By Yana Mickevich and Dzmitry Charapahau (Belarusian Investigative Center), Karolis Jursys, Gabrielė Navickaitė and Jūratė Damulytė (15Min.lt Lithuania), Gareth Vaughan (Interest.co.nz) & the Organized Crime and Corruption Reporting Project (OCCRP).

Interest.co.nz is grateful for funding support from the Brian Gaynor Business Journalism Initiative in helping bring this project to fruition.

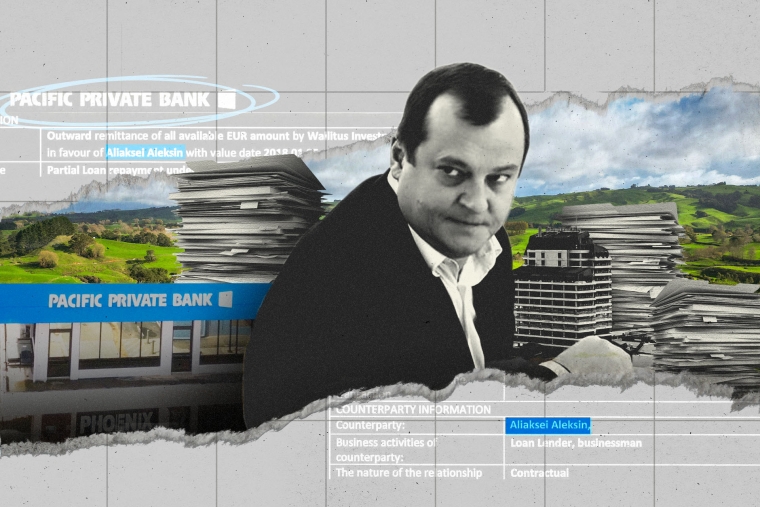

As businessman Aliaksei Aleksin’s influence grew in Belarus, leaked documents reveal how cash flowed between his energy firms, two Cypriot companies, and his personal bank account in a series of complex transactions involving loans with no clear commercial rationale and a series of cancelled oil contracts.

- Leaked documents show how apparent loan repayments from a Cypriot firm called Wallitus Investments to Aleksin totaling almost US$2 million were processed by Vanuatu-based Pacific Private Bank (PPB) and New Zealand financial services provider Worldclear.

- At least three transfers were rejected by other banks before the payments were repackaged and attempted again, prompting experts to question whether PPB and Worldclear carried out adequate compliance checks.

- Just before the loan repayments were made, another Cypriot firm which had signed hundreds of millions of dollars’ worth of oil supply contracts with Aleksin’s energy companies transferred almost the exact same amounts to Wallitus. Several of the contracts were later cancelled.

- Experts questioned the complexity of the arrangements and said they should have raised compliance questions about the true nature of the transactions.

- Reporters found no evidence to show Aleksin, PPB or Worldclear engaged in or knowingly facilitated criminal offending. Worldclear's founder denied any wrongdoing by himself or the firm, while lawyers for the owner of PPB at the time of the transactions said he “vehemently denies any allegation” that he assisted in any financial crimes.

After Belarus’ old-guard oligarchs were hit by European sanctions, businessman Aliaksei Aleksin’s fortunes began to rise.

Untouched by the 2012 sanctions package, which was designed to punish the autocratic rule of long-time president Alexander Lukashenko, Aleksin became increasingly influential. Starting in 2018, Lukashenko issued a series of decrees that granted Aleksin almost total control of the tobacco industry. He was also involved in multiple other industries in Belarus, from energy to food.

Aleksin was sanctioned by the United States and the European Union in 2021 as they tried to hinder what the US described as Lukashenko’s “corrupt and brutal regime” by targeting key businessmen - labeled by the US as “wallets” — who they said helped prop up the president’s rule and benefited from it.

Now, reporters have obtained leaked documents from inside a New Zealand financial service provider called Worldclear, the Vanuatu-based Pacific Private Bank (PPB), and Aleksin’s companies that offer a rare behind-the-curtain look at financial transactions connected to his business empire in Belarus years before he or his companies were placed under international sanctions.

The files reveal a pipeline of cash flows between Aleksin’s energy firms, two Cypriot companies, and his personal bank account, with the funds routed via PPB and Worldclear.

