Under the banner “Cut your excuses and sort your tax” Inland Revenue last Monday issued what it called a “last chance warning to the construction sector” to do the right thing and get on top of their tax obligations. The release advises that if people do the right thing, then Inland Revenue will help them. If they don't, Inland Revenue will find them and start follow up action.

Richard Philp, a spokesperson for Inland Revenue, commented;

“Most people and businesses in New Zealand pay tax in full and on time but there is a core group who don’t. … we also know that while some are struggling just to keep up with the everyday grind, others are actively avoiding their tax obligations.”

Tax evading tradies?

Apparently, tax debt is high in the construction sector and there's also a fair amount of cash jobs apparently happening in the sector. The Inland Revenue release commented that across all sectors, it gets about nearly 7,000 anonymous tip offs about cash jobs and the like each year noting “Construction is the industry most anonymously reported to Inland Revenue”.

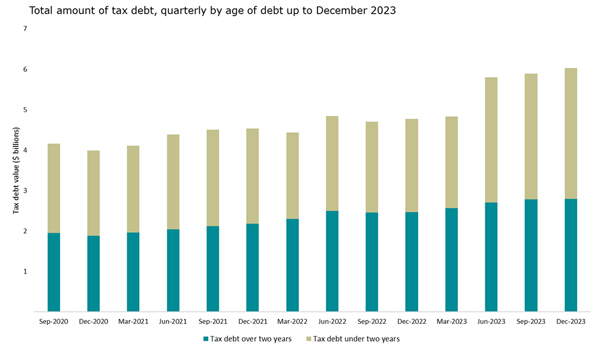

The media release is silent about the extent of the debt within the sector, but we do know from the latest statistics as of 31st December 2023, that tax debt over 2 years old has increased to from $2.5 billion in December 2022 to $2.8 billion in December 2023.

Understandably, with the Government’s books under pressure, Inland Revenue is keen to collect as much of this overdue debt as quickly as possible. This is probably the first of many such campaigns where we will see Inland Revenue taking additional action. And remember, under the Coalition agreement, additional resources have been promised to Inland Revenue for investigation work.

In this particular campaign, Inland Revenue is saying it's going to issue emails and letters to 40,000 taxpayers in the construction industry who have either outstanding tax debt or tax returns, or both. It then specifies that 2,500 of those will be contacted by text message, asking if they would like to support to get their outstanding tax sorted. There will be a follow up call if the taxpayers they respond that they do want help. Inland Revenue will also be carrying out site visits to key locations across the country.

As I said, this is likely to be the first of several initiatives we're going to see from Inland Revenue. I would be interested in seeing some specific stats around the proportion of debt and the composition of debt and get an understanding of what sort of businesses are struggling here. It will also be interesting to see how successful this campaign turns out to be.

More on the new GST rules for online marketplaces

Last week I discussed the confusion that has seems to have arisen following the introduction of new GST rules from 1st April. These rules affect people who are not GST registered but provide services through such apps as Airbnb, Bookabach and Uber.

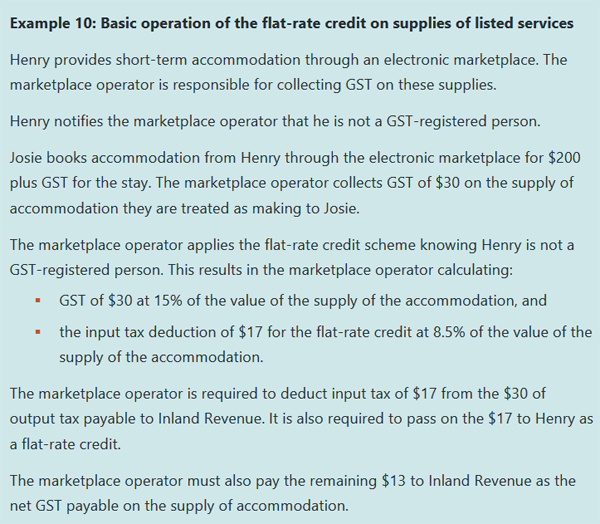

This week, Inland Revenue released three special reports relating to the new legislation and one of these is on accommodation and transportation services supplied through online marketplaces. In fact, this is an updated version of a report previously issued in June last year. The report has been updated to include the changes that took effect as of the start of this month and in particular how the flat-rate credit scheme operates.

Changes to online marketplace operators

Under the new rules, so-called online marketplace operators such as Airbnb, Uber and Bookabach will charge GST on all bookings made through them. However, the person who actually provides the ride or the accommodation may not be GST registered. This is where the flat-rate credit scheme comes into effect as the following example illustrates:

The full report is 68 pages so there’s plenty more to dive into.

