental growth of the main centres at 9.4%.

The most expensive place to rent a home in Q4 2018 was Queenstown-Lakes, where the average rent was $633 a week, while the cheapest place to rent was Invercargill at $265 a week.

| Changes in Average Rents By District | |||

| Average Rent Q4 2018 $/week | % Change Q4 2017- Q4 2018 | % Change Q4 2016-Q4 2017 | |

| Whangarei District | 387 | 5.4% | 9.4% |

| Rodney District | 557 | 2.9% | 5.1% |

| Waitakere City | 507 | 2.2% | 4.7% |

| North Shore City | 594 | 2.7% | 4.1% |

| Auckland City | 571 | 4.2% | 1.9% |

| Manukau City | 543 | 5.1% | 4.7% |

| Papakura District | 514 | 6.3% | 2.9% |

| Franklin District | 480 | 1.2% | 2.7% |

| Auckland Region | 549 | 3.6% | 3.6% |

| Hamilton City | 395 | 6.1% | 4.0% |

| Tauranga District | 465 | 3.9% | 5.2% |

| Rotorua District | 359 | 7.7% | 6.1% |

| Napier City | 404 | 10.3% | 7.5% |

| Hastings District | 426 | 20.7% | 5.0% |

| New Plymouth District | 363 | 7.3% | 2.8% |

| Palmerston North City | 340 | 3.7% | 2.5% |

| Wanganui District | 285 | 13.8% | 8.5% |

| Kapiti Coast District | 419 | 10.1% | -0.7% |

| Porirua City | 500 | 15.8% | 4.9% |

| Upper Hutt City | 421 | 14.2% | 11.1% |

| Lower Hutt City | 420 | 8.3% | 7.9% |

| Wellington City | 534 | 8.4% | 7.0% |

| Wellington Region | 500 | 9.4% | 6.3% |

| Ashburton District | 324 | 0.4% | -0.3% |

| Banks Peninsula District | 375 | 0.8% | 1.1% |

| Christchurch City | 381 | 2.6% | 0.4% |

| Selwyn District | 452 | -0.5% | 2.1% |

| Timaru District | 332 | 9.8% | 5.8% |

| Canterbury Region | 378 | 2.3% | 0.7% |

| Nelson City | 385 | 7.1% | 4.9% |

| Queenstown-Lakes District | 633 | 14.5% | 4.6% |

| Dunedin City | 404 | 1.1% | 5.5% |

| Invercargill City | 265 | 5.8% | 3.1% |

| New Zealand | 456 | 5.5% | 4.1% |

| Based on bonds received by Tenancy Services - MBIE | |||

149 Comments

These rent rises are just the calm before the storm. And can one of you DGM geniuses please explain to me why rents are going up faster than inflation if there is supposedly a massive oversupply?

There is no oversupply where I live (Rotorua). If there was a massive oversupply why are there so many being housed in temporary accommodation?

I agree, there is a shortage, which is why rents are increasing faster that inflation. If supply exceeded demand, prices would be falling.

I get daily emails from trademe of all new rental listings in both Auckland and Hamilton to see what's happening in areas where we invest. One thing that's clear, there are very few new rental listings coming up. Rents will keep rising above inflation definitely.

30/1/18 Trademe had 412 rentals listed for Hamilton. Today 31/1/19 there are 411. So what data are you using??

Factor in the hundreds of new builds going up which will not sell, then we have a flood of rentals arriving - not to mention the infill housing.

For sales were 699 verse today of 773.

Are you a geared up specuvestor by any chance?

Ignore me, i'll just be sitting here with my popcorn

You're very welcome pragmatist to watch from the comfort of your rental accom. Mind the crumbs to avoid any tenant vs landlord issues

Just amusing watching you specudebtors squirm when confronted with data. Dodge, weave, deflect, rinse and repeat eh?

See below for answer. Can you explain (without dodging) why rents on like for like are rising faster than inflation?

Inflation? Wrong measure to start with. You don't pay rent out of inflation, you pay it out of income.

And where is this like for like rental data you speak of?

