Here's our summary of key economic events overnight that affect New Zealand with news there are growing concerns about the global growth trajectory - and wobbles in the US. Both equity and bond markets are picking up on the vibe.

American retail sales softened last week, as monitored by the Redbook survey, a noticeable shift lower than the week before.

And US new home sales took an unexpected fall in March, down -12% below year-ago levels and a rather sharp fall-away from February levels. Higher mortgage costs are probably biting this corner of their real estate markets rather hard now.

After they fell in February, US durable goods orders were expected to rise in March, and they did. But not by as much as was expected. The miss however is more to do with timing of "transportation" orders (read aircraft) which can be lumpy. Other than that, March durable goods orders actually rose more than expected and are up +9.9% from the same month a year ago. Orders for capital goods are up more than +10%.

The Richmond Fed factory survey has held its level in April, but the Dallas Fed services sector survey has weakened slightly.

American consumers however remain upbeat in the context of 2022, although still not back to pre-pandemic levels. But given the global challenges, the 2022 levels are quite positive.

The US Treasury had a very well supported 2-year bond auction earlier today. But the median yield was 2.53% vs 2.30% at the equivalent event a month ago.

Singaporean industrial production fell hard in March and that was not expected. But it is becoming a data item that has some sharp and unexpected retreats on a regular basis.

In Malaysia there is an interesting real-time economic experiment underway. They are about to raise their minimum wage by +25% after a +25% rise over the prior three years. Will that aid consumer spending power? or just fuel inflation as low-paid job levels fall away? There is trepidation over the move.

The UST 10yr yield starts today lower by another -5 bps at 2.76%. The UST 2-10 rate curve is unchanged at +22 bps. And their 1-5 curve is little-changed at +81 bps. Their 30 day-10yr curve is steeper at +243 bps. The Australian ten year bond is now at 3.03% and down -1 bp. The China Govt ten year bond is up +2 bps at 2.85%. And the New Zealand Govt ten year up +2 bps at 3.62% and building on last week's rise.

On Wall Street, the S&P500 is down -2.4% in late afternoon Tuesday trade. Overnight, European markets were very mixed with London up +0.1% but Frankfurt was down -1.2% with its own late selloff. Yesterday Tokyo ended its Tuesday session up +0.4%. Hong Kong was up +0.3%. But Shanghai fell another sharp -1.4%. The ASX200 ended yesterday down -2.1% in sympathy with Shanghai. The NZX50 ended down -0.8%.

The price of gold starts today up +US$2 since this time yesterday at US$1900/oz.

And oil prices are back up +US$4.50 at just over US$101.50/bbl in the US while the international Brent price is now just under US$105/bbl. In Germany, their Economy Minister said his country has already cut its reliance on Russian oil enough to make a full embargo “manageable”. A full EU ban that would upend the global trade in petroleum. Meanwhile, Russia has cut off Poland from gas supply. Russia is having trouble selling its oil now.

The Kiwi dollar will open today softer again at 65.8 USc and another -¼c fall. Against the Australian dollar we are little-changed at 92.1 AUc. And against the euro we are marginally firmer at 61.8 euro cents. That all means our TWI-5 starts today at 72.8 and little-changed since where we left it yesterday.

The bitcoin price is down -2.5% from this time yesterday at US$38,399. Volatility over the past 24 hours has been high at just under +/- 3.6%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

84 Comments

US Tech stocks are down by more than 3%. World stock indices are in red. Are markets spooked, or have been roiled.

NASDAQ nearing -20% YTD.

Sell-off continues this morning against the Yen, pretty agressively too. Suggests some negative prospect for the NZD as a risk-on proposition.

I think people are starting realise what a messy position we're in, and that the scope for OCR increases may not be as wide as people thought. It seems like the swap rates are getting way ahead of RBNZ and mortgage rates may reach a point where lifting the OCR too much further isn't really possible without absolutely demolishing spending or confidence. So huge OCR hikes and appreciation of the dollar may not be the slam dunk people have been expecting, or hoping for in the context of battling imported inflation.

We're a small fish in a big pond. I don't think our actions are having much effect on the dollar, good or bad.

There is a bit of history with JPY/NZD and the Japanese love of forex as a defacto investment option that makes it an interesting pair to keep an eye on.

