Here's our summary of key economic events overnight that affect New Zealand, with news global markets are shuddering today as the Fed's rate hike has been followed by other central banks, and investors worry that the very sharp rises in interest rates will bring recession. Most benchmarks are falling.

But first, initial American jobless claims rose last week from the prior week but the rise was minor - and it was less than expected. There are now 1.27 mln people on these benefits, also a weekly rise, but in turn also near their all-time lows.

However both housing starts and new residential building consents fell sharply in May, even as completions jumped to an all-time high. Now both consents and starts are below year-ago levels.

US mortgage rates are rising fast again, and their benchmark 30yr rate is threatening 6% all of a sudden. These rates are now at their highest since just before the GFC in 2008.

And the Philly Fed factory survey has turned negative in June. The indicators for current activity and new orders dived, and the shipments index also fell but remained positive. However, firms reported continued increases in employment. Both price indexes declined but remained elevated. Expectations for growth over the next six months deteriorated, as the future general activity, new orders, and shipment indexes fell sharply.

Meanwhile a heatwave is baking the middle part of the US and thousands of beef cattle have died in parts of Illinois, Indiana, Missouri and Kentucky.

In Canada, wholesale sales fell in April when a rise was anticipated, so the change from March has been rather sharp on this front.

In South Korea, manufacturing giant Samsung Electronics has moved to reduce its ballooning inventories, cutting orders from suppliers.

In China, house prices fell the most in almost seven years. Average new home prices in China's 70 major cities fell -0.1% year-on-year in May 2022, reversing from a 0.7 percent gain a month earlier. The latest figure represented the first drop in new home prices since September 2015, as tighter COVID-19 restrictions dented buyer confidence in their property market. Only 25 of those 70 cities recorded any gain from the prior month, only two over +½%. Existing home sales prices fell much faster than new construction.

The demise of freedoms in Hong Kong is seeing an exodus, and a major move of Chinese entrepreneurs, professionals and their families moving to Singapore is underway. It is not minor.

Meanwhile, the Hong Kong Monetary Authority raised its benchmark rate by +75 bps to 2.0%, matching the US Fed as it usually does on a formula basis. (China's one year prime loan rate is 3.7%.)

Taiwan also moved its policy rate higher, up to 1.5% as expected, a small rise from 1.375%.

But in an unexpected move, the Swiss National Bank hiked its policy rate by +50 bps to -0.25% at its June 2022 meeting, surprising markets that expected the interest rate to be held constant. They did not rule out further rate increases in coming meetings. It was their first rate hike since 2007.

In Britain, the Bank of England raised its policy rate by +25 bps to 1.25% at its June 2022 meeting, a fifth consecutive rate hike and pushing borrowing costs to their highest in 13 years as it tries to control soaring inflation. There was dissent. Three policymakers voted for a larger +50 bps rise. That is because English inflation is now over 9% and is expected to rise above 11% in October. Further, they forecast economic activity to slow sharply over the first half of their forecast period.

In Australia, in May their labour market expanded by more than +60,000 jobs, all of them full-time. Their participation rate blipped up with a small but impressive rise to 66.7%, and their jobless rate held at 3.9%. Analysts were impressed. (The NZ, out participation rate is 70.9% and our jobless rate is 3.2%, just saying.)

Aussie inflation expectations jumped markedly in June, now running at 6.7% and up from 5.0% in May. This is a very sharp shift. But this same survey recorded that consumers thought their pay would rise a measly +1.2% in the next 12 months. Despite this, Australians are still planning to spend like it is 2021. They might have to change their tune at some point; some of these survey results will have to change.

The decline in container shipping rates out of China continues, but it remains small. But rates for bulk cargoes have stopped falling.

