By Gareth Vaughan

The Reserve Bank is unlikely to enforce an industry wide rule for how banks would apply a haircut to the interest component of a term deposit under new rules for dealing with bank failures, potentially opening the way for savvy depositors to shift their savings to the bank pledging to freeze the least interest.

A spokeswoman for the Reserve Bank confirmed to interest.co.nz it's likely banks will be allowed to adopt an individual approach to freezing interest on term deposits in the event of a bank failure and the prudential regulator enacting its Open Bank Resolution (OBR) Policy.

"At this stage, it is anticipated that banks will adopt the approach which fits best with their existing systems, rather than an industry wide solution," the Reserve Bank spokeswoman said.

Banks operating different systems for the treatment of term deposits potentially means some banks may have different plans in place for the treatment of interest should the OBR policy be implemented on them.

This may effect the amount of money available to depositors, which some may want to factor into which bank they deposit their savings with.

Some depositors, especially those with big sums to deposit, may want to use the level of deposit interest a bank plans to freeze - or make available - as a bargaining chip in deciding which bank to deposit their money with.

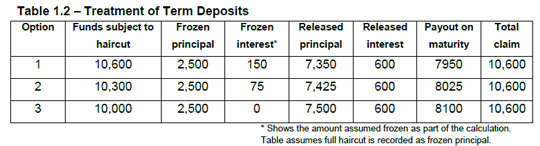

Meanwhile, the Reserve Bank spokeswoman's comments come after a submission from bank lobby group the New Zealand Bankers' Association on the Reserve Bank's IT pre-positioning for OBR consultation paper highlighted three options being considered by the Reserve Bank for dealing with term deposits (see table below).

The NZBA said there was "a level of support" for Option 2, - with interest accrued up to the date of statutory management subject to the haircut, but interest accruing after the date of statutory management not subject to the haircut.

In May the Reserve Bank revealed that it was delaying the deadline for banks to pre-position for its OBR policy by six months. It now says all registered banks with retail funding of more than NZ$1 billion, which ranges from the country's newest bank The Co-operative Bank to the biggest bank ANZ New Zealand, must have OBR functionality in place by June 30, 2013. The previous deadline was the end of 2012.

Effectively the the OBR policy will give the Reserve Bank a new tool it could use to deal with a bank failure. If implemented the policy is touted as allowing a bank to open for business on the next business day after its temporary closure following an insolvency event or it being put into statutory management, and being able to provide customers with full or partial access to their accounts and other bank services.

The key feature of the policy is that creditors - including depositors - are able to access a portion of their funds immediately after the bank fails and is placed in statutory management. The bank can quickly reopen with the unfrozen or accessible portion of funds guaranteed by the government to avert a further run by creditors. The idea is creditors' additional funds can be unfrozen at later dates as the final losses are determined.

Also in May Reserve Bank Deputy Governor Grant Spencer said the OBR policy should be seen as a complement, rather than a substitute, for the various “recovery plan” tools in the event of a bank failure such as living wills and loss-absorbing debt instruments.

Moody's sees less government support

Pre-positioning for the OBR policy means the banks must redesign their core banking systems, leading to suggestions it'll prove a costly exercise. International credit ratings agency Moody's Investors Service told interest.co.nz last year the OBR policy will mean there's less expectation the government would use taxpayers' money to bail out one of the country's major banks if it got into strife and more pressure on a bank's owners/shareholders to cough up in the event of a bank failure.

Such comments have led to suggestions bank credit ratings could be negatively impacted by the OBR policy, although Standard & Poor's has played this down, saying in its initial view the OBR policy won't be a significant imposition on its view of banks' financial strength.

A Reserve Bank cost-benefit analysis, which it says points to a significant net benefit from the OBR policy, is due to be released soon. Meanwhile, the Reserve Bank says it will consult on the introduction of a new banking standard to cover pre-positioning for the OBR policy later this year.

'All unsecured creditors to be treated equally'

The Reserve Bank spokeswoman says it's intended that under OBR all unsecured creditors will be treated equally. However, policy work is "ongoing" about the precise treatment of derivatives. She noted a distinction between being pre-positioned and being subject to a haircut in the event of a bank failure.

"All unsecured creditors are intended to be subject to the same haircut. The pre-positioning is to ensure that customers (i.e. depositors and small businesses) have access to the non-frozen portion of their funds as soon as the bank re-opens, so as to minimise disruption in the wider economy as much as possible. The statutory manager will release the non-frozen portion of the remaining liabilities (i.e. wholesale funding) in due course," she said.

Covered bonds, meanwhile, will be beyond the reach of a statutory manager.

