Here's our summary of key economic events overnight that affect New Zealand, with news international travel may be back on the agenda for many, but it is likely to cost a lot more post-pandemic.

But first, US jobless claims came in virtually unchanged last week from the week before. That remains a low level. There are now 1.916 mln people on these benefits. Still this leading indicator isn't yet showing labour market stress rising.

But those monitoring major layoffs are finding more now. US-based employers announced 102,943 cuts in January, and far higher than the 19,100 cuts in January 2022. As spectacular as these changes are, you need to keep in mind the US workforce is 156 mln, so this new level is just 0.07% of that.

American labour productivity rose in the December quarter and labour costs rose at a much slower pace than anticipated, only at a +4% annual rate. Financial markets kicked along on this news.

And US factory orders bounced back to growth in December from their big and unexpected November fall, but not by as much as expected.

Going the other way, Canadian building consents fell more than expected in December after an unexpectedly large rise in November.

In what might be seen as an act of desperation as Beijing's grip on Hong Kong tightens and confidence leaks away, the city's governor is giving away 500,000 free airline tickets to try and entice visitors back in 2023.

As expected, the ECB raised it policy rate by +50 bps to 3.0% during its February meeting, its highest level since late 2008 and indicating to will deliver another +50 bps rate hike at its meeting in March.

And in a mirror decision as expected, the Bank of England raised their rate by the same +50 bps, taking their policy rate to 4.0%.

In Australia, their building consent levels rebounded very strongly in December ending a period where they languished. Bouncing back most strongly were approvals for new apartments, surging by more than +50%. However, despite this December jump, Q4-2022 consent levels are still lower than Q4-2021.

The IMF has been reviewing Australia, and its report says specifically: "The capital gains tax exemption for the sale of main residences, costing around 2½ percent of GDP annually in foregone revenues, should be restricted." (See page 14.)

A commodity we don't watch much is the cost of aircraft jet fuel. But it is in shortish supply, made worse by a sudden shift higher for air travel demand, which started in the US and is expected to grow rapidly in Asia now. We are talking +20% to +60% year-on-year rises. Just in the past few weeks the cost of this fuel has risen +11% since the start of 2023. It is hard to see it reverting back any time soon.

One commodity we do watch regularly is container shipping rates and they were unchanged last week. Bulk cargo rates seem to have stopped falling, bottoming out at a low level.

The UST 10yr yield starts today at 3.38%, and down another -8 bps from this time yesterday. That has added up to a -15 bps retreat in a week, most in the past two days since the Fed decisions. The UST 2-10 rate curve is slightly less inverted at -70 bps. And their 1-5 curve is more inverted at -118 bps. Their 30 day-10yr curve is more inverted at -114 bps. The Australian ten year bond is down another -14 bps at 3.40% and a big shift lower. The China Govt ten year bond is down -2 bps at 2.93%. And the New Zealand Govt ten year is starting today at 4.10% and -11 bps lower.

Wall Street has opened it Thursday session with a +1.5% rise on both good earnings reports and encouragement the Fed is nearing the end of its hiking phase. The tech sector is doing especially well. Overnight, European markets all rose led by Frankfurt's +2.2% and trailed by London's +0.7%. Yesterday, Tokyo ended its Thursday session up a minor +0.2%. Hong Kong fell -0.5% on the day. Shanghai ended little-changed. The ASX200 ended up barely, up +0.1% yesterday while the NZX50 ended with a better +0.5% gain.

The price of gold will open today at US$1916/oz and down -US$8 from this time yesterday.

And oil prices start today with little net change at just under US$77/bbl in the US. The international Brent price is now just under US$83/bbl.

The Kiwi dollar is firm at 64.9 USc and up +½c. Against the Australian dollar we start today back up +½c too at 91.6 AUc. Against the euro we are back up +½c too at 59.5 euro cents. That all means our TWI-5 starts today at 71.4 and up +50 bps from yesterday and back to where we were this time last week.

The bitcoin price is now at US$23,817 and up a strong +3.6% from this time yesterday. Volatility over the past 24 hours has been high too at +/- 3.2%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

46 Comments

So the CCP drags Hong Kong into their swamp then wonders why nobody wants to visit. Won’t be me either. Comrade X on here won’t tell where I am on his or her list.

China is on all the West's lists: With 'US-style security' view, corn can have watchful eyes: Global Times editorial

Have you not read the new thought protocols? We have dispatched a team to your house to educate.

Ah, that explains the red firecracker in our letterbox then.

What's happened in Hong Kong is very sad. Thought police to the fore.

Consents for apartments do come in bunches by design.

That's a point, is a block counted as 300 new dwellings

One building one consent?

What about retirement villages ,?

Remember most of these new homes are for the Govt and their " housing the ever growing car sleepers/ motel dwellers"…. AKA-- " if I don't like my mates/parents I just go sleep in my car in Rotorua and wait for the " be kind agency's" to give me free ( tax payer subsidized) accomodations brah!"

