By Gareth Vaughan

S&P Global Ratings says it expects New Zealand's economy to recover faster than the Budget assumes, with its positive outlook on New Zealand's credit ratings supported by an expectation deficits may not peak as high, and large deficits might not be as prolonged, as the Budget indicates.

S&P notes the Budget's economic overview says the COVID-19 lockdown is easing faster than the Treasury’s assumptions with the COVID-19 Alert Level 3 restrictions removed sooner than expected. The Budget's main economic forecasts include one month at Level 4, and assume one month at Level 3, followed by the remainder of the year to March 2021 at levels 1 or 2.

However, with Thursday's move down to Level 2, we only spent 16 days at Level 3. Treasury assumes COVID-19 alert level restrictions constrain economic activity by about 40% at Level 4, 25% at Level 3, 10% to 15% at Level 2, and between 5% and 10% at Level 1.

"We expect New Zealand's economy to recover faster than the budget assumes, aided by the quicker easing of lockdown restrictions than assumed in the budget. This will support revenue growth and could lower outflows from the COVID-19 Response and Recovery Fund. Most of the weakening in the fiscal forecasts is because of COVID-19-related spending and not a substantial increase in ongoing expense measures," the credit rating agency said.

Anthony Walker, Director of Sovereign and International Public Finance at S&P, told interest.co.nz S&P expects the global economy to rebound faster than Treasury does, and pointed out there's potentially the equivalent of another 8% to 9% of Gross Domestic Product (GDP) in spending to come. That's because Treasury's main and alternative economic forecasts assume around $35 billion and $62 billion of fiscal support, respectively. This, Treasury says, reflects the uncertainty about the timing and nature of further fiscal support when the economic forecasts were finalised.

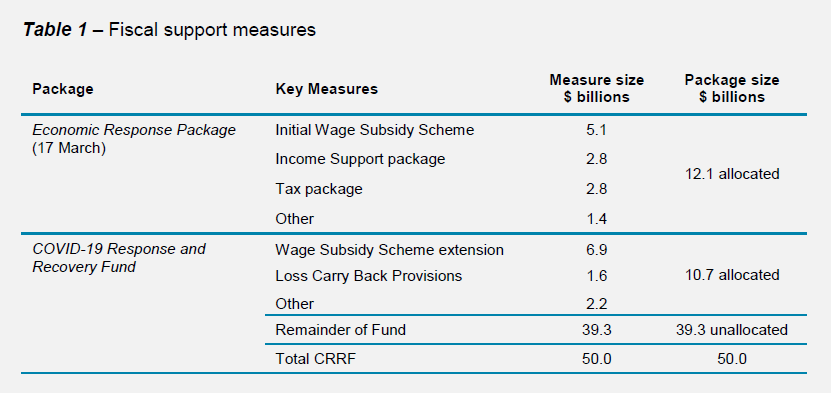

"The main forecasts include approximately $35 billion of fiscal support, including wage subsidies, other forms of business support, and increased expenditure on health and main social assistance benefits. This $35 billion includes the $12.1 billion Economic Response Package announced on 17 March, and a further $23 billion of assumed support from the Government’s CRRF [COVID-19 Response and Recovery Fund]. This leaves around $27 billion from the Fund for other initiatives," Treasury says.

If the $27 billion is spent this would "provide an 8% to 9% boost to GDP," Walker said. "If there's a recovery in 2022, 2023 or 2024 we're still comfortable with our positive outlook [on NZ's credit ratings]."

Separately S&P said the Budget shows NZ's finances will be hard hit in fiscal years 2020 and 2021 before slowly recovering.

"The positive outlook on our ratings on New Zealand is supported by our expectation that deficits might not peak as high and large deficits might not be as prolonged as the budget indicates," S&P said.

"The COVID-19 pandemic, government response, and resulting effect on the economy and financial markets continue to evolve rapidly. We believe the economic and fiscal shock will be temporary and that outcomes will improve after fiscal 2021, though debt levels will remain elevated for some time."

Treasury forecasts a $28.3 billion deficit in the year to June 2020, versus a forecast as recently as December for a deficit of only $900 million. It forecasts deficits across its entire forecast period, peaking at $29.6 billion in 2021 and falling to $4.9 billion in 2024. Net core Crown debt is expected to increase from 19% of GDP in 2019 to 30.2% in 2020, rising to 53.6% by 2023.

Meanwhile forecast government bond issuance for the year to June 2021 has been increased to $60 billion, six times more than forecast in December. Bond issuance is expected to be $40 billion in 2022, $35 billion in 2023 and $30 billion in 2024.

On May 4 S&P affirmed its ratings on NZ and maintained its positive outlook on the ratings. S&P has an 'AA' foreign currency rating on NZ with a positive outlook, and an 'AA+' domestic currency rating with a positive outlook.

"Our ratings on New Zealand reflect the country's monetary policy flexibility, economic wealth, and sound institutional settings. These strengths provide the country with flexibility to offset potential risks related to its large external imbalances, high household and agriculture sector debt, dependence on commodity income, and financial system stability," S&P said.

On May 4 S&P said:

The government's domestic lockdown, combined with a global recession, particularly for key trading partners China and Australia, will weigh on New Zealand's growth. We estimate the economy will contract 2.4% in fiscal 2020 before growing 1.7% in fiscal 2021 and 4.4% in fiscal 2022. China is a key trading partner, consuming roughly 25% of New Zealand's goods exports, mainly dairy, meat, horticulture, and forestry, and 14% of its service exports through tourism and education. Furthermore, travel restrictions will severely limit tourism and international student flows as well as migration levels, dragging on population growth.

Headwinds remain, with private consumption growth slowing from its highest levels in more than a decade and business investment staying weak due to the COVID-19 outbreak, policy uncertainty, and geopolitical issues.

While there continues to be a high degree of uncertainty about the rate of spread and timing of the peak of the coronavirus outbreak, some government authorities are estimating late second to mid-third quarter 2020, which we've used in assessing economic and credit implications. As the situation evolves, we will update our assumptions and estimates accordingly.

New Zealand's free-floating exchange rate, which has depreciated sharply since mid-2014 and is down about 10% this year relative to the U.S. dollar, should support economic recovery. The agriculture sector, especially dairy, remains the key export of New Zealand.

National property prices and transaction volumes are likely to be subdued during the COVID-19 outbreak and lockdown as unemployment rises and potential buyers aren't able to inspect properties. Prices had begun picking up following interest-rate cuts last year after a period of stabilization since 2017. Risks to the economy stemming from high property prices and household debt persist. Credit growth appears to be playing a diminishing role in economic growth with household lending slowing. Recent financial history in other developed markets shows that rapid credit growth can lead to vulnerabilities to financial, fiscal, and economic stability if a dynamic expansion suddenly and unexpectedly slows.

*The table below comes from Treasury. CRRF stands for COVID-19 Response and Recovery Fund.

See credit ratings explained here, and there's more detail on NZ's sovereign credit ratings here.

6 Comments

Yup, no credibility left.

I wouldn't put too much faith in the people who failed to forecast either the dot com bust or the GFC.

I hope they are right, but it's just wall to wall assumptions that aren't proven so who knows.

It's amazing to see how fast 50 billion disappear in the air.

So, how much can we expect to be invested in NZ in the next 2 years by rich Americans and Investment Banks ?

About the same as they invested after the earthquakes?

That was close to zero.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.