Financial markets struggle with uncertainty.

But they have a mechanism to 'price' the chance of future events. They do this using swap trades.

Banks tend to borrow short and lend long. Without laying off the risk of this mismatch, it would be a quick way to become insolvent and go broke. Banks don't go broke because they hedge their positions using financial instruments. There are many ways to do this and it is technical. But those mechanisms are highly effective.

However, if you are a saver or a borrower, you need to make a sensible decision about a financial decision that will play out in the future. You will almost always be unhedged. So the question is, how can you look ahead using the signals of the financial markets?

You can, but it isn't overly reliable. It is the future, after all. Anyone who 'knows' what will happen in the future is a charlatan, no matter how they couch it.

Money market participants struggle too.

One way to see how they price the likelihood of future events is to look at how they price the chance of an OCR rate change. We all know when those reviews will happen.

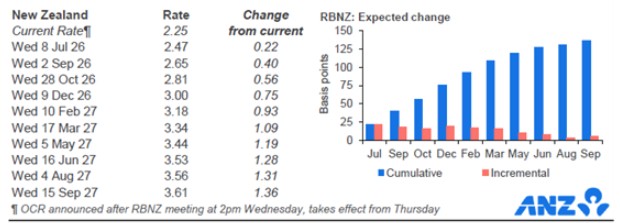

On Thursday, a day after an Official Cash Rate review, this is how the future is priced.

This is saying that by the December 9 Reserve Bank review, financial markets expect there to have been three 25 basis points rate hikes, taking the OCR to 3.00%.

(This is different to what economists and analysts assess. It is not unusual for them to be sceptical of market pricing.)

But that is only what they think today. It may change tomorrow. "Events" will happen and will alter this pricing.

![]()

The randomly chosen market pricing is in the rows for the OCR decision rates that are in the columns.

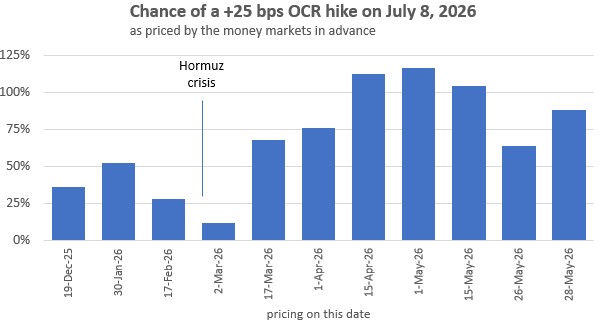

From this, we can track how financial markets shifted their pricing in the run-up to the May 27 'decision' for a July 8 OCR change.

And we can also see how they shifted their pricing for a September 2 OCR change. As of today, they now say there is an 88% chance we will get a 25 basis points rate hike then. Just before the Reserve Bank meeting it was only a 64% chance. The split decision and the Governor's briefing raised those chances, but to be fair as the inflation threats rose in April and May, those same chances were more than 100% in this market pricing. They have fallen back since.

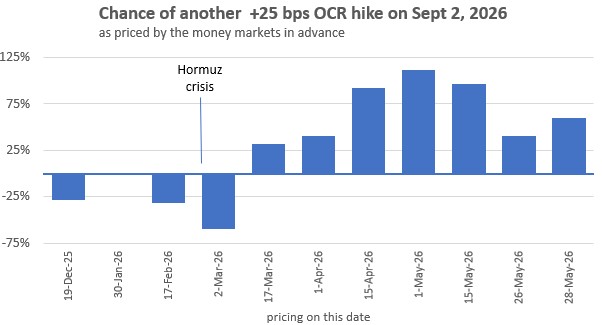

A similar pattern of shifting sentiment applies for another 25 basis points rate hike on September 2, although today's pricing has more uncertainty built in. The September decision is further out, giving more opportunities for more uncertainties. Again, an early May 100% chance has been scaled back.

The bottom-line point of this artilce is that even the professionals don't know when they have to put money on their pricing decisions. The oil crisis has made a decisive change, the inflation following from it added to it. But the scaling back since mid-May probably means something.

The next big test is the June 15 electronic card data and the June 16 release of the May 'selected prices' as an early indicator of inflation's latest track and whether there are signs it is being embedded.

If you are making a mortgage rate decision, or a term deposit decision, it may be helpful to be aware of this professional pricing. But equally, you should know that even the professionals are uncertain with where things are headed. You are on your own.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.