Special report on 39% trustee rate

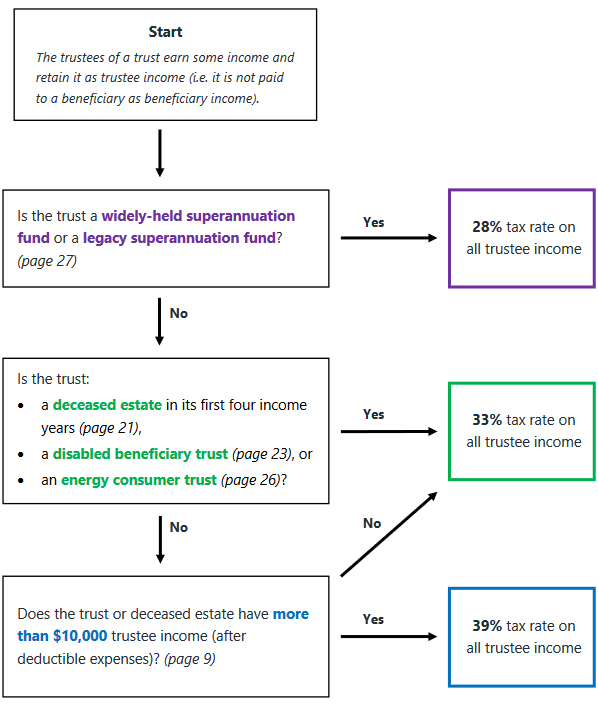

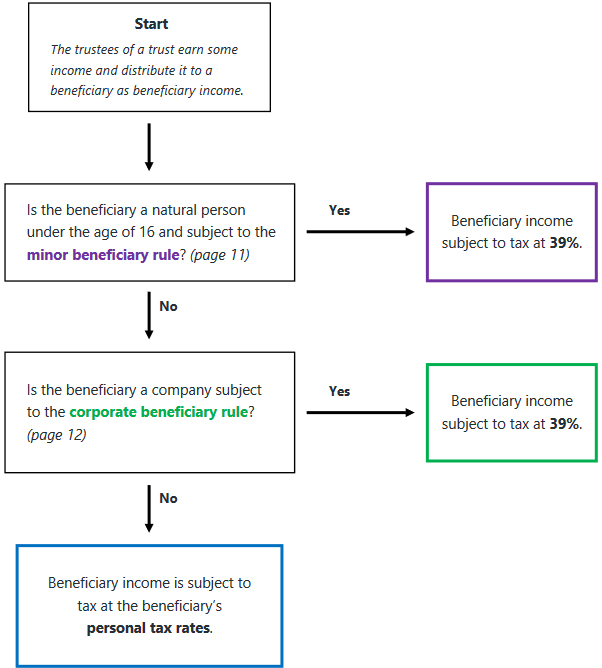

One of the other reports that was issued is on the application of the trustee rate of 39%. Basically, trustee income is the net income of the trust, which has not been distributed to beneficiaries. The 30-page report explains the basic provisions about “beneficiary income” and “trustee income” together with a couple of useful flow charts.

Trustee income flowchart

Beneficiary income flowchart

The report references the minor beneficiary rule which applies where the beneficiary is a natural person under the age of 16. In such a case only $1,000 of income per year can be distributed to that person as beneficiary income and be taxed at that person's marginal tax rate, presumably below 39%. Under the new rules, any beneficiary income in excess of $1,000 paid to a minor would be taxed at 39%.

Overall, this is useful guidance. Just remember the $10,000 threshold is all or nothing: if trustee income is $10,000 or less, the trustee tax rate that applies is 33%, but if it's $10,001 then it's 39% on everything.

The third report is on the proposed offshore gambling duty, which takes effect from 1st of July and will apply to online gambling provided by offshore operators to New Zealand residents.

The bright-line test and tax evasion - a couple of useful real-life case studies

Finally, this week a couple of interesting Technical Decision Summaries from Inland Revenue. Technical Decision Summaries are anonymized summaries of some interesting cases that Inland Revenue’s Tax Counsel Office has encountered either through tax disputes and investigations or applications for binding rulings.

The first one, TDS 24/06, is an application for a ruling regarding whether the bright-line test or section CB 14 of the Income Tax Act would apply. The facts are complicated but involve three sections of land currently owned by the ruling applicant.

The applicant had initially acquired one section outright before his spouse and another co-owner acquired interests as tenants in common. Over time, the applicants proportion of the ownership changed until at the time his spouse died the property was held 50% as tenants in common with his late spouse. The second section was owned 50% each as tenants in common with his late spouse. After her death her 50% interest had passed to him under her will. The third section was owned by the applicant and his late spouse as joint tenants. Following her death, her interest was automatically transmitted to him.

