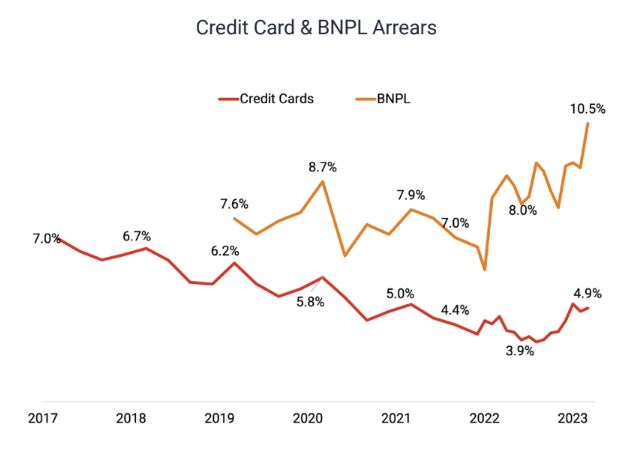

New information from the credit reporting agency Centrix shows people using buy now pay later (BNPL) schemes are drifting further behind on payments.

The latest numbers, till March this year, show the percentage of BNPL loans in arrears has risen to 10.5%. BNPL loans had been 7.6% in arrears four years ago and dropped lower than 7% in 2022.

However there has been a sharp rise in the rate of arrears over the last year to a record high.

Meanwhile there has been a steady decline in credit card arrears over the past six years but like BNPL, there has been an uptick in the past year from 3.9% to 4.9%.

The managing director of Centrix, Keith McLaughlin, agrees debt arrears have been generally tracking down since 2017 across all types of lending.

"That is because Kiwis generally want to pay their accounts. There has also been more responsible lending with more credit data available, so there has generally been a downward trend in arrears.

"But in the past seven to eight months, we have noticed that being reversed, almost across the board. We have now seen arrears start to increase and that trend really is the worry."

This rise in BNPL arrears comes as the Government moves to regulate these schemes.by bringing them under the ambit of the Credit Contracts and Consumer Finance Act (CCCFA).

BNPL schemes are currently exempt from the CCCFA because they do not charge interest. Instead, they make their money from charges to retailers and from the payment of late fees. The proposal under consideration is to apply affordability checks to BNPL loans over a threshold of $600.

Meanwhile there are signs that some BNPL customers are getting cagey. The total number of people seeking such arrangements has declined 15% in the past year, even as the people who remain in BNPL schemes get into worse debt.

In a parallel though lesser development, the number of telco and utility bills in arrears both rose over the past year but is still down on the levels of most of the past six years.

Meanwhile the business sector is definitely feeling the pinch. Loan defaults have risen 13% in a year for the construction sector, 12% in the retail trade and 10% in hospitality.

The property market continued to be impacted by the cost-of-living crisis, with mortgage arrears climbing for the eighth consecutive month to 1.31% in March. That amounted to 19,300 mortgage accounts past due. This was a big rise year-on-year but remains low by historic standards.

More dramatic was a 48% fall in new mortgage lending and a 15% fall in new mortgage applications.

Overall consumer arrears climbed to 11.8% of the borrowing population in March, meaning 427,000 people are behind on their repayments, Centrix says. That's up a little from 11.5% in February.

23 Comments

This is not a green shoots article............... More dramatic was a 48% fall in new mortgage lending

I don't know why mortgage arrears aren't mentioned in this article, as they were part of the Centrix data. From RNZ this morning:

The number of households behind on their mortgage repayments is up 26 percent on the same time last year, with 19,300 accounts past due.

Ouch. What makes it hard to read is that cafes, restaurants etc are still packed giving the illusion that there’s lots of cash around. Of course this hides the fact that there are probably many households not going out and spending but because we don’t see them it doesn’t register that there are people really struggling.

There is a lot of cash around, just not for everyone. Y shaped recovery in effect.

Winners are the young and old, losers are those in the middle with inelastic liabilities.

