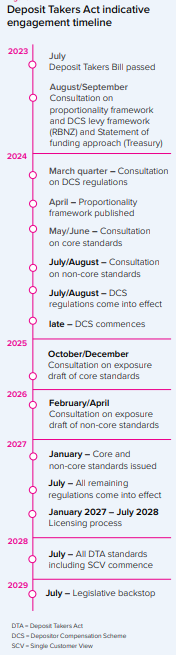

This week's bi-annual Reserve Bank Financial Stability Report (FRS) highlights just what a slow burner the Deposit Takers Act (DTA) will be.

Enacted on July 6, the DTA rollout timeframe detailed in the FSR runs until July 2029.

Whilst plans to introduce a Depositor Compensation Scheme have hogged the headlines, there's plenty more to it. Another issue highlighted in the FSR is that the DTA requires the Reserve Bank to "prepare and maintain a resolution plan for each deposit taker" in case it fails.

"The DTA requires the Reserve Bank to act as New Zealand’s resolution authority. This means we will have direct responsibility and accountability for the resolution of licensed deposit takers."

"As part of these new responsibilities, we are required to prepare and maintain a resolution plan for each deposit taker and publish a Statement of Resolution Approach (SoRA). The SoRA will set out our expected strategies for dealing with failing deposit takers, and our intended approach to cooperating and engaging with relevant agencies, both domestically and internationally," the Reserve Bank says.

"We are currently undertaking policy work to explore optimal resolution strategies for different cohorts of deposit takers. This work will include consideration of the need for additional statutory powers to recapitalise a failed deposit taker, upon which we are expected to report back to the Minister of Finance within the next two years. Considerations will include recent increases in minimum capital requirements for banks, our existing resolution toolkit, and the ownership structure of New Zealand banks."

The Reserve Bank notes its Open Bank Resolution (OBR) prepositioning policy applies to locally incorporated banks with over $1 billion of retail deposits.

"It [the OBR] is set to provide depositors next-day access to a portion of their funds when a bank fails and is placed into statutory management. This is intended to reduce disruption to banking services compared to liquidation or receivership, while avoiding the upfront cost associated with taxpayer-funded bailouts."

"In addition, the BS11 Outsourcing Policy applies to locally incorporated banks with over $10 billion of net assets. It requires those banks to ensure that any outsourcing arrangements do not compromise the bank’s ability to be effectively administered and operated if placed under statutory management," the Reserve Bank says.

There's a detailed explanation on how OBR could work here.

Speaking in September Kerry Beaumont, Reserve Bank Director of Enforcement & Resolution, said work exploring resolution, or failure, strategies for different types of deposit takers will include another look at the potential role for statutory bail-in powers.

Statutory bail-in is a resolution, or failure, tool where unsecured liabilities may be written down or converted into equity. Bank liabilities typically include deposits and bonds. The idea is the costs of a deposit taker’s failure would therefore fall on its investors and creditors rather than the public purse. Bail-in powers are designed to help authorities recapitalise failing financial institutions quickly, helping restore viability and capital ratios above regulatory minimums.

Although there have been no bank failures in New Zealand in recent years, there have been banking crises in the past, and much of the finance company sector dissolved between 2006 and 2012.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

15 Comments

The more I learn about banking, the more I think small countries like NZ should transition to a single state-backed bank paying (for example) A% interest on transaction balances, B% on savings, C% on term deposits, with 25-year fixed rate mortgages offered at D%. The bank deposits would be liabilities of the state (Govt debt) and the mortgages would be Govt assets (as they were in the 1940s and 50s). Govt net debt would be the difference. This approach would negate the need for Govt to pretend to borrow by selling bonds, although they would probably have to carry on issuing bonds given how much the finance sector relies on safe Govt assets for collateral.

Customers could choose a basic online State bank account, or opt for their account to be managed by an approved customer service intermediary who would make their money from transaction charges, selling add ons, airpoints credit cards etc.

I would fix the interest (A, B, C and D above) long-term. This approach would return billions of dollars to the NZ economy by removing the drain of bank profits. Remembering that bank profits are a function of (a) the level of banks deposits held by banks (which are created by loans), (b) RBNZ requirements for the level of equity that banks need to have in relation to their deposits, and (c) the expected return on that equity. With the State effectively backing the bank, there is no need for equity or profit, so the interest collected and paid would net to zero.

Alas, it wouldn't work. You'd get a shadow banking system within days and your system would either die quickly or cost heaps to let it die slowly.

Try approaching banking from the point of view that for most people (90% plus?) banking is a pure utility function.