The ruling applicant was concerned about the treatment of future sales. Would the bright-line test apply or failing that, would section CB 14? This section is a little used provision and applies where there's been a disposal within 10 years of acquisition and during that time there’s been a 20% more increase in value of the land thanks to a change in zoning, or removal of restrictions.

The Tax Counsel Office concluded neither the bright-line test nor section CB 14 would apply. This is obviously a good result for the taxpayer but it’s actually also a good example, of how you can apply for a ruling to get Inland Revenue’s interpretation on a tax issue. You don't necessarily have to follow it, but if you don't, you better have good reasons for not doing so.

Fiddling the books and getting found out

On the other hand, TDS 24/07 involved suppressed cash sales, GST and income tax evasion and shortfall penalties. The taxpayer carried on a restaurant business which was registered for income tax and GST. Inland Revenue’s, Customer Compliance Services (CCS) investigated the company and formed the view that was fraudulent activity going on. There was suppression of cash sales, and the taxpayer was under returning GST and income tax.

CCS reassessed the taxpayer’s GST and income tax returns for the relevant periods and they increased the taxable revenue for suppressed cash sales based on analysis of point of sale data, the taxpayer’s bank statements and industry benchmarking.

Industry benchmarking – an underused tool?

Just on industry benchmarking, I think Inland Revenue ought to be much more public about its data here and warn taxpayers there are benchmarks against it will measure your business. It has done so in the past, but I think the combination of Business Transformation and then the pandemic interrupted progress in this space.

What people should remember Inland Revenue has some of the best data available anywhere about measuring industry benchmarking. I believe it should be making this much more public so that it it can serve as an early warning shot for businesses that think they can suppress income. Everyone loses when this happens. Gresham’s law about bad money driving out the good is very applicable here, because businesses which are not tax compliant are undercutting those businesses who are following the rule. This is not a healthy situation as it leads to considerable frustration, anger and if not dealt with, will just simply encourage more of the same behaviour.

Tax evasion? Have a 150% shortfall penalty

In this particular case, the taxpayer’s fraud was identified, and GST and income tax reassessments followed. In addition, Inland Revenue also imposed tax evasion shortfall penalties, which are 150% of the tax involved. These evasion shortfall penalties were reduced by 50% for previous good behaviour, but that's still represents a penalty of 75% of the tax and GST evaded.

Unsurprisingly, the taxpayer counter-filed a Notice of Proposed Adjustment under the formal dispute process, and the dispute ended up with the Adjudication Unit, which is run by the Tax Counsel Office as part of the formal dispute process. The Adjudication Unit did not accept the taxpayers counter arguments including an attempt to claim an income tax and GST input tax deduction for the cost of fresh produce purchased with cash. The problem was there was no supporting evidence for this claim, so the Adjudication Unit probably found it easy to reject it. The Adjudication Unit ruled not only was the tax due, but the penalties were also correctly imposed.

Get ready for more Inland Revenue action

Circling back to our first story, this TDS illustrates what lies ahead for those in the construction industry who have been suppressing income. As I said, I do think Inland Revenue should make everyone more aware of its benchmarking data which would be a warning for would be tax evaders. It's pretty clear from the announcement about the construction industry that Inland Revenue is gearing up for many campaigns targeting debt arrears and clamping down on tax evasion in particular industries. As always, we will keep you updated as to developments in those areas as they happen.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

18 Comments

Apparently, tax debt is high in the construction sector and there's also a fair amount of cash jobs apparently happening in the sector.

😲

I'm shocked, are you shocked? This is shocking.

I wonder how many BNB providers earn over 60,000 pa but have been doing it without being GST registered, and without paying income tax?

And then there are those who don't earn over $60,000 so aren't registered for GST, but might not have been paying any tax on the income over the years.

Now they'll all be visible to IRD, I assume. Could be interesting, and we could see a lot of conversions to long term lets instead. Not a bad thing.

"...I wonder...might not...could be..."

Good to see intellectual rigor, evidence & demonstrated facts in the comments. God knows where we'd be with suppositions, fantasies and unproven accusations.

Yet ironically Kate’s comment above still added more value and was better thought out than your own wonderful opinion here.

I think the percentage of BNB operators who earn anywhere near $60K/year from their BNB and pay no income tax on it is probably close to 0%. To earn that much it's not going to be from a spare bedroom in your house, it's going to be a dedicated property, and IRD already have information of such properties.

it's going to be a dedicated property, and IRD already have information of such properties.

What mechanism gives IRD that information on those properties?

1. Cross-check property title searches with home addresses of taxpayers and residential tenancy bonds, to eliminate OO homes and rentals.

