Home loan rates will likely rise soon. The key 2-year fixed home loan rate averages 6.93% among the five main banks, and is boosted somewhat by ASB's unusual 7.05% rate. But it seems unlikely that they will be left hanging up there for long. The one-year fixed rate average among these same banks is 7.23% and that may be where the two-year is headed. Interestingly, more recent borrowers are on the 1-year rate than the two year one.

And there are a large group of borrowers coming up for re-fixing who will be facing these new higher rates. A year ago the one year fixed rate was 5.11%. Two years ago the 2-year fixed rate average was 2.51%. In late 2023, both groups face sticker-shock.

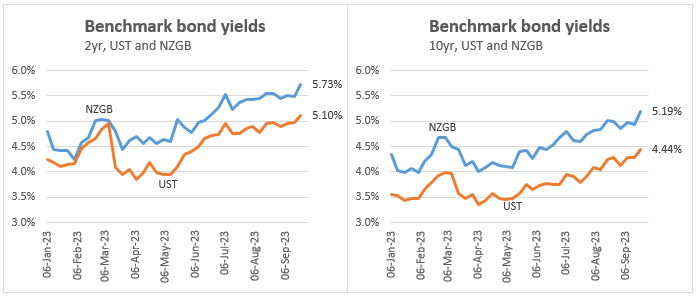

Benchmark rates are high and rising

The current rates are now their highest since the GFC. And wholesale markets now have a full +25 bps priced in for another OCR rate rise sometime in the first third of 2024.

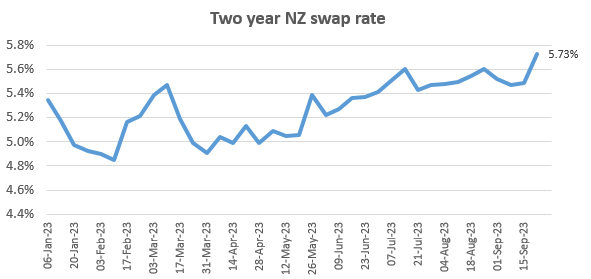

Local wholesale rates are high and rising

At about 5.7%, the two year swap rate ended last week at its highest since 2008. (Yes, it did spike one day in mid-July a few bps above that.)

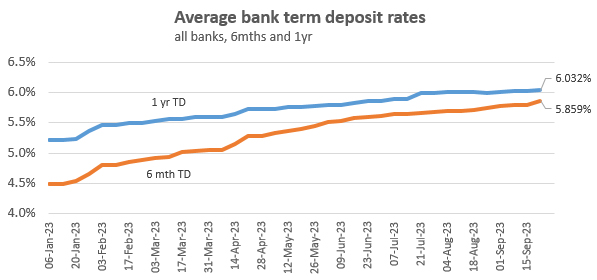

Retail rates are high and rising

Retail rates paid to savers are important because most of the bank mortgage activity is funded from retail savers. Term deposit funding is only part of that savings base (one that includes current accounts and savings accounts), but the TD part is the most sensitive to rising rates. And savers are switching into term deposits now they are yielding much better returns.

Most term deposits are for six to 12 months. Four of the five main banks offer 6% for a one year term deposit. It won't be long before at least one major bank offers 6% for a term less than 12 months.

Current rate levels for savers are now also their highest since 2008.

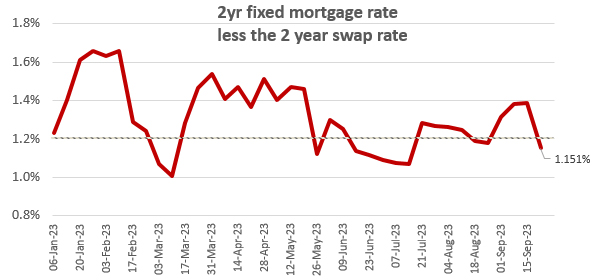

Bank margins have fallen below a key point

Over a long period, banks have tended to keep the margin between the fixed rate offer and the wholesale money cost at about 160 bps (1.6%). But that has been tough to do in 2023 when mortgage demand has been tepid.

However, there is a low point where banks don't feel they can live, and when it is breached, the pressure is on to raise rates even if demand is low. ASB has been the first to respond to that, but others will be feeling the pressure. That 'breaking point' seem to be about 120 bps (1.2%).

With benchmark, wholesale, and retail funding costs all rising in 2023, and quite sharply very recently, it isn't hard to conclude that fixed home loan rates will be rising again soon.

181 Comments

And according to economists house prices will be going up.

Hmmm, something doesn't add up - and based on their record...

It doesn’t have to add up, all that matters is a signature. Salesmen with a background in economics.

Do the politicians and central bankers with property portfolios have some other plan to pump more welfarism into property over and above what's already been done?

Do you mean higher accommodation supplements?

Yes more than likely under Labour. Not the Gnats as they want to chop govt expenditure

Nominally. But they clearly want to boost their property portfolios. And last time the put supplements up - including WFF despite John Key previously labelling it "communism by stealth".

Ouchy Ouch..... higher rates, higher bank provisions, higher house prices....... I smell BS

Yep, I suspect the green shoots will soon disappear (if they ever existed) and interest rates will soon be quite a bit higher and house prices will continue their downward track. That guy with the scrolls was right about a few things.

