The last couple of weeks or so I've been talking about the changes to the threshold for the application of the Foreign Investment Fund (FIF) rules with effect from 1st April this year. The change means that if the cost of your foreign investment funds, typically overseas shares is less than $100,000, you do not need to enter the FIF regime. Instead, you only need to return dividends, and, if you're a share trader, any capital gains. Notwithstanding the new threshold a taxpayer can continue to elect to opt into the FIF regime.

The new threshold drew some interesting commentary in the media with some noting the change seems to favour the wealthy. The Minister of Revenue, Simon Watts, rejected that assertion by saying that he would not see people holding $100,000 or less of shares as wealthy.

So who holds FIFs?

Many of our clients have investments within the FIF regime. and the majority of them acquired those interests when they were either working overseas on an OE or before they migrated here. In many cases, they're professionals who took advantage of tax-preferred schemes, such as the United Kingdom's Individual Savings Accounts, or maybe acquired shares through employee share ownership plans.

It's also worth noting that many overseas jurisdictions have considerably deeper capital markets than here, so investing on the stock market is perhaps more common, although the advent of KiwiSaver and Sharesies has made a huge difference.

The FIF regime – a quasi-wealth tax

When I'm looking at this issue, it's not so much whether $100,000 of overseas investments can be considered wealthy although someone holding that level certainly would be above average wealth, but rather how the clients see the FIF regime. It’s very unique compared with how overseas Jurisdictions particularly in how it taxes on an unrealised basis. This makes it very much like a wealth tax. In fact, that's how I describe it to overseas clients and advisors, most of whom come from jurisdictions with capital gains tax regime which mostly work on a realised basis.

I believe there's a considerable amount of non-compliance with the FIF regime. We regularly file voluntary disclosures of FIF income for clients, mainly because clients are completely unaware of its scope and operation until something triggers it. They may come across something or in some cases Inland Revenue catches up with them and asks a few pertinent questions.

A welcome increase

Against that background, the increase in the minimum threshold to $100,000 to me is welcome. I think the expansion of the FIF revenue account method for unlisted shares is also welcome because it aligns with a laypersons concept of how a capital gains tax regime operates.

Anyone who has migrated here from Australia, the United Kingdom or the United States, will have encountered capital gains taxes. And one of the things about capital gains tax is a realisation is a potential taxable event. My observation is that most people when they're thinking about tax and how systems work, it's really around money flows. If money comes in, they think that might be a taxable event - if they receive an inheritance, for example. But more importantly, if they are selling stocks or overseas properties, there’s an awareness it could have tax consequences.

Is a Capital Gains Tax too complex?

A frequent counterargument to a capital gains tax is its complexity. My response to that is the FIF regime is complex and as I said above, its unrealised basis of taxation counter intuitive. Alongside that consider the bright-line test, the treatment of commercial property, then associated property transactions for those dealing in land or builders, etc together with other carve-outs for farmers and main homes. In short, the existing tax treatment system is complicated. And that's before we get to the financial arrangements regime.

I've always been of the view that perverse as it may seem to opponents, a capital gains tax regime would probably simplify matters for many people. Now, that’s not to say there's always devil in the detail. We talk about that all the time. But I think in terms of understanding where people think they may have compliance, a CGT scheme is much more understandable than the foreign investment fund regime.

What to get GST for its fortieth birthday? An Inland Revenue issues paper.

Moving on, Inland Revenue has issued an officials issue paper for consultation on current GST issues, just in time for the introduction of GST's 40th birthday on 1st October. GST is a very important tax for the Government because of its broad base and relatively low rate compared to other jurisdictions. This makes it an extremely efficient tax gatherer. For example, the Budget projected GST revenue of $33.1 billion for the year to 30th June 2027. To put that in context this is expected to be just over 22% of the total forecast government revenue for the year.

GST is not a simple tax though; this is perhaps one of those common misconceptions about it because of its broad reach. Like all taxes there are interesting and complex issues on the boundaries and with its operation. As paragraph 1.2 notes

“While the GST system generally works well, a number of issues have been identified where the legislation produces outcomes that do not reflect the underlying policy or intent or where technical changes could improve the way the system operates. Addressing these issues would improve the certainty, efficiency, integrity and fairness of the GST rules.”

Eight issues under review

The paper reviews eight topics it thinks may merit further consideration. It starts with the question of the definition of dwellings and commercial dwellings, which is quite important for GST purposes because commercial dwellings, if a person is in long-term accommodation, GST applies at 60% of the standard 15% rate, or effectively 9%. Inland Revenue’s question is whether the definitions of what represents “commercial dwellings” can be improved?

This might seem a little arcane, but commercial dwellings definition could impact emergency housing and student accommodation. You can see why it’s relevant.

Chapter 3 reviews the issue of electricity being exported to the grid from residential premises and what happens if the surplus being exported to the grid is made from a GST registered person. Again, quite a technical issue, but it's something that's going to happen more often. Bear in mind that income tax changes have been made to treat those proceeds or offsets as not being taxable for income tax purposes.

Chapter 4 reviews some GST cross-border issues in relation to non-residents suppliers who are usually making supplies to GST registered entities in New Zealand and the practical effects of requiring registration in certain circumstances.