Not dodging? There are examples everywhere in Hamilton and Auckland. The only place I've heard about with falling rents like for like is Christchurch. The pressures of life for a tenant, whether rent stress or landlord issues are never ending. Between being a homeowner or a tenant, I know which side of the fence I prefer.

"There are examples everywhere".. then show us. Like for like rental price comparison data. Lets see it.

Not your rental obviously, just don't move because that's usually when the sh*t hits the fan.

Conclusion: Like for like rental data only exists in Houseworks head, which is why he can't produce any.

Next move is likely to be into something we buy.

Pragmatist I am all for you finally buying your home, it will probably change your young perspective immensely. The other thing that will do that is starting a family. Literally the worst thing that can happen is trying to raise a family in a rental, we have tried that. Actually I am in favour of the KB concept, it's the execution and the smug minister that has to change.

Miles off as usual..

...not young haha, you better get cracking dude

Am neither geared up nor specuvestor, I watch what's in the market to stay informed. And from what I see the total number of rentals is falling. If you are correct and it FELL by one over the last 12 months when the city is growing strongly. And a large number are shared boarding house type accom quoted as "one" bedroom, that dont interest or suit a lot of potential tenants.

Growing strongly with overpriced houses. This is the problem. People will just keep crowding into houses, garages, caravan and streets. Demand doesn't mean price increases - it's the ability to pay that matters. And every indicator out there suggest most will have less cash in their pockets in future...not more....

The minimum wage recently went up, and is expected to go up again this year.

..at a much slower rate than everything else will.

Rastus it is cheaper paying a mortgage on a home than current rents for the same place so is that overpriced housing? The problem most tenants have is saving up for the deposit. It's better to forego discretionary spending in the short term to be better off in the long term

Houseworks, stop spreading untruth. In depth analysis has proven its presently cheaper to rent, it has been for a while; https://www.interest.co.nz/property/rent-or-buy

Milford investments also predicted falling house prices here; https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

"People have placed to much weight on supply and demand imbalance in Auckland. They say there's a shortage of houses so house prices can't fall – that's baloney."

Houseworks. BLSH, I challenge you to predict that as Auckland house prices continue falling, rents won't follow. Also, for once, backup your grave assumptions with some in depth analysis (links). Milford are in a position to know as where you and BLSH are obviously not.

26.8% of an after tax first home buyer income to pay rent, versus 27.3% to pay a mortgage.

So a 0.5% difference.....

...presuming you are factoring in rates, insurance and preventative maintenance costs, just think of all that compounding interest adding to the principal sum that the first time buyer will never have to pay interest on.

It's better to willingly receive it than it is to unwillingly give it.

With the back drop of falling house prices, it's highly profitable for the first time buyers to wait and watch.

Yes, the article factors in rates, insurance and maintenance.

In October two years fixed mortgage rate of 4.47% and a lower‐quartile house price of $390,000 will require a weekly mortgage payment of $367.77. This is up from last month’s $357.85 and up from the $350.59 that was required the same month last year.

In addition to the mortgage payment, this analysis also includes the household costs of rates, insurance and maintenance, amounting to $70.38 per week.

This is equivalent of 27.3% of the after‐tax income of a first buyer household income. This is up from last year’s 26.8%.

Good question Anaconda. The reason of course is a question the media will never ask the 'tenant' telling their story to the world. Go talk to some landlords out there and you'll get the idea as to why they are homeless. Track record and history being the hint.

Change in price bracket at which 'investors' purchase property, pushes up average rents.

That's one thing that has been proven entirely wrong since QE started. Property prices are based on debt expansion, rents move far closer to incomes.

"Averages of new bonds lodged"

If you wanna use broad averages, compare them to broad averages.

Reference rents to household income, not CPI.

Household income increased 41% for the 10 years to June 2018. Annualised, that's around 3.8%. - Stats NZ (2018)

I think the truth is somewhere in between. There is a housing shortage, specially in bigger cities. But at the same time "effective demand" for property is low given that the price of houses relative to annual income is seriously out of wack (again especially in bigger places). So there is "over supply" at current expected price range for more expensive properties. So either prices have to fall to where people can afford it or more cheap houses are built (smaller, with little or no land etc) at price ranges seriously less than what is currently in the market.