Land values in backstreets of st heliers are fetching $5500 an sqm, I wonder what the front row would get. But I can't afford either.

Those with good views flew through that price a long time ago, The view of Rangitoto and a developers inability to interupt that sacred peaks views has protected the prices. So much money tied up in there for sure.

Insightful article for me. Thanks David. 👍

Yes, with surging international swap markets, oil rising, 14% pay rises in the public sector, and Nationals stimulatory tax cuts, RBNZ cannot lower rates anytime soon.

You forgot the plan to initiate hyper immigration.

With inflation at 6% and oil prices rising? An RBNZ pause is as poorer policy now as transitory inflation was two years ago. They know it but they don't want to wear criticism in an election year.

Yes there should be at least 1-2 more hikes.

Oh my gird.

Thanks for the analysis! Are ‘online call’ interest rates also increasing? Just curious if they go up/down similarly to TD’s. TD’s obviously have a higher return, but I’d rather have access to my savings at the moment. Cheers.

Kiwibank is the place to be for online call, 4.5% vs ASB 2.9% and ANZ 2.75%. ANZ are real laggards here.

BNZ Rapidsave has been 4.55% for a while, watching & waiting for an increase

BNZ rapid save is not daily call interest, it is monthly. Kiwibank call is the same rate but daily, no hooks.

https://www.interest.co.nz/saving/e-saver-online

Heartland 4.6% on call

Rabo is the best: 5.25% as long as you add $50 a month. It is on call except you loose the bonus interest for that month.

Heartland (BBB) 0.1% higher than Kiwibank, not worth the extra risk.

Retail rates paid to savers are important because most of the bank mortgage activity is funded from retail savers.

Banks don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source

Big ups for pointing this out. David Chaston taking a few liberties.

It's funny that it's been pointed out by many and more so since the GFC, yet no-one wants to get it.

It's also easy to understand that when something believed to be the truth gets unmasked as a lie, one might begin to question everything else they were taught as truth. It's easier to deny.

Richard Werner is an idiot. He sounds smart but falls into the same trap we all did. There is pressure between humans, and money is there to mediate that. In the past that pressure was alleviated as we all believed in the same god. Today we relieve that pressure by relying on debt and ever increasing asset prices. That way all humans can get along as friends and every trade we do benefits both parties. The downside is, of course, exponential growth on a finite planet....

You have all of that around the wrong way : https://www.rbnz.govt.nz/hub/publications/bulletin/2023/-/media/project…

I believe a lot of people are simply hanging on with the hope or belief that National will win the election and everything will change relatively quickly back to how it was a few years ago.

Dreams are free..but at least National will allow more zoom zoom on the motorways to burn more dollars in your shrinking wallets.

Indeed... how many of the people moaning about the lower speed limits are also the ones who moan about how much gas costs?

Optimal fuel efficiency is between 50-80 kmph so when you are idling along at 30 kmph all around town, you are burning more petrol along with time. Not only that but you are increasing emissions the slower you go.

With that many different engines, models, styles of cars out there I’d need to see evidence to believe that statement.

I think it's just another example of "twisting the data" to fit the argument. Regardless of "styles" of cars, the higher the speed the higher the aero resistance.

The sweet spot that K.W. refers to is more like 30 - 50 mph, and that's evident if you just Google "car manufacturers speed sweet spot". They're certainly wrong about "wasting fuel" driving at 30km/h because again drag is considerably less than 50km/h. Remember, cars have things called transmissions that select the optimal gear relative to vehicle speed for efficiency.

Constant deceleration and then acceleration burns way more than any "optimal" gain. This is more common when travelling (sometimes) at 50, but then down to 20 or 30 frequently on an urban road.

Also even if 50 zones the average is often 35 anyway cause of traffic

If the speed limit was 100kmh in all urban roads, would that be more fuel efficient than 50kmh?

If you drove 50 km/h from Hamilton to Auckland, it would take you twice as long as 100 km/h, but the motor is doing less work to overcome aero drag. Squared velocity, the required energy to travel a unit of distance increases as speed increases due to air resistance.

Rolande

This is not correct (well bits of it are correct but you've misunderstood the reality of driving in urban environments). Average speeds of 50kpm are rarely achieved regardless of speed limits.

The issue in urban environments is intersections, side streets and driveways where you are forced to come to full stop or close to full stop.

Dropping from 50 to 30 is not the main issue.

Dropping from 50 to zero/10 is the main contributor to acceleration deceleration emissions.

Dropping speed limits to 30 generally keeps traffic flowing at a more steady rate (instead of accelerating and decelerating from 50 to zero between intersections).

So you are right to focus on acceleration deceleration but lower speed limits help address this and do not make it worse.

There was a study done back in the late 80s early 90s (can't remember which) which showed 80kmh to be the sweet spot (we covered this in ENG101 when I was at uni). Can't vouch for its veracity, but it's fairly well known.

In addition, aside from air/rolling resistance while cruising, 95% of your energy expenditure while driving is in braking (source: I was part of a team implementing fuel efficiency calculations based on tracked vehicle motion for Z). The reason it feels like you're less efficient under heavy acceleration is more likely related to your heavy foot on both the accelerator and the brakes.