The UST 10yr yield will start today down -6 bps from this time yesterday at 3.33% in a further settling after the Fed moves. The UST 2-10 rate curve is steeper at +16 bps and their 1-5 curve is steeper at +50 bps. Their 30 day-10yr curve is also steeper at +231 bps. The Australian ten year bond is down -2 bps at 4.13%. The China Govt ten year bond is little-changed at 2.83%. And the New Zealand Govt ten year will start today unchanged at 4.31%.

On Wall Street, the S&P500 is has resumed its selloff, down -3.5% in Thursday afternoon trade and down -6.1% for the week so far. Overnight European markets fell by about -3%, except Paris which was down -2.3%. Yesterday Tokyo ended up +0.4%, Hong Kong fell -2.2%, and Shanghai fell -0.6%. The ASX200 ended its Thursday session down -0.2%, and the NZX50 ended up +0.1%.

The price of gold is up US$16 in New York, now at US$1850/oz.

And oil prices have risen back some today from this time yesterday and are now up +US$2 at just on US$115/bbl in the US, while the international Brent price is now just on US$118/bbl.

The Kiwi dollar will open today very firmer at just on 63.9 USc and more than +1c higher. Against the Australian dollar we are more than +½c higher at 90.5 AUc. Against the euro we are up at 60.4 euro cents. That all means our TWI-5 starts today at just under 71.3, and up +70 bps since this time yesterday.

The bitcoin price has firmed from this time yesterday and is now at US$21,016 but up only +0.9%. Volatility over the past 24 hours has been extreme again at +/- 6.7%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

103 Comments

High chance US GDP is already negative in Q2 just like Q1 had been, following the prior two quarters (2H21) of nearly zero growth (apart from inventory which is right now about to be turned into the historic deflationary bomb). Link

I hope that quote is wrong. But everything is pointing to it being right. GDP growth and GDP flatlining during pandemic has likely been driving most of the asset bubbles/ inflation and has been caused by low rates and money printing.

Turn off the low rates and reverse the money printing and we will find out what the economies really looks like and who is still willing and able to buy at inflated prices (who can still make money at the consumer end).

Not pretty if people are sitting on tons of stock?

That is the real issue - In South Korea, manufacturing giant Samsung Electronics has moved to reduce its ballooning inventories, cutting orders from suppliers.

China doubles down on vision with Russia

To borrow the undiplomatic words of European Commission President Ursula von der Leyen, Xi may have inflicted “a major reputational damage for China” in the West. Quite obviously, Xi has ignored the repeated warnings by US officials that the “sanctions from hell” to weaken Russia would visit China too if Beijing gave support to Moscow. Curiously, Xi rebooted the China-Russia partnership although Biden Administration officials are spreading a notion lately that a “thaw” is on the cards in US-China relations.

Xi sending his country back to the ice age…

China wants to avoid doing anything that would interrupt the process of U.S. decline. Link

Decession maker in central bank goofed up, specially fed but USA being much bigger and diversify economy may still survive unlike NZ, where only economy has been housing - Thanks to all the support and promotion by RBNZ with government backing.

The US has been dependent on QE and ever lower rates for a while now, it seems.

Im just a small fry but our stock levels are double what they were this time last year, and Im sure Im not alone. Our suppliers were actively pressuring us to buy more earlier at the start of this year, but we resisted that, not all would have. There will be a ton of money tied up in warehouses around the country.

Anecdote, mate has a high spec MTB on order from Europe. Called them to cancel the order. Was called back next day, we'll give you another 1k EUR off if you keep your order.

Sounds anti-inflationary.

I imagine this will start happening with building supplies. And probably even quotes from builders.

Anything that went up dramatically can also come back dramatically. House prices are on their way, some commodities have already unwound, some of the big Covid winners have share prices lower than pre-Covid (Peleton are lower, Zoom only a little higher and ~80% down from peak etc).

I have a couple of moderately expensive projects around the house but will be waiting a while as I expect them to get cheaper and easier to schedule.

Exactly,there is a lot of dynamic pricing out there,algo's constantly tweaking.Businesses charge what they they think you will pay in many cases,many have had their snouts deep in the trough,the tide may be turning.