Low rents and high prices are a classic real estate bubble symptom. The fact that rents are rising while prices are flat suggests it may be changing.

It's not doom or gloom to see all the neon flashing warning signs of a bubble.

Who said there is an oversupply? There's clearly an undersupply, The question is how much (I think less than the conventional wisdom suggests)

It's not a simple relationship. Auckland has had an undersupply for many years, yet for several years rents didn't increase much at all

No increase from me, hard to find and keep good tenant nowadays.

That's because renters are generally low IQ, hence they are renting.

So almost 50 percent of the New Zealand population is low IQ?

Yes Cowpat thats how it works. The average IQ is 100 so you would expect 50% the population to be below this. Pretty harsh in a world that everyone gets a hospital pass these days, there are no fails anymore.This would only apply to those renting long term. Anyone getting ahead buys a house.

Unfortunately that's not how it works. Low IQ is defined as 70 or below. Yes 50% should be bellow 100 IQ but the majority of the population sit between 85 and 115, ~70%.

Out of curiosity, Carlos, what is your profession?

Retired at age 48. Electronics related industries most of my life. IQ score of 125 on a reputable test that was used on me at a job interview so no pressure. Of course anyone with a brain knows that IQ is not everything, "unfortunately" I think a little different to most people.

Good for you.

I'll let the rest of the commentors decide whether your IQ test score is legit.

For reference, it implies that you are smarter than ~95% of the population.

I remember Keynes did too.

Not Carlos, though.

He has a very high, nice round number IQ, tested at his workplace. He knows how to beat the system.

I would think that an IQ of 125 was normal for interest.co commentators. It's not "very high" and about right for technical workers and Nazi party officials.

Not too high, not too average. You would generally start bragging if you scored over 130. People like scarfie but then obvious personality disorders and maladjustments start to reveal themselves

An IQ of 125 is higher than approximately 95% of the population, ZS.

So yes, it is regarded relatively high and nowhere near average - average is 100, remember.

So Australians have an average IQ higher than that of New Zealander's ?

They don't let in as many low IQ individuals

Skudiv - whats your take on the difference between intelligence and wisdom?

Having a high IQ is no guarantee of wisdom but it is an essential factor.

Not really. Our tenants are a bright young couple. The girl is a junior lawyer and the guy is a young professional. I'm pretty sure they are working torwards their firsrt home. The couple we had before them were also junior lawyers. They moved out after they secured their own house.

Don't mess around with lawyer as tenant - they will take you to the cleaner

I assume this heat wave has caused the trolls to come out from their bridges. When saving a deposit which is 1.5x to 2x the yearly income one must rent. Unless they have been given a loan from the bank of mum and dad then use that loan to get another loan. Do you expect them to live on the streets during this time to save those extra few dollars or should they rent?

Or does that comment just show how low your IQ is?

Yes, smart to be renting while saving a sizeable deposit if possible, and not buying until affordability improves, which it will. Like Australia, we’re in a bubble. Fear of Missing Out will end.

I think we'll find that FOMO will result in FML.....LOL...