Want to drive more efficiently? Minimize your braking - allow a decent following distance, and coast as often as possible.

Did any of you actually look at the link above?

Kw is correct that slower speeds are less efficient, but so is going 100 instead of 80 (which is what the previous poster was referring to).

See the 1st chart in the link

Saw Grant Robertson and Nicola Willis on Q+A this morning. When asked about what they thought affordable housing meant - both went with the 3:1 price/salary ratio. What a joke. Jack Tame missed a seriously good opportunity to ask them how they plan to get there.

There was some 'talk' around it (but not directly about the magnitude drop needed) by both. Nicola is growing to grow the economy with tax cuts and force councils to re-zone to residential up 30 years worth of additional (I assume currently zoned rural) land and Grant is going to retain the measures already put in place to discourage investors, which (according to him) give first home buyers a better chance.

He did throw out an interesting statistics, that being that before Labour upped the Brightline to 10 years; implemented the overseas buyer ban; and removed interest deductibility - FHBs made up 21% of all buyers - whereas now (since those measures) they are 27% of all buyers.

However, I'm not really convinced that has had much of a material effect on house prices though. More to the point, what are they going to do to reign in inflation?

Prices are lower because interest rates are higher. Sadly however, I suspect the folks most likely to have to sell at whatever price is offered are now the FHBs that bought in the 2020/21 years and the landlords that are so highly leveraged they can't afford the healthy homes upgrades.

What an absolute mess.

He did throw out an interesting statistics, that being that before Labour upped the Brightline to 10 years; implemented the overseas buyer ban; and removed interest deductibility - FHBs made up 21% of all buyers - whereas now (since those measures) they are 27% of all buyers.

However, I'm not really convinced that has had much of a material effect on house prices though.

The opposite, from the looks of it. This is because our attempts at improving housing affordability is centred on limiting access to less desirable purchasers (foreigners and investors), rather than actually producing cheaper new housing.

How does a government produce cheaper new housing (aside from state house builds).

Shifting from freehold to leasehold (or similar) titles, and support of wide scale offsite factory-style housing fabrication.

Exactly!

And I was in the ear of the government on both, about 2 years ago, and dutifully ignored.

I’ve given up. Wasted time and energy.

Those are the two most significant areas you can get savings from.

Assuming housing the population is of high priority, this should be something enacted almost under urgency, as if we were having a pandemic.

Slums you mean?

Hold a national design competition for say 12-16 designs, offer them in a combination of colours, and scalable up to hundreds of square metres if necessary.

Part of the problem with house design and construction in NZ, is each build ends up being slightly bespoke, and assembled in a disjointed fashion. We need Toyota Corollas but we are building them like they're custom cars. There are some modular builders, some quite good, but they struggle scaling independently. You want a facility that can produce dozens of houses simultaneously, in one place. Then it needs to be integrated into an efficient site works system for the install.

That's if your aim is sufficient supply of steady housing to meet demand. At the moment building a house can be a year or more journey. Dumb.

Agree. Bring some consistency in design standards, and you'd probably find that level of certainty would enable manufacturers to keep pre-built sections. If designs agreed that each wall framing section came in say 2m wide increments, and each increment could be solid wall, + internal door, + window etc then you wouldn't be building to order you'd supply from a picking list.

Probably put a bunch of pre-nail detailers out of a job.

Exactly. It’s the kind of model Simplicity Living are applying.

Agreed, having watched our building industry close up ( two large scale renovations in the last 14 years), I was shocked at the waste and rework that occurred ( that’s doing the job wrong to begin with - having to pull out a redo), the builders we worked with were not good at following/reading plans. Also not great at problem solving. I can only think the boom and bust nature of building in NZ has meant we don’t have a solid and properly trained building workforce. The las5 group of builders we had were young guys with massive brand new utes who didn’t understand how to project manage and were way too focused on taking their massive boats out fishing. I think they are bust now. So agree let’s get some standardised and preferably factory based building happening here.

Leasehold? Buyers don't like it, but perhaps if more were offered that would change. It's effectively what retirement villages are, isn't it - so might be more attractive to retirees.

More factory-style housing fabrication would be great, but then what subdivision developers don't have covenants preventing such buildings? Very hard to find sections to put them on. Good for state housing but most pre-fabs are single story and the trend for SH builds are two stories these days. Not ideal for the elderly. Hence, most of the state house neighbourhoods are design and build. Yes, drives government costs up, for sure. Recall an interview with the Kāinga Ora CE and they are working a lot on bringing their own costs down.

Leasehold? Buyers don't like it

If people want freehold they can fight amoung each other for the existing stock. In Singapore, leasehold property is 7:1 price/income, freehold is 15:1.

If you want to substantially lower land prices that's the fastest way to do it.

More factory-style housing fabrication would be great, but then what subdivision developers don't have covenants preventing such buildings?

You will need to strongly encourage adoption of these properties. Or, they're part of new Greenfields development.

These properties could be multi or single storey. They should be able to cater for any sort of NZer. We also have access to much of the raw materials domestically.

The way we currently build is highly inefficient and cost prohibitive. The quality at the low end is pretty mediocre, the government cannot get much more efficiency from the current model, and neither can the private house building sector. We are effectively trying to do factory work, outside of a factory. As it stands, doing housing work for the government is some of the most expensive work for a contractor to undertake.

