By David Norman*

This increase in size is being driven by a desire for more efficient vessels (much like the changes seen in the aircraft industry) and growth in world trade over the longer term.

In the short- to medium-term, the surge in vessel size in New Zealand is also being driven by a mismatch between shipping capacity and demand, with both the GFC and the recent slowdown in China reducing the latter.

Bigger ships are much cheaper to operate. They are estimated to reduce costs per container carried dramatically – by up to 50% or more in some cases. They use less fuel per container, and ships are staffed by a similar number of crew members almost regardless of size. With an oversupply of capacity, shipping lines are moving bigger ships onto routes traditionally served by smaller vessels.

We have pointed out that ports would need to upgrade infrastructure through further gantry cranes, dredging and the like to meet the needs of larger vessels. The cost of these upgrades and the efficiency gains of large vessels make it very likely that the number of New Zealand ports being directly served by international container vessels will fall over the next 15 to 20 years, probably to between four and six ports. Some ports have seen the writing on the wall, and are engaging in tie-ups that will ensure an ongoing role for smaller ports as feeders (via coastal shipping) into larger ports.

But there are detractors from this view. Some have suggested that point-to-point shipping will predominate, with ship sizes to suit. So, for instance, smaller New Zealand ports would continue to operate, served by smaller ships, with direct links to overseas ports. But this view seems at odds with the evidence.

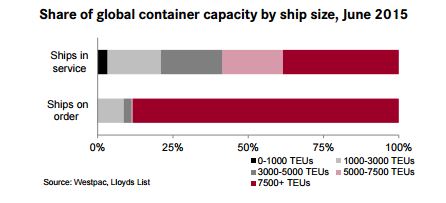

The efficiency advantages of larger vessels have resulted in even large markets like Northern Europe (the corridor from France to Sweden) being predominantly served by just six ports on main Asia-Europe route. Coastal shipping or overland transport modes get product to and from these large ports.

The mix of imports and exports passing through New Zealand ports is heavily weighted in favour of exports. Many more containers are imported empty than those that are exported empty. The cost of carrying empty containers in one or both directions dramatically raises the cost per container, which makes long-distance point-to-point routes unattractive.

As a result, almost all international container ships visiting New Zealand already include at least one Australian port on their itineraries. Indeed, on average only 38% of containers on vessels travelling to New Zealand are unloaded here. Larger import markets (e.g. Sydney or Melbourne) mean many containers can be full for a longer proportion of the trip from Malaysia or Shanghai for instance.

Point-to-point international shipping may ironically mean less direct access to world markets to New Zealand as the only distance over which carrying such a mix of empty and full containers may be economically viable would be to Australia. New Zealand businesses would then be reliant on less direct trans-Tasman hubbing through Sydney, Melbourne or Brisbane, to access larger vessels to Asia or North America.

On the other hand, some have expressed concern that the number of ships visiting New Zealand will plummet as ship size rises. But this outcome is not necessitated by ship size growth. The number of ships visiting New Zealand each week is also a function of the growth in New Zealand container demand. This demand is in turn a function of our increased trade with the world, and a move to more containerisation of products.

Sea change?

We estimate that although bigger ships will predominate in the future, the number of container vessel visits per week will also likely grow. These estimations have massive implications for port infrastructure and the role individual ports will play