This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

Keynes famously pointed out that practical men and women are usually the slaves of defunct economists. Bear with me if I tease this out over economists’ theory of value. You’ll see from the many examples in this column that it matters.

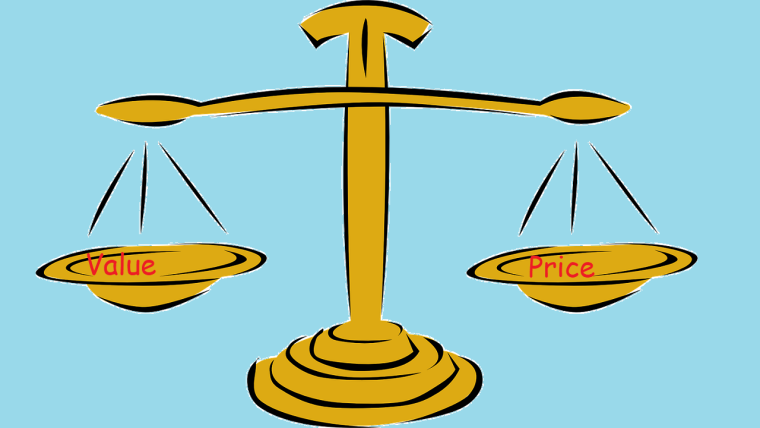

At an early stage in the development of economic theory – say beginning with Adam Smith – economists puzzled over the determinants of the prices of things. At one stage they made a distinction between ‘use value’ and ‘exchange value’. We don’t use those terms so much today but that is where the expression ‘the theory of value’ comes from. It would be better to describe it as the theory of price, but we are stuck with the historical phrase. I am going to use the current terminology comparing ‘objective value’ with ‘subjective value’.

The objective theory of value holds that the value of an object, good or service, is ‘intrinsic’, so that it can be assessed by objective measures. The labour theory of value (wage) – that the value of something reflects the amount of labour that is in it – developed by David Ricardo and used by Karl Marx in the nineteenth century, is the best-known example of this theory.

However, late in the nineteenth century, William Jevons (England), Carl Menger (Vienna) and Léon Walras (Lausanne, Switzerland) developed, almost in parallel, a subjective theory of value. Here an item’s value/price is not dependent on any inherent property of the good but on the consumers’ wants and needs. The modern subjective theory of value is the critical difference between classical economics and neoclassical economics and is the workhorse for most of today’s economists, underpinning their analysis of supply and demand. (Note that neoliberal economics is quite different from neoclassical economics, although it too is based is on the subjective theory of value.)

The subjective theory of value offers a solution to the classical economics puzzle of why diamonds are so much more expensive than water despite water being necessary for life. The key difference here is that water is plentiful and diamonds are rare. Because of the availability, one additional unit of diamonds exceeds the value/price of one additional unit of water, even though the total value of water to the community exceeds the total value of diamonds.

So, deep in an economist’s training is the idea that the price of something reflects the outcome of supply and demand and there is nothing special about it. For example, in various occasions in our history many economists thought the exchange rate should be devalued – and most of those who disagreed did so for technical reasons – rather than that there was an inherent value to the New Zealand currency compared to other currencies in the world.

Probably most of the population disagreed, thinking there was an inherent relativity. In the 1930s and long after, there was a view that the New Zealand Pound should equal the British Pound sterling. In 1933, one Minister of Finance even resigned when Cabinet overruled him.

Another example from the period is that histories of the Great Depression frequently mention that public sector wages were cut 10 percent by government fiat. They don’t mention that consumer prices had fallen by the same amount. The historians are thinking in terms of wages (the price of labour) having an inherent value; the economists are thinking in terms of supply and demand. Keynes pointed this out when he wrote about the downward stickiness of wages – the reluctance of workers to take nominal wage cuts.

You sometimes see demands for wage increases framed in terms of the belief that the workers involved should be paid what they are ‘worth’. It is an appeal to an intrinsic theory of value. In fact, most workers are worth (in a social sense) more than their pay, just as most water is worth more than the price you pay for it.

