The home loan market is dominated by the big five banks.

As at September, 2023, the latest RBNZ Dashboard data shows their mortgage books had a combined share of 93% of total (C5) housing lending. It is a share that basically hasn't changed in at least four years and probably longer.

But within the big five, there have been winners and losers.

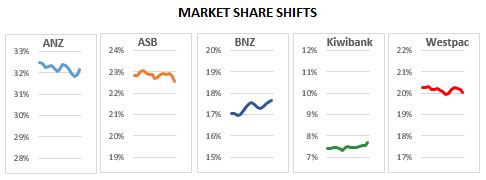

Essentially, ANZ is holding its own, ASB and Westpac have been losing share, and BNZ and Kiwibank have been gaining share.

Size matters in mortgage lending. Margins are small and unless you have a large enough book, the margin isn't sufficient to cover the basic regulatory and operational (marketing) costs.

Size matters in another way too; a large embedded mortgage book allows a bank to weather the market share shifts. A loss of 1000 mortgage clients from ASB for example ($500 mln) is a relatively minor event. But to TSB or SBS Bank it wouldn't be. And such is the competitive nature of the mortgage market, increasingly driven by the mortgage broker channel that is more cut-throat, that shifts from rate competitiveness or broker compensation, can generate such movements.

We have analysed the Dashboard data in detail to track the changing market shares of the five big banks and that does reveal shifting tides.

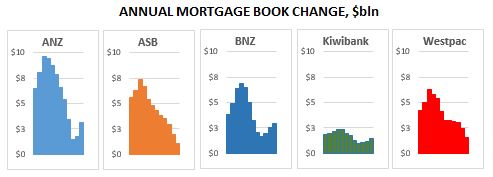

The annual growth in home loan lending peaked in September 2021 (at +$34 bln) and since that expansion has fallen away significantly to be only +$10 bln in the year to September 2023.

Things are much more competitive when loan growth slows.

Recently a couple of banks have managed to change this trajectory, but their gains are hard-won and relatively minor.

Perhaps it is worth noting that the September gain by BNZ, the smallest of the Aussie-owned banks, almost matched the gain by the largest, ANZ. Although BNZ maintained even growth over the four quarters of that year, their gains were primarily in the first two quarters. ANZ roared back in the three months to September.

It is ASB and to some extent Westpac, who are leaking market share.

This set of charts tracks year-on-year share changes, quarterly, over the past four years. Market share shifts are very had to win in commodity markets like home loans and can only be identified over a longish perspective. No main bank is at threat of having its long-term ranking challenged, but the current 'losers' will not want the recent trends to continue for another four years. That will be motivation enough to keep this market very competitive - and probably prevent any new player from disrupting the status quo.

13 Comments

Size matters in mortgage lending. Margins are small and unless you have a large enough book, the margin isn't sufficient to cover the basic regulatory and operational (marketing) costs.

So do exceptionally low capital risk weights - page 28 (29 of 52) Hence:

{kind=link}

Banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%. Thus around 60% of NZ bank lending is dedicated to residential property mortgages owed by one third of already wealthy households

{kind=link}

So much so they would rather lend to you for car or small business working capital via a resi mortgage extension...... you get lower rates and they make more margin

2 year SWAP rate 5.34%. Margins are growing

It's even worse than you think. 2y Interest Rate Swap currently 4.80%

It will be an interesting 6 months ahead regarding competitiveness of mortgage rates from the so-called big 5 banks. Current rates remain at around 7%, and there is minimal difference between those banks in the rates offered (floating and fixed).

Great article thanks, would be very keen to hear about the fortunes of the next tier banks as well if possible!

I had dinner last night with a friend in a high position at BNZ in Wellington. He believes that banks will be culling their staff this year, because lending growth won't be sufficient to keep up their profit share.

I heard the same but from another Oz bank. They simply can't keep the current headcount and maintain profits.

You know the market is not competitive by the movement in fixed mortgage rates relative to interest rate swap movements. There have been only token changes to standard fixed mortgage rates with the irrelevant fixed rate terms of 2-5 years while the 1 year rate has been left unchanged while banks reap higher margins. The market will be competitive when carded rates are lowered as a starting point to get banks talking to customers. Right now they are happy to smile and wave.

Lol would be quite funny if Orr had a hand in telling the banks to not lower the mortgage rates. Orr is the gift that keeps on taking from NZers to give to the banks overseas.

Adrian Key.

but their gains are hard-won and relatively minor

About as hard-won as shifting slightly on the sun lounger to ease a numb spot, no doubt it felt exhausting though.

Nice to see Kiwibank included in Big 5, which was Big 4

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.