“without absolutely demolishing spending or confidence.” There it is, in a nutshell. True as that may be, just as true is this government’s and its agencies, dismal record of not reacting to anything until after it has happened.

Seems like housing - and probably too much consumption - is now utterly dependent on central welfare / wealth transfers to sustain it.

Interesting opinion piece in the Herald today by a macroeconomist professor - references how the RBNZ admits employment is higher than sustainable and that the OCR is still stimulatory AND unlike the US Fed, the RBNZ is deliberately breaking [driving a truck through] its agreement /legislated aim, ignoring the Taylor Rule in the process.

Hard to disagree with.

Yvil, your thoughts?

And oil prices are back up +US$4.50 at just over US$101.50/bbl in the US while the international Brent price is now just under US$105/bbl.

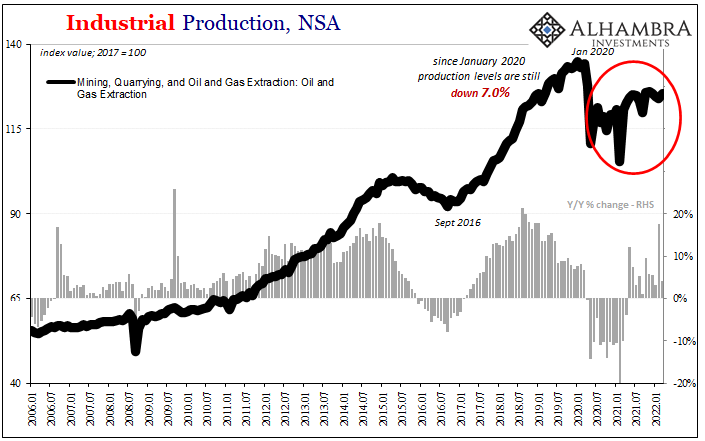

According to last week’s Industrial Production estimates for the month of March 2022, oil/natural gas output remains nearly 7% less than what it had been more than two years ago back in January 2020. Two years, rising prices, still less oil. Something beside the enthusiasm for Drill, Baby, Drill is clearly missing.

{kind=link}

It's fascinating to watch the big US oil producers at the moment. They are saying very clearly that they can only make profits when oil is above about $60 a barrel and they need to look after their capital investors by not increasing supply. To be fair, some of these investors lost a lot of money when oil prices nosedived a few years ago.

"Everyone says consumer prices and CPIs were caused by money printing when, in fact, the lack of money and global liquidity rather than anything else has prevented crude supply (above), thus created instead “inflation.” "

I've read some intellectually "twisted" stuff from Snider ( thks to Audaxes sharing ).... AND ..this takes the cake !!

Alice in wonderland logic... in my view..

In the context of his article, I think he is basically saying that money printing can be kind of ignored, it is the several other undrelying factors that is constraining the O&G output.

I hope you read the rest of the article, very good points and illustrations.

So called "money printing" undertaken by central banks is no substitute for global credit creation, or lack of, undertaken by banks. The former resides inert on central bank balance sheets, while the latter circulates in the community.

Three structural features of monetary systems form the starting point for this paper. They include (1) a two-layer structure comprising a private sector agent deposit system with commercial banks, parallel to a commercial bank deposit (reserve) system with central banks, with the two being separate and not allowing transfers between the two, that is, reserves cannot be “lent out” to the private sector (Sheard 2013); (2) the fact that money is created upon the creation of bank loans (Werner 2014/16) while repayment implies money destruction, both of which are an accounting reality, and implying that banks would better not be called “intermediaries”; and (3) the fact that the money stock is endogenously and elastically driven by demand and constrained loosely by regulation. The constraints to the provision of new credit include capital regulation, banks’ conditionality on an incremental profit prospect, and, eventually, demand (McLeay et al. 2014)1. Link

A recent Bloomberg article described central bank easing with the phrase “pumping money into the economy.” That’s a misconception. Monetary easing is actually an asset swap. The public was holding savings in one form, and now it holds it in another. The Fed buys Treasury securities from the public, and replaces them with currency and bank reserves (base money) that someone has to hold, at every point in time, until the Fed sells its bonds and retires the cash. All monetary policy does is to change the mix of government obligations held by the public. Only fiscal policy – specifically deficit spending – changes the total amount of those obligations.Link

The only thing you need to know about reserves: they go up, it's bad.