Multiple finance experts, including a former banking professional turned fraud investigator, and an attorney who is a certified anti-money laundering expert, said the details of the arrangements – which feature an interest-free loan with no clear commercial rationale, repeated cancellations of oil contracts, and transactions blocked by banks – raise compliance questions about the true nature of the transactions.

The findings come as part of an investigation into financial services provider Worldclear by OCCRP and partners, which showed how Worldclear processed millions in transfers for a colorful global clientele – and how inspectors from New Zealand’s Department of Internal Affairs found it was only partially compliant with anti-money laundering requirements.

On its now defunct website, Worldclear offered “transactional banking services to international corporate and institutional customers,” but it was not itself a bank; instead, Worldclear held its clients’ money in accounts in its own name at mainstream banks which functioned as a pass-through account, holding the amounts clients wanted to transfer before sending them on to their destination. Worldclear’s staff would then execute the transfers requested by the firm’s clients, the leaked files show.

PPB at centre of apparent crypto scheme

- Last year OCCRP and 15min revealed how PPB's current owners bought a portfolio of luxury real estate using loans from PPB backed by the proceeds of a crypto coin fundraiser. (Lawyers for a company belonging to the bank’s current owners denied that the crypto fundraiser was fraudulent but declined to comment on specific transactions).

- In November 2025 Vanuatu’s central bank revoked PPB’s international license. It had warned PPB two months earlier that it had violated the conditions of the license. The decision was stayed in December 2025 pending an appeal, and PPB’s managing director told OCCRP in April that the bank’s license is “not suspended and [PPB] is operating as per usual.” Reporters didn’t receive a response to a request for confirmation sent to the Governor of Vanuatu’s central bank.

The energy company and the loans

The troves of leaked documents from Worldclear, PPB, and Aleksin’s firms cover the years 2014 to 2020, before Aleksin was sanctioned and when his star was rising in Lukashenko’s circle.

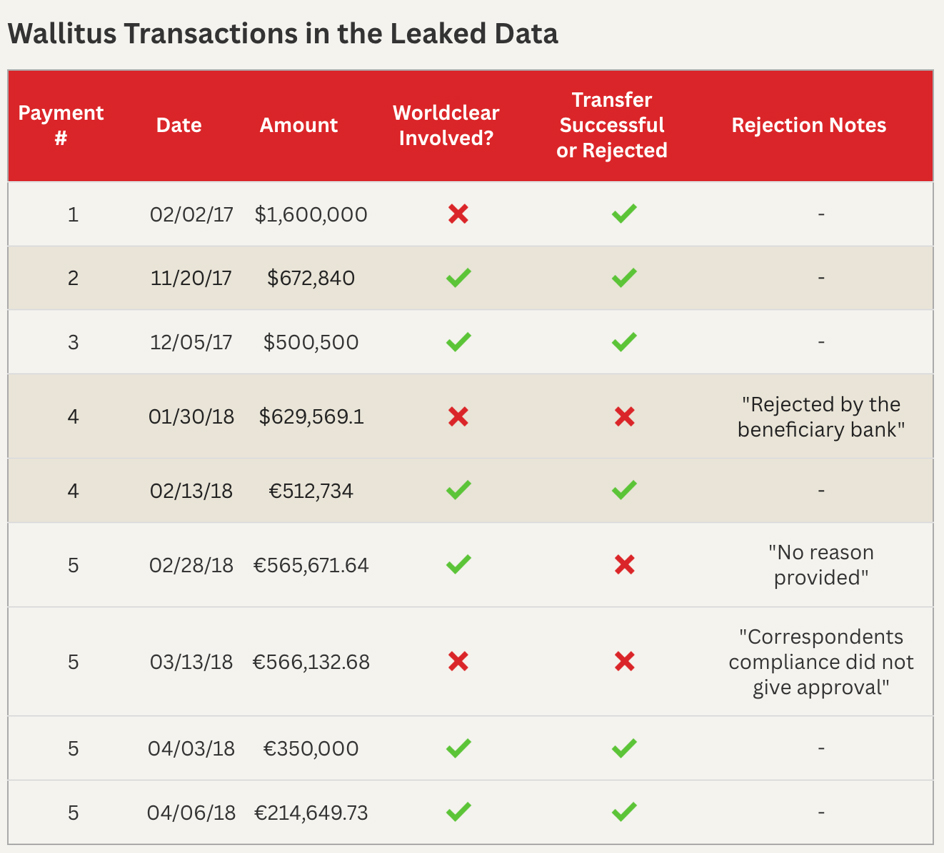

They reveal how in 2017 and 2018, PPB used Worldclear to process around US$1.8 million in transfers labeled as loan repayments from a Cypriot firm called Wallitus to Aleksin’s personal account at MTBank, a Belarusian bank he had acquired in 2015.

