A factor behind the government's push for a deposit protection regime appears to be because many New Zealanders believe their deposits are already protected against bank failure.

The work undertaken by the Treasury and Reserve Bank team leading the Government's review of the Reserve Bank of New Zealand Act included a survey of 1,000 New Zealanders on depositor protection. Bernard Hodgetts, director of the review team, says 66% of those surveyed believed their deposits were guaranteed. Thus they have an expectation taxpayers will cover any losses they experience.

This is not the first time such a survey has shown an expectation among New Zealanders that their bank deposits are guaranteed. A survey conducted for the Financial Markets Authority in 2014 showed 52% of respondents believing New Zealand bank term deposits come with a guarantee.

New Zealand did temporarily have deposit insurance through the hastily thrown together and flawed Crown Retail Deposit Guarantee Scheme. It ran for 38 months from October 2008 until the end of 2011 and cost taxpayers' the thick end of $1 billion largely due to the demise of South Canterbury Finance. This may be a factor for some of the confusion. (Also see Treasury's ambulance at the bottom of the Crown retail deposit guarantee scheme cliff wasn't good enough).

Of course not having a formal deposit protection regime doesn't necessarily mean the government wouldn't bail out a failing bank with taxpayers' money.

A consultation paper released as part of the RBNZ Act review notes "a limited understanding amongst survey participants of the status quo, with only a quarter aware that they stood to lose money in a bank failure."

"When the status quo and the various protection options were explained to survey participants, three-quarters supported introducing some form of depositor protection in New Zealand. Of those, two-thirds supported deposit insurance up to a guaranteed limit and one-third favoured a depositor preference. One in 10 survey participants wanted to keep the status quo," the consultation paper says.

The consultation paper argues that without a formal depositor protection scheme, depositors and investors in New Zealand banks face uncertain risks.

"This uncertainty was reflected in the survey of 1,000 New Zealanders, with only some survey participants realising they stood to lose money if their banks failed. Others thought that their deposit would be protected from loss, or that their bank would be protected from failure."

"If depositors (and other bank stakeholders) cannot predict what will happen to them (and their banks) in a failure event, they may struggle to identify and price their risk exposures. This may lead them to mismanage those risks, or misallocate their resources. A depositor protection scheme will make resolution processes and outcomes more predictable for everyone, allowing risks to be made more transparent and better managed," the consultation paper says.

"Depositor protection can give officials flexibility and independence to deal with a troubled bank using the most appropriate approach for that bank. Without a stand-alone depositor protection scheme, supervision or resolution officials (in New Zealand, the Reserve Bank) may be constrained or directed by the Government to use a particular recovery or resolution approach to get an acceptable result for depositors."

'An important issue for New Zealanders'

Last Monday Finance Minister Grant Robertson said Cabinet had made an in-principle decision to introduce a deposit protection regime in phase two of the RBNZ Act review. The proposal calls for the regime to include a depositor insurance limit of between $30,000 and $50,000, which Robertson said would cover 90% of individual bank depositors and 40% of funds in bank deposits in New Zealand. Hodgetts said the review team had recommended a depositor protection scheme to the government. The regime would cover deposits issued by banks, and non-bank deposit takers such as credit unions, building societies and finance companies.

The consultation paper says the RBNZ Act review process to date has shown depositor protection to be an important issue for New Zealanders, with a significant majority of New Zealanders thinking depositors in failing banks should be better protected. Of 67 written submissions received, 49 addressed depositor protection with about 80% favouring strengthening depositor protection in some way, the consultation paper says.

Out of the 67 submissions, 32 were in favour of a formal depositor protection scheme. They represented a "broad cross-section of New Zealanders," the consultation paper says, ranging from members of the general public to three of the country's big five banks. However, submitters who didn't support a depositor protection regime included non-bank deposit takers, non-financial corporates, and two of the country's big five banks.

"They either were opposed to special protections for depositors in-principle, or thought that - given the safety and soundness of New Zealand's banking sector - the benefits of developing formal procedures to protect depositors in a bank failure event did not justify the costs," the consultation papers says.