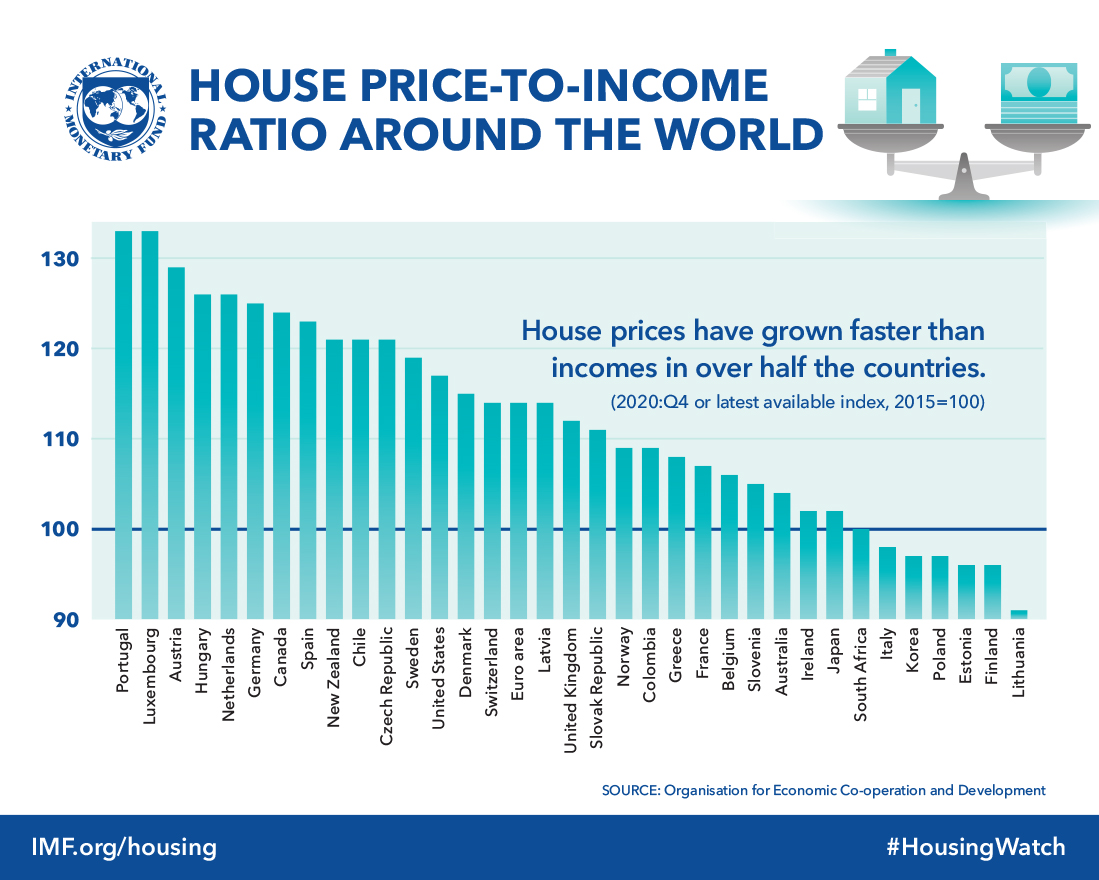

Or just too intelligent to buy into the most expensive housing market in the world relative to income.

https://www.imf.org/external/research/housing/images/pricetoincome_lg.j…

{kind=link}

You mean most expensive relative to income out of those 32 countries.

Jut another excuse for doing nothing as if there weren't enough of them already, those metrics have been like that for many years but the fact remains that if you had bought 10 years ago you would be much better off today, or if you buy today you will be much better off in 10 years.

False logic here - doing something does not equal buying property. Buying houses is not the only show in town, although the easy leverage has made it an easy place to look for the unimaginative.

One might even say the unintelligent...

Umm u been 2 japan?

can't believe my eyes I'm reading this sort of shit

Shows how arrogant part of our society has become. They confuse intelligence with luck and benefit of timing. And greed with intelligence. Taking from others for one's own financial benefit isn't intelligent, its just self-centred behaviour based on a paradigm of greed.

Be interesting if they had this argument with someone like, say the Dalai Lama. It would be argued that he is stupid because he isn't into taking from others for their own benefit - yet he is highly intelligent.

Yeah I'm pretty sure even Dalai Lama would say renting is worse than buying. Your brain is misfiring if you think that buying a house means taking from others, and renting is somehow more virtuous.

Going to an auction and out bidding a young couple who also wanted to buy? Or landlord/speculator demand on the market raises prices significantly meaning younger generations now take on a mountain of debt just to buy a house?

Just continue to act in greed by making as much money from houses that young people would like to buy and live in to raise families without the risk of a massive market crash due to excessive speculation, while at the same time dealing with significant mortgage stress....but landlords buying houses has no influence on the demand side of the market right?