Leaked PPB records indicate Wallitus was part owned by Vilius Kavaliauskas, who was also PPB’s owner until 2018.

Each time Wallitus attempted to transfer money to Aleksin, it had days earlier received an almost identical amount from another Cypriot company connected to the tycoon called Sumsteg International, raising questions about the real source of the loan repayment funds.

A wealth management firm owned at the time by PPB’s Kavaliauskas provided administrative staff and services to Sumsteg. (Lawyers for Kavaliauskas did not respond to questions about his role in Wallitus. They said the wealth management group of companies’ activities “were entirely lawful” and fully regulated).

Vilius Kavaliauskas featured in the Art’s Vilnius fair website as part of its council.

IMAGE CREDIT: Screenshot/artvilnius.com/about/artvilnius-counci

Leaked files also reveal how Aleksin’s petrochemical and petroleum companies had signed hundreds of millions of dollars’ worth of oil supply contracts with Sumsteg, which is owned by a friend of his son.

However, reporters found that Sumsteg did not appear to be equipped to fulfil the contracts – its financial statements describe its main business as “provision of financing” and acting as an “agent for financing,” not supplying oil.

Sometimes the loan repayments from Wallitus to Aleksin were rejected by the recipient or intermediary banks, but the transfers were quickly restructured and PPB attempted to send them again, the leaked documents reveal.

Alex Cobham, chief executive of the Tax Justice Network, an international non-governmental organization that lobbies for fair and open tax and finance systems, said he thought these “clearly questionable” transactions should have provoked compliance questions, especially after some of the transfers to Aleksin were rejected by banks.

“There should be a system in place that asks some questions, and they need to keep on asking those questions rather than let the transfers through when they try again [after some were blocked.]”

PPB’s current managing director Eimantas Kazlauskas did not comment on the due diligence reviews carried out specifically on the Wallitus transactions, but said failed transfers should not “be treated as establishing wrongdoing or a deficiency in due diligence.”

Kazlauskas said the bank could not comment on specific clients or transactions due to banking secrecy requirements, but noted that PPB’s relationship with Worldclear was terminated in 2018. He said the bank’s current owners and managers assumed control of PPB after the transactions mentioned in this article.

Worldclear founder David Hillary said neither he nor Worldclear had ever “knowingly or recklessly facilitated criminal offending, acted for the purpose of assisting any person to commit an offence, or designed or operated services for the purpose of concealing the source, destination, or beneficial connection of illicit funds.”

Aleksin did not respond to a request for comment.

Lawyers for Kavaliauskas, PPB’s owner at the time of several of the transactions, said he “vehemently denies any allegation” that he assisted in any financial crimes, noting that their client “has never been so much as questioned by any relevant authorities.”

‘Compliance did not give approval’

Using documents from the Worldclear leak and additional leaked records from PPB, reporters were able to analyze precisely how transactions were made from Wallitus to Aleksin.

The files show that after Wallitus initiated a transfer from its PPB account to Aleksin, they sometimes passed first into one of Worldclear’s accounts at mainstream banks. Worldclear then sent the money via an intermediary — a so-called correspondent bank — to Aleksin’s personal account in Belarus.

In total, Wallitus sent at least US$3.4 million to Aleksin’s personal account, more than half of which was sent via Worldclear accounts. Each transfer was marked as a "loan repayment" connected to a 2015 agreement, found among the leaked Worldclear records, in which Aleksin issued a US$13.1 million line of credit to Wallitus.

![]()

The purpose of the original loan agreement between Aleksin and Wallitus was vague, with the agreement describing it as money for "financing day-to-day expenses of the borrower.” It was also originally interest-free, prompting Martin Woods — who has worked in banking compliance, as a police detective, and as a fraud and anti-money laundering investigator — to question whether the loan was a genuine business transaction based on standard commercial logic.

“If it’s got no interest, [Alekin’s] losing money,” said Woods. “It doesn’t appear to be a logical transaction.”