Not too late to pivot into a new career,apparently Christopher Luxon used to run an airline,he flipped a coin,real estate or polly next...

We are still seeing price rises of between 6 and 20% for the upcoming season from our suppliers, and as yet freight has not cheapened in any meaningfull way.

Margins will be squeezed with rising costs, and fewer discretionary dollars/less demand.

And when supply exceeds demand prices go ???? - the clue is in the ?

Brace for another pummeling on the NZX50 today I suppose. Look in horror at how fast the KiwiSaver balance goes down too.

It was all so predictable though. That’s why I sold my shares in October last year. It’s why I told my son to not buy shares and go in to a cash KiwiSaver fund for now - good that he listened.

I also switched my KS to cash in October last year.

I am far from a financial whiz kid. This was just so obvious.

Sometimes corrections are well signalled, sometimes they are not. Either way the most important thing is to get back on the horse and ride.

Same, even the "stupid " gardener,'meself', switching KS to cash, although bonds also getting collateral damage, only down 2%, in my balance, won't be going back into shares for 18-24 months,maybe longer. A lot of leading indicators to watch ,before a move back.

Exactly, well done.

What should I do now though? KiwiSaver only represents a small percentage of my investments and I don't have much in shares so I thought I'd just leave it there in an aggressive fund.

Do nothing, selling now will only crystalise your losses. Don't look at your balance and just keep doing what you have been doing.

So when do you plan on getting back into the stock market? Your chances of picking the bottom are slim to none. Dollar cost averaging and ignoring the noise has been shown to be more successful in the long term than jumping in and out of the market.

See below my comment at 9.22am. Picking the bottom of the market is obviously close to impossible. If you are within 10% you are doing well. I won’t be trying to pick the bottom, but I will be looking for signs that the bottom may be close.

At this stage, I expect the bottom to be around June - July next year. But that’s just a very early stab in the dark, obviously I will monitor consistently.

If there is a big slump again this year it might be worth buying some shares at that point.

The bottom is a valley, the top is a peak. You want to buy at the knees and sell at the shoulders. When the 50day moving average cross the 200day moving averaga is normally a good sign. Its not an impossible still to learn

That’s a great way of putting it.

It's ok. All the experts reckon you are best not to change to cash fund cause it will all be alright in the end.

Changing fund type works if you can call the big moves, I have been cash for a while and convinced partner to change about 3 months ago. I was in a fund where company matches my contributions, so it's an automatic double, why be greedy after that.

The tricky bit is deciding when to switch back to growth. Easy to sit and stagnate in cash when the world is getting on with the recovery, worrying it's a dead cat bounce.

I disagree. If you educate yourself I think it’s quite easy to read the markets and what the forward trajectory for economies is, with the one caveat of course, that black swan events can occur…

I think you are overestimating your abilities. The markets are chaotic, and a few lucky calls does not mean you are on top of it. If you follow even celebrated and hugely successful market participants, they are frequently wrong and often for long periods of time.

If it was easy, everyone would do it and we'd all be rich. But of course that would change the system and the easy thing would no longer work...

I strongly recommend humility as a protective measure.

I am not saying you can pick every dynamic, not at all. Nor those black swans or even somewhat unexpected things.

But I think if you know your stuff you can get quite good at picking the big macro movements. I have been pretty accurate the last 2-3 years. And that’s definitely not luck.

I have been far more accurate in my forecasts than economists over the past few years.

Humility? Yes. But my moves have been more on the bearish side so less room for bad outcomes, although potentially also less room for making gains on the upside. But I am not a gambler.

So instead of picking up more assets on the cheap, you've decided to lose more purchasing power?

Please explain further.

assets? Are you talking about houses? If so, they have much further to fall, and I am not interested in housing as an investment anyway.

C'mon man, we're talking about KiwiSaver obviously. The point of KiwiSaver is to pick a timeline and choose the appropriate fund and continually add to it. Not go in and out of funds based of where you think the market is going. Hopefully you don't re-enter the market too late...

