By Terry Baucher*

The first clue there might be some potentially significant tax changes in the Budget was when Inland Revenue announced on Wednesday afternoon it would be holding a post-Budget briefing. This is unusual and prompted some last-minute speculation much of which turned out to be wide of the mark.

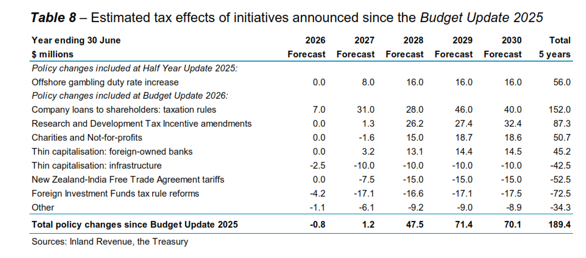

The main tax headline is the changes to the taxation of charities and not-for-profits. The good news for smaller organisations is that the amount of net income they can earn tax free each year is increased from $1,000 to $10,000. There will also be legislative clarifications to ensure membership subscriptions and levies received by not-for-profits remain non-taxable. This will be a huge relief for such organisations after Inland Revenue had indicated it thought subscriptions could be taxable.

The trade-off is capping eligible donations at $100,000 per person per year. However, in certain circumstances donors will be able to claim donation tax credit refunds during the year rather than wait until the end of the tax year.

Tackling the issue of shareholder loans

Last December Inland Revenue dropped a bombshell with proposed changes to the taxation of company loans to shareholders. In March the Government then beat a retreat after the proposal generated pushback from various sources including the ACT Party and New Zealand First. Work did continue on the issue of the treatment of outstanding shareholder loans when a company goes into liquidation owing tax.

The Budget includes legislation to make clear that a tax charge will arise if a shareholder owes money if a company goes into liquidation or is otherwise removed from the Companies Register. The amount of any outstanding loans will be taxed as income. My understanding is that the measure will have effect from 4th December 2025 as originally proposed and is expected to raise $152 million over the period to 2029-30.

There are changes to the Research and Development Tax Incentive, some to enable in-year payments and others to expand the range of R&D expenditure mining businesses can claim (cheers Shane!). But there is a reduction in the cap on non-internal software for R&D from $25 million to $3 million. This means overall the Government will gain $87.3 million over the forecast period.

Foreign Investment Fund changes

The Foreign Investment Fund (FIF) revenue account method introduced in last year’s Budget and targeted at migrants has now been extended to include New Zealand residents who are invested in unlisted overseas shares. Such investors will now have the option to be taxed on realised gains instead. Furthermore, the FIF de-minimis threshold will double to $100,000, a welcome move for many small investors. (Arguably, it also reflects the widespread non-compliance in this asset class).

Overall, the expected return on the specific tax initiatives is $189.4 million over the five years to 30th June 2030 per the table below.

Fiscal drag – helping balance the books, again

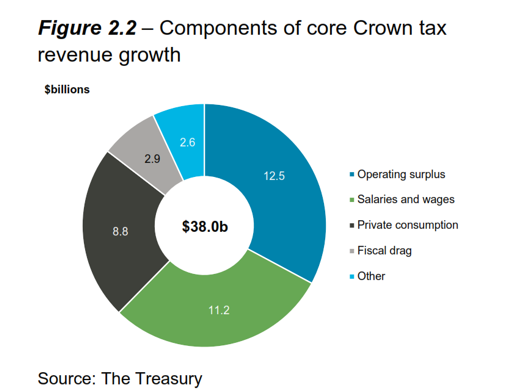

The Budget predicts that total tax revenue will rise by $38 billion over the period to 30th June 2030. $2.9 billion or 7.6% of this represents fiscal drag. This is where growth in salaries means average tax rates for individuals increase as they cross tax thresholds which have not been increased since 2024. Fiscal drag is a long-standing tactic which helps balance the books without attracting too much attention. We were given no indication of any increase in tax thresholds.

A tax by any other name… the new prudential levy on financial industry

Beforehand I expected some increases to various levies to help balance the books. Like fiscal drag it’s a well-worn path to raise revenue without directly increasing income tax or GST. The new prudential levy on the financial industry was not on my horizon, particularly since at $209 million over the four years to 2029-30 it’s the biggest single fund-raising initiative in the Budget. The levy will be paid to the Reserve Bank, but the expectation is that the revenue will flow through to the Government “through an increased dividend.” In other words, the levy is more than the cost recovery described in the Budget documents. It will be interesting to see how the banks respond to this.

Incentivising house building

David Seymour had floated the suggestion that councils be allowed to retain part of the GST collected on sales of new homes. That hasn’t happened, but instead from 1 April 2027 councils will receive payments for consenting new homes. The incentive payment starts at 0.25 per of the national average consent value for the first additional one percent of existing dwellings consented. This rises to 1.25 percent of the national average consent value where more than two percent of existing dwellings are consented.

This all sounds good but I do wonder if it might cause a short-term hiccup as it is arguably in councils’ self-interest to delay issuing consents until after 1 April 2027 when the payments start.

More Inland Revenue funding for litigation and compliance but less for front line services?

The headline announcement is that following on from prior years, Inland Revenue has been given an extra $15 million per year to boost debt compliance. However, when you drill down into the Vote Revenue Appropriations a different picture emerges.

Inland Revenue have not been excluded from the agencies subject to cuts. To meet those targets its total appropriation for the 2026-27 year has been cut by just over $15 million to $771 million. This includes the effect of the additional $15 million boost. This implies nearly $30 million of cuts from the 2025-26 year.

Services to manage debt and unfiled returns take the brunt of this hit with a reduction by over $20 million from the prior year. Services to Ministers and to assist and inform customers to get it right from the start – probably the main public-facing part of Inland Revenue, falls by $3.5 million. This seems at odds with maximising revenue collection and I am personally highly sceptical that AI systems will be able to take up the slack as apparently expected. Expect telephone hold times to lengthen.

On the other hand, the appropriation for undertaking investigation, audit and litigation activities rises by $10.1 million to over $146 million. This reflects increased investigation activity we are seeing and also will fund court cases several of which relate to crypto-asset taxation involving “tens of millions of dollars.”

Overall, this was a much more interesting Budget from a tax perspective than I anticipated. As usual there’s a lot of devils in the detail, some welcome and others not so welcome.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.