Analysis by the World Gold Council.

Since the publication of our Why gold in 2025? A cross-asset perspective report earlier this year, much has happened on the policy front and in the broader economy. Uncertainties and vulnerabilities remain across geopolitical, fiscal, and trade domains.

Investors are particularly concerned about growth and inflation, creating a challenging situation for policymakers as the dual policy goals of the Federal Reserve are in direct conflict. With persistent fears of stagflation, gold has once again stepped into the spotlight, rising more than 50% this year.1

Importantly, the core reasons for considering alternative assets such as gold, as outlined in our May report, remain largely unchanged.

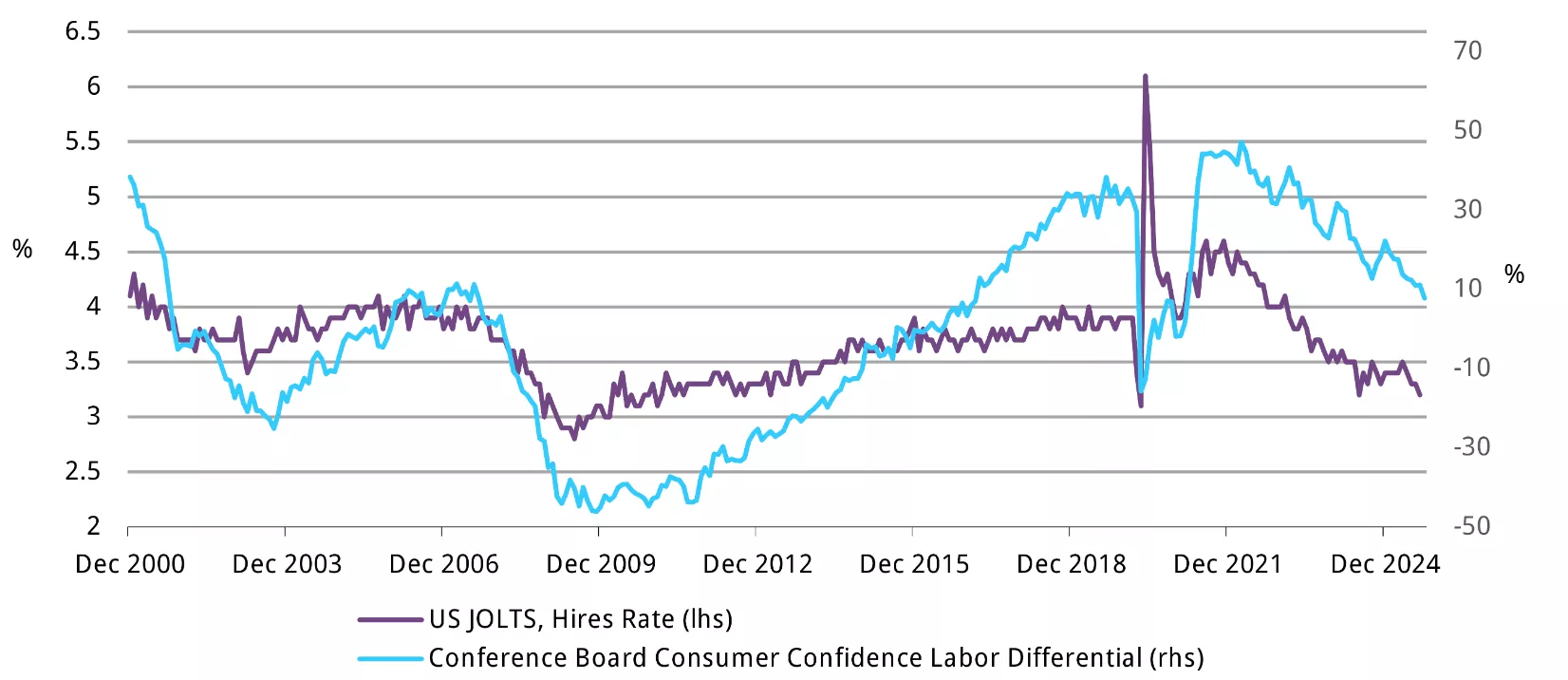

First, equities appear complacent. US equities have posted remarkable gains in recent months, reigniting concerns about valuation excess and concentration risk. Indeed, investors face a market that feels euphoric on the surface but remains fragile underneath. Should economic pressures mount (Chart 1), investors may increasingly seek refuge in safe-haven assets, with gold standing out as a historically resilient option, as outlined in our mid-year outlook.

Chart 1: The “slow hire” risks turning into a “no hire” narrative

US JOLTS, Hires Rate and Conference Board Consumer Confidence Labor Differential*

Source: Bloomberg, Bureau of Labor Statistics, World Gold Council

Second, bond markets remain uncertain. The Fed officially resumed its easing cycle in September, cutting the federal funds rate by 25 basis points in response to a cooling labour market (Chart 1) – an action widely anticipated by markets. However, US long-term yields could face renewed upward pressure if tariffs and reshoring efforts drive domestic costs higher, complicating the Fed’s inflation target. At the same time, long-term treasuries remain exposed to concerns over the Federal Reserve’s independence and the US government’s sizeable fiscal funding needs.

Against this backdrop, gold’s appeal as a hedge against both equity and bond market instability is growing – though risks exist. As we discussed in our recent blog, gold’s rapid ascent could prompt rebalancing and profit taking. For example, from a technical standpoint, the monthly Relative Strength Index (RSI) is above 90 and gold is sitting more than 20% above its 200-day moving average. These factors could lead to short-term reversals. In addition, the sharp increase in the gold price could dampen consumer demand while global trade normalisation and a pick-up in GDP growth could revive risk appetite further.

In summary, maintaining a diversified approach and remaining vigilant to shifting market dynamics is essential. Amidst a growing investor base, secular US dollar weakness and continued geoeconomic uncertainty, gold’s enduring resilience and diversification benefits remain as relevant as ever.

Footnotes:

1 As of 10 October 2025. Our Gold Return Attribution Model (GRAM) points to a combination of a weaker US dollar and a highly uncertain geopolitical environment as the reasons for the strong investment demand.

This article is a re-post from here.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here.

Comparative pricing

You can find our independent comparative pricing for bullion and coins in both US dollars and New Zealand dollars which are updated on a daily basis here »

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.