No that wasn’t obvious from what you said.

What you say is the conventional view and there is obviously a lot of merit in that view.

Anyway, I am hitting the road for a break now. My view is obviously a minority one, it’s great to have a range of views, and people need to make their own decisions.

I am comfortable where I have landed.

I agree with you, but then I have sat on trading floors most of my life, these major corrections are no mystery events..... you just have to learn about fear and greed. No one is saying you should switch funds often, but if you see the signs you can massively protect capital.

Of course you should talk to your qualified financial adviser (prob a failed real estate agent, insurance sales person or spot trader...),

The replies above my first response (including yours) are talking about KiwiSaver...

The funds are still picking up assets at lower prices whether you are in them or not.

I'm not sure of the unit price ramifications of switching in and out of funds but one assumes they go up and down with the assets.?

If it's working for you, all good. So long as you don't fall into the trap of feeling infallible and sticking 50% of your net worth on some penny dreadful or alt coin.

There is plenty of research out there that the vast majority of people taking active decisions with their portfolio underperform those who just choose a fund, set up a regular payment and then get on with their lives. One brokerage firm found that their best performing cohort was deceased customers.

I am sure that some outperform, and for a small minority of them that may be skill rather than luck. But, I am a gambler and I don't fancy my odds in this area, playing in a field with all the hedge funds and investment companies in the world. My rule is to only gamble when I have some kind of edge and the odds are in my favour.

It's not really gambling if the odds are in your favour. Much like the house in a casino isn't gambling and card counters are thrown out.

I still consider it gambling - having a 51-52% edge still means you often lose money. The casino will smooth things out by having hundreds of customers making small bets but my personal statistics will be much noisier.

Agreed that markets are chaotic and unpredictable. I think there is a sort of natural selection. Those investors that do well will survive to chortle and those that don't are not heard from.

Housemouse is right.

Its important to learn to move your money around - its the easiest way to make or protect your money. I am not sure it takes a great deal of education at the moment to realise that stocks are at a very risky juncture,

In general terms I agree HM is correct. But the share market is more driven by emotion than reason and that is hard to predict.

Fair enough. But I still maintain you can be quite successful in picking macro movements, if not all the micro stuff, and certainly black swans are unpredictable.

To me, it was pretty obvious by October last year that a big economic slump was on its way, induced by a number of factors including debt levels and rising interest rates.

if you look at history, these sorts of factors typically precede share market slumps.

I also listened carefully to commentators that I respect such as Jeremy Grantham.

There was no luck behind all of that and my resulting financial decisions.

The challenge for me is when to dip back into shares and a more aggressive KiwiSaver scheme.

But that’s a call for 2023.

The trouble is, they were at a very risky juncture in mid March 2020 too. The S&P then proceeded to double over the next 18 months or so.

If you were able to sell right at the pre-covid peak in February, you needed to get back in before August in order to actually benefit from that first decision.

I've been wondering: does an individual moving between Kiwisaver funds mean they crystallise their losses (i.e. moving from Growth to Conservative will definitely be the case), or, if they stay put, does it actually then depend on the KS fund investor themselves and whether they exit certain stocks and crystallise the loss for everyone? Surely if investment fund holds firm, then they still have the potential to realise gains (if any) if that particular stock rises again or conversely hang around and take a hammering if the stock continues to decline?

If anyone knows, would love to hear your thoughts. Also, wouldn't the above (if true) tend to lean in favour of the general DCA advice to keep investing in the same fund / KS fund (assuming you've got time on your side to ride out the peaks and troughs)?

If you haven’t read Simple Path To Wealth I would strongly recommend it. It’s a invaluable resource

Thanks Albert2020! Will do.

It depends. For House Mouse, he didn't crystallise any losses because he exited at the peak. He crystallised his gains.

I'm with a passively managed fund, so I'd expect less of the crystallisation of losses for everyone.