Chapter 5 considers the issue of correcting errors and inaccuracies. Apparently, our legislative framework is a little less coherent in this approach than overseas jurisdictions. There are also some inconsistencies with other legislation. For example, generally speaking, refunds for more than four years ago are not permitted for income tax purposes. However, in some GST cases, it’s possible to make claims going back eight years. Understandably, Inland Revenue wants to resolve that discrepancy.

Chapter 6 is mostly technical and discusses a range of miscellaneous changes including claiming GST on pre-registration expenses and whether a group GST registration should have a separate IRD number rather than the IRD number of the group representative?

Modernising the GST Act

Chapter 7 is something I'd probably have put first, and that is modernising the Goods and Services Tax Act 1985 which is now over 40 years old. A lot of amendments have been passed in that time so it’s not easy to follow.

The issues paper asks whether there should be a complete rewrite as was done with the Income Tax Act? It concludes it’s not necessary partly because Inland Revenue doesn't presently have the resources for what would be a fairly major move. I agree with that conclusion.

On the other hand, reordering the act and tidying it up and presenting it in a more cohesive manner is something I think should be done. For example, section 20 deals with the “Calculation of tax payable” and currently runs to more than 35 subsections. I believe restructuring and renumbering the act would be strongly supported by tax specialists.

GST and international business events

Chapter 8 has an interesting review about the GST treatment of business events such as conferences and conventions supplied non-resident businesses. This is an issue raised by parts of the tourism industry. The paper suggests this is perhaps a zero-sum game in that a non-resident business could register for GST and reclaim some of the input tax on business event services. Apparently, Singapore and Australia have specific GST rules for business event services and the paper canvasses whether similar rules could apply here.

International developments and improving GST administration

Chapter 9 considers international developments in GST/VAT administration. This primarily considers digital reporting tools and improving administration of the tax such as the use of e-invoicing. The paper notes that when looking at what's happening in the rest of the world in digital reporting, we may have slipped behind in terms of efficiencies noting “developments suggest that New Zealand’s current approach is more cautious than some comparable jurisdictions.” Should New Zealand follow the lead of countries such as Singapore and the United Kingdom?

This chapter considers an interesting point from Australia where if someone is defaulting on their GST returns, they are moved from reporting quarterly to reporting monthly as a means of improving debt collection. The view is increased reporting means better debt intervention. We already have bi-monthly reporting as the standard and monthly reporting is also available. (As an aside I think quarterly reporting as in Australia and the UK would be helpful).

I understand the thinking, but I think it's better for Inland Revenue's own systems to be picking up GST defaults much sooner, say if two successive GST returns are in default. I think you don't need legislative changes to enable this, rather Inland Revenue should use the tools it already has,

What about GST on fees to managed funds?

Overall, there’s quite a lot to consider in this paper. I am surprised to see that the question of GST on fees charged to managed funds is not included. Back in September 2022, the last Labour government introduced a proposal to apply GST on such fees. This was to clarify the ad hoc approach which meant newer entrants to the market were paying GST, but older market operators were not.

The proposal provoked a storm of protest resulting in the Government backing down very rapidly, within 24 hours on the proposal, instead leaving it to Inland Revenue to ‘review’. In terms of major issues, I would have thought this was probably quite a significant issue because the numbers were quite large (an estimated $225 million annually), but it’s not included (and therefore it must be assumed the present treatment is acceptable).

Inland Revenue is seeking consultation on 56 questions across the various topics and submissions are now open until 29th June.

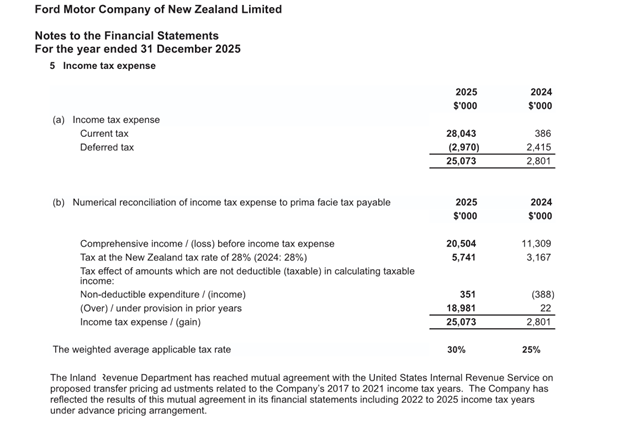

Ford forks out $18 million in back tax

Finally, this week, we frequently discuss the question of transfer pricing and overseas payments made by New Zealand subsidiaries of overseas companies. to tax havens or tax favoured jurisdictions and the effect on the tax base. Most of the time we are thinking perhaps of Google and the over one billion dollars in service fees paid to Singapore.

It's therefore interesting to see Thomas Manch of Business Desk report that Ford Motor Company of New Zealand Limited’s 31st December 2025 financial statements included a comment regarding settlement of a transfer pricing dispute with Inland Revenue. Note 5 to the accounts (see below) records an under provision of tax in prior years of just under $19 million. The result was Ford Motor Company’s tax bill for the year went up from $2.8 million for the year ended 31 December 2024 to just over $25 million for the year ended 31 December 2025.

It’s tempting to be cynical and think Inland Revenue is not paying a lot of attention to transfer pricing, but clearly this is a matter that has been in some dispute for quite some time as the adjustments go back to the year ended 31st December 2017. This also shows that these disputes can take some time to settle. Inland Revenue will be happy with this win, and it will be interesting to see what other disputes may be going on.

And on that note, that’s all for this week I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.