What about the other side of the transaction, doesn't the seller then miss out if they don't get the highest bid? It may be a forced sale due to loss of job, injury, death, divorce. All your thinking is based around falling house prices, all of your thinking. It's insane, seriously. Everyone is buying and selling the same market, if someone can't afford it, that should motivate them to get a better job, make more money, save harder.

Oh yes the poor seller - why would it matter if houses prices are falling and they are buying into the same market? The house they sell, they get less for, but the need less to buy into the same market.

Its those that got left behind because of credit expansion the last 10-15 years - not their fault. Many in their 20's now who are looking at buying were at primary school when the current market distortion started. But no need to feel any compassion for them right? Its all about making as much capital gains as possible for those in their 40's, 50's and 60's?

That's garbage, and actually offensive.

There's plenty of financially successful people who aren't 'intellectually smart' (they are obviously financially smart), and vice versa

Haven't heard from our landlord except to arrange a time for the insulation guys to quote for the underfloor. Guess he wants us to stay.

It's a legal requirement for him to do it, isn't it?

Yes, but my point was not a thing has been said about rent increase, should've happened a couple of months age as our initial year was up and rolled over to periodic.

Well there goes most of the average wage earners annual 'salary adjustment' in recognition of their hard work and improved efficiency since they know your job better than a year ago now. What's left over for the rest of the weekly bills?

That rent would pay the interest on a 600k mortgage.

So the owner is just left to pay rates, insurance, maintenance and the principal out of their own pocket? Can't see how people can resist "investing" with a deal like that.

Yes, you’d know what a terrible investment property is. It’s not like you’re be hundreds of thousands in equity richer if you hadn’t exited the market permanently in the mid/early 2000s. Not to mention the fact that your interest and principal payments would now be way less than the rent you are currently paying.

You do realise that mortgage payments average out at 5-6% over the life of the loan, but rent increases at 3-4% every year. It’s not long until rent overtakes the mortgage and other ownership expenses, even if it doesn’t start out that way.

Yea, pragmatist.

Stupid you. You should have purchased in the mid/early 2000s like all the smart people. You'd be all good now.

Instead you chose to be a teenager.

.

Not quite, I'm a bit older than that.. instead I chose to go get an education instead of staying in a dead-end job, living a miserable life while enabling a family members self-destructive behaviour.

I don't regret selling, it was good move for me at the time, and enabled me to improve my life. Sure, i missed out a ton of capital gains, buy I also missed out on lots of negatives that were part of the bundle.

Creepo stalker up above sure seems to have a hard-on for me. He's not my type, my partner is a lovely person, and we will probably be buying sometime next year depending on where the market goes (I'll won't catch a falling knife if it turns to crap, which is getting more likely by the day IMO)

Pragmatist, yes, looking at what’s happening in Australia is a good indicator of what’s going to happen in NZ imo. Best to wait a little longer!

Don’t flatter yourself. I’m am however interested in you in the same way I’d be interested in a train wreck. Very sad, but can’t help not look.

So you are going to buy right before the crash? Or “steady decline” as you’ve said previously. Don’t do it. Why would you buy if values are going to go down? If that were the case it would obviously be better to rent, with yields below 4% in Auckland. On so many occasions you’ve gone on about how renting is so much more prudent than buying.

There are a few on this site claiming to have sold on the highs, and now waiting for the crash so they can buy back in again. It's hilarious that the crash never eventuates but they still think they did the right thing.

No train wreck here, my life is going just fine. Perhaps you should stick to minding your own business.

Yes, I’m sure. You don’t seem bitter at all. You just want to tax my recreational boat and steal my pension out of the kindness of your heart.

If you think your recreational boat will make a capital gain, the rest of your comments finally make sense.

Shows how much you know. I’m talking about the TOP Party’s wealth tax. They want to tax recreational boats based on the imaginary income you earn from them. Year after year until the tax paid exceededs the value of the boat.

The boat example was given by leader of TOP, Geoff Simmons, in an interview with Jenée Tibshraeny.

Oh, well next time I'll make sure I reference a policy from the legalise cannabis party to make sure I stay relevant.

Your pension? You haven't got one son.. you need to knock out a few kids to pay tax when you retire to fund your pension, they aren't pre-paid. Your kiwisaver is yours, do what the hell you want with that.