HM,

I disagree. If you educate yourself I think it’s quite easy to read the market. Really? If so, fund managers would show good results pretty much all the time. You are indeed overestimating your abilities-big time. If you did indeed have that ability, you would be even wealthier than Warren Buffett.

I have been in this game-professionally and personally for almost 50 years and I think I've done ok- fully retired at 57, but I am well aware of my limitations. I would never contemplate selling all my shares. I did start to take some money off the table several years ago(too early) as I knew that somewhere down the line there would be a substantial correction, though I had no idea what would trigger it. Accordingly, I have kept building my cash reserves and can now consider a gradual reinvestment in companies with decent balance sheets-good cash flow being at the top of the list. I want dividends to be both sustainable and growing. Right now while capital values have fallen appreciably, none of my holdings have cut their dividends.

Yes good point - it was the 2/10 inversion in 2019 that was the trigger for me to step back from risky assets.....it meant I missed some of the 2020-2021 speculative boom....but then again...I think it was a speculative boom so not my style of investing regardless so didn't buy into the hype. Some of my friends did, and thought they instantly became smarter than Warren Buffett for the last 2 years, but they now realising the hard way that they don't know that much at all.

If there is real value in the market then I might start investing again, but as HM points out, that time doesn't appear to be now or likely this year.

Was being sarcastic. Changed mine months back. Did make the mistake of switching some other cash from growth to conservative not cash. That conservative fund is now worse return than TD over three years.

Warren Buffet quote - be fearful when others are greedy and be greedy when others are fearful.Right now I reckon the Beehive 9th floor & Mr Oorful is terrified.

I doubt it - the revolving door never stops

That’s true for most punters who aren’t interested in, or knowledgeable, on finance and markets. But I would say people should be more interested and knowledgeable.

You can change funds at the flick of a switch.

once I am confident the economic carnage has settled down, or the worst of it is over - probably about this time next year - I will switch back to a more aggressive fund.

Redcows is correct Housemouse - some conservative funds are fearing worse than Balanced or growth due to bond carnarge. So even if you "educated" yourself how was this to be forseen?

Luck plays a big part or better yet inside knowledge

You are right. But I am not in a conservative fund, I am in a cash fund. Big difference.

Which also is being debased heavily ..carnarge everywhere

That’s a bit of an exaggeration. Sure in real terms it’s going backwards a bit, but that’s still a much better position than sustaining big losses.

Out of curiosity is the cash fund a basket of currencies or is it held in NZD? You could also incur significant losses in currency devaluation

I watched TV1 news last night (a rare thing) to see what they had to say about the state of affairs relating to GDP figures. I was put at ease with two main points, it was "due to Omicron" and "just a blip".

Thank god for that, back to the good times next quarter.

Will they put a mandate on 'blips' next?

Thank God we have TV1 news and Liam at the Herald to calm the masses. Dishing out that opium for the people!

If you have data access to a diverse client base in an larger accounting or law firm you can determine changes in the general economy far quicker than stats, the economists and media will ever report.

Apart from that inside knowledge, general trends in share markets you can see yet never pick timing...charting and fundamentals can provide some assistance but still limited.

Love to know how those above above that pulled their money out quick on the advent of covid-19 actually managed to pick getting back in time for the next upswing....

Anyone with access to some "big data" and the nous can get some great insights. You just have to be able to look at things through a wider lens.

that was GR response this morning, now saying that we need to look at this annually not quarterly, trying to compare the period when NZ was in lockdown. Anything to move the goal post, to deflect attention from the government.

https://www.newstalkzb.co.nz/on-demand/week-on-demand/

Listen to Andrew Kelleher @ 06:15 today and he tends to agree that GDP is so volatile that it is difficult to compare qtr to qtr and even harder to compare with other economies at different stages of the cycle.

With Oz,you have to take into account they were heading into an election,so all may not have been as it seems,not that I am implying that scomo splashed the cash.

