Three weeks ago, the Reserve Bank of Australia (RBA) raised the cash rate for the ninth time in a row to a decade-high 3.35%. There’s been much speculation since about the impact of the unrelenting rate increases on the economy. The early signs are mixed.

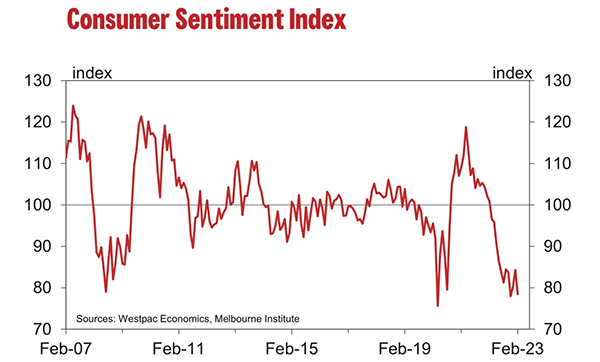

Last week, Westpac released the latest figures for its ‘Consumer Sentiment Index’. The index fell a massive 6.9% from January to February. The RBA’s most recent rate hike occurred in the middle of the week during which consumers were surveyed.

The heading says it all – ‘Consumer sentiment falls back into deep pessimism’.

The depths of that pessimism can be seen from a long-term graph of the index. It shows that over the last 16 years, confidence has only plumbed current depths during the global financial crisis and the early stages of the Covid pandemic.

The survey also asks respondents how their ‘family finances’ compare with a year earlier. The responses from those with a mortgage were ‘amongst the bleakest responses on this question in the history of the survey, which goes back to the mid-1970s’.

Westpac says that the survey provides ‘a very clear warning that the pressures bearing down on the consumer are becoming intense’ and concludes that ‘we expect an abrupt slowdown to show through in coming months.’

The degree of that slowdown will be influenced by the extent to which the RBA imposes further rate hikes. The minutes of the February board meeting of the RBA were published this week and they won’t give much comfort to borrowers. They reveal that the RBA considered an increase of 0.50% before settling on 0.25%, and record that ‘members agreed that further increases in interest rates are likely to be needed over the months ahead’.

In a small piece of good news for borrowers, the Wage Price Index released on Wednesday by the Australian Bureau of Statistics, revealed lower-than-expected wages growth in the December quarter. Annually wages rose 3.3% rather than the 3.5% forecast by most commentators.

That translates to less upward pressure on inflation, although by itself won’t prevent more rate increase.

The RBA is well aware of the adverse impact of its rate rises on many Australians. However, it views that as a lesser evil compared to the damage to the economy that would be caused by rampant inflation.

Speaking to a House of Representatives committee in parliament last week, the RBA governor Philip Lowe, acknowledged that ‘this is a challenging environment for many people’.

According to a report in the Australian Financial Review, the assistant governor of the RBA, Brad Jones, warned a Senate committee last week that about 8% of borrowers are in dangerous territory – ‘Virtually all their expenses are going on mortgage costs and general cost of living obligations, and they also have very little in the way of mortgage prepayment buffers.’

Clearly, many of these borrowers could be in trouble if the RBA raises rates by a further 0.50% or more over the coming months. Those whose mortgages shift from low fixed interest rates to much higher floating rates are likely to be in dire straits.

To date, there’s been little evidence of actual default among borrowers. In fact, the numbers from Australia’s biggest banks suggest that the vast majority of their customers are OK, and the banks are not predicting serious difficulties at least in the short term.

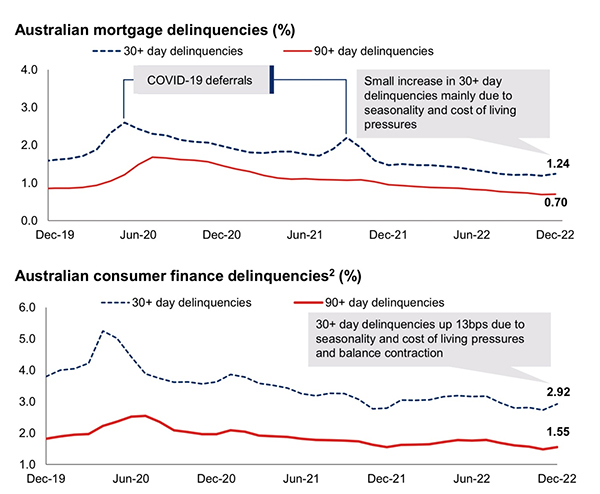

In its ‘Capital, Credit and Funding Update’ for the three months to the end of December, Westpac reported that ‘stressed assets’ were at 1.06% of ‘total committed exposure’, down one basis point from the previous period. 90+ day delinquencies on mortgages in Australia were at 0.70%, down 5 bps. (The corresponding figure for Westpac NZ was just 0.24%, up 2 bps.)

It’s interesting to consider Westpac’s Australian delinquency figures for mortgages and consumer finance over the last three years. They are at lower levels now than they were back in 2019 before the pandemic, a time when interest rates were lower than they are now.

Source: Westpac ‘Capital, Credit and Funding Update’

These graphs paint a reassuring picture. There has been a steady improvement since the worst of the pandemic and if there is a crunch coming, the bank is starting in a reasonable position. Peter King, the Westpac CEO, said this week that the key credit issue going forward is unemployment.

National Australia Bank’s ‘First Quarter Trading Update’ for the period to 31 December 2022 presented a similar picture. The ratio of 90+ days ‘impaired assets’ to gross ‘loans and acceptances’ was 0.62%, down 4 bps. The bank said that ‘continued strong employment conditions and healthy savings buffers mean most customers look well placed to manage through his period.’

Last week, Australia’s largest bank, CBA, announced its half year results to the end of December. It reported that ‘troubled and impaired assets’ as a percentage of total committed exposure dropped 2bps to 0.46%. The outlook from CEO Matt Comyn was cautious but sanguine -

We are conscious that many Australian households are feeling significant strain from rising interest rates, alongside the rising cost of electricity, groceries, and other household items. Despite this, consumer spend remains resilient with signs of spend slowing in pockets. The fundamentals of the economy remain solid, with low unemployment, strong exports, and returning migration.

The overall impression from Australia’s banks is that, for the moment at least, bad debts are not a significant problem, many customers have a good savings buffer, and most customers are up to date or ahead on their mortgages. Provided employment holds up, there’s no need to panic.

*Ross Stitt is a freelance writer with a PhD in political science. He is a New Zealander based in Sydney. His articles are part of our 'Understanding Australia' series.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.