{kind=link}

Audaxes... The reality is that normal credit creation happens in normal times. Money printing is resorted to when there is a crisis, and private sector incomes are compromised...etc.

As Friedman says ( same article where Snider got his "interest rate fallacy " quote ) :

"The answer is straightforward: The Bank of Japan can buy government bonds on the open market, paying for them with either currency or deposits at the Bank of Japan, what economists call high-powered money. Most of the proceeds will end up in commercial banks, adding to their reserves and enabling them to expand their liabilities by loans and open market purchases. But whether they do so or not, the money supply will increase.

There is no limit to the extent to which the Bank of Japan can increase the money supply if it wishes to do so. Higher monetary growth will have the same effect as always. After a year or so, the economy will expand more rapidly; output will grow, and after another delay, inflation will increase moderately. A return to the conditions of the late 1980s would rejuvenate Japan and help shore up the rest of Asia."

https://www.hoover.org/research/reviving-japan

Also... I find the argument that monetary easing is an asset swap, and therefore means nothing ... kinda amusing. Its almost inane since , by implication, exchanging anything for money becomes, simply, an asset swap. eg.. buying a loaf of bread. ( The Baker does look on it as an asset swap. )

https://twitter.com/JasonEBurack/status/1518391482411008002?s=20&t=_HbW…

Its a real laugh when the states government rags on O&G for years and pushes through plenty of prohitionary and limiting policies, just for the global energy supply network to be majorly disrupted and then expect rigs to magically start pumping.

As the above link points out, one limiting factor is the cost and availability of steel piping.

These sorts of projects have a lag time of months to years.

Oil and gas received US$427 billion in direct subsidies in 2020 according to a study from the IMF, and another $5.5 trillion in indirect subsidies. How they are ragged on, the poor blighters!

The World Bank and just about anyone else with any sense can see pressures and wild swings on energy and food prices persisting for the next 2 - 3 years. Indonesia just decided to stop exporting palm oil to keep prices down for their people (that's not good for everyone else by the way).

Meanwhile brave little NZ setts out to tame the global price-storm by hiking rates and encouraging banks to push mortgage rates to the moon ahead of further rate rises. Meanwhile, Govt fiscal stimulus plummets, and the billions of dollars of Govt spending has got stuck in the savings accounts and paid down mortgages of the wealthy.

Before anyone jumps on me and tells me that 'low rates are evil, unnatural, look at the inflated housing market etc' - my view is that the rise to 1.5%; the aggressive signals to go further that is pushing mortgage rates; collapsing confidence; and high prices for imports have already baked in a huge slowdown. The way to a 'soft landing' now involves signaling clearly that rates will be left where they are for the next 6 months. Anyone pushing for rate hikes in this environment has a fetish for unemployment queues. If we want to deflate the housing market - just do something targeted - e.g. mandatory landlord licensing and rent caps for houses that don't meet healthy homes standards, coupled with compulsory purchase of land that is banked.

Meanwhile, Govt fiscal stimulus plummets, and the billions of dollars of Govt spending has got stuck in the savings accounts and paid down mortgages of the wealthy.

The whole purpose of low interest rates is to get people investing in riskier assets.

Not necessarily:

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

{kind=link}

Banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%. Thus around 60% of NZ bank lending is dedicated to residential property mortgages held by one third of already wealthy households.

Exactly. The central bank could constrain investment in unproductive / speculative assets without adjusting the cost of credit for productive enterprise.

What confuses me is that we have had low 'unnaturally low' rates across the world for years doing next to nothing to stimulate economies (and the converse has been true as you note). Surely there has to be a point when economists think, 'Do you know what? I think our models are totally nonsense'.

A lot of folk have been receiving a lot of free money from this policy approach though. That may have something to do with it.

Most are ignorant of physics and advocate for exponential economic growth in a finite biosphere. Clearly berserk.

The manipulation of the money supply via interest rates and QE etc., makes people believe their future is secure through ownership of transferable tokens.

The trouble is a lot of us still play the game but are aware the real world of resources and energy can not fulfil the promises made.

We are at the beginning of a gargantuan sh#t-storm.

"makes people believe their future is secure through ownership of printable for no cost tokens."

The fact that they are transferable is besides the point. It is the fact that these $$ and digits in our bank accounts are supposed to be representative of energy expenditure in the real world. But when a central organisation can just create them for no cost at the push of a button, every $ they create devalues the $ already in existance.