‘Buyers don’t like it’

That’s effectively what Megan Woods said to me.

But that assumes that low-middle and middle income earners can afford to buy freehold. Increasingly they can’t. Isn’t some form of ownership better than none? It also grants much greater tenure security than renting.

And one of the reasons that ‘buyers don’t like it’ relates to the horror stories around lease hikes. If it’s done on government owned land, those can be avoided. The leases could even be peppercorn ones.

Agree on government owned land. Great idea with strong lease conditions that a new government can't re-set.

What I've seen of leasehold is that LV isn't taken into the equation on re-sale. So folks need to be careful with government valuations that reflect a land value, e.g.,

https://www.realestate.co.nz/42408759/residential/sale/10-parawera-driv…

As you can see from recent sales - sections are going for around $90K but the LV component for this property is $372K. Misleading if new to the property market for leasehold.

Fundamentally it comes down to a choice whether you want a house for life at a reasonable price, or a house as some sort of tradeable commodity.

Such changes would likely diminish the value of some existing freehold properties, particularly cookie cutter greenfield subdivision properties. If the wealthy want to battle amoung one another to live on Paritai Drive or Pt Chev let them have at it.

Leasehold is not the only option. LVT on unimproved value of land coupled with liberalised zoning to allow more building will do some very heavy lifting.

Megan thought it was an awful idea. I got a 3 page explanation as to why everything they are doing is awesome. 😂

Yes, well leasehold on government land is a great idea - not so sure just how much government land suitable for housing there is - aside from re-developed existing HNZ sites. It would be really interesting to find out. Any government needs to first service the state housing market over the private sector market - but yes, if they own some substantial, large greenfield sites it would be a great idea to subdivide it and offer it as leasehold on the open market.

Might just give private developers an idea as well if the government-owned leased land took off.

You should do an OIA request for all undeveloped central government owned land parcels in a specific geographic area - at least that would give you some idea of how viable it would be for central government to implement.

And that said, local governments that own golf courses and the like ought to think along the same lines - given they are always looking for new revenue streams.

How about building prefabricated homes on government land, as leasehold? Rather than 33.33% of all land and homes in Kainga Ora redevelopment areas going to the private market ( which is increasingly difficult to get to work in terms of feasibility)

My guess is that they (Kāinga Ora) are in no way selling 1/3rd of those properties on the private market. There is just so much competition out there for similar properties from private developers.

Look into what Te Puni Kōkiri is doing with iwi partnerships on papakāinga.

Yes, really good initiatives. Communal living will become a much bigger part of our future, and wonderfully suited to te ao Māori/Māori worldview.

It was actually most of our past also, up until only a short time ago.

Living in households of under 10 people or so is terribly inefficient.

There's a reason why 3 generations living in the same household is common in poorer developing countries. In the old USSR a newly married couple would stay in the same apartment as one of their parents and the rest of their adult siblings until they Soviet system found them their own apartment. Which might be when they already had one or two children on the way. So that's where we are headed. "Efficient" indeed.

I think covenants are not such a big issue, except for the size of house (140m2 plus garage is an example of past requirements - now houses can be much less). I have seen some surprisingly modest houses meet covenants, the main covenants that are very specific is the requirement for a gabled roof and claddings - such as listing cladding options ( ruling out non durable claddings such as corrugated iron) and the use of two differing cladding types ( pretty sure this is not in fashion either at present because plenty of high end houses have a single cladding).

Anyway the covenants I have seen (Tauranga area) have produced both expensive and very modest houses in the same subdivision.

We wanted leasehold when we were first looking back in 2013. Unfortunately, the council had just the year prior divested itself of all leasehold (which was all sold to a developer). Would've been great to put a transportable building on in preparation for future relocation.

There was some on leasehold properties we would've considered in Auckland last year - unfortunately the leases seemed to all be held by Chinese (in name at least) people who wanted way more for them than they were worth, esp. considering the leases were nearing renewal with no right to renew.

Shifting from freehold to leasehold (or similar) titles

This is what an LVT does, instead of paying ground rent you pay the LVT.

In either case, the initial outlay for land will decrease due to the expected future LVT/ground rent payments.

Stable population would help a lot.

Reduced cost of infrastructure for a start. Land cost is crazy and reduced demand would sort a lot of that. Reduced demand for construction. makes a big difference as we would not be chasing tail to catch up. Might get better houses too,

They regulate the market and land values?

Kate, Treasury did some modelling in 2021 on the affect of removing interest deductibility on residential house prices. Their conclusion:

We expect the removal of interest deductibility will have a material impact on house prices. Without this tax change we would have forecast an increase in house prices of 34% over the forecast period. Due to the removal of deductibility we revised our forecast to around 14%, a downgrade of around 16%.

https://www.treasury.govt.nz/sites/default/files/2021-08/b21-t2021-967-…

Wow - that's a big difference! And National wants to remove it? Yikes.

I saw my son today. He said in no uncertain terms he will leave NZ if National win. It’s the party for the landed gentry. And provide zero hope for young kiwis.

Will they vote though?. Big unknown in this election.

