By Gareth Vaughan

Why do banks love housing so much? Is this good for the overall economy? And if not what, if anything, could be done to change things?

We address these questions in the latest episode of interest.co.nz's Of Interest Podcast with Martien Lubberink, Associate Professor at Victoria University’s School of Accounting and Commercial Law. Lubberink has previously worked for the Dutch central bank and contributed to the development of bank regulatory capital and disclosure standards both in Europe and globally.

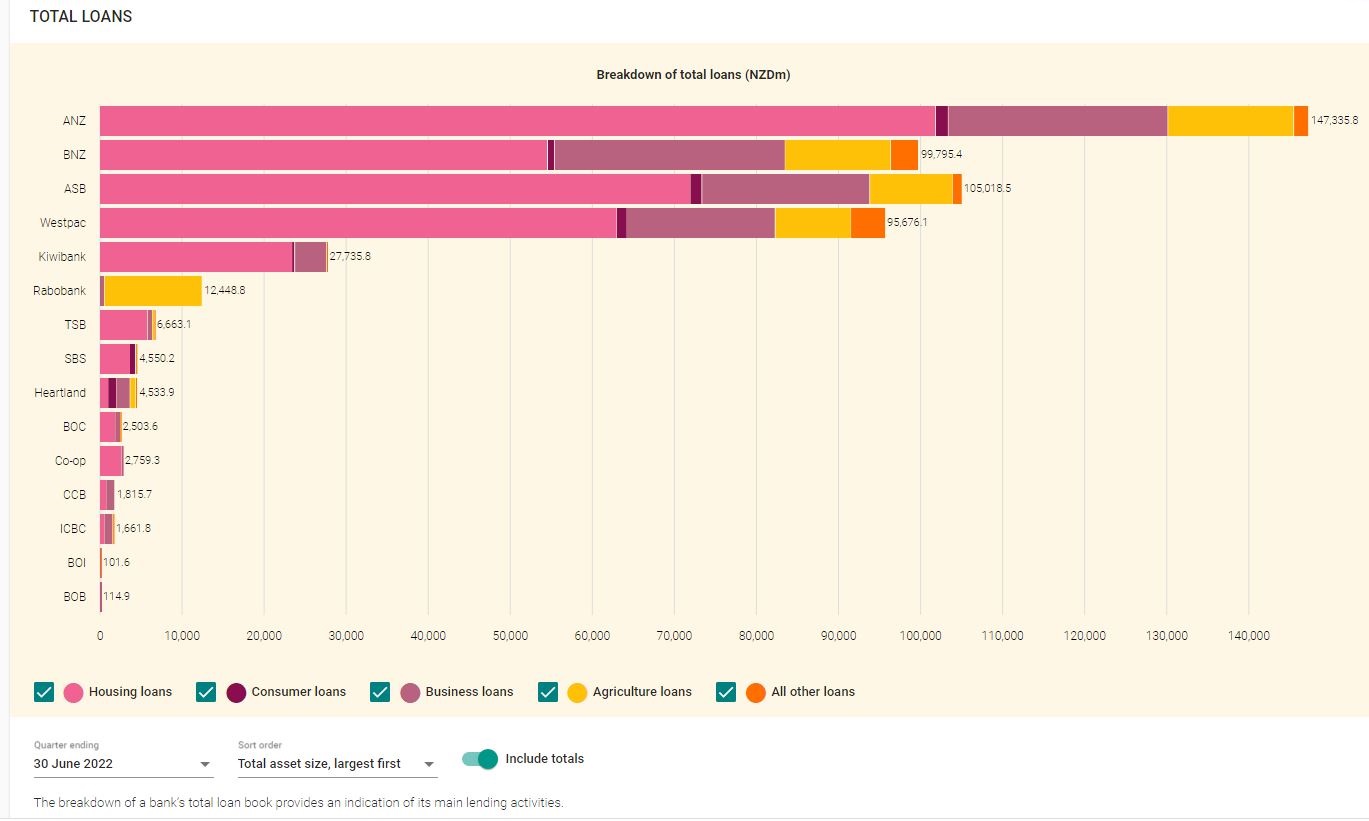

New Zealand banks do the majority of their lending to people buying houses. ANZ NZ, the country's biggest bank, has $104 billion of housing lending, which is 71% of its total lending. It's a similar story at the other major banks. At ASB 69% of total lending is housing lending. At Westpac NZ it's 66%, at Kiwibank it's 84% and at BNZ it's 55%.