It doesn't matter who is providing it as consumers really can't see any difference - if they shop around - as there are none. Imagine if Genesis started saying their electricity was better than Contact's. Banks are supplying money, and money, like electrons, is the same from any supplier. Consumers are really only interested in the price (and the occasional freebee that is never free).

The 'products' supplied by utility companies are homogeneous. Retail banking products likewise. A bank account, while there are flavors, operates the same. A mortgage, again flavors, operate the same. But unlike a normal utility company that has to build and maintain significant infrastructure, banks have almost none (even their data centers & computers are leased, rented or paid for on a subscription basis.). Even how banks evaluate risk has become much the same and the only reason some banks will take you on as a risk is down to minor fluctuations in un-committed capital (and of course the bank's size as bigger can absorb isolated risk more easily).

Retail banking could be run as tweakable algorithm. It's needs to be 'tweakable' to adjust to competition (to maintain market share) and changing market conditions. Were it a non profit service - few of us would be prepared to indulge in enriching bank's shareholders as very few would need to step outside the services offered.

I feel like most of your latter points (which I basically agree with) contradict your 'alas it won't work' starting point?

Respectfully, I think you're also missing two things. First, banks are licensed by the State and they operate within the Crown's regulatory framework - they need settlement accounts at RBNZ to operate etc. So, banks (or shadow banks) can only exist if they are permitted to do so and provided with the infrastructure to run their operations. Second, if customers know that their money is 100% safe with the State-backed bank, and their mortgage etc is guaranteed to be fixed for 25 years (and refixable at zero cost if rates change), why would 90% of people move their basic banking? How could private banks compete?

The more I learn about banking, the more I think small countries like NZ should transition to a single state-backed bank paying (for example) A% interest on transaction balances, B% on savings, C% on term deposits, with 25-year fixed rate mortgages offered at D%

I very much like this thinking. My only concern is that the Cantillon Effect would simply manifest itself in a different way. F'more, govts would be more powerful and better positioned for their own self interest (often to the detriment of constituents).

No good in an economy that produces little of what it needs as you effectively remove yourself from international trade.

How so? You still have a central bank that plays its part in the global network of central banks?

A Central Bank that only controls NZD....and indirectly only that available in NZD, which aint much.

If we wish to be part of the international banking cartel and all that provides you can hardly banish them from the NZ market....and then there are the subsequent currency implications.

If we were Japan and produced highly desireable products and ran a persistent current account surplus (along with the associated foreign reserves) then it may be possible for a while....we are the antithesis of Japan

I see what you're saying. Yes, having a current account deficit robs us of some of our monetary sovereignty, but there is nothing to stop us varying interest rates on govt bonds to ensure that we can continue to export bonds to close our current account deficit (as we do now).

We could convince ourselves that the offshore money markets would be happy with such an arrangement but I doubt they would see it that way...especially when you consider the size and significance of our economy.

Frankly im surprised we have managed to retain the level of support the NZD has enjoyed the past 40 years.

Yes, I think it is because the strength of the NZD is not about real trade, it's about the return available on NZ govt bonds, and market confidence that the govt will make the payments.

A (illogical?) confidence easily lost...and difficult to regain.

And the access needed is not solely the Government....indeed the bulk of our offshore debt is held in private hands.

You are probably right Jfoe, even tho I am a free market capitalist by nature. The 5-6 billion dollars of bank profits a year not sent offshore is worth the consideration alone. NZs next Labour Govt [hopefully a long time away] will be so far left that something along these lines will probably happen.

Socialism, humanity's ultimate death-star.

I remember reading somewhere that one of the secrets to Germany's ability to maintain many medium sized technologically advanced family owned industrial firms was the amount of local banks available and willing to extend credit to local firms over many generations.

In New Zealand we have been going in the opposite direction with a reduction in local banking services and an increase in online banking entities without ties to regions.

Technology like m pesa may have had the effect of enabling Africans to have access to a bank account but technology in New Zealand seems to be having the effect of reducing the availability of credit to small businesses without the political will existing to enable the provision of commercial credit or the protection of savers and their deposits.

The bureaucracy and time involved in setting up a deposit protection scheme (we had one before) just shows you that the generation in power now in the institutions doesn't really believe in deposit protection and is slow walking it. They are neoliberals at heart and believe in survival of the fittest rather than any type of financial justice.

The trouble with a survival of the fittest attitude towards bank deposits is that trust in banking institutions erodes and when trouble strikes the trust deficit can't be reversed in a timely fashion. So the financial institutions freeze the deposits and the system gradually freezes up altogether.

Above link to banking crisis not working.

Link to RBNZ paper.

Banking crises in New Zealand - an historical overview

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/events/june20…

Too big to fail. Does this reassurance from the state mean that banks will engage in more risky behaviour on account they know there is less liability should they get it wrong?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.