I agree when he says it doesn't really matter whether it is -.02,+0.15 etc,it becomes a technicality that we will all get hung up on.

Either way it is aneamic growth,but it is more pyschological than anything and we will all go into a frenzy,but if by some measure we don't record negative growth next quarter,the fundamentals won't have changed much.

Worst PM and Government in living memory.

:-) ;-) ...I'll give you points for consistency Rex...I hope the dementia isn't affecting that memory too much.

As I value your opinion,how do you rate Luxon as a Nat leader,best,worst,middling?

It would not appear to concern you that some folk have family circumstances with dementia which to them is something of a tragedy. To weaponise that condition as a means for your brand of low insult is abhorrent and it is offensive.

I apologise if my humour offends anyone,my dear old mum has dementia...and a sense of humour,it's her British side.

But I hear ya,apologies.

Smudge - did TVNZ also confirm that this year Christmas day will fall on Good Friday?

Hong Kong sliding further away from its former high powered financial/ corporate international hub status. Tokyo, Taiwan, Seoul, Singapore will pick up the slack no doubt. Hong Kong will remain though a vital port for China, even in the old sense of where the West meets the East. Perhaps this is what the CCP had always been planning?

Hong Kong was only important while the court systems followed English law. Not so much anymore.

by Audaxes | 19th Apr 20, 11:40am

Singapore or Hong Kong’s economic model is largely about arbitraging the inefficiencies, or loopholes, in their larger neighbours. To some extent, money laundering is the core business. It doesn’t take a genius to come up with this economic model. How hard could it be? You just need a powerful friend for protection. Singapore has the United States. China just lets Hong Kong get away with it. It believes that what’s in Hong Kong stays in China anyway. And some powerful vested interests need Hong Kong to get their ill-gotten wealth out. Link

Its not hard to get money out of China, you just need to own an importing business.....

I don't think so. The autocrats of the world think they're better than everyone else, and I think the Chinese are no different. I don't think they can see past their egos far enough to realise that Hong Kong's success lay in the basic freedoms, rooted in democratic principles, that gave the people scope to be their best. And yes sometimes that means being able to criticise the political system. But debate and criticism strengthens those systems. It doesn't weaken them. Only the weak are threatened by it. I think the CCP honestly believed that gaining control over Hong Kong, making it conform to their ways and politics meant they could gain its strength, wealth and prestige. Bluntly I suggest that China had more to gain by leaving it under British rule, but now they stand to lose it all but the territory itself.

"When he became Financial Secretary, the average Hong Kong resident earned about a quarter of someone living in Britain. By the early 90s, average incomes were higher than Britain's. Cowperthwaite made Hong Kong the most economically free economy in the world and pursued free trade, refusing to make its citizens buy expensive locally-produced goods if they could import cheaper products from elsewhere. Income tax was never more than a flat rate of fifteen percent. The colony's lack of natural resources, apart from a harbour, and the fact that it was a food importer, made its success all the more interesting.

Asked what is the key thing poor countries should do, Cowperthwaite once remarked: "They should abolish the Office of National Statistics." In Hong Kong, he refused to collect all but the most superficial statistics, believing that statistics were dangerous: they would led the state to to fiddle about remedying perceived ills, simultaneously hindering the ability of the market economy to work. This caused consternation in Whitehall: a delegation of civil servants were sent to Hong Kong to find out why employment statistics were not being collected; Cowperthwaite literally sent them home on the next plane back.

Cowperthwaite's hands off approach, and rejection of the in vogue economic theory, meant he was in daily battle against Whitehall and Westminster. The British government insisted on higher income tax in Singapore; when they told Hong Kong to do the same, Cowperthwaite refused. He was an opponent of giving special benefits to business: when a group of businessmen asked him to provide funds for tunnel across Hong Kong harbour, he argued that if it made economic sense, the private sector would come in and pay for it. It was built privately. His economic instincts were revealed in his first speech as Financial Secretary: "In the long run, the aggregate of decisions of individual businessmen, exercising individual judgment in a free economy, even if often mistaken, is less likely to do harm than the centralised decisions of a government, and certainly the harm is likely to be counteracted faster."