I’m paying for the pension of current retirees through my taxes, as well as contributions to the super fund. Unless KiwiSaver is made compulsory and I’m paid out what I’ve paid into the super fund and other people’s pensions, you and your plans to shaft your fellow kiwis get stuffed.

Unlike sickness or unemployment, retirement isn’t an unexpected event. Social welfare is a payment to cover unforeseen hardship. The pension is the pension, not social welfare.

Yes, the first sentence of your post is correct, everything after that is just your opinion.. not backed by reality. Want your money back that you've paid for your parents and grandparents pensions you better go beg them for it. Maybe there will be a pension when you get to 65 or 70 or whatever age it becomes, but I wouldn't count on it.

There is also the option of buying your own home, I suspect the reason home ownership is declining in NZ is because people are too stupid to do the math and rely on 'experts' like Shamobuel Eaquab when they say it's better to rent than buy. Or they have friends like RP and Prag who talk a lot of crap.

Why do you want people to buy into the market so much now skudiv? Is it because your want more demand side pressure to prevent prices from falling? No self interest?

Shamobuel Eaquab woke up one day and then he bought a house. Sooner or later you get sick of other people trying to control your life. One very positive aspect of home ownership that seldom gets a mention, your in control.

So because of that position, you'd be against landlord'ism because that competes with the rights/benefits you mention above?

It's not the repayments that tend to be the problem. It is the 20% Deposit that is the issue for most people.

Yeah it's hard to save money when there are now growing avocados the size of baby.

"Yeah it's hard to save money when there are now growing avocados the size of baby."

*they're; *babies

I wonder if renters know the difference between "there", "their", and "they're" and when to use a plural, given they have low IQs.

People in glass houses shouldn't throw stones. You squarely reside in a glass house, skudiv.

Actually I changed "there are now avocados the size of babies" to "they are now growing avocados the size of babies" but clearly didn't do a good job, or bother to proof read. It's not a fatal flaw and I could easily edit it, but I'll let it stand. Deciding to rent instead of buying, is a far more costly mistake and not so easy to correct.

People in glass houses need good Air-con. I do get fantastic sea views but without the AC on, the house turns into an oven.

Let's say you borrow 800k for an average Auckland house. 5% for simplicity. Interest alone is $800, then you've got to factor in depreciation of the building which is about $200 per week. Then factor in maintenance, $100 per week. Then factor in rates $100 per week. Then insurances etc. Cost of ownership is about $1200 per week if you're not expecting any growth in land values. That means you need about a $90k before tax income just to afford an average house.

It wouldn't pay the principal, though.

So...What's your point?

All renters should purchase a house on interest only loans right now (if they can even get them)?

That is just dumb, the point is obvious, the average rent would cover the interest on a 600k mortgage. You could take a 600k mortgage and just pay interest on it if you like?

Some people think they can't afford to buy, but renting is just going to make you poorer while making someone else richer.

I think you need to run the numbers again factoring all the costs of owning the property.

You have made a worst case scenario and pretend it is the baseline. It is always toughest in the first couple of years, the real advantage comes from owning a house for 10 years or more, which is why it takes a high IQ to be able to see that far into the future. In 10 years inflation would have eaten up a big chunk of the real value of the mortgage, which is a winner even without any capital gains, which you are sure to also have. You can back test throughout any timeframe, rent v mortgage repayments over a 10 year period, rent goes up with inflation while mortgage repayments are fixed and inflation reduces the amount of take home pay that goes on the mortgage.

Depends.

Kiwibuild house at $650k. $500k mortgage over 25 years @ 6% = $965,000 total paid plus $100k rates?.

Median rent of $550 per week, assume 2% p.a. increase over 25 years = $916,000 paid.

But, you'd be stupid to not increase your mortgage payment amounts over the course of the loan. Increasing the scheduled payment amount by just 2% every 2 years will bring the total paid on the mortgage down to $906k, and that's very bare minimum increases.

skudiv, generally I would agree with that, but with prices at 9 times income, which is historically way, way high in world terms (no, NZ is not different than the rest of the world), it's best to wait. With a 600k mortgage, you'll likely be sitting on some negative equity as the market falls, depending on how big your deposit was.