Because of this: countries, companies and individuals who use the $ to try to denominate value are using a measuring stick that is always changing in length. Try building a house with an elastic tape measure.

The Ultimate Guide to Inflation (lynalden.com)

Even just look at the first chart of the M2 money supply.

Bitcoin fixs this. Has a unalterable fixed supply cap of 21m coins and the cost to produce has a real world link through the energy used to mine it. Proof of Work is essential.

Bitcoin is already working as a Gold facsimile, I can't see the change coming until it becomes a more universal tender token. Until I can be paid in BTC, buy my groceries or a car with it, I can't see that changing. What would force this change?

Adoption, user inprovements and network growth.

New Zealand was actually the first country in the world that legalised being able to be paid in Bitcoin if you want to.

You already can do those things, except it happens on the back end of your credit card such as Crypto.com, Fold or Strike and the company just receives dollars.

El Selvador has it as a legal tender, so you can choose to pay and get paid in Bitcoin.

It will take time, in terms of adoption we are where the internet was in 1996 at the bottom of the S curve. I am happy to wait a few decades becuase the early adoptors who put in the research and have conviction will be rewarded.

I mean just look at how broken the fiat system is and ask yourself how long can they keep kciking the can down the road? Because the have overarching controll of the system, the answer is very liekly decades or until people become more knowledgable about how Bitcoin works.

I think the great first step in the right direction has been the increase in everday use of the word Fiat, so that people know that their dollars are not backed by anything at all.

Bitcoin will come under huge pressure as countries around the world start own digital currency. Like when US made it illegal to buy gold. New Crypto currency’s are created every day and some just disappear as for promoting El Salvador you would be lucky to cross the road their without getting kidnapped or shot. Bitcoin is used by criminals and this the way it will be outlawed the drop to zero will be quick.

Hmm I give you a FUD score of 2017 on that one :)

Better luck next time!

P.S I hope you are shorting Bitcoin to zero, Peter Schiff needs some friends.

The lightening network is already doing that - Strike, the world’s leading digital payments platform built on Bitcoin’s Lightning Network, today announced its integration with Shopify, unlocking the ability for eligible U.S. Shopify merchants to receive bitcoin payments from customers globally as U.S. dollars.

The lightening network is already doing that - Strike, the world’s leading digital payments platform built on Bitcoin’s Lightning Network, today announced its integration with Shopify, unlocking the ability for eligible U.S. Shopify merchants to receive bitcoin payments from customers globally as U.S. dollars.

Actually this was announced some time ago.

While I'm a big fan of Jack and Strike, to be honest, on the technology front, this is not "groundbreaking", only for those who're interested in BTC and LN. In terms of functionality, Ripple was capable of doing this years back.

Excuse me, but it was only about 6 weeks ago this was announced? Ripple seem to be stuck with their court case with the SEC, which they seem to be winning?

It was announced at the Miami conference (ability to use Strike with Spotifiy). Ripple is not XRP. That understanding is crucial to the SEC case. Regardless, Ripple is going about its business as a cross-border exchange 'technology' and solution. The SEC case does not prevent them from doing that.

I think Snider has taken Friedmans assertion completely out of context. Friedman said :

"Initially, higher monetary growth would reduce short-term interest rates even further. As the economy revives, however, interest rates would start to rise. That is the standard pattern and explains why it is so misleading to judge monetary policy by interest rates. Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy. "

https://www.hoover.org/research/reviving-japan

My view is that he is implying that the best way to judge the efficacy of Monetary policy ,is to look more at "Quantity of money" ( money supply growth ) .... rather than interest rates per se.

Snider conflates a friedman quote, taken out of context, with a Wicksell idea of a "natural" interest rate.... to validate and legitimize his own unusual ideas...

thats my view..

So we are happy to have emergency low rates and gorge ourselves stupid on massive debt but the minute things turn slightly it’s “Pump the brake this might hurt”. I’m not looking through rose tinted glasses and yes, damn straight we are in for some pain but you know what, as a generation we seem to feel we have some right to copious amounts of credit allowing us to live well beyond our means risk free (by “we” I mean some). Zero f’s given for any future generations and what their lives and opportunities may look like. We created this pile of shite so we should deal with it, not our kids.

