By Gareth Vaughan

In the current low interest rate world, investors with an appetite for risk can earn close to 10% on "junk" bonds issued by Graeme Hart's packaging empire.

Hart's Reynolds Group Holdings is paying interest rates of up to 9.8% on just shy of US$18 billion (about NZ$22 billion) of debt it's carrying with the vast bulk of the debt, denominated in the US dollar and euro, not due to start maturing before 2016.

As reported by interest.co.nz on Friday, Hart's Reynolds Group Holdings had its "junk" credit rating downgraded by Moody's a notch to B3, with a stable outlook, giving it the equivalent of a Standard & Poor's (S&P) or Fitch Ratings B- rating. The new rating's regarded as "highly speculative." S&P followed suit on Saturday, New Zealand time, dropping Reynolds to B with a stable outlook from B+. The new rating signals a company "more vulnerable" to adverse business, financial and economic conditions but currently with the capacity to meet financial commitments. S&P's issue level rating on Reynolds' senior secured debt was cut to B+ from BB-, and its issue level rating on unsecured debt was downgraded to CCC+ from B-.

"We expect Reynolds to remain in compliance with its financial covenants, including a maximum senior secured leverage ratio (of 4 times or below) and minimum interest coverage ratio," S&P says. "We expect limited headroom under the minimum interest coverage as the covenant steps up from 1.65 times as of June 30, 2012, to 1.7 times at March 31, 2013, and steps up further to 1.75 times at March 31, 2014, and we would expect the company to take timely steps to obtain an amendment if necessary." See S&P's statement here.

In a recent filing to the US Securities and Exchange Commission (SEC) Reynolds says although downgrades to its credit ratings could adversely affect its ability to access the capital markets and/or lead to increased borrowing costs in the future, the interest rates on its current indebtedness wouldn't be affected.

Auckland-based Reynolds, the holding company for Hart's global operations manufacturing and supplying consumer beverage and food service packaging products, has been put together by the leveraged buyout king since his 2006 acquisition of Carter Holt Harvey. Reynolds spends about US$1.45 billion annually servicing its debt. The company has an array of bonds on issue. Here's a summary, including the interest rates they're paying, and when they're due to mature.

US$1,125,000,000 7.750% Senior Secured Notes due 2016;

EUR 450,000,000 7.750% Senior Secured Notes due 2016;

US$1,000,000,000 8.500% Senior Notes due 2018;

US$1,500,000,000 7.125% Senior Secured Notes due 2019;

US$1,500,000,000 9.000% Senior Notes due 2019;

US$1,500,000,000 7.875% Senior Secured Notes due 2019;

US$1,000,000,000 9.875% Senior Notes due 2019;

US$1,125,000,000 9.875% Senior Notes due 2019;

US$1,000,000,000 6.875% Senior Secured Notes due 2021, and;

US$1,000,000,000 8.250% Senior Notes due 2021;

Reynolds' subsidiary, the Luxembourg domiciled Beverage Packaging Holdings, also has debt listed but not traded on the Irish Stock Exchange. This is in two tranches, being €480 million of senior notes paying 8% that are due to mature in 2016, and €420 million of senior, subordinated notes paying 9.5% that are due to mature in 2017.

Reynolds' half-year financial statements show an equity deficit of US$131 million and a half-year profit of US$8 million (versus a loss of US$104 million in the same period of last year), on revenue of US$6.9 billion, which was up US$1.7 billion, or 32%, to US$6.9 billion. Net financial expenses rose US$129 million, or 24%, to US$667 million. The group's total debt is equivalent to 6.2 times its proforma, adjusted half-year earnings before interest, tax, depreciation and amortisation of US$2.7 billion..

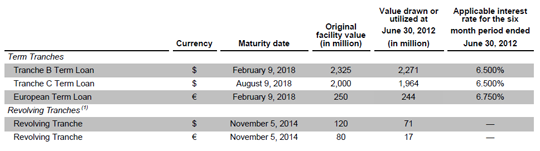

Here's the bank debt:

With global manufacturing operations centred around the United States and Europe, Reynolds has exposure to numerous currencies and several raw materials.

"Although our reporting currency is US dollars, we operate in different geographical areas and transact in a range of currencies in addition to dollars. Our other transacting currencies include the euro, the Brazilian real, the British pound, the Canadian dollar, the Chinese yuan renminbi, the Japanese yen, the Korean won, the Mexican peso, the New Zealand dollar, the Polish zloty, the Russian ruble, the Singapore dollar, the Swiss franc, the Taiwanese dollar and the Thai baht," Reynolds says.

Its manufacturing operations use a range of raw materials such as resins, aluminium, fibre - principally raw wood and wood chips - and paperboard - notably cartonboard and cupstocck - commodity chemicals, steel and energy, including fuel oil, electricity, natural gas and coal.

Pension shortfall

Meanwhile, an SEC filing from Reynolds dated July 10 notes that, as of December 31, 2011, its subsidiary Pactiv, the maker of hefty garbage bags, has a US pension plan that was under funded by US$892 million. Reynolds says the Pactiv pension plan is its biggest one.

"Subsequent financial market performance and decreases in interest rates may have significantly increased this deficit. Future contributions to our pension plans, including Pactiv's US pension plan, could reduce the cash otherwise available to operate our business and could have an adverse effect on our results of operations," the Reynolds filing says.

"In addition, certain of our businesses participate in various multi-employer pension plans administered by labor unions representing some of our current or former employees. We make periodic contributions to these plans, and if we withdraw from participation in these plans, we could be required to make an additional lump-sum contribution to the plan. If other participating employers withdraw from these plans or become insolvent, our liability could increase. Some multi-employer plans, including some of those in which we participate, are reported to have significant under funded liabilities, which could increase the size of our potential withdrawal liability."

This article was first published in our email for paid subscribers this morning. See here for more details and to subscribe.

8 Comments

why is this guy only paying 10%

a low income family with a loan at instant finance is paying around 29%

i know which one is more likely to repay the full amount and it's not mr hart

this is why our financial sysem is in the poo and it sure smells bad

Well I guess its why he is worth a lot (apparantly) and you are and I are not.

regards

NG - ah you are onto something. On a 12 month contrcat for say $299m. the differnce bewteen say IF rates 25% and bank rate say 9% is only 0.53m!

Weekly Payments over 12 months

Amount $299m at 24.9% IF rate - weekly = $7.71m

Amount $299m at 8.9% Bank rate - weekly = $7.18

kane you may need to check your maths???

HG this is straight out of a reputable bank handbook.. The finance rate on a reducing balance loan is virtually irrelevant over such a short term

HG this is straight out of a reputable bank handbook.. The finance rate on a reducing balance loan is virtually irrelevant over such a short term. I get :-

=pmt(.249/52,52,-299,0,0)=6.51

=pmt(.089/52,52,-299,0,0)=6.01

Amounts slightly different. Result is same. ie the difference is negligible

and what about safety?

Right now there is 9 trillion or so in US treasuries alone with in effect a negative return.....surely that should be telling you something about the level of risk some number of investors feel.

regards

Okay , so Hart is really like almost every other Kiwi, as long as he can service the debt he is sweet ,. Even if we are a few month's cashflow away from trouble.

In reality , if his cashflow dries up he is in the same position as a Tongan in Mangere who loses his job.

The only dfifference is that Hart is quite adroit

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.