2. Search properties on Airbnb, bachcare, bookabach, etc., and match them up with whatever wasn't eliminated in step 1.

3. Ask NZ banks to provide lists of accounts that receive substantial deposits from those same companies, and further crosscheck that with the above. (I don't know if they have the legal powers to do that, but it's theoretically possible).

In some tax jurisdictions, Airbnb will take care of calculating, collecting and remitting local occupancy tax on your behalf. Occupancy tax is calculated differently in every jurisdiction, and we’re moving as quickly as possible to extend this benefit to more hosts around the globe.

So Government introduces a Bnb tax and Air Bnb (hopefully) collect and remit on behalf of the hosts. Easy way to get this data.

Yes that part is clear. The discussion was about whether IRD were already able to collect that information before these changes. I suspect yes (but now it's even easier for them).

"Now they'll all be visible to IRD, I assume."

Terry? Will such people become visible to IRD?

This would mean the 'online marketplace operators' would need to provide information to IRD on their 'suppliers' where there is no direct tax angle. This would be overreach, would it not?

I hope Terry responds - as a girlfriend of mine said as part of setting up for this BNB GST change, her online marketplace operator wanted her IRD number. She is not GST registered.

Every tradie I know offers cashies. Usually weekend gigs. I don't know how you stop it without getting into people's personal bank accounts.

You get into people's personal bank accounts. Have each bank account linked to an IRD number, and the banks report the aggregate incoming deposits for each IRD number.

If someone has $150k of incoming funds against $15k of tax, then a please explain is generated. One off gift payments could be declared via IRD website. Might sound Orwellian but it would work.

Where IRD has sufficient reasons to do so, getting into people's bank accounts isn't much of a problem for them. While NZ Customs has almost unlimited investigative powers, IRD must be close behind. Further, 'cashies' may never see the tradie's personal bank account, or any bank account related to that tradie.

The problem for IRD is that people have multiple bank accounts, across multiple banks, both local and overseas, and the names (and other details, e.g. a PO Box) on the accounts frequently do not reflect the beneficial owner which may be 'hidden' through multiple tiers, and splits!, of ownership through non-natural persons (companies, trusts, etc.) that may exist in other jurisdictions. Further, the money can be laundered ("I won it at the casino") and the trail can be lost.

There are other less obvious, and more obvious ways, IRD get wind of cheats. One of the most common for tradies is where some outraged taxpayer dobbs them in. Being among the 'humble wealthy' allows many cheats to get away with it for quite a while - while the flash harries get found out pretty quickly.

"What people should remember Inland Revenue has some of the best data available anywhere about measuring industry benchmarking."

They certainly do! It should be published. And in much more detail. And for more business types.

And it should become mandatory reading for people who are about to enter a new area of business for the first time ... and/or want to know how well they're doing against their peers.

This would save NZ Inc. millions. And save many younger enthusiastic entrepreneurs consider heartache. And help NZ's woeful productivity.

Learning from your mistakes is part of life. But it is costly. A far better way is studying how others have done it and learning from them. And then refining their model to be well above the benchmark. This is 'good business'.

IMNSHO ... IRD is doing NZ Inc. a great disservice by not using and presenting this information to help NZ businesses.

100% with you on this one Terry! ... In fact, more like 1000% with you !!!

Does anyone remember the ads for me on Radio Hauraki by IRD in 2016 regarding tradies - "IRD is coming to get you."

I have been preaching to my clients get tidy now and that good old 7 year look back will be much less a problem.

In the later 90's IRD did the full length of Ponsonby Road on a Friday evening demanding to see employment records. Can you imagine some of the reactions.

More recently the Wellington taxi drivers got a blanket audit.

Great reads Terry keep them coming.

Great article. Good to see that the IRD will be ramping up this type of work. A couple of areas I would suggest:

1. With businesses increasingly moving to using "self-employed contractors" instead of "employees", one would expect to see a drop in real-time tax revenue (from PAYE type employees) but an increase in provisional tax payments (from self-employed) tax filings. Is the IRD seeing this and does it seem to add up? It seems that self-employment income is much easier to under report and an easy mark for tax avoiders. Am I wrong?

2. FIF tax. As a expat from the US, I not only file/pay tax in 2 countries but I also pay that a tax on "unrealised gains" for investment funds held overseas.....the New Zealand FIF tax. Most other expats I know seem blissfully unaware of this requirement and don't bother to declare it. Maybe the tax income stream from this source is not worth the effort to put in some checks and balances but it does seem like another area where it's easy to fly under the radar and avoid paying tax. Hope I am wrong.

I think IRD need to really emphasis how it is morally reprehensible for you to not to pay your tax. In effect you are gaining the benefits of taxes taxes without paying your fair share. In effect you are free riding.

I propose a new slogan. "Tradies pay your fair share, just like the property investors".

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.