PPB’s current managing director Kazlauskas said it was not the role of the bank to understand the reasons behind a client’s arrangements or “whether the client should enter into a transaction in the first place,” but rather to “assess, review, process, decline, suspend, report, or otherwise deal with payment instructions” according to applicable laws and regulations. He said questions about the “commercial rationale” of arrangements should be directed to PPB’s clients. Lawyers for Kavaliauskas said he was “never involved in the operational activities of PPB,” and Aleksin did not respond to requests for comment.

While the first three transfers from Wallitus visible in the leaked records, all in 2017, seemed to go smoothly, other banks blocked payments in early 2018:

- In January 2018 a transfer of US$629,569, sent directly by PPB to Aleksin, was “rejected by the beneficiary bank,” according to PPB records, without specifying which bank declined the transfer. The leaked files show that the money was converted to euros and sent again, this time via Worldclear. It was successful.

- Then, in late February, PPB used Worldclear to try to send €565,671 to Aleksin on behalf of Wallitus. The leaked bank records show this was blocked but there was “no reason provided.” A day later, PPB tried to send an almost identical amount, directly this time, but the funds were returned again. This time the leaked bank records indicate the intermediary bank had identified a compliance issue: They list the returned amount alongside the note “correspondents [sic] compliance did not give approval,” without providing further details.

- In late March approximately the same amount — around €565,000 - was sent to MTBank on behalf of Wallitus again. Once again, PPB used Worldclear. This time, however, there were two differences: the amount was split into two payments, and the money was sent to Wallitus’s own account at Aleksin’s MTBank, rather than to Aleksin’s personal account. The transfers were successful.

PPB’s Kazlauskas did not comment on these specific failed transfers, but said “it should not be assumed…that relevant review, assessment, escalation, or internal procedures did or did not take place in connection with any particular sequence of events.”

While Worldclear was transferring money on the instructions of PPB, the leaked records from the New Zealand firm include references to Wallitus in transaction-tracking spreadsheets, showing it knew the identity of the ultimate client.

It's not clear what, if anything, Worldclear knew about Wallitus, Aleksin, or the transfers it was processing, or whether it routinely carried out due diligence on PPB clients for whom it was moving funds or even knew their identities.

The New Zealand Department of Internal Affairs report that found Worldclear to be lacking on anti-money laundering measures criticized the financial services provider for relying too heavily on due diligence carried out by its own banking clients, though the report did not make specific mention of PPB, Aleksin, or Wallitus. (Hillary strongly disputed the accuracy of the report’s findings. He did not respond to follow-up questions about Worldclear’s due diligence processes).

US attorney, former banking regulator, and anti-money laundering expert Ross Delston said he thought the transactions could be “a classic example of layering, which means using multiple banks and multiple corporations to hide the origin, to hide the source of funds.”

Kazlauskas defended PPB’s use of Worldclear, saying the New Zealand firm “operated as an aggregator of correspondent banking relationships” and “maintained relationships with major New Zealand banks.” Lawyers for former PPB owner Kavaliauskas reiterated that he “denies…in the strongest possible terms” any suggestion he facilitated any wrongdoing.

‘Abnormal contracts’

For each of the loan repayments Wallitus sent, or tried to send, to Aleksin, it had days earlier received an almost identical amount from the Cypriot company Sumsteg. These transfers were marked as repayments for 2015 and 2016 loans from Wallitus to Sumsteg.