He really doesn’t know who he could vote for, as none of the major parties offer him or his generation much at all. Maybe TOP, which is where I am headed if I can be bothered voting. On policy grounds, not that it will make any difference to the result.

I think they said much the same on TV news tonight.

National Party MPs have some pretty large size property portfolio conflicts of interest.

I personally think we're getting to the point we should be describing it as corruption.

Yep

Yes- Many Nats are corrupt, if they vote for their own vested self-financial interests.

Yes I was a Nat voter- now no good options other than TOP.

Saw Grant Robertson and Nicola Willis on Q+A this morning. When asked about what they thought affordable housing meant - both went with the 3:1 price/salary ratio

Atrocious discussion. They have no answer or solution. Both referred to the long-term ratio as 3x and suggested the current ratio at being approx 7x.

Incidentally, Jeremy Grantham referred to 3.5x vs 10x, 15x, 20x to describe long-term / current in terms of the 'global property bubble.'

His comment that "people pay more because they can afford to (obviously reference to cheap debt servicing over past 20+ years) transforming to paying less because you can't afford to" is on the money.

Grantham has been predicting stock market crashes for years, and a spiralling upward gold price. Both 100% wrong.

Another grifter emptying out gullible subscribers.

Gold has been spiralling upwards since its cycle bottom in 2015. You're just unaware. What's more, if you expect the gold price to 100x like an altcoin, you don't really understand how these markets work.

Well yeah, the gold markets what, 150x larger than the buttcoin market, with far less consolidation of holdings. Far more difficult for someone to affect a parabolic price move. So slow and steady she goes.

Not so my little sock puppet. Let's try a little bit of the ol' framing.

1. BTC is not an "altcoin". Probability of it appreciating 100x is much lower now than in the past. BTC price of USD2.6 million is possible, but not in the near term.

2. The market cap of gold to BTC is not 150x larger. Gold mkt cap is approx USD13 trillion. BTC market cap is approx USD500 billion. Total crypto mkt cap is approx 2x the mkt cap of BTC.

3. The probability of altcoins 100x'ing is higher than BTC. And the probability of gold 100x'ing is low. Gold represents approx 5% of global assets.

Must feel special being one of only hundreds of millions of unique and powerful thinkers trying to ride that same gravy train.

The gold price may increase relative to other assets. The last two cycles have good returns, but it's not a 'gravy train'. The only gravy train that could be associated with gold has been JPM's spoof trading.

I'm talking more about the genius, non-sock puppety crypto world you're sharing with hundreds of millions of other suckers.

If you're all holding superior information to the sheeple, it doesn't appear very lucrative.

As I said, don't expect gold to behave like altcoins. It's not going to 100x nor is there any chance its price falls 90%+.

And any exposure that Jeremy Grantham has to gold is not based on this. It's based on being a safe haven during periods of high inflation. In fact, he should not be seen as someone recommending to go "all in" on gold.

If he says that housing is in a massive bubble globally, look at his narrative. Pretty strong evidence for his case.

All's I know is the prime determinant of wealth building is the ability to generate decent income in the first place, and your superior information and belief system is not accomplishing this for you.

Baaaaaaaa

Gold is a terrible bet, it's got no dividend and the suckers who buy the real thing get gouged every time they buy or sell. The gold 'experts' are always banging on about what a greatt bet it is, but it isn't.

Because they sell the stuff. I knew there'd be a few goldbugs here.

It's illiquid, it's got no dividend and it costs to store it.

Funny. Undeveloped land with flood risks has exactly the same set of attributes.

You need to catch up on the cases of precious metals market manipulation (price suppression) which have been going on. China is going to end the shenanigans that JP Morgan was involved in by offering an alternative market exchange for major commodities in Shanghai.

I agree Jack missed a golden opportunity there. Just like in the leaders debate when the Chris's both said they bought their first house at 24yrs ,there was no follow up question about how they plan to make it possible for young people in future.

Making it just as easy for a 24 year old to buy their house today, as it was in the 90's & prior, would just serve to undermine this delusion that home buyers back then worked immensely harder and were much more prudent with their finances than young people today.

You do not measure the success of a policy based on percentages as any increase may simply be because other buyers have dropped out of the market. Have the absolute number of FHB gone up? If not, then Labour's changes have done nothing to help them into homes.

Banks get a lot of deposits for which they pay nothing. In my small business I liked to have about $30K in the account just to run on. The bank paid nothing.

Similarly there are millions of wage earner, even beneficiaries, each of which, who have hundreds, often thousands of dollars in accounts for which the bank pays nothing.

Better to be an owner than a borrower. But it's not the New Zealand way.

Isn't that why everyone borrows?

Nobody likes to mention that the bank's are the biggest landlords with zero responsibility.

As an interesting aside, in 'straya, ANZ lowered rates last week.

Well that's good news - certainly here they'll be feeling the pinch as expansion of their loan book on residential was such a large part of their business model. No doubt JK will be chomping at the bit to get investors and overseas buyers back into the market. Hence Nationals policy moves.

That's my reckon as well. Not sure how the Gnats are doing their demand forecasting. Coincidentally, SCMP suggests that the gravy train of Chinese buyers of foreign property is drying up. Article is more focused on Chinese buying in Asian markets where properties are far cheaper than in the Anglosphere.