Interesting post, thanks.

enjoyed that too. thanks. elements of Northcote Parkinson’s theories curled up in that, on a grand scale.

Smart man. Some other comment streams I read here often give rise to the thought that if governments worried less about business and the macro economy, and just ensured the ordinary people on the street, starting from the bottom, had good opportunities and incomes, and therefore money to spend, then the rest would take care of itself. Still think that - people spending money is what makes the economy go round. But governments put more effort into pumping business and the rich while all else collapses. I think when people have good levels of disposable income and there are plenty of choices, then we can get closer to the ideal of a free market, but big business doesn't like that. They have to work too hard.

Maybe the Aussies are being smart? Buy now (using cash), before your cash loses its value.

Of course. Another obvious strategy. On a personal level we did a lot of that second half of last year.

All Data and News pointing towards man made finacial disaster created by generousity of central bank with support from over generous government, still many are still not ready to accept that worse is yet to come.

Even today house prices not reflecting true value ( should be much lower) and vendors still holding to high price though in their mind have dropped from their imaginated expected high price.

May be new appraisal and listing coming be better price as they say - meeting the market expecatation and also only those vendors, who have to sell will list, knowing and admitting the fall. Domino effect has started and will roll into fast decline of house price from here on.

Its a mess, ocr rates and money printing are being unwound too late and too fast - globally. Reserve banks should be the conservative, slow moving, predictable protectors of a stable economy.

They are playing with fire now - with deflation/stagflation and black swan events becoming a very real risk as people, businesses, countries and industries (not just housing) have not had time to plan to unwind their own positions (inventory, asset ownership, debt etc). They will all be reacting too fast (focus will be survival first) so mistakes will happen and compound the mess as for example people stop spending overnight (as the bad financial news accelerates and media jump on) , asset fire sales accelerate (to prevent bankrupcies), businesses revenue and profit forecasts collapse, inventories unwind to match revised forecasts (deflation - happening now in some industries), supply chain orders are cancelled, or pulled back (already happening), employees are laid off (unempolyment rise - natural reaction to less revenues and profit) and we risk a rapid downward spiral all too fast

Unfortunately its looking too late to stop much of it.

ECB wants to intervene in bond markets (buy Italy debt and sell German bunds) to stop fragmentation, BBG reports. But this also eliminates market forces, which are an important disciplining tool. And who actually determines which risk premiums are justified for which debt ratios? Link

This is all crazy because it has been previous market intervention that is causing the current chaos!

By intervening now, are they just going to create even more problems down track?!

This whole pain avoidance at all cost mentality we have is insane to me.....we need to eat our frogs then get on with it.