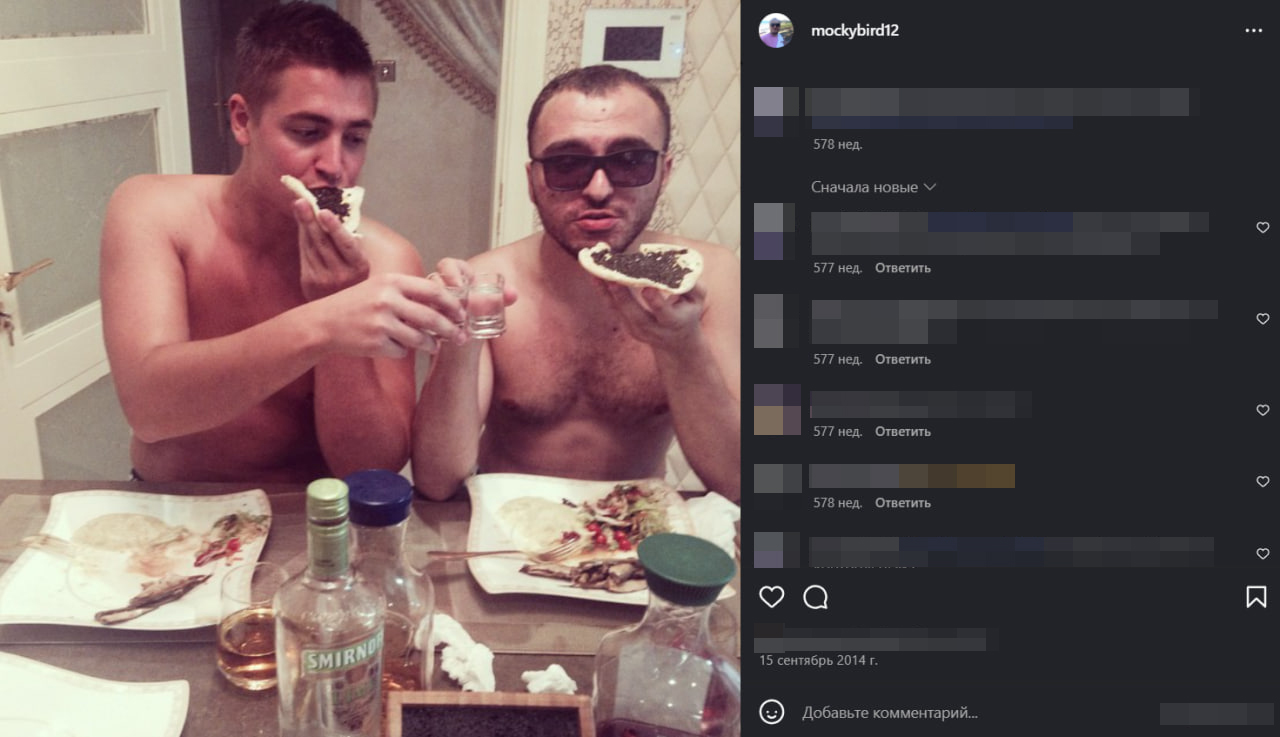

Sumsteg’s owner shares personal ties with Aleksin’s family. Mekhti Mekhtiev is an Azerbaijani-born Russian businessman who was a friend of Aleksin’s son Dzmitry.

Social media posts show Mekhtiev attended Dzmitry’s wedding, while a photo from 2014 showed them bare-torsoed, tucking into black caviar with vodka. Mekhtiev has also flown on a private jet with the elder Aleksin, flight records show.

Mekhtiev did not respond to a request for comment.

Between 2015 and 2019, Sumsteg signed 18 deals worth more than US$300 million to supply petroleum products to Aliaksei Aleksin’s Energo-Oil and Belneftegaz. (Both companies were sanctioned by the US in 2021. Neither responded to a request for comment).

But Sumsteg’s self-declared principal business activity, its owner, and the nature of the contracts raise questions over the real purpose of the deals with Aleksin’s energy firms – and the flow of funds between Sumsteg, Wallitus, and Aleksin.

Despite signing deals worth hundreds of millions of dollars to provide petroleum products, Sumsteg’s financial statements describe its main business as “provision of financing” and acting as an “agent for financing,” not an oil supply company. Yet, several contracts say that Sumsteg is the “seller” of the goods, rather than any sort of broker.

The contracts it signed with Aleksin’s companies typically required 100 percent payment in advance, and notably 17 of the 18 contracts reviewed by the Belarusian Investigative Center were then cancelled.

Mikhail Krutikhin, an expert on the oil and gas market, said the cancellation of multiple contracts was “abnormal.”

“Balance reconciliation” documents obtained from within Aleksin’s energy companies show they tracked a flow of funds between themselves and Sumsteg. In at least one instance, it appears Sumsteg returned a contractual payment to one of the energy firms.

Internal documents from the last quarter of 2019 set out amounts that Sumsteg owed to Belneftegaz and Energo-Oil — US$9.4 million and US$42.4 million respectively — listed in a table and marked “liabilities.” The Belneftegaz figure correlates with a March 2019 contract it signed with Sumsteg for just over US$9.5 million.