'Material' costs to banks and their customers

In terms of the costs, the consultation paper says a depositor protection scheme will have the upfront costs of establishing a deposit insurer, plus ongoing operational costs. It suggests a depositor protection scheme is likely to come at "a material cost" to member banks and their customers, especially during the build-up stage post-establishment or if the scheme is drawn on. Additionally it could have implications for supervisory intensity and costs.

"However, the international consensus is that this is an appropriate redistribution of the costs of bank failure that will ultimately reduce the burden on taxpayers."

The consultation paper says deposit insurance schemes are normally funded by levies on member banks, supported by a temporary funding backstop from the Government.

"Banking sector levies build the insurance scheme to a ‘target size’ that is proportional to the expected exposure of the scheme. Extraordinary levies are also used following a pay-out to rebuild the scheme back to target and repay the Government for any temporary funding. With low probabilities of bank failure (thanks to other safety net elements such as strong regulations) and access to government liquidity, the target fund size for a New Zealand insurance scheme is likely to be far smaller than the value of the deposits that the scheme insures."

"This also reflects that it is not expected that all banks will fail at once, and there are certain ‘systemic’ banks which would be resolved in a way that made the banks’ assets immediately available to depositors (unlike a lengthy liquidation process), reducing the burden on the insurance fund," the consultation paper says.

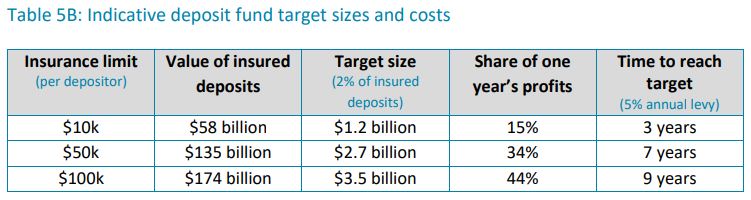

"Looking at countries with banking systems and per capita GDP similar to New Zealand, a target size for a domestic insurance scheme of 2% of insured deposits would be large. At a per-depositor insurance limit of $30,000-$50,000, this implies an insurance fund of around $2 billion to $3 billion (see Table 5B below). The Review Team estimates this could be built up over a decade through a levy of 5% of the banking sector’s annual profits, or a premium of 20 basis points on banks’ insured deposits."

"A depositor preference might also increase funding costs for New Zealand’s banks as risks are shifted away from depositors onto wholesale investors; the Review Team estimates that bank bond yields could be 10-30 basis points higher than current levels. Any increase in banks’ funding or operating costs under a depositor protection regime might be passed on to bank customers through higher mortgage rates or lower term deposit rates, or might result in a lower supply of credit to the real economy. This could adversely affect investment and economic activity in New Zealand," the consultation paper says.

"Alternatively, the costs of pre-funding a deposit insurance scheme might be partly absorbed by banks’ own margins and retained earnings. The extent to which costs are distributed between banks (as lower profits) and their customers (as higher borrowing rates) depends on competition and contestability in the banking sector."

The Reserve Bank's controversial bank failure tool, its Open Bank Resolution Policy (OBR), is not being reviewed. Hodgetts describes the relationship between depositor protection and OBR as "symbiotic." The introduction of a depositor protection regime would give authorities more breathing space to resolve a failing institution, he says. Thus introducing a deposit protection regime would enhance the potential use of OBR, should it ever be needed, Hodgetts adds.

The review team is seeking submissions by 5pm on Friday, August 16.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

16 Comments

There is an alternative. Significantly higher capital requirements and no off balance sheet debt.

or RBNZ plants inside the banks ala what the USA did straight after the GFC

And introduce a law stating that customer deposits may not be used for bail in or bail out.... easy!

Exactly.... get those risky off balance sheet derivatives back onto the balance sheet!