In the podcast we discuss how and why bank regulatory capital settings incentivise housing lending, how the political economy favours home owners, the potential of so-called fintech financial service providers to boost borrowing opportunities for small businesses, or SMEs, and more.

"We are very much focused on lending to residential real estate, our homes. We've got no capital gains tax, everything's geared up to supporting the home owners. And that is because we vote for that, we want that. We are not explicitly voting for SMEs, and SMEs themselves are fragmented, poorly organised. So they can not stand up against powerful politicians, [the] powerful interests of other parties. SMEs are in a way the wallflower of our economy and that's kind of detrimental because a lot of growth and great ideas will come from that sector," Lubberink says.

"The banking system in itself is not a problem, it's more the way that the lending is organised. And that's more like a political deal made between voters who want their homes. In fact these homes are subsidised because there's almost no risk attached to them. If something goes wrong owners will be bailed out or banks will be bailed out. That's the world we live in, which I think is very hard to change."

"There is a bit of a trade-off. The banking system is safe. On the other hand the big problem still is the very large exposure to a single asset class [housing]. If something goes wrong in that single asset class it goes wrong very quickly," Lubberink says.

*The chart below comes from the Reserve Bank's Bank Financial Strength Dashboard.

65 Comments

Implement Dti. It would halt speculation on kiwis need for shelter, and hopefully force the banks become more sophisticated in business lending.

DTI has been given go ahead by government since long but Mr Orr is reluctant, hence delaying with hope of avoiding.

Falling market is the best time to introduce DTI.

A better question would be whether long term they increase or decrease individual home ownership.

Because the other alternative to it making any improvement is bulk home ownership by mega corp landlords.

Don't scoff at 'bulk home ownership by mega corp landlords'. Corporate build-to-rent landlords do not have the voting power of individual owners and mum'n'dad landlords, so unlike them corporate landlords can be tightly regulated by both central and local government, ensuring price-controlled secure lifetime tenancy in quality homes for renters.

We already have a form of this in the guise of state and council housing and she don't seem so flash long term. Maybe if it's private itll be better.

That sounds alot like a way to implement the World Economic Forums "You'll Own Nothing and be happy" thing.

That "thing" the WEF never said you mean?

https://www.reuters.com/article/uk-factcheck-wef-idUSKBN2AP2T0

any of this sound familiar:?

https://seekingalpha.com/article/4553122-housing-market-crash-be-worse-…?

Summary

- The number of privately-owned housing units under construction in the US is at an all-time high of more than 1.7 million as price declines accelerate.

- Who's going to buy all of these houses with mortgage rates of 7.3%? At current prices - people really can't, indicating the need for some serious price reductions.

- Housing demand is tanking while supply is about to soar. Real-time home prices are now falling at a faster rate than the 2008 housing crash.

- This could be one of the biggest housing crashes in history.

- The Fed waited too long to hike rates during the boom and now needs home prices lower, so the cavalry won't be there to rescue with rate cuts this time.

Interesting...

Just wondering what is " privately-owned housing units under construction " mean ? People who have paid initial fee , but waiting for completion ?

Or are you talking about private builders here ?

I had a feeling US housing market is relatively safer , as they have looong term Fixed mortgage rate, which is immune to inflation and interest rate hikes.

But you obviously explaining a different scenario.

Surely the massively over-riding influence is risk.

Exactly.

You want to end up with a house you can mortgagee sell if the borrower stops paying the money back, or end up with a business that makes no money that can have zero value, so risk losing all the $.

Land, housing is a hard asset that has intrinsic value that may fall a few % but never evaporate, unlike a business case that's often nothing more than a sales pitch with no real way to establish the real value until years worth of solid revenue is obtained.

{kind=link}

Exactly.

So yes in an ideal world NZ will be full of quality entrepreneurs with innovative and PROFITABLE businesses that allow banks to pump money into them.

Unfortunately, most businesses and start ups fail, there is no getting around this, it is inherently risky.

You suggest, based on an idealized world summarized by some academic, forcing banks to lend more to businesses and have their entire loan book be at much higher risk?

You can't do that as much as commie lefties would love to have that sort of control to fit their idealized world that doesn't exist in reality.

Increase risk = increase price/expected return.

The money is in the system, it falls where it may, and in a risk based real world economy that means good businesses then they left overs (which are large as good businesses that have very low risk are scarce) go into property, residential and commercial.

The money is in the system..

Banks don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source.

The money is in the system..

Thank you Audaxes. Keeping it real as usual.

Ok.