Chinese investors scramble to sell overseas properties amid shaky economic conditions

- As the Chinese property crisis continues and the growth of household wealth dwindles, some have had to sell their overseas investments

- But with a saturated market and very few buyers, property owners are struggling to offload their foreign properties

https://www.scmp.com/economy/china-economy/article/3235448/chinese-inve…

JC do you know how active the Chinese have been in the Japanese property market?

Very active according to the Japanese media. The following is a really good overview of what's been going on. The SCMP article referred to only suggests Chinese owners of investment properties for Chinese tourists to Japan are doing it tough at the moment.

Great, thanks. I suspected so, especially as Japan’s little lift in property prices seems a little anomalous

Japan's population is shrinking fast, real estate there is going to be getting very cheap as literally abandoned houses stand empty in shrinking regional towns.

by

Scottnlp

|

24th Sep 23, 4:40pm

I agree Jack missed a golden opportunity there. Just like in the leaders debate when the Chris's both said they bought their first house at 24yrs ,there was no follow up question about how they plan to make it possible for young people in future.

I think everyone was still laughing, after Willis pointed to a single sentence as her proof their policy was costed.

She didn't do too well. Took the wrong strategy in jumping in and answering first to every question JT put to them both. GR just sat back and waited and had so many opportunities to just fire shots at her responses. Some of those shots were pretty good quips as well. He's the better debater.

I have said several times that I have seen her in parliament on several occasions and observed a very average intellect.

So smarter IRL than on the telly

😂

Betcha if they need ACT in a coalition - David Seymour will want the Finance Minister role.

They dropped their fixed loan rates, which are immaterial to the bank as everyone is on the much lower variable rates.

"The data showed that in April, only 5.1% of new and refinanced loans were fixed, while 94.9% were variable."

https://www.brokernews.com.au/news/breaking-news/why-borrowers-are-choo…

People forget that in Australia the loan market is around the other way to NZ, there everyone goes variable and hardly anyone goes fixed as variable rates are always lower than fixed unlike NZ where fixed rates are lower than variable.

A long time back - NZ was the same. Always wondered why that changed so dramatically over here.

Hundreds of thousands of NZ mortgages will be in significant duress when they are forced to pay more than 6 to 6.5%, for longer than 6/12 months.

Sure they can chew up their retained savings for a few months and keep the water, food and lights on for some short durations. Yet many borrowings past 500K are not sustainable at/north of such rates.

This current Swaps/OCR/Mortgage hiking cycle will be a "hiking and hold period" that will exhaust many who bet it all on 2.5 to 5% mortgages.

This has been obvious since 2021, if you ignored the warnings posted here and instead have lived by the dross peddled by the crookeconomic Oneroofers ......a lesson in Deflating "bubble markets" is coming.

Buy property when interest rates are high, and drive a hard bargain.

There are a few things David has written between the lines here.

There is a delicate balance between telling the truth and being responsible which is hard to deliver.

In the weeks and months to the come we might get drowned in the latest data, but this central picture will not change.

Every time I see the line - "rates are now at fifteen year highs" - I'm reminded by what happened after that peak 15 years ago.

Financial history has a pattern of repetition, not always for the exactly the same reasons, but always for similar ones.

Rates weren't really the cause of the global financial crisis, it was a risk management issue that caused credit markets to freeze. The last time we had a classic rates based recession was the early 1990s really. That's not to say it won't happen this time but it's at least equiprobable something else will cause a recession.

I’d argue the GFC was caused by sheer greed and corruption given the level of deceit involved and complicity by the US bankers who all knew that shoddy mortgages were being packaged up and on-sold with questionable credit ratings. A mass cascade of kicking the can down the road knowing the end consequence but profiteering on passing the bomb.

The GFC was a stock market disaster due to subprime home loans being sold as gold plated prime loans.

The current situation is an inflation battle, historically these take 5+ years to battle out. If NZ interest rates had stayed at 2006/07 levels for the last 15 years then housing values simply would not have rocketed to the moon. They would have bumbled along at 2% to 3% annual increases.

This confirms what many here already knew was coming. Interest rates higher for longer, house prices and finances under pressure for even longer. Its entirely understandable Higher TD rates will suck loose change of the streets. At some point real value will re-appear along with other viable options to invest.

Let's not forget what happend in the GFC...

I remember the GFC quite well. Lots of mutual funds, property and mortgage funds seized up.

And plunged, along with the stock market. People lost fortunes, probably another reason kiwis prefer a plain vanilla renter than trusting your money to someone else.

Which would suggest we've never addressed the issues behind this. A parasitic financial system? Faulty maths? A system driven by fear and greed?

It cracks me up. We're taught to despise 'socialism' for using other people's money yet our modern day rentier and finance capitalism is built on this notion. The entire residential property investment market was built on using other people's money to pay the mortgage. There are some very 'narcisstic' "capitalists" who brag about this, promote it and teach it as the means to getting rich.

...yes-yes-yes Nifty1, just like clockwork, when it once again implodes, it will be major Central Banks in unison to the money pumps and interest rates will go negative, TD's holders will have to pay banks to hold their money - right?