AND Then look at the Capital requirements of the Trading Banks. It would show the true picture and i'll bet it would not look pretty

I fall in the 10% outside of $50,000. Would be taking a huge haircut, much more than OBR. Effectively subsidising those with 50k or less. I'm happy with OBR. Not enough banks in NZ to spread my deposits around. Looks like I'll have to go into bricks and mortar outside of the house I live in.

Or hold treasuries in your own name.

It's hard to imagine where they will put all these 'premiums' that won't

- Be at massive risk of shrinkage at times when things are so poor banks are failing or

- Be eaten by compounding inflation

But catching a margin on every bank return in the country, against a backdrop of reduced risk from newly capitalised banks, is a great new revenue stream. Imagine we will lend it to ourselves as Infrastructure bonds, to pay for our Infrastucture debt (or find some other way of spending it now.....)

So you deposit your hard earned money into a bank, and you accept that you will be rewarded with an embarrassing low-interest rate for this money, and then you standby and watch this bank lend "your money" out to people with a maximum of 20% deposit, who want to buy a property that is 50% overvalued. What!!!!!! How is there not panic withdrawing of deposits from the banks already?

There can never be deposit protection from this madness... NEVER.

Governments are very good at introducing legislation that have us look in one direction, while they look in the opposite direction.

The work undertaken by the Treasury and Reserve Bank team leading the Government's review of the Reserve Bank of New Zealand Act included a survey of 1,000 New Zealanders on depositor protection. Bernard Hodgetts, director of the review team, says 66% of those surveyed believed their deposits were guaranteed. Thus they have an expectation taxpayers will cover any losses they experience.

Would have beeen good to ask the following questions in the survey:

1. Is the ratio of NZ banks' Tier 1 capital to lending approx 12%? (Y/N/Don't know)

2. Do you believe that house prices double every 7-10 years? (Y/N/Don't know)

"NZ house prices double every 7-10 years" - over what time period? 25 years? Or 85 years, which would encompass a full 4 cycles.

Several comments;

I would prefer that any deposit protection scheme return money to the depositor not the bank, and that the bank be allowed to fail. while I do understand the importance of the banks to our economy, no one bank is the only one operating and the others can pick up any slack, and likely make some money when one fails. Fundamentally the principle behind this is that banks are undertaking risky practices while not having to bear that risk. They instead, with some justification, expect tax payers to bail them out if they get it wrong. This is wrong! No business that is not Government owned should have the right to expect the tax payer to bail them out.

"a depositor protection scheme will have the upfront costs of establishing a deposit insurer, plus ongoing operational costs." This reads like the cover will be provided by someone other than the tax payer, but also as above, I feel that any payout should have to be made to the depositor not the bank, and the depositor can then decide where it is placed.

Finally if banks chose to pass these costs on to their investors and depositors, then surely would they not see those very customers head for the door? One of the traps here of course is how hard is it to operate without a bank account? It has long been acknowledged that the banks biggest costs are around those with the least amount of funds in their accounts. Further legislation may be required to protect people from predatory practices and charges in the name of rapacious shareholders.

Firstly has it been forgotten that the very same, and now very vocal, ANZ not so long ago was caught out in a subject, that is akin to this issue, that was downright lax. Secondly the best return on capital for any investor, is the return of that capital. Would think that most investors would be inclined to meet an extra cost, if indeed that is in fact justified and/or eventuates, if it means their hard saved funds are safely invested. Or are the banks simply saying that the cost will be born by borrowers?

Derivative ban?

Great NZ public evidently clueless.

NZ government should simply pay the customers of any failing bank whatever their loss is, when the bank is allowed to fail. Directly, not via bank being saved.

Alternatively of course, the State, as in China (which everyone thinks is a marvellous safe place for finance ....) should be responsible for printing money and controlling its circulation rate.

Banks attitude to proposals re their capital s simply making alternatives to their stewardship over money production look more alluring. Had it all their own way for far too long.

250K deposit insurance just across the ditch in Australia

Why are kiwis waiting Jacinda ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.