People with money and security have just banked billions - they will be basically unaffected by the coming downturn and their kids will be born into wealth and prosperity. Meanwhile households who pay rent and live with precarious income are about to get an almighty kicking as unemployment returns with a vengeance. It is their kids that will grow up with the stress of poverty. My point is that the people who are 'in for some pain' have done nothing to contribute to the housing bubble, nor have they gained from any 'gorging' on low rates.

Exactly:

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR17...

Audaxes. I enjoyed the above, it made me think.. So am I to understand 'standing still' is the most we could have hoped for. That the best outcome possible was an illusion where asset growth is matched by liability growth taking into account future consumption? What about those whose assets increased but they did not lift their lifestyle/consumption to match their new circumstances? Ie asset rich, cash poor farmers?

There's plenty of home owners who haven't sold, refinance or 'banked' anything in the current cycle who are facing a smashing as well. It's not limited to renters. We need to get our heads around how small the group of winners is when basics like housing become massively unaffordable.

Fair point.

The problem being everyone /most aspire to be a winner and the losers are "others" so ignored. Also ignored is the your fact that there are few.

Easy to feel like you're winning with a new ute, trip to Queenstown each winter and a new outboard for the boat.

A lot harder to feel that way when the bank takes a 50% bigger chunk out of your bank account each month just to keep the same house you already live in.

To quote the great Charlie Sheen... "WINNING!!"

Agree with what you are saying there JFoe and yes you are right, the wealthy and their kids with locked in gains will be just dandy. There has always been wealthy and poor, the haves and have nots but my point is this period of cheap money and living beyond our means has created a sector of society that have as I say “gorged” themselves on debt in order to fit into the “wealthy” bracket but are in fact cash poor. I think this group is larger than what many realise. At the end of the day we can’t ‘all’ be rich and lives of excess. Hard earned wealth is all good but living the high life off massive cheap debt needs to stop.

There is a lot of ambiguity on this topic. I agree that the price of housing, but especially rents is far, far too high, but assuming a person who owns a house is 'wealthy' is wrong. I own my own home, it is mortgage free. I have been in it for around 20 years. Some would say I've been raking it in ove rthe last few years because of that, but i never received a cent of income from owning it (it has cost me though). It may have been worth just shy of a $Mil last year, but now it is worth a bit less. Next year it will be worth a lot less. But none of that is income or lost income. It is just paper value that essentially means nothing until I take action to turn it into some tangible, tradeable currency.

It is income murray. You have an investment of about a $Mill and instead of paying you interest, you are taking the income as accommodation.

It is no different than having a $Mill in the bank and using the interest to pay your rent.

This is one reason why we have inequality in housing. The renter is taxed on the accommodation, the home owner is not.

That is just utter BS of the most rank kind. You've obviously bought into Gareth Morgan's 'implied income' theory. There are costs to owning a home. To argue that I received an income, or the equivalent of one is stretching too far. From that perspective you can argue that anyone owning a car gains an income because they don't have to pay a taxi. Should I be living on the street? Should all property ownership become the province of the state only? Should ordinary people never be allowed to profit from their labours and own anything that can be hired of another? The bounds of your position are just ridiculous!

It also shows a marked lack of true understanding of how the current housing mess was arrived at.

This is one source of the housing mess - a major one- the tax advantage.

Income comes in many forms. Capital growth shares for example, provide income from capital gains, not dividends. Tax free.

You home is no different. The income is the accommodation this investment returns to you and is not taxed.

To nullify your advantage over renters, they could be allowed a term deposit up to a million with interest not taxed. And use the tax free interest to pay rent

You think that might be fair?

Or do you wish to deny you have a tax free advantage over the less fortunate?

income

/ˈɪnkʌm/

noun

-

money received, especially on a regular basis, for work or through investments.

You have a weird (and wrong) definition of income.

Owning a house (mortgage free) is not an income, its a reduction in expenses compared to paying rent, but its not an income. Neither is the value of the shares in my kiwisaver, or my brokerage account.

You are in one aspect correct, but the tax advantage came after Government failures to regulate where they were required to.

But I gained no tax advantage from living in my own home. I paid full tax on all that I earned, I have not gained anything from a theoretical change in the value of my home (but my rates went up!), nor will I receive a tax rebate because it fell in value.