We get into the same muddle over housing. If I ask you what your house is worth, you will probably answer by giving your estimate of the price it should sell at. However, if the price of housing falls, you are likely to hang onto that old price. When house prices fell in 2009 as a part of the adjustment following the Global Financial Crisis, sellers said that they sold below what their house was worth. The same people were unlikely to mention that when they bought their new homes the price they paid was also lower than the ‘worth’ on the same criteria.

That is why I am more doubtful than many economists that the price of housing will fall markedly. They are applying supply and demand considerations; I think homeowners have an intrinsic assessment of their homes and will be as reluctant to cut the prices they sell them at, just as they would be reluctant to take a nominal wage cuts. Sure, there will be some distress selling; some will have to sell for various reasons such as they have to move or they can’t service the mortgage. But I am doubtful that will generally depress housing prices much.

That means that people who hope to purchase first homes will stillfind it a challenge; the likely fall of house prices will not be enough to correct the wealth imbalance from the house price boom. In an earlier column I argued that we had three broad housing problems: we have not built enough houses in the past decade (the supply problem); we have had a Minsky speculative boom in house prices; but that there wont be a Minsky bust because of attitudes to what homes are worth, so that it will remain difficult to purchase a first home. My bet that we shall see a lot of political activity trying to remedy the imbalance by way of assistance to first home buyers.

Do you think gold has an intrinsic worth? Many investors do which holds up the price of gold in a speculative bubble. The trick is to make a capital gain by flipping your holdings on to the next purchaser, who makes a capital loss on purchase, which they hope to recover (and more) when that flip it on to the next investor.

Speculating on bitcoins and the like is a similar gamble. Crytpocurrencies may have a role in future monetary systems as a mechanism for improving the medium of exchange, but that is not the same thing. If you want to gamble on bitcoin that is your thrill; the danger is – as for all gambling – if you borrow (or steal) to fund your recreational activity.

When you are looking at the various markets, supply and demand is a big help. But transactors are not as rational as the late nineteenth-century theory of subjective value assumed.

Exercise: Explain NFTs (non-fungible tokens) in terms of objective and subjective value.

Brian Easton, an independent scholar, is an economist, social statistician, public policy analyst and historian. He was the Listener economic columnist from 1978 to 2014. This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

27 Comments

Was housing in Ireland (or US, Spain..Japan) 100% over priced before their bubbles burst, or were they 50% discounted after the bubble burst? Ie what was the true value of housing during those periods? (Somewhere in between perhaps?)

Where were the rational buyers of value?

Enjoyed the article.

I'm more worried about the real, productive economy than I am the housing market. If people find that their jobs can't pay utility bills or buy groceries any more that's far more serious than finding out your house is nominally valued at a lower number than it was a month ago. Some perspective is needed on the inflation menace.

Exactly…but central bankers appear to have decided that protecting asset prices for the wealthy is more important that controlling inflation and allowing the poor to pay their bills.

The CPI measurement appears to only be useful if it supports that narrative of decreasing interest rates so that asset prices can go even higher.

When the shoe is on the other foot, they appear to want to ignore the data. Biased much?

Its always good to know who pays their salaries, might explain what they are saying.

I agree that people don't want to mentally re-value their properties to a lower number. Really, really don't want to -- will do anything to avoid it. But it's still possible that reality will intrude vigorously enough that they will be forced to.

As for NFTs: their objective value is close to nil. They represent an entry in a database, of no legal standing. They confer no intellectual property rights. They are largely hideous, as artworks. They are an example of pure subjective value - their value is as a luxury signalling good, indicating that the possessor is a forward-thinking individual who is sure to prosper in the coming golden age of crypto and Web3. Note that NFTs are a great demonstration of the difference between value and price; prices are largely set by wash-trading, where the same person sells it to themselves via a different wallet, in the hope of enticing a buyer by 'proving' the high market value of the NFT. So prices can be extremely high in a manipulated market, when the value is near zero.