How about instead of "the money is in the system" we say the potential for bank credit expansion is large and banks are rewarded for creating credit but that credit must go to safe places, until the values get pumped to a limit, therefore making the once "safe places" i.e property no longer a safe place to pump this credit into.

So we get the boom bust cycles as he points out.

Japan and Germany have demographics that mean the "limit" for property prices gets hit then that's it - the limit/threshold never increases as people per unit land decreases.

In rapidly growing or long term positive population growth countries, aussie, Canada, NZ (once we get immigration pumping again) then the limit gets hit - and a consolidation period happens during which time that limit/threshold slowly creeps up as people per unit land increases - giving banks the opportunity in 5 years or so to once again pump credit into property until the new higher limit is reached.

I think professor Werner needs to deconstruct his 12 min presentation there to first principles so the idea of credit creation can be distinguished from increased money supply.

I'll need to do more reading on this.

Simon - most recent stats from Interest .co do not support you - May Bankruptcies 100 April Liquidation 5.

I have been in a situation where the bank wouldn't lend me money. Even though I had over 1m of unencumbered stock in my business, and all the fundamentals were positive. Banks are the knee cappers of business in this country.

We have been successfull in spite of banks.

1m of stock would get valued at cents on the dollar. Despite everyone's insistence their business is rock solid, the failure rates don't lie, so unfortunately everyone gets viewed fairly the same.

I'm not disagreeing that business lending is pants, but also that it is what it is for good reason.

Maybe. That was 6 years ago. Now we have triple that stock and have been in business for nearly 13 years. We also pay a lot of tax.

I still don't own a home, Therein lies the issue.

Yeah, for the aforementioned reasons, lending against inventory carries way higher risk than using a house, or business premises as leverage.

Obviously the longer you are trading (and trading well) will improve your profile.

Even 6 years ago there would've been some funding available, but it would've been on fairly bad terms.

What's sad is you've had to pay significant tax while we've collectively been giving property speculators a comparatively free ride. No wonder the economy is so distorted.

What's the bank going to do with your 1mill of stock? Open an "ANZ discount store" to recover some of their money?

Houses have 70% plus of buyers that just want a home (owner occupied) - while your customers might disappear, in 10 years time people will still need shelter.

And where do you suppose people get the money from to pay their mortgage? While businesses may seem to be a greater risk than property, their success has created all the mortgages which the banks have lent against. Try getting a loan if you dont have a job.

Getting a new job is almost infinitely easier and faster that creating a new business from the ashes of a failed one.

Correct.

Which is also why the idea of owner occupiers being lower risk and FHB getting helped into an overheated property market is wrong.

Tenants lose job - winz and gov cover rent.

Rental vacancy for 12 months + etc far less likely than a single job lose - esp if the investor is skilled and has 5+ so any single vacancy doesn't hurt mortgage repayments.

People will always need quality safe shelter, will they always need whatever you skill set is that earns you money?

Automation, banks closing physical stores, talk to robots on ph all the time, supermarkets self checkouts.

Simon - that's known as risk assessment.

A familiar story - Banks Bureacrats & Lawyers stuff more deals than anyone else. Greed is a close second place.

Those business debts are often with personal guarantees that have the owners house as collateral. Banks are seldom last in line for anything.

I personally wouldn't be buying up houses right now even if they were a few % cheaper than the market price. Might buy one to live in, but that's it.

We've been used to the mantra that houses can't fail for too long.

I think people are confusing mantras.

Housing is a statistically safer bet than many other forms of investment.

That doesn't mean houses are invulnerable.

Bank shareholder returns on regulatory bank capital required to lend against land and the improvements built on it are higher.

As a result of a combination of the “risk-weighted assets” system and the credit crisis, banks have basically withdrawn from the thing they were set up to do: facilitate commerce.

For the big four banks, only 16 per cent, on average, of a real estate mortgage is counted when measuring the bank’s capital ratio. This is rising to 25 per cent next year.

But every dollar of an unsecured personal and business loans counts against capital and in some cases the risk weighting is 150 per cent.

Capital — that is, the bank owners’ money — has to be 8 per cent of assets, although mostly it’s around 10 per cent. That is, the ratio of owners money to other peoples’ money has to be no greater than 12.5 to 1 and is usually 10 to 1. The result is that for every dollar of capital, the big four banks can choose to lend $62.50 secured against real estate or $10 unsecured.