One of the internal documents, dated December 21, 2020 shows Sumsteg returned US$9.37 million — almost exactly the total amount of “liabilities” set out in the “balance reconciliation” — to Belneftegaz in 2020. (Reporters could find no such record for Energo-Oil in the leaked data).

It’s not clear from the leaked documents whether Aleksin’s energy companies made contract payments to Sumsteg in every case, or if Sumsteg returned payments to the Belarusian companies every time a contract was cancelled.

Cobham from Tax Justice Network said that while there could be a legitimate basis for the transactions involving Sumsteg, Wallitus, and MTBank, Sumsteg’s ownership and the questions over the petroleum supply contracts all meant “a commercial justification is slightly difficult to see."

The countries involved could also have raised compliance questions from PPB, Worldclear, or correspondent banks, Cobham said, noting that Cyprus has often been used by Belarusian and Russian figures as a preferred offshore location “with conferred EU legitimacy" and that Vanuatu has a notoriously poorly regulated finance sector that is open to exploitation.

Sumsteg’s owner Mekhtiev also owned a United Arab Emirates-registered company which signed several similar supply contracts with Energo-Oil and Belneftegaz. When combined with the Sumsteg deals, the contracts inked by Mekhtiev’s companies were worth more than US$550 million.

Reporters were unable to obtain the UAE firm’s financial records, but they combed through Sumsteg’s financial statements from 2017 to 2020. The documents paint a picture of a company that existed on paper as a massive clearinghouse, with tens of millions of euros showing on its books, yet operating with very little commercial revenue.

Reporters found no evidence in the statements of significant income that could be indicative of payments from Aleksin’s firms, whether through contracts that were active or cancelled. Instead, it reported income from “interest receivable” on loans it had made.

The reports do, however, indicate significant sums were flowing through the company. They show it was issuing and repaying tens of millions of dollars in loans, while also recording tens of millions more as “trade liabilities” or “trade payables,” and “trade receivables” – funds the company owed to, or was owed by, another party.

For instance, in 2017 alone, Sumsteg granted over €94.5 million in loans and received €93.8 million in loan repayments.

In 2019, the company recorded a massive €48.1 million surge in trade creditors/payables, and a €37.8 million cash outflow related to a surge in trade debtors/receivables.

Aleksin and Mekhtiev did not respond to questions about the transactions or the relationship between Sumsteg and the energy companies.

Three men and a bank

The leaked documents reveal PPB also processed transfers for a businessman previously linked to Aleksin and Kavaliasukas, the owner of PPB until 2018 who was also identified in internal bank records as a co-owner of the Cypriot company Wallitus.

A 2012 investigation by OCCRP’s member centers the Belarusian Investigative Center and Siena revealed an arrangement involving Aleksin and Kavaliauskas related to the export of Russian oil to Europe via Belarus labeled as ‘solvents,’ evading import duties and generating billions in profits in the early 2010s. It also featured a third businessman, Lithuanian Vitold Tomaševskij, according to the Belarusian Investigative Center and Siena’s investigation.

Leaked compliance records from PPB reveal that one of Tomaševskij’s companies was a PPB client, and engaged in transactions whose legitimacy were questioned by finance experts.