They represent an entry in a database, of no legal standing. They confer no intellectual property rights.

Incorrect. NFTs are all about property rights.

NFTs don’t confer intellectual property rights. They confer ownership of an entry in a database which describes a specific instance of an infinitely replicable digital item. People only think it’s complicated because it’s so unbelievably stupid they assume they must be missing something. Nope, it’s that stupid.

NFTs don’t confer intellectual property rights. They confer ownership of an entry in a database which describes a specific instance of an infinitely replicable digital item. People only think it’s complicated because it’s so unbelievably stupid they assume they must be missing something. Nope, it’s that stupid

Incorrect. NFTs are based around smart contracts. If you buy a digital reproduction with no property rights, you've been scammed. That doesn't discredit what an NFT is.

If you buy the property rights to an artwork via *any* kind of contract, that’s a thing. The NFT adds no value to that contract that didn’t already exist; it’s equivalent to a receipt. And plenty of people are buying the receipt *without* getting the property rights, because of the mistaken idea that there’s some inherent value to NFTs.

If you buy the property rights to an artwork via *any* kind of contract, that’s a thing. The NFT adds no value to that contract that didn’t already exist; it’s equivalent to a receipt. And plenty of people are buying the receipt *without* getting the property rights, because of the mistaken idea that there’s some inherent value to NFTs.

OK. I'm not going to argue the point as to why a smart contract is a feature of an NFT and has 'inherent value.' What I will say is that you cannot argue doesn't have inherent value related to property rights. If an NFT is created with property rights, you cannot deny that.

In a world looking at depleting supplies of energy, an increasing amount of assumed-to-be-fungible tokenage will become non-fungible.

but that there wont be a Minsky bust because of attitudes to what homes are worth

This is going to slam head on into the buyer attitude of what homes are worth and ultimately it is the buyers that set the price. Most buyers in New Zealand seem to think not much further than the affordability of the weekly mortgage payment. With mortgage rates now skyrocketing and household budgets being eaten into by rampant inflation there could be some interesting times ahead.

I went for a drive through the overpriced developments at the back of Milldale and Orewa over the weekend. I wonder how the astronomical prices out there in woop woop are going to hold up in the face of $4 or $5 per litre petrol.

The test rate is about 7% for mortgages so RBNZ should have ample headroom to control inflation without causing a wave of defaults. The only caveat is that high inflation over a long period may reduce mortgage holders available income to service a loan which is why the Reserve Banks needs to act rapidly to prevent an inflationary spiral.

7% would trigger a wave of default-by-proxy, as in life would be so miserable for Kiwis trying to meet other exploding living costs that they just give up altogether. Just because you can make the payments doesn't mean your life will be worth living in any meaningful way.

This is US based, but if you look back over the past 60-70 years, when CPI went to 5% or more, which the US is above, the the effective funds rate had to go to approx 10% to tame the inflation.

{kind=link}

This time, we're well above 5% and no action from the Fed - effective funds rate is 0%. Interesting from this chart, you could also say that the effective funds rate actually leads inflation (i.e. raise rates and inflation gets worse periodically and its an almost 100% chance of causing a recession).

I get the feeling the Fed are walking a complete tightrope and what they do has the potentially to have a massive impact on NZ mortgage holders (and the global economy...)

All that I can conclude from this is that our central banks are responsible to creating massive debt/share/property bubbles, but if history is also true, they don't really care as they will raise rates if they have to, to control inflation. Arsonist and fireman all in one.

Yeah, I don't there's actually that much of risk of a large amount of defaults if interest rates hit 5-6%+, in the shorter term, assuming the economy remains a float.

However, I don't think the economy is going to stay afloat. As job losses and/or income loss mounts AND rates shoot higher, that's really when defaults will start arising at a significant rate.

Things are fine until the economy, business income, and jobs start tanking.

It really feels to me like we are on the precipice, but most people are oblivious to it.