"Moreover, covered bond holders are secured creditors, and would be expected to look to their security in the first instance. To the extent that their security is not sufficient to cover their claim, they would become an unsecured creditor of the bank (through the dual recourse of covered bonds). This remaining claim would be subject to the same haircut as all other unsecured creditors, and would be released by the statutory manager in due course."

This article was first published in our email for paid subscribers this morning. See here for more details and to subscribe.

12 Comments

So bank failures are a definite, just a matter of how we divvy the spoils, and who gets to wear the losses.

That's my view of it.

What is a bank's pledge worth once it is subject to OBR? The gist above is that there will be a cap on losses if predetermined % owings are made available - a part guarantee by Government irrespective of the level of problem? Hmm no wonder the systems don't need to be in place until mid 2013. Savvy investors won't want bargaining chips, they won't be investing in TD's if they can help it.

I always thought that if you took a haircut, you took a loss, yet it appears that a haircut is the frozen portion to be released later?

The same people designing this monstrous cash grab are the very ones charged in the past with the responsibility of regulating this unfolding fiasco.

I believe they need to be rigorously tested to evaluate whether they are fit for purpose as one would test an alcoholic - the increasingly obvious failure of global regulatory agencies to say no to debt requires such diligence by the saner members of the community.

The glib comments from the RBNZ spokeswoman reflect indefensible detachment from the catastrophic consequences planned by her incompetent superiors.

How will the nation withstand the loss of savings at any haircut level? How do we collectively take care of those diasbled from normal spending functions required to survive? Not one of these questions has been answered or possibly been asked so the public can review their acceptance of the planned draconian measures.

Banks should be banned from cosy, cuddly type national advertising campaigns and directed to warn us of the dangers ahead as we do with those that consume excess alcohol or smoke cigarettes. There is no other way to bring the public up to speed prior to the near backdoor introduction of what I perceive as legalised theft.

So now its down to risk management of your deposits. Hmm we need Bernard to give us a guide to the most likely banks to fail. Unfortunately that wont be good for advertising revenue.

Im going with the BNZ first, they are running around in the farm sector without a clue, if they have the same level of expertise regarding the rest of their loan book they are doomed.

Then I think its going to be ANZ-National or are they too big to fail?

ASB must have a high risk level as well as Westpac. Hmm which is the best horse in the glue factory?

Rabo? I see they have been caught up in the Libor scandal. They are tough to get a loan off, much harder than the others and because they purchased Wrightsons loan book, they got some top clients when they first came to NZ. Then they did lend to Crafar, so thats a big black mark but they are not exposed to housing big tick there.

So lets see, Hmm, I'd rank them in this order

BNZ

ANZ-National

ASB

Westpac

Rabo

I think the best option is to take your deposits elsewhere while you can, currency controls are coming. Its obvious the government doesn't have the resources to backstop depositors. The RB has failed its one roll to safe guard our banks, or should I say save us from ourselves? We pay the head honcho 600k a year for what?

I think Stephen is best qualified to rank banks.

Save us from ourselves, our own pollies and the OZ owners....RB for me is the whipping boy...

Currency controls, yes probably, however this is a world crisis, just where do you go? If say you put the money in the UK, exporting it again or getting it out of a uk bank could be impossible for a non-resident....

Interesting that you didnt list kiwi and tsb, also possibly co-op. What Id like to see is the exposure each bank has to each sector. So for instance if say co-op has no farming or business exposure but high household and say TSB is the opposite, it may make sense to have internet transfer accounts at both banks....Also the covered bonds thing, kiwibank has none.....maybe able to end up with a cross referenced matrix or risks and this would tell you where to go.....of course the banks maybe all lemming like and there is no difference.

regards

Whatever the ranking Andrewj - people are out in the streets of Spain - just as they will be here if our leaders get their way.

Once again, The Best Content This Site Produces is in the posts of Stephen Hulme and Andrewj.

Who do you find to watch the watchers? The only alternative that springs to mind is steve keen/minsky that consider debt to be an issue....most toher economits dont...

regards

This is inflationary!

Intelligent people will be wary of term deposits.

Maybe we should spend money now rather than save for the future.

(Saving runs the risk that your savings will be halved)!

Will kiwisaver accounts have their cash portion similarly afflicted?

Eeeeeek!

To see what NZ could look like regarding unsecured creditors, read Jeremy Warner's article on Spain yesterday in the Telegraph. NZ's treatment of unsecured creditors (including term deposit holders) could, in crisis, lead to the predicament of Spain's unsecured creditors in Spanish banks.

http://www.telegraph.co.uk/finance/comment/jeremy-warner/9393587/Proud-…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.