People have been saying exactly that for decades, and been dead wrong. Meanwhile those that worked hard, saved money bought a house, are now reaping the rewards. Rents are even less likely to fall than house prices, so you are guaranteed to lose money by renting.

Ever noticed we've just had decades of falling interest rates? I want to see houses continue to appreciate at the same rate over the coming decades while interest rates rise.

If interest rates rise, it means inflation is hot, inflation eats up your mortgage over time, while also pushing up rent. I know these concepts are difficult to grasp hence my original point.

Doesn't inflation mean the cost of everything goes up so people don't have extra $$$ to spend on things like mortgages, or is it assumed that our low wage economy will suddenly have big increases in salaries?

And what happens if you have no intention of becoming a darklord to rent isn't a factor? Ie. one house, one family type situation.

Generally inflation means incomes are rising, in fact that is often the cause of inflation.

"Generally inflation means incomes are rising"

Really?

Are incomes rising in Venezuela?

Did rising incomes cause inflation in the Weimar republic? Argentina? Zimbabwe?

If inflation was mainly caused by raising incomes, why don't we scrap the inflation targeting tools and just use wage guidance as the sole monetary tool?

The government in Venezuela is constantly raising the minimum wage, not as fast as inflation, but every few weeks the minimum wage is raised. Same goes for all those cases of hyperinflation, the government keeps raising the minimum wage, and pays all its workers in freshly printed million dollar bills.

I think you have cause and effect around the wrong way, skudiv.

The minimum wage is increasing so frequently as a result of hyperinflation. Not hyperinflation is the result of the frequent wage increases.

If you haven't noticed nymad, NZ housing price appreciation is NZ government and RB backed - no matter what happens, the government or RB will change the conditions so that house prices never fall.

Where did I say raising the minimum wage causes hyperinflation?

Okay. So what was your point, then?

What do you mean by 'hot'? That they are high, or that there is inflationary pressure / expected inflation is high?

Because if you think interest rates are high because measured inflation is high, you are categorically wrong.

Inflation doesn't push up rent. Rent (can) push(es) up inflation (CPI - I assume that's what you cryptically refer to here) levels.

It would seem you yourself is having a bit of trouble grasping these concepts, too.

Interest rates are used to control inflation, if inflation is high rates will rise if, inflation is low, there is no reason for rates to rise. You nee to understand the relationship between interest rates and inflation, it's not random. You don't have high interest rates, without high inflation.

Nope. My hunch was right; you don't know what you are talking about.

Perhaps you should have stayed in school and done 7th form Econ.

In NZ we have this wonderful thing called inflation targeting whereby the inflation rate sits at, ideally, around 2%. We use the interest rate mechanism to control this. The official interest rate will adjust based on expected inflation (not measured inflation) in order to maintain this target.

That means that measured inflation should be ~2%, while the interest rate can, in theory, be anything.

Sure if I had said inflation 'expectations' instead of simply inflation, you would have restated my point.

But you didn't.

And they are two very different and important concepts which you didn't differentiate.

As you stated it, you were categorically wrong. That's the point.

But you yourself didn't take out 30 year mortgages, did you?

I wonder how much of the rent rise is a like for like basis, and how much of it is the new builds being rented out at justifiably higher prices pushing the average up.

Very skewed by this.

Additionally also very biased by geographic distribution of rental properties in each area.

When you look at constant quality increases, they are markedly different to the broad averages.

Have you ever heard of Deepak Chopra?

Why?

Is your logic that if he can make a killing with alternative medicine, you can make a killing with alternative facts?

"The less you open your heart to others, the more your heart suffers."

Or the depreciation of existing rental stock.

Just reading the herald today with Milford AM reducing exposure to NZ Property predicting AKL to follow SYD and MEL, Bagrie saying the same but they don’t have as High IQ as Carlos67.

I would be VERY surprised if Auckland didn’t follow Sydney down (now down nearly -12% from peak), with the rest of NZ to follow in due course.