Seriously now, with trade barriers being erected everywhere as we speak and powerhouse China in serious trouble we cannot rely on them to rescue trade as in GFC. The next downturn is going to be an absolute shitstorm. Another GFC now will totally crush house prices for starters!

Think StAgFlAtIoN!

💯

Thoughts on ‘viable options?’

I'd like to know how many posters here are goldbugs, predicting economic Armageddon. I'll bet there's more than a couple.

....sounds like you're worried.

Not at all, about to build a new house. Gold is for the Armageddon dudes, not for me. It's got no dividend either, a failed bet.

I'm more of a prepper than a goldbug.

If PDK is right, if the dino-juice runs out, your golds' not worth much if there's no food to buy. Get self sufficient for your diet, and worst case scenario, you have lots of cheap food to consume or sell.

It can be melted into bullets. Lead clearly cheaper though. Depends how hard core your prep needs are.

You'd be wise to have an easy means to hunt for more protein, for sure.

Prolly won't get that bad, but as a society we have outsourced most of our basic requirements and are now being held to ransom for them.

Gold buys a lot less eggs in 2023 than it did say in 2015.

The dino juice ain't running out and it won't. I've heard about it for half a century, it's the biggest BS story on the planet.

I'd say it'll just keep getting more expensive.

Because of tax, and the Arabs don't seem to have any trouble gouging us for it.

Why wouldn't you? Captive market and all.

But yeah fossil fuels will become like cigarettes.

Hardly, aircraft don't run on solar power, neither do cars, trucks or ships.

I meant you can keep doing it, it'll just get more expensive and they'll restrict where/how you can use it.

Just like cash and food. Welcome to the NWO.

Oh it could get ugly real quick god forbid we experience the big one in this generation. If you can’t defend your broccoli and chickens its only a matter of time until someone decides to feed their family at any cost

In this reality, of the highest and fastest % spike in the Cost of Funds, any of us have seen - and its rise is still NOT DONE!

- Are the housing/land asset hoarders expecting rainbows and unicorns ???

Good luck on finding anyone, still liquid enough to paying your expected moonbeams for your dirt and ticky tacky housing.

I bought into a lifestyle subdivision a few months ago and it's all sold out. It's just a matter of being diligent, no matter what the market's doing.

Interest rates got a lot a lot higher in the 80's, 20%+ plus. It's a minor blip, has to happen every now and then.

Wingman, what suddenly compelled you to join this, what you labelled as a "enclave of envious socialists" news platform and forum just eight months ago? Was it to help you make financial decisions?

No, I've been making very good financial decisions for many decades. I just happened on this forum, it seemed to be a hotbed of socialism, and how we're all doomed. It's very interesting.

Is this forum a closed club that no one else is allowed to join, do we have to submit our political views to the likes of you to be 'admitted'? Are 'rich', 'successful', people not allowed?

Of course this is an open forum. Its also a known fact the truly rich and successful usually don't boast. They don't need to convince others using pseudonyms:)

I'm not boasting, just proving that making money isn't that hard, that using your nous, saving money and taking risks provides jobs, keeps the economy going and is a worthy goal.

Not just whining about how bad it all is and how the real estate market is going to crash, which it isn't.

by wingman | 24th Sep 23, 8:03pm 1695538993 - "I'm not boasting"

You're funny :)

I'm "funny"? Well I'll bet I'm a lot more successful and ambitious than you've ever been or ever will be.

Is ‘success’ and ‘ambition’ only based on monetary criteria?

I mean, it is a finance/economics site, after all.

Not that you need to advertise what you're up to. Unless you're saving orphans in Rwanda or something, you'll probably be profiting from some sort of exploitation if you have money.

It’s just that some here consistently frame ‘success’ and ‘ambition’ in purely monetary terms. And yeah it’s a primarily financial website, but it also frequently crosses over in to non-financial matters. And of course the two are intertwined, especially if we think about the holistic concept of ‘wellbeing’…

If it were some sort of personal empowerment forum, then you would expect people to list whatever subjective ideal they use to gauge success and ambition.

The site presents itself to the uninitiated as a resource for assessing forms of financial investment. The comments section is largely its own beast, but it is fairly anti-capitalist.

Personally I find the consequences of being uber-aspirational not worthy of the return, if others want for riches and large surpluses, that's up to them, not something I feel the need to knock.

Like it or not though, we are all commercial entities, trading our time for money. You want to maximise that value, giving you extra time and resources to pursue that which might really spin your wheels.

"And of course the two are intertwined, especially if we think about the holistic concept of ‘wellbeing’…"

That sounds very Jacinda, I thought you couldn't stand her...

I quite like it when commentators choose to divulge their backgrounds. It let's me frame their points and points of view.

Happy to hear from the successful, unlucky and in-between.

I'm quite proud of wingman's achievements. I could have been the next wingman if I just had some balls and appetite for risk. Had my opportunity to leverage myself up in late 2021, sold my first home for shy of triple what we paid in 2017. Could have dumped $100k into crypto, leveraged the rest into a portfolio of rentals. But stupidly dumped all that equity into a 4x2 villa on 1/4 acre within 500m of several schools. I guess fools choose family over finance.

I always love those posts..."I could have been rich but I chose education/travel/benevolence/God/family/altruism/planet (you choose the word) first".