It's also 300 new dwellings that don't get built if the project doesn't go anywhere because sales drop or finances unwind.

We need to get out of the mindset that one consented dwelling = one dwelling that is definitely going to happen.

It's one 'could-be' dwelling. The only thing it tells us for sure is that people are prepared to incur some level of cost to bet that the land itself will be profitable at some point in some way, and a project could be sold before anything is actually built. That may in fact be the actual point of the whole exercise - the actual dwelling building could be completely out of scope.

Absolutely true. Sales in NZ down 80? 90%?

A good example of this would be the secondary dwelling on my property, built by the previous owner. Consent granted in 2009, first inspection (foundations) in 2012, preline inspection 2017, final inspection 2019.

The beauty of doing it slowly like that is that for some people, it can be done without getting a mortgage.

yet 80% of building consents have CCC within two years.

Sure not all consents become dwellings, but we are comparing like for like, how many consents were issue today, compared with last year, when also some of those consents will not turn into dwellings.

Unless you want to wait 5 years for the data, it's as good as you are going to get.

The fact that the 1-5 year and 30 days - 10 year are more inverted means that the short term rates remain elevated. Let's see what the decision of all those mortgage owners who have to refix their interest rates will be. Longer term rates are becoming more enticing but more than the half of the financial world is shouting that central banks will cut interest rates later this year.

That's because interest rates are the one playbook central banks use.

I wonder how many people will have no option but to fix long, because they simply can't afford the shorter rates.

Doubtful, because the longer rates offered by banks are not much lower than short rates.

Those with mortgages due to roll over will be facing an uncertain decision. Choice will depend on both view of likely future rates and their risk tolerance.

Those who want to sleep with a degree of certainty are likely to look longer term. The uncertainty in economic future (e.g. Ukraine), likely future OCR rises in at least the short term, with likely inflationary wage, and longer term rates are currently below their bank stress tests rises support this . . . and if there are significant rate falls, well that is the price of that certainty.

Those looking shorter term will be those prepared to take a little bit of risk and uncertainty that the economy will improve, Ukraine won’t escalate, and OCR cuts are likely in the short to medium term.

Tough choice but depends a lot on personal risk appetite. I see Tony Alexander has put up a detailed argument and is recommending shorter term.

That view has already been priced into swap markets and so should be priced into mortgage rates too. So you shouldn't really try and guess where borrowing rates will go since the market gurus have already decided, unless you're Bill Gross or something. Rather, fix what makes sense to fix depending on whether you can afford to service it if rates go higher than the market currently expects etc.

Funny how we've gone from a housing shortage to a over supply!...

Couldn't be that building expensive houses for the homeless doesn't work!🙄.

Supply up demand down,. FHBs are gone and standby for the cash buyers / speculaters to kick ass and take names

not surprised FHB are not there, on a 800k home at 20% deposit over 30 years you looking at 1900 a fortnight payment. A heck of a burden to have, paying that.

and what are you even getting for that money! all these new townhouses aimed at FHB, too narrow to live in comfortably and will take your office working life to pay off, the myth of 'entry level'. I would happily buy a new townhouse if they were actually livable. Granny flats of the 70s look like palaces next to these things.

There's no unwinding the fact we all (middleclass and below), need to do more with less now.

Doing more with less is one thing.

Paying through the nose to do it for your entire working life is another.

Yeah, almost double what I pay to rent a 3brm in AKL, plus rates + insurance + maintenance + capital loss over time. The premium to be on the snake (formerly ladder) must be worth it to somebody I guess.

This should be no surprise as we have had record building and very low immigration. Housing crisis solved as we all wanted.

Now all we need is for a flood of immigrants to screw things up again.

Solved where? In Christchurch and the Hutt Valley perhaps.

Add Auckland to that list.

With house prices falling like they have been Im betting FHB are hoping to come in when the drop hits nearer the bottom.

We have a way to go yet.

Where is the over supply any way?

The UST 10yr yield starts today at 3.38%, and down another -8 bps from this time yesterday. That has added up to a -15 bps retreat in a week, most in the past two days since the Fed decisions.

This wasn't just expected, it has been practically inevitable.

What was behind the Fed's aggressive hawkishness from just a couple weeks ago? A whole lot of bad assumptions. What is behind the Fed's sudden conversion? The inevitable consequences of those assumptions. Lessons from history for what's going on right now.

Jet fuel up, low quality bitumen on the roads, no CO2 for beer....... We should build an oil refinery!

More tax to fund that purchase...whos in........??

Exactly - we have one of the most egregious regressive tax rates in the world. Link

From the Central Bank that had to be dragged kicking and screaming into the world of reality we now get:

Andrew Bailey has warned that interest rate rises may have to continue for longer if pay keeps rising in the face of surging inflation. The Governor of the Bank of England said policymakers "will have to respond" if wage data and inflation continue to "overshoot" to avoid the risk of such a situation becoming permanent.

Airline fuel starts to rise. We were warned that diesel is closely aligned to aviation fuel yet diesel has dropped in price quite nicely of late. For a while back Sept Oct it was more than 91. Watch that space.