And mainstream property cheer-leading press printing it.

Like in Australia, the mainstream media will likely be largely optimist about the market until it's very obvious we're in for a big decline. FHbs will be encouraged to buy the dip, as it sinks 5%,10%. When FHbs stop buying and wait to see what happens, that's when the market will really tank. Notice how the banks are offering lower and lower rates to attract FHBs right now, to keep it going at current prices.

I just looked at the available rentals in my area of Hawkes Bay. The current selection is considerably higher at the high end than what was available when I rented. The rents appear to have increased by 10-20% in the last decade for a 3-4 bdrm "executive" home. The home value has increased considerably more than that. Just in the past two years, there has been at least a 30% increase in home values locally. In other words, the rent price increases are not keeping up with the home price increases.

I suspect strongly that more than a bit of the rent price "increases" are due to a change in the types of homes rented. Admittedly, it has been a couple years since I've seriously looked through the available rentals. In the past, I would be lucky to find just one home that I would consider renting. Today, there are at least a half dozen that I'd be happy to rent. I've never before seen so much high end rentals available here. I was very surprised to see the quality selection available.

I've just raised the rent on four of my HB rentals by an average of $40 week. I don't usually raise rents until I am in the process of re-letting with new tenants as I like to look after good tenants. Problem was our rents were falling so far behind we had to do a bit of catch up. We are still below comparable market rentals and all four tenants are staying on. All our properties are quality new or near new which attract the best tenants.

Lol my previous comment was deleted by the mods. Lets try again: rents can only go down with the current amount of vacant, mortgaged properties flooding the market in Auckland.

comments get deleted if you are rude or racist etc.

I referred to DFA as an alternative source.

guwop, try reading the article above, rents are going up, not down

Imho... Rents prices are governed mostly by demand, as long as we continue to import more renters than we have rooms for... prices will continue to rise.

As long as those renters aren’t construction boom workers who leave as the work starts to slow down, which is what happened in the Ireland and Spain busts.

Its assumed that we'll never have another recession and the credit expansion phase of the cycle will continue forever - creating jobs and inviting more people to come to NZ. This will never change...

Absolutely, and house prices never go down...

House prices are double every 7-10 years!

Timaru rents up almost 10% last year!

How many of those rentals are compliant with the Healthy Homes Act per 1 July 2019?

Zero. Because the healthy homes standards have yet to be published. We still don't know if we will need a heat pump in every bedroom for example.

The Property Bears on here are just so funny!

You missed the boat and can not afford or want to buy a house at the moment, we all get that!

Worrying about what the market is going to do is just a total waste of time and will get you no where financially!

Personally don’t care what anyone thinks about property investors not being very smart, intelligent or whatever, and they are supposed parasites etc.

Reality is that if we are pretty thick, then it clearly pays to be thick, rather than having all the brains and missing the boat financially!

The housing market in ChCh is as stable as ever, and even if the Auckland market does drop, it won’t flow on to the ChCh market.

Love being a non intelligent financial investor than an intelligent broke non investor!!

What boat did you catch TM2? It wasn't the one heading up a brown creek with no paddles was it?

I thought about jumping on the boat but the destination didn't seem clear, the boat didn't seem well repaired and the navigators appeared rather lost...

One of those punting boats on Christchurch’s Avon river with dead hookers and used needles discarded by skinheads.

NZdan, why on earth you go on about skinheads in ChCh is mystifying?

Haven’t seen them in CHCH in many many years, but then you obvious hang around in different circles to The Man!

As for your other mentioned, think it is in total bad taste and not worth commenting further on!

Everyone has the right to invest in what they desire, whether it be houses, shares, art, classic cars or whatever!

All I know is that property investment has made us extremely financial well off and a lifestyle that is envious of most on here!

If people don’t listen to The Man doesn’t affect me, but what I will say is that I have made people who have, far better off than they were!

Geez Man, you appear to see things so black & white..

For example I own a paid-for property but am renting for mobility reasons and cos I get bored easily. I wouldn't be suprised if my net worth is higher than yours. And I am at least 20 years younger than you. And way more diversified.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.