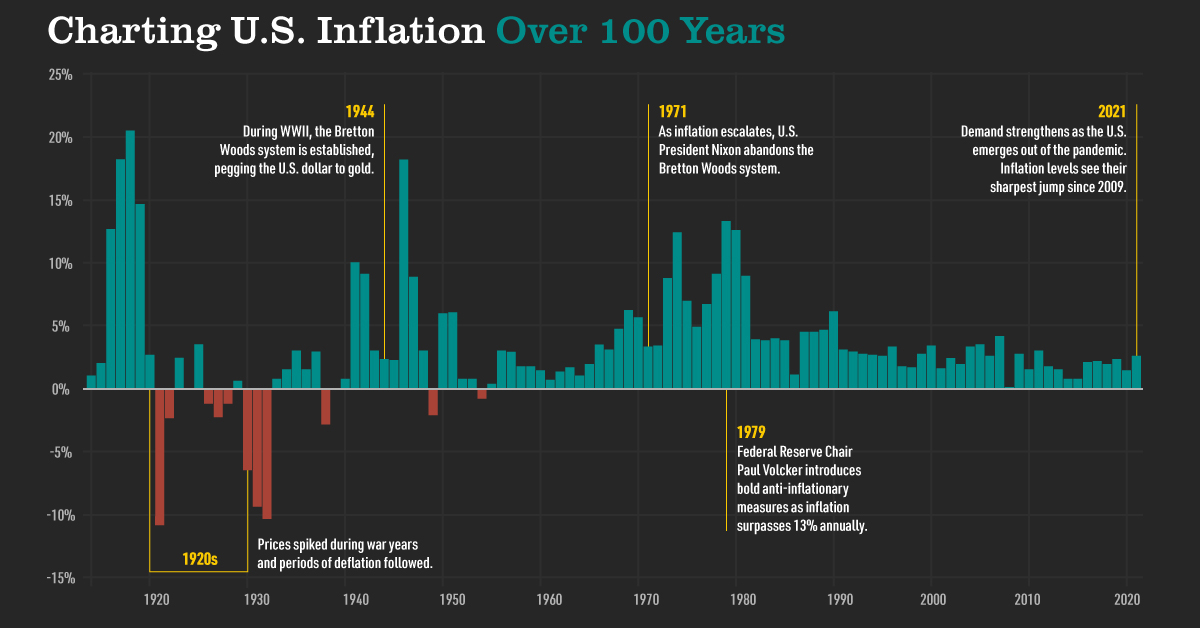

A useful chart of the history of inflation in the US over the past 100 years.

https://advisor.visualcapitalist.com/wp-content/uploads/2021/06/Miam-34…

{kind=link}

With inflation approaching 9%, you can see that the US (and by interdependence, the world) are experiencing a one in 40 year event....or its possible if this is going to be the end of the long debt cycle, and therefore a once in 80-100 year event unfolding.

Noting that many countries have war-time national debt levels (like the WW2 period), its possible this is more like the 1940's than the 1970/1980's.

Lyn Alden, whom I respect as a macro analyst, discusses the parallels between now and the 1940s vs 1970s and she agrees. We're in for one hell of a rodeo.

Yes I follow her on twitter

Thanks for that, I'm enjoying her most recent YouTube clip and will search out some others. She doesn't appear to have any agendas to push, would you agree?

Its way way worse, as back in the 40's or 30's we didn't have derivatives and the huge counter party risk we have now.... This my friend is the Big Kahuna

Had a look at the FB property investor website last night...a few people talking about buying their first rental and asked the FB community if now was a good time to buy.

The general trends of comments where:

"Its always a good time to buy property'

"We bought our first IP 5 years ago and will buy another soon, so yes absolutely"

"Yesterday was the best time to buy a rental"

There were perhaps 1 in 20 comments actually warning about what is unfolding in the property market at present with rising rates and falling prices.....the rest were still in denial that anything had changed. It honestly looks like many people in society have completely lost their minds...far worse than what I saw in the US before their property bubble burst...

Pretty scary, ey. It’s like a cult.

I left that page when they started debating who should pay for replacing a blown light bulb - landlord or tenants

Funny how they will often blindly pay hundreds of thousands of dollars more for a property than it is actually worth... to the point where yields are lower than a bank deposit... and then will try to screw every last little nickel and dime from their tenants.

It hurts to say but in some ways this activity allows for a softer landing... but those entering the market now may get burnt. Maybe not, test interest rates are high enough to give some wriggle room. They will need to be prudent for the next few years to make it work. Though asking in a property investor chat if now is a good time is pretty telling in terms of general awareness.

That's the neat thing about property, you only have to find one bigger idiot bigger than yourself to sell too.

A lot of people are already struggling however there is certainly a lot of money still out there....few listings of quality properties that people want in the SI. One down the road sold for a 400k premium days ago. We could currently sell at 20 percent above November peak...I had unsolicited call to see if wed would sell... There are always people unaffected by the economy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.