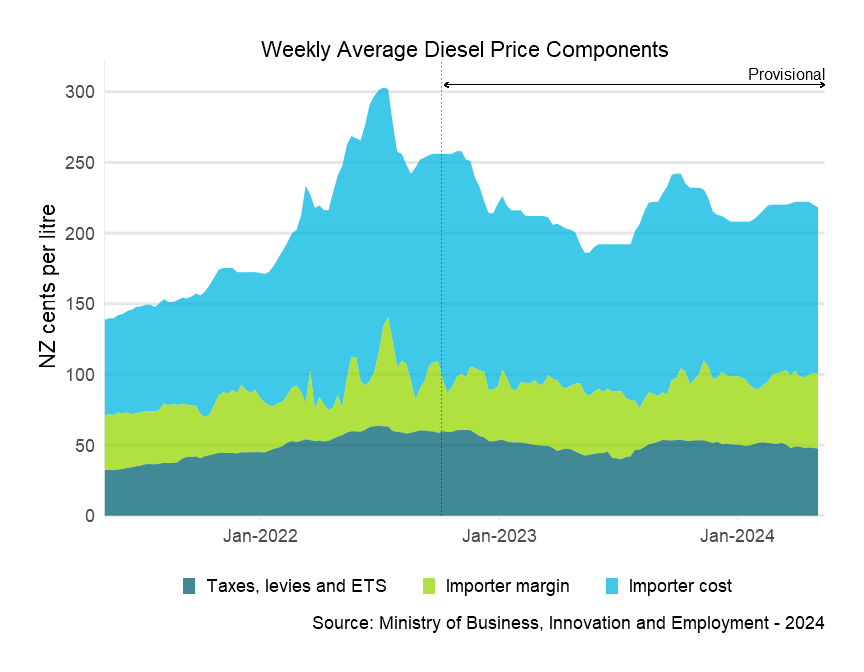

Some people think we are about see another oil price spike. There is some good diesel price stuff on the mbie website...

{kind=link}

When you hear economists confidently saying that domestically driven (non-tradable) inflation is up, remember that non-tradable CPI includes domestic airfares, which added about 0.2 percentage points to inflation in 2022. I wonder what a huge leap in international jetfuel prices will do to airfares?? Non-tradable inflation also includes a range of products (e.g. beef) that cost us whatever price our exporters can get overseas.

These details matter - we massively under-estimate how reliant we are on overseas prices, and we make stupid mistakes with our medieval monetary policy tools as a result.

The main issue with our decision making is the CPI numbers the RBNZ will rely on on Feb 23 include what happened in the first week of last October.

we massively under-estimate how reliant we are on overseas prices, and we make stupid mistakes with our medieval monetary policy tools as a result.

Lifting the OCR strengthens our exchange rate and alleviates the very issues you are complaining about.

It is true that offering a relatively higher rate of return on Govt Bonds attracts foreign capital into NZ dollars (balancing our trade deficit / holding currency value - note overseas investors now hold $60bn of our Govt bonds). But, a few fractions of a cent change to the NZD makes negligible difference when oil prices, dairy, beef etc are moving 10 - 20 times more up and down in a single year. One of the biggest challenges facing NZ is that we think we are in control of a lot more than we are. We have a kind of collective little man complex.

Fractions of a cent? If you think our exchange rate would still be between 0.64 - 0.65 on the greenback had we left our OCR at 0.25% the last year, I've got a bridge to sell you.

That isn't the counter-factual though is it? I am talking about the changes to OCR that were made in the last few months months or being considered in the next few months. Any impact on exchange rates from those will be tiny and drowned out by global factors.

I'm not sure why we even bother targeting overall inflation seeing as we can do sweet-FA about imported inflation. Why doesn't the RBNZ just target Non-Tradable inflation instead?

I'd rather the central planners stopped trying to control price signals and just closed up shop.

What would actually promote price stability in the short- to medium-term:

- Implement a strategic price control on fuel - set a single wholesale gate price, take the wins and losses on the Govt balance sheet and adjust the price overtime to smooth things out. MBIE already have the data they need to do this - they understand (to a fraction of a cent) what the importer and retail margins are

- Get the food wholesalers to agree a rolling fixed price annual contract for key items with major food producers (e.g. Fonterra) - set at cost + margin. This would insulate kiwis from the price swings we see when the Chinese and Japanese (for eg) bid up the price of our exports, which translates quickly into higher prices in our supermarkets

- Work towards a trade balance so we don't have to rely on monetary policy to protect the currency (Japan have got this nailed)

- Set the interest rate at 3% and just bloody leave it there - use LTV restrictions and other tools to restrain the flow of credit into the housing ponzi

- I would also Nationalise the food and construction material wholesalers, and implement a cap (wage-index-linked) on rent increases but I'm getting political now!

Just booked daughter a retunr flight to London on Singapore Airlines. Its about 4.8k and you have to pay in full now, I guess they hedge there fuel out 6-12 months as they book.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.