Property developers seem to think the true value of their finished homes is what it cost plus their profit margin. The person buying it doesn’t give a damn what it cost, only what it’s worth to them.

Spot on.

Subjective seller expectations are high and steadfast currently due to past capital gains in house prices, essentially a doubling in price every 9 years or so.

But the reason for this is more than supply and demand, or perceived value, it is simply because the banks create money by lending against property, and with the M2 or M3 money supply increasing exponentially. In addition the CPI has been deliberately manipulated to drive interest rates lower.

Property prices are designed to keep increasing.

Until you reach a point, which we are currently nearing, where the price of a house makes no sense to anyone without existing capital. There is little prospect of further interest rate declines as CPI has been manipulated to drive them down towards zero, there is little opportunity to save a deposit for first home buyers, and government grants to them become increasingly meaningless. Then you have the money supply start to level off and then there is no reason for prices to rise, the money supply contracts and then money starts to become scarcer and so increases in value. Then property prices and money supply are in serious decline.

It's called a ponzi and is currently unraveling, we are about to see the mother of all crashes.

We will soon see the subjective valuation placed on houses by sellers and investors is nothing but utter foolishness. The emperor has no clothes.

On the money.

Good analysis. But remember that landlords own many houses. And many landlords are overleveraged and/or short term fixed and/or on interest only loans. So they will face much greater selling pressure than homeowners. They make up a significant percentage of the market. And price is set on the margins - it only takes a few forced sales when there are no buyers.

Not so sure about that. Drop the price sufficiently on a house and you will always get a buyer, unless of course you're in Kharkiv or Kyiv right now.

Sure, but all we need is for fewer buyers than sellers.

"Too few buyers" rather than "no buyers". The effect is the same.

Have you lived in a country and watched a property market when prices are tanking?

'You will always get a buyer' - perhaps...but in a falling market, buyers start waiting until they think the market has stopped dropping. And question on everyones mind becomes...'where's the bottom'? And nobody knows.

Many if not most landlords are baby boomers with low or no debt, so that wont necessarily be the part of the market that crashes. A growing number are now "cashing up" though, as they realise the market has peaked in this cycle. It can fall a long way before they lose any money. It will be the younger generation who may panic for the first time in their lives as they see their "cash cow"' beginning to fall in value.

In my 30 + years as a valuer, I know that is has more to do with sentiment than anything else, and sentiment has definately changed. I see it drifting downwards 1-2% a month this year, unless the current behaviour of Putin continues, which could result in a much bigger correction. Dont expect values to rise again for a couple of years at least.

Yes, it's almost like there are 2 completely different types of landlords.

There are the older, established ones you talk of. They have made huge capital gains and (if they aren't silly) have low debt.

But there is also a massive cohort of landlords who are highly leveraged. A lot are in debt from 7x right up to 9x income, according to RBNZ figures. A lot piled in when the LVR restrictions were removed. A very large chunk of them are on interest only loans.

Although it is hard to believe that so many people could have jumped in hollis bollis at the top of the market overleveraged to the hilt - they do exist, and there are a lot of them! As rates rise, they will be the marginal sellers. They will drag prices down for all.

For me objective/subjective perspective is kinda pointless when it comes to economics... I suspect its a mixture of things.

In regards to price vs value , surely one has to include the price/value of money itself.

We use money as a "measuring tool" ( unit of account) . The big problem here is that as a measuring unit it is not a constant ( think monetary inflation/deflation ).

Money printing profoundly alters the price of things, without altering the value of things.

eg. Brian thinks that it is speculators that hold up the price of gold. Another perspective is that it is money that is losing value when measured against gold ( in the same way we try to use the CPI to measure moneys value).

Golds intrinsic value , as a commodity, is related to its scarcity and cost of production.

Looking at modern money.... it has ZERO intrinsic value.

Without discussing Money Brians argument is kinda like splitting hairs ( objective vs subjective ), in my view.

Is economics mostly a subjective science or an objective science ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.