Guess what happens? It’s only natural and totally understandable. It’s true that interest rates on personal and business loans can be three times what the banks make on residential mortgages, but that still doesn’t make up the revenue. Link

good read, I feel that DTIs should be introduced, but to achieve even a 6 AKL prices have to drop another 30-40%

Just give it a few more months...

It's going wrong now. The minsky bubble they engineered is reaching its inevitable conclusion.

Every market seems to be reaching this at varying timeframes and it's already been happening for 30-40 years in some territories.

It would seem like the US' endgame is to be last man standing as other large economies like Germany and Japan have fallen by the wayside as their populations and markets plateau. You can see this in how low interest rates have wildly varying effects.

They probably have a cycle or two left to keep the QE train a running.

And this time, the housing bust won’t take down the banks, as it did last time, because the banks no longer own the mortgages. The whole industry has changed. Most of the mortgages are securitized into mortgage-backed securities, by entities such as Fannie Mae and Freddie Mac, which are under government conservatorship, or by Ginnie Mae and the Veterans Administration, which are government agencies, and the government guarantees the mortgages. And these mortgage-backed securities are sold to investors such as pension funds, insurance companies, bond mutual funds, etc. around the globe.

If mortgage credit blows up, if there’s another huge wave of foreclosures, it won’t hit the banks; it’ll hit taxpayers mostly, and investors to a lesser extent.

But we’re not seeing any signs of credit blowing up yet. Mortgage defaults and foreclosures are just now creeping up from the record lows during the pandemic and remain lower than any time before the pandemic. So we’re far from that happening, and if and when it happens, it’ll hit taxpayers and investors, and not banks.

So the Fed, which is in charge of keeping the banking system from toppling, won’t have to bail out the housing market because it won’t take down the banks.

And if it wants to because inflation is still raging, the Fed can just let the housing bust rip. Link

Audaxes - you are right but the first cracks are car loan arrears - next Lehman Liar Loans???? Credit Suisse Evergande and Deutschebank looking shaky.

Brock speaks the truth. There is a point where housing at crazy high prices relative to income (and therefore Minsky moment excessive leverage) becomes as risky as lending to a business on a non recourse basis. A lack of acknowledgement of this in terms of regulatory capital requirements and banks own internal models, has skewed the pitch.

Once the NZ house prices drop the 30 to 60% that coming down the pipe, in the next few years, Whammo! the already agreed and stated plan of the DTI is locked into place. Just as Ireland did - "copy and paste" it.

The DTI should be at 3.5x your max debt to your annual income. Never again will we have destructive and runaway house prices distorting our economy and risking the financial Armegeddon that the big 4x banks are new exposed to the burning heat from! ....... like a newly arrived Scottish ginger on Northland beach, without suncreeen.......

Sounds like a good way for everyone to live in tenement housing.

Ireland just recently increased its DTI by 0.5. Orr has said he'd like to take the LVR's off as soon as circumstances permit. What is it with central bankers.

Ireland did some housing jiggering with mixed results, one of them being that rental housing has gone away - theres often less than 1000 properties available for rent, in the whole country. So now they're having to backpedal, dropping taxes for landlords, reducing capital gains taxes, improving lending conditions for owner occupiers, etc etc.

Just implementing a bunch of laws and taxes to nerf housing doesn't seem to be a panacea. Will get a party elected in the short term though.

But presumably all houses are occupied, so renters have become owners?

Perhaps the unwinding is more a resurrection of regulatory capture.

Society has been programmed over generations to believe that a mortgage is supposed to be a 30+ year line of credit, with zero need to prioritize repayments, and with the 'benefit' of it also providing an extended line of credit towards cars, holidays, renovations and just generally keeping up with the Joneses.

Borrow, borrow, borrow until you are so deep into a debt hole you will essentially be spending the rest of you life 'working' for the bank in the process of trying to deal with your debt.

This is exactly the illusion the banks want. Become enslaved to them. That's where those mega profits come from.

I'll let you in on a sad secret. Mortgage or no, most people are up for 40-50 years of work. You'd just likely have less stuff in the end if you tried to subsist off the fruit of your labour, because if people aren't tied to some sort of greater commitment, they usually end up blowing every penny on consumption (which is why you end up with mandatory superannuation in many places).

I guess some people who were super disciplined and didn't have a family or nothing might be able to work 15-20 years and then just chill.

Yes most people up for a lifetime of work. Some thought they were getting ahead by leveraging their house to live a fancy lifestyle but ended up working more for the stuff they had.

Without capital gains, it’s exponentially better to save and buy than to leverage debt for the things you want.