"Capital growth shares for example, provide income from capital gains, not dividends. Tax free." Capital gain is not income unless someone does something to realise that value into something tangible, such as sell the item, or using it as security for a loan or some other trade, and then it effectively had an agreed value between two parties. That is why I cannot get taxed for a change in the value of my shares, until I sell them - hopefully at a profit. I will get taxed on any dividends I receive because that is actual money. Otherwise the value is purely theoretical and meaningless, just like the earth being flat. Call what you're arguing for what it is - jealousy tax!

Unless you're investing in only Aus/NZ shares (why?) the IRD might take issue with some of that...

It's a hard concept to sell Rastus - but keep at it. New ideas take a while to take root. Galileo ended up spending his life under house arrest, I hope you don't suffer the same fate :-)

Why not just sell houses at a affordable rate say 4 x average wage earners income 450k for average house in Auckland because this is where market will end up it has to be affordable for people to buy

Try and build a new house these days for 450k. If you got a sweet deal on the land at $150k, you might be able to build a 60 sqm house given current build costs.

Exactly. Getting build costs down is such an important part of any affordable housing strategy. Govt should be investing heavily in this area through Kainga Ora. The private sector won't do it because they are making good money doing what they do now.

Coincidentally, also a big part of how home ownership was made affordable for today's older generations.

There are some 69,000 state houses are managed by Kāinga Ora, most of which are owned by the Crown. The Dept. of Stats private dwellings estimate in Mar 21 is 1,954,000.

Therefore your opinion in regards to having a government built house as the reason home ownership was affordable for today's older generations cannot be correct.

Perhaps you could do a 5 minute Google search before commenting?

Maybe google the number of households in NZ in the 1940s, the number of state houses built at the time, and the impact of state standardisation and subsidy on build costs and efficiency? For example...

"Suburban expansion in the 1920s was a boon for house builders but few firms survived the onset of the 1930s economic depression. The creation of the government’s state-housing scheme in 1937 re-energised the sector and for the first time saw streets of houses being built at once. Under the 1950s Group Housing Scheme the government encouraged builders to construct new homes by pledging to buy those left unsold. This facilitated the creation of large private building companies that helped to build whole suburbs. Many provided ‘design and build’ services: clients chose a house from a pattern book and had it constructed on a section in a new or existing settlement."

The majority of our housing was built in the 70's not the 40's. I agree that having the government actively involved is beneficial, as would be a review of the whole building industry.

Bizarre argument. You look at the current number of state houses today to argue that the government and PPP build efforts of the post-war decades never occurred or were ineffectual in aiding our high home ownership rate achieved by the 1980s? The implicit assumption that current number of state houses is the total that has ever been built is clearly wrong.

Perhaps you could do a 5 minute Google search before commenting? Better yet, read a book covering many of the post-war efforts or even talk to people in their 70s and 80s who remember them well.

Building sector is making a lot of money but spending a lot of money too.

Also tried building houses for HNZ years ago, contract pricing can come down to $1500/m2 incl GST if the volume is there (500+ units). However between HNZ, TA's and engineers/geotec with their snouts in the trough managed to release & build on less than 50 sections and gave up.

Consultant and TA costs ended up being equal to build costs!

If Fletchers or someone else teamed up with a motivated TA or Gov. department you could volume build (5000+) quality houses for $1500/m2 today.

Possible, but wont happen. You would need to cut through swathes of red tape, baked in old mate compliance costs, elf n safety and other associated consultant & planning BS.

Yes that’s the problem land and building cost but if people just can’t afford to buy something will have to give or peoples wages will need to double. But from what I can tell a lot of new builds will be in trouble, now rates are raising from emergency levels prices will fall quickly, people who made huge amount as markets climbed will now lose a huge amount as they fall, lots of speculators would have sold at high last year and wont be back till market hits bottom which will be a long wait and hopefully government will put laws in place to stop house prices raising above inflation

Nationalise land. It is senseless using supply & demand for something with fixed supply. Now your 60sm house sells for $300,000 and instantly 3 of my 4 adult children would be buying instead of renting.

Land is over valued big time people are being ripped off.people said this at every downturn but house prices crashed and it will be the same here.

Current cost to build is approaching $4k/m2, its not possible.

Because to do that somebody would have to take a loss, but we live in a society where everyone thinks they can and should win.