Yep.

I would add that cafes are probably doing well because they represent a ‘little treat’ that is pretty affordable ( if you just have a coffee and perhaps a small bite)

I don't think the likes of booze shops suffer much in a downturn.

There's a certain amount of products people say f it and buy anyway.

Booze shops suffer plenty. People still get their booze, they just stop paying for it.

You don't see too many going out of business.

Booze is quite price sensitive actually. If you can look at prices of beer from the 80s. It hasn’t moved much. Spirits have increased slightly but much of the increase in prices have come from adding perceived value i.e. boutique, special blend etc etc. It would be interesting to get brand data but I suspect their will be growth in both premium and budget offerings.

For sure.

It’s the bigger expenses that get whacked - houses, cars, appliances, furniture etc.

I wonder how domestic tourism will fare. I am a bit over the offering in NZ, expensive relative to quality. Just booked some accommodation in Japan, $270 per night for a five star hotel in Kyoto. The weather is too unpredictable in NZ right now too.

Once you pop on an international flight in the current airline pricing environment it equalises the costs somewhat.

Although flights to Japan in particular are looking pretty cheap in a couple months. Enjoy.

Thanks. Day to day costs are pretty cheap there too, eg. $10 for a bowl of ramen (versus $20 here)

Yep, it's a pretty low wage economy.

Japanese dont typically ask for pay rises.

It actually looks like there's quite a few people repatriating the countryside, you can get a house cheap or free there.

Chebbo, they are.

That’s a massive fall, doesn’t bode well for property prices.

Isn't the BNPL business model to have people in arrears so they can charge punitive fees?

So it's working how they want it to.

Pretty hard to fund a business model that relies on customer defaults. banks won't touch them, and investors will be nervous. Laybuy has just delisted from the ASX. Expect more BNPL Providers to fail.

If there is a 15% fall in new mortgage applications and a 48% fall in new mortgage lending that implies a lot of mortgage applications are being declined.

and/or the approved mortgages are smaller - i.e., falling house prices? Is that lending by number of people, or number of dollars?

Good question but either way it will still be a big discrepancy.

Who ever would have guessed it. People that can't afford stuff... can't afford stuff.

I had thought this was the beginning before xmas when arrears payments were ticking up. Who would have thought NZ could hold this back for so long. My interpretation being that NZers have not heeded warnings and altered spending behaviours in advance until it effects them directly e.g mortgage payments, savings depleting etc

For a mental model, let's break this down.

I purchase some nice brown leather shoes for $500 using afterpay from a shoe store. They borrow $375 plus interest after the initial payment of $125, which is paid through to the merchant. The merchant pays a 3-4% fee to afterpay (~$15 to 20) on the loan. If we consider they have to pay a Visa fee to take the payments (something like 1-2% maybe with a negotiated rate), it costs ~ 4*$1.25 or 4*$2.5 in visa/mastercard fees. The merchant is happy (despite decreased margin on that note), customer is happy. Afterpay then pays back that loan using the regular payments of their customers. So in theory, with no defaults, they make ~$15 to 20 dollars off a $375+interest rate loan. If we assume the loan rate is 0%, they make 4% to 5.333% as your profit ceiling. So after deducting interest on these loans, any default rate over 5% is definitely going to make you lose money.

Considering these services borrow money from banks to make these loans and effectively are just a new spin on payday loans, with default rates like this, I think it is likely these firms are effectively bankrupt. Given they make their profit off merchant fees (3-4%) and late fees, while paying above riskless rates for loans from banks which are probably above merchant fees. Not just that, but with a default rate of >5%, you are effectively losing moneys on every loan and hoping to make it up on volume. This is ignoring how many expensive accountants and software engineers are working on these products, what is the burn rate for these firms.

If it was possible to short the ASX and NZX for smaller guys (without brokers like Forsyth Barr or Jarden), I would be shorting the hell out of these firms. They are only viable in zero interest rate environments with next to no regulation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.