People may just have to learn to be happy to settle for less if they want to retire early. Or alternatively provide a valuable addition to society and get paid out.

”I have a home and so I deserve to live frivolously”, is daft.

Yea I do wonder if people know the true cost of extending your mortgage for consumables.

For the programmers here, mortgage debt is like a queue. First in first out. That is the first dollar you borrow is the first you pay back. You borrow more money for a boat against the house, it sits there at the bottom of your debt pile with compounding interest until you’ve paid the house back first.

Absolute dream for the bank.

You could think the same for those saving for a house. Every dollar you spend is a dollar sitting at the bottom of your debt pile until it’s all paid back.

Without capital gains, and I do hope DTI comes in to put a lid on speculation, having 30+ years of credit to live a fanciful life makes no sense. The value of owning your own home is reduced back down to simply having a roof over your head.

From then on, if you want that bach or boat or both, you’re going to have to learn to be productive for it. Going to be a significant mind shift in this country. For the better.

I think it would be better modelled as a stack.

The first dollar you borrow is the last you pay back.

In fact these homes are subsidised because there's almost no risk attached to them. If something goes wrong owners will be bailed out or banks will be bailed out. That's the world we live in, which I think is very hard to change."

Just like Taleb's turkey, whose sense of well-being and trust in the farmer reached its highest point on the day before the day before Thanksgiving.

🦃 "In fact, the farmer has my best interests at heart, and there is almost no risk from him. If something goes wrong the farmer will look after me. That's the turkey farm we live in which I think is very hard to change." 🍽

Didn't Christchurch teach us anything? Obviously not.

"If something goes wrong in that single asset class, it goes wrong very quickly" Exactly.

What happens when properties in a substantial part of Wellington and Palmerston North; together, get wiped out in an instant in the Big One; the one that we know will arrive at some stage?

If anything, Risk in New Zealand is more obvious than it might be elsewhere (Australia, say, with their random floods and fires).

New Zealand is literally sitting on the edge of a known disaster with the way it lends for that one solitary class, and one day, it will pay a price far higher than the one we are still paying for, for Christchurch.

Yes, scarily The Christchurch earthquakes will look like small fry one day when one of the Wellington faults rupture, or when the Alpine fault goes.

Kiwibank and TSB really high percentage of home lending, over 80%. Read recently where TSB has not ruled out takeover, but aware of their 'NZ' brand. A Kiwibank takeover over TSB would make good sense to both banks. Kiwibank gets more scale its after, and TSBs customers would likely be happy with an NZ takeover.

Kiwibank is already circling the drain.

Why? Because there is a ready market for houses - there is always someone out there prepared to buy. Banks know their customer can always sell if needed, the variable is price.

Homeowners turn to 35-year mortgages.

https://www.telegraph.co.uk/personal-banking/mortgages/homeowners-turn-…

It's inevitable that the same will happen here. Then we will move on towards 50 years mortgages, and beyond.

The longer the debt can be extended, the 'cheaper' it appears as an item on the household weekly bank statement.

The other aspect is initially mortgages were financed by one individuals' career.

Things are far different now.

Excellent podcast - love listening to people who actually know what they're talking about.

"If we take a mortgage, bank owners have to put x% and rest is contributed by depositors "

So he is saying NZ banks are just financial intermediaries? Credit creation theory is not true here??

From memory, he clarified what he meant immediately after this, to be clear that he didn't mean people's savings etc.

So he is saying NZ banks are just financial intermediaries? Credit creation theory is not true here??

He didn't explicitly describe this. I got the feeling Martien was suggesting that banks are intemediaries early on the podcast. But if you listen to it fully, he's objective without being emotionally critical in any way. He's more or less saying that the monetary system is very difficult to change in terms of lending for productive activity as opposed to hosuing.

Is our productivity an issue because of our propensity to invest in capital gains or does our high cost base prevent us from investing in productivity, therefore capital gains is the only direction?

Or is it simply that the gains since the introduction of neolib economics/capitalism, the selling of the NZ economy, have only flowed in one direction?

The monetary system is just a tool, how it functions and what it leads us to is ultimately created by our collective beliefs and fears, and those controlling the system. Unless these change nor will the monetary system.

Who can I vote for to have a capital gains tax introduced?

The country where people sell houses to each other at ever increasing prices and call it productivity.

In terms of pointless, its right up there with watching paint dry.

Its a glorified Ponzi scheme that won't end well.

When it does, hopefully we can get back to improving the world and the lives of others around us.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.