By David Chaston

Interest rates are on the rise, especially short term rates.

Westpac reviewed this trend recently.

But we want to take another look, especially to put New Zealand rises in context, and to assess where this recent shift is going.

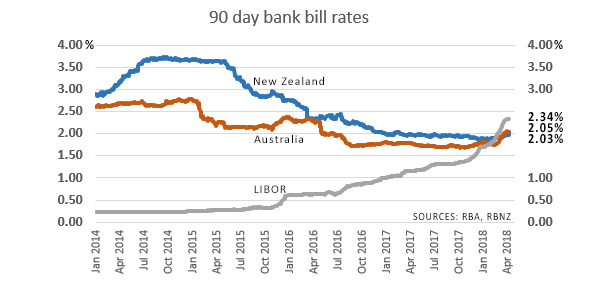

It all starts in international markets. There has been a relentless rise in three month LIBOR rates starting in 2016, but getting new impetus in 2018.

These trends are now spilling over into local rates.

In fact, the premiums New Zealand rates have been at to both LIBOR and equivalent Australian rates have been turned on their head.

We now have rates that are at a discount to both those international references, something that is very unusual indeed.

In the past we have been comfortable knowing that local bank treasurers could borrow offshore at cheap rates and swap those funds back here on wholesale markets. While that never resulted in low international rates converting to domestic rates, it did set a floor.

But the recent switch means that it no longer makes sense to source short term money from offshore because it is now more expensive.

It is an unusual double-take for us to see that funding is now less expensive locally.

The domestic influences

So local supply and demand pressures will now set the tone for these rates. And that means local loan demand is now a more important influence.

We know that bank funding from domestic sources (household and business bank account balances including term deposit balances) are growing strongly and keeping 'supply' lines well filled. These are up +6.5% in the year to February. See RBNZ data series S40. The household portion of that growth is up +7.1%.

And we know loan demand is growing more slowly, up only +5.2% in the year to February. See RBNZ data series S30.

Percentages are one thing, but in dollar terms we are nearly at the point where the dollar growth in loans (+$21.5 billion) is being matched by the annual dollar growth in local funding (+$20.0 bln).

And that means on an overall basis, local pressures are not strong enough to press local rates higher.

The offshore influences

The rise in LIBOR rates is underpinned by the US Federal Reserve rate rise track.

The rise in Aussie rates may also have to do with repo rate demand, including demand from Japanese investors chasing yield.

But for us, we are in an unusual situation where the impact of domestic forces - deposit growth and loan demand - now are more important factors that the availability of offshore money, especially for short term needs.

The outlook

Any sag in local loan demand may put downward pressure on deposit rate offers. Conversely, any pick up in loan demand could quickly translate into rising deposit rate offers, and rising loan rate costs.

But it is important at this point to understand these are still primarily pressures at the short end of the local money markets.

However, we are seeing signs of fixed rate mortgage increases for 12 and 18 month durations. If these international trends keep rates rising and they affect our two year swap markets, then the impact felt will be more widespread.

And don't forget, the variable rate lending in New Zealand is where SME loans are targeted, and other business lending tends to be tied to short-term benchmarks. New Zealand business enterprises may feel the impacts sooner than homeowners.

6 Comments

David, you start this article with: "Interest rates are on the rise, especially short term rates."

However you also wrote an article today, entitled " Two banks drop their 2yr mortage offers" https://www.interest.co.nz/news/93178/both-asb-and-bnz-announce-lower-t…

...?

This article makes it clear that the primary risks are for businesses and others who borrow based on floating/short-term rates. (But ASB did raise home loan rates for 12 and 18 month terms today.)

When we talk about short-term rates, these are for terms of less than one year.

Thanks DC

It looks like LIBOR rates started rising in 2015, well before the Fed rate rises. They are now well ahead of the Fed rises, presumably this is pressuring those companies and countries that have borrowed in USD. So far we have a collapsing Ruble and Turkish Lira, but if past episodes are anything to go by, there should be some big defaults and broken currency pegs coming sometime not too far away.

... we are as Dorothy in Kansas , in " the Wizard of Oz " .. ... within the calm and serenity of our familial home , looking out the windows to see the tempest roaring outside .... witnessing the ravaging storms wrecking havoc , uprooting all in their wake ... we are uncomprehending to the devastation that is about to descend upon us ...

.. .. pat Toto , Dorothy ... pat the wee doggie whilst you still can ...

The " fun " is about to begin .....when the bond market in the USA sneezes ... it will be as if the 1918 influenza has struck once again ... all the borrowers .... all the property speculators .. All will fall down ..

It cannot happen!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.