That depends on the importance one sees being rich as, in reality we don’t need a lot to be happy.

....still boasting.

Our closest family friend is top 100 in NZ in terms of wealth (used to be top 50). Very humble and not boastful in the slightest. Made their wealth in a productive business employing people, rather than entirely self-interested speculation.

What do you mean "self-interested speculation".

Every time I build a house I'm employing dozens of people. Builders, plumbers, roofers, excavators, drainlayers, architects, local body pen-pushers, glaziers, electricians, curtain & blind manufacturers, you name it. Even as I write this I'm employing 4 people, an architect and 3 well drillers. I'm contributing to the economy, big time. What do you do, leave your money in the bank for them to speculate with?

And it's risky, if it's so easy, you do it and 'get rich', or maybe 'get poor'.

Altruism huh wingman? Free advice

Are 'rich', 'successful', people not allowed?

No. But I understand those 'born at the right time' may sign up without delay.

I see, it can't be done Muzz? Well you're doomed from the start aren't you?

Did interest rates rise over 200% in a fraction over 2 years to 20% ???? NO!

Borrowed sums in the 1980s/90s we a fraction of the Current Insane DTIs.

- DTI legislation will go towards limiting/resolving this, over time.

We are in the short term Bubble of Everything. Are you not observing reality? or just so very much taken with the current irrational exuberance mania?

We’re pushing 300% in the 2y. That alone would be like servicing debt three times the size when rates were low. Onwards and upwards.

Word on the street overseas is that its not just "Higher For Longer" but maybe Forever, as the neutral OCR rate appears to now be higher than previously. The global stock and bond markets are waking to this reality, the housing markets will too.

We arent going back to pre-Covid times, but to pre-GFC times. Possibly pre-2000. As we should. Two decades of loose monetary policy and quantitative easing has completely distorted the markets, and its time for a reset.

I think they're going to keep attempting financial reinvention until it goes totally bust.

Yep. But in saying that I don’t think this will be a GFC style bailout this time round, there are many different factors at play and we’ve essentially skipped a cycle due to the COVID money hitting right as we looked like we were heading into a silent recession. Things are now twice as bad and loose money intervention now will make every man and his dog hard for houses and crypto once again pushing money offshore and having very little effect other than higher imported inflation. OCR is too slow for modern markets and hard cash is dead so infinite money supply it is until the population revolts, whenever that may be.

My reckon is there’s still more to fiat as it is a currency of transaction. And that is all there is to it. A control over people’s spending, and tax can provide incentives to spend on certain consumer industry. Whereas gold was a hoarded store of value, fiat is a method of inflated transaction, the next turning could see a number of different scenarios along with their own enigma to protect wealth of the few, but the western world will have a few rounds of deflation as we’ve seen in Japan before then.

Do I reckon this means crypto and houses will take off like they did during covid? No. Will they increase again at some point? Probably. Once China and America figure out who wants to blink first, we’ll know more. We came about as close to infinite reserves as we could in 2021 without adjusting our monetary policy increments to a halving method. RBNZ basically gave the message to create anything you possibly can. And we chewed into it like crazed animals force fed steroid infused dollar bucks. Next comes the call from the bank, thank you for your service.

My reckon is there’s still more to fiat as it is a currency of transaction

For sure. An alternate store of value can be useful if someone is generating a strong surplus, but in a world where most people are hand to mouth, or slightly above, then fiat is the most logical form of currency to operate in.

Assuming things deteriorate, then you will see an increase in some form of grey currency, as people lose trust in the system, and increasingly want to operate outside of it. I believe in Lebanon, over half the population now transact in USD for this reason, including the likes of medical staff receiving pay.

Yes ......deglobalisation and ingrained inflation will equal "Higher and Higher and Hold Forever"

Thems DDDEBTs are now grenades - with pin pulled!

Take cover!!!!

Banks also need to make profits to survive. With the CCCFA, a lot of fee revenue dried up during bottom of the interest rate cycle. As we are now nearing the peak of the cycle, reduced bank margins are sadly putting further pressures on the interest rates.

New World Orewa tried to charge me $13.30 for two medium sized Kumara this weekend. Still lots of interesting times to come before the economy will add up for regular folk.

Interest rates are subject to outside influences. A change in government with reduction in spending. The Ukraine war ending. Rates will drop, we just don't know when.

Looks like now's the perfect time to get out and take some risk.

Elevated interest rates, house and land prices down, lots of posts here about the coming financial implosion, predictions of a stock market plunge, depression and currency crashes, preppers hunkering down, and those perennial merchants of doom, the goldbugs loading up on a useless metal.

There's nothing like being a contrarian.

Hey guys, look everybody is heading to the lifeboats, looks like the queue at the buffet is down.

Contrarian on the Titanic.

Unless I see all the property markets in NZ showing a coordinated decline, it's too early to be contrarian.. and LOL on the Titanic, 'hey the buffet queue is down' remark !

Um - you forgot the disclaimer about this not be financial advice :-).

House and land prices aren't really down (yet) unless you are looking very short term.

I'm wondering and waiting for them to get seriously down... but it never ever seems to happen here. Seems there's always a buyer to underpin prices before they drop significantly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.