Too much ticket clipping, not enough innovation or actual value add.

The 70's was a boom time of immigrants helping each other build houses, since then building standards and our building supply markets have changed significantly.

Perhaps with some investigation we could return to that model?

https://ww3.rics.org/uk/en/modus/built-environment/homes-and-communitie…

The Kiwi dollar will open today softer again at 65.8 USc and another -¼c fall.

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now

The “dollar” shortage only got worse

Big sell off happening,NZD tanking this will make inflation higher RBNZ leave rates at emergency levels this cost us all as NZD tumbles

Looks to have bottomed out for now. Let's see what sort of pullback we get when Asia comes on line, I'm guessing there's still a bit of bloodshed to come today.

After the dismal start to the cropping season late last year it was pretty depressing watching our squash crop get poisoned, smashed up and tilled back into the ground over the past week. The leasee couldn't secure shipping space, and while they'd given away some of the crops on other properties as a charitable act there was just no way to move ours. The lack of RSE pickers also meant the crop had sat in the paddocks for longer than ideal and the plants had mostly died by the time the tractors came through.

End result: 100% crop loss, and no lease next year.

I'm not reliant on the income for survival but it will slow down land improvement and so affect future crop yields. Looks like the food crisis isn't just about climate change.

Why not sell cheap to NZ market.people need food rather than throwing it away give it away.

Some was given away from other plots, but ours was simply too small and too remote for the cropper to get to in time before the crop started going off.

That sux. From experience even when it costs you nothing, milk covered by insurance for instance, it's really depressing to simply dump so much food and there's absolutely nothing you can do.

One of the facts of our often sad world is that there's always been enough food in the world it's always been about distribution and politics. I doubt climate change will affect that either way.

redcows - that is a historical comment. Have a good look at the graph:

https://www.thegreatsimplification.com/episode/12-dennis-meadows

Bad news, but the highlight will be an improvement in the soil for next year plus RSC workers back in (love to know what hourly rate these Pacific Islanders are on).

A few years ago some friends of mine picked grapes in the summer holidays between semesters at uni. They were not paid an hourly wage, they were paid by weight of the fruit they picked. It was a physically gruelling job all day in the heat of summer, but their earnings were equivalent to less than the minimum wage at the time. They weren't too sore about it because it paid for their beer and accommodation in a beautiful bit of the country, but it's an industry that relies on exploiting students, backpackers and "seasonal workers" from deprived parts of the world. You see these buggers on the news now and again crying out that they can't get enough workers and the local kiwis are too lazy for some hard graft; not so. If they paid a fair wage they would be swimming in workers.

Where will these workers come from? We are at full employment, the permanently lazy will not budge from the government teat, the disabled remain so, but I am sure you thought of that so where will they come from?

Also perhaps you might consider the impact of paying more for picking fruit on your ability to buy it at an affordable price, we are determined not to fix our oligopolies so you can be assured that if farmers pay more you will.

Where will the workers come from? If the pay isn't slave wages, you attract workers who are in other employment that has less favourable conditions or wages, i.e. you compete in the labour market rather than using imported slave labour as an emergency valve in your badly managed business. I'm happy to pay more for food if it means kiwis are actually getting a fair income and conditions are improving, it sure beats paying more for food and getting the current status quo.

Real estate agents.

I have an older relative who picked fruit in the late 60s. According to the RBNZ inflation calculator, they were paid the equivalent of $28 per hour today, and received free dormitory accommodation because it was understood it simply wasn't feasible to expect workers to rent accommodation for seasonal work.

Yes, if we pay people reasonable wages not everything is dirt cheap. The expectation that everything should be dirt cheap while we receive lots of money isn't necessarily viable.

(Albeit we need to fix oligopolies, thus we need to find politicians equipped with spines.)

How much are the Pacific Islanders paid? The is a lot of smoke and mirrors in that. While you might be shown a wage figure it can be there is an accommodation cost, compulsory and outrageous.

Even kickback payments accommodation provider to employer.

But but. There is no universal thing here. It varies. Sometimes it's the employer getting the bad deal from 'agents'

Russia has cut off Poland from gas supply.

At least it's warm in Europe for the next few months. Allow Europeans to go and buy/install a diesel heater to keep their houses warm and water hot.

Or a heat pump and some solar panels?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.