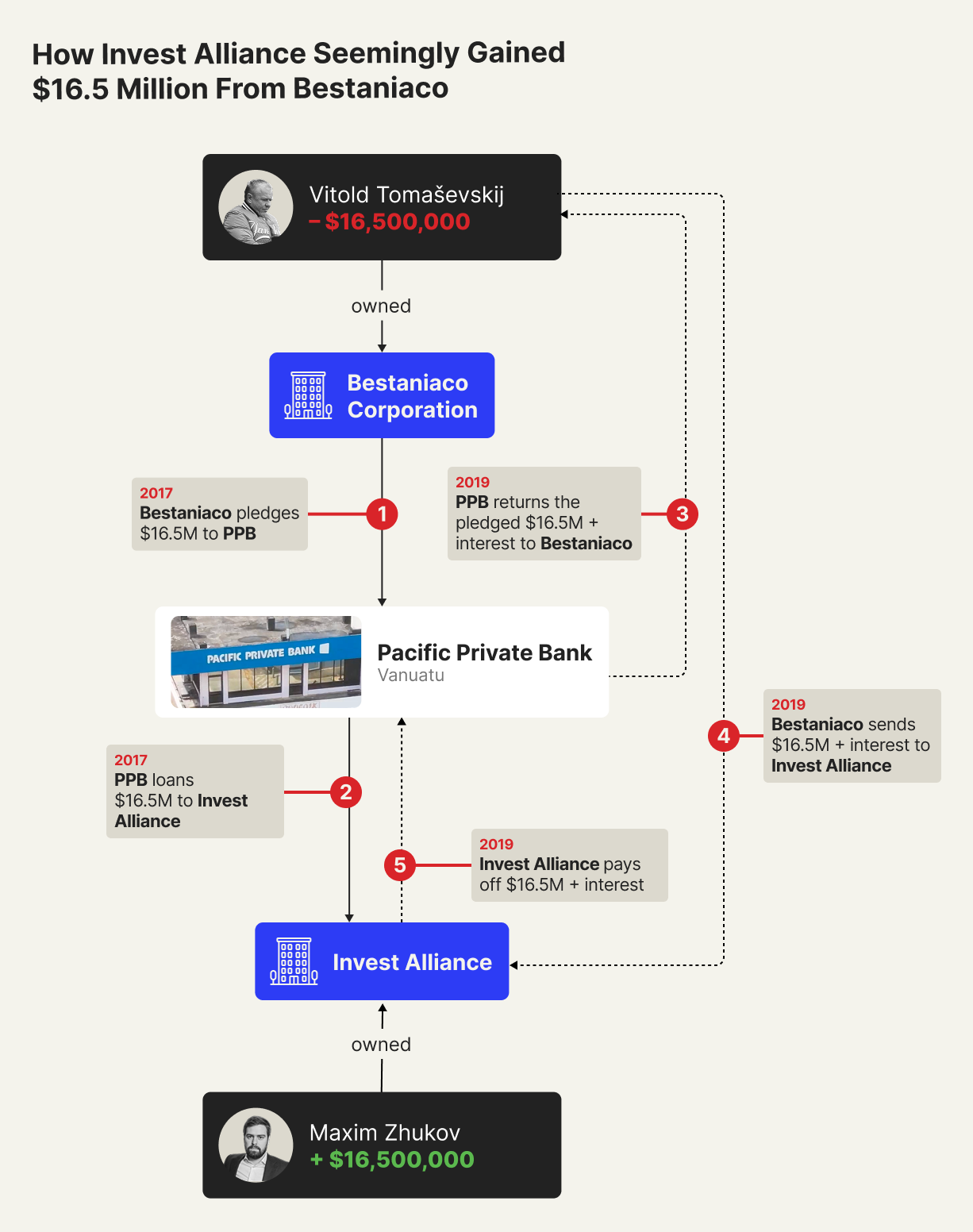

The PPB compliance records show that Tomaševskij was the owner of a company called Bestaniaco Corporation in 2017 and that during that time the firm pledged US$16.5 million as collateral for a series of loans from PPB to another firm called Invest Alliance in the British Virgin Islands. (The purpose of the loans and transactions is unclear from the leaked documents).

The transfers involving Bestaniaco and Invest Alliance substantially took place in August 2017. Leaked bank records show a flurry of transactions, whereby millions were sent to Bestaniaco, which pledged money to PPB to support loans to Invest Alliance, which then quickly moved the money to a bank account in Cyprus:

- On August 3, a company called EE Airport Holding — belonging to a firm that acted elsewhere as a nominee owner for Kavaliauskas — sent US$8.7 million to Bestaniaco under the terms of a loan agreement, according to bank records. (Lawyers for Kavaliauskas said he “has no relation to EE Airport Holding [or] Bestaniaco Corporation.”)

- A day later, Tomaševskij sent US$5.4 million to Air Flying Ltd, a company he owned, which sent the same sum to Bestaniaco.

- On the same day, Bestaniaco made a US$14 million term deposit — a kind of pledge to support a loan to another party — with PPB, which then loaned the same sum to Invest Alliance. (Leaked records show the money from Bestaniaco was to support the loan to Invest Alliance).

- On August 4, Invest Alliance transferred US$10 million from PPB to its account at Cyprus-based Promsvyazbank (PSB). A leaked Worldclear spreadsheet indicates PPB used the New Zealand firm to execute the transfer.

- On August 9, Bestaniaco pledged another US$2.5 million with PPB, which sent another loan of the same amount to Invest Alliance on August 16.

- Invest Alliance immediately sent the same amount, plus the outstanding US$4 million from the US$14 million PPB loan it received less than two weeks prior, to one of its Promsvyazbank accounts. Worldclear records indicate it was again used to send at least a part of the funds from Vanuatu to Cyprus. (There is no suggestion Worldclear had any involvement in or knowledge of the PPB transactions involving Bestaniaco and Invest Alliance, or the transfers between Bestaniaco and EE Airport Holding and Air Flying).

By the time the transactions were completed, Invest Alliance had gained US$16.5 million in loan funds, guaranteed by Bestaniaco. Two years passed before the debt was repaid to PPB – but the leaked files indicate PPB returned the pledged collateral to Bestaniaco, which then sent the same amount to Invest Alliance, which then reimbursed the bank. Invest Alliance therefore seemingly kept the US$16.5 million it had initially received as a loan.

It is unclear why multiple companies, term deposits, and loans were used to seemingly transfer money from Bestaniaco to Invest Alliance.

PPB compliance documents show Invest Alliance was owned by a man called Maxim Zhukov, but do not give other identifying information.

Reporters identified a Russian real estate businessman called Maxim Zhukov. They were unable to independently confirm this is the same Zhukov that owns Invest Alliance, but the Russian businessman had links to companies owned by PPB owner at the time, Kavaliuskas, suggesting it is the same man.

The real estate figure used Charter Jets, a private charter flight company partly-owned by Kavaliauskas. And Zhukov’s company, Invest Alliance, shared a contact address with the wealth management group Lewben, which Kavaliasukas owned until last year. The company’s contact person also appeared to be a Lewben employee.

Neither Zhukov nor Tomaševskij responded to requests for comment about whether they knew each other or about the purpose of the transactions.

Lawyers for Kavaliauskas noted that he sold Charter Jets in 2023, and said the company had always abided by all relevant laws and regulations. They did not respond to specific questions about his relationship to Aleksin, Tomaševskij, or Zhukov, but said he “does not have any interests, businesses or partnerships with any Russian and/or Belarusian companies or individuals.”

PPB’s current managing director Kazlauskas declined to comment on the specific transactions, but noted they occurred before the bank’s current management assumed control.

Cobham from the Tax Justice Network and a Lithuanian independent auditor both raised questions over the structuring of the loans.

Cobham said he thought pledging funds against a bank loan to Zhukov’s company was not the easiest way to arrange to lend funds.

“It may be a more standard way of [loaning funds] through a bank, but if you are based in Europe and you’re proposing to do this through a Vanuatu bank, if anything your legal protection is less,” he said. “It’s not clear that there’s any operational or confidence benefit, certainly no compliance benefit, from doing it this way.”

Auditor Vaida Kačergienė echoed Cobham’s questions about the arrangements, and noted that specific attention should be paid to “complex transaction chains involving financial or credit institutions without a clear economic purpose.”

“Where a financial institution functions merely as a transit point, this may indicate a risk that information about the movement of funds is being deliberately fragmented,” she said. “The addition of unnecessary intermediate steps may suggest a heightened likelihood of attempts to obscure the original source of funds or make it more difficult to identify the ultimate beneficial owner."

4 Comments

This series of articles justifies my subscription on their own.

The only slightly disconcerting things are that it details only a tiny fraction of the dodgy money flowing around the world and that I now can't help but wonder what purely local dodginess is going on.

These articles are but a glimpse into how the elite work, and the precise reason that the argument that wealth taxes for the ultra rich are not 'punishing success' but simply taking something back for the public good form those with such excessive wealth gained through not only success, but the ability to do the likes of the above to multiply their wealth at an unnatural and unfair factor compared to the majority.

Other versions of this story;

15min (Lithuania ) - https://www.15min.lt/verslas/naujiena/bendroves/zurnalistinis-tyrimas-k…

The Belarusian Investigative Center - https://investigatebel.org/en/investigations/aleksin-money-laundering-n…

The Organized Crime and Corruption Reporting Project - https://www.occrp.org/en/project/the-worldclear-files/leaked-files-rais…

Holy cow, such a money go round. All these claims nobody did anything wrong and "oh it was the last lot and we don't know anything" are all a bit rich. We really need an international money laundering agency that can just prosecute under international laws where these sorts of cross border transactions where a multitude of jurisdictions are involved make prosecuting near impossible. And they should have power to wind up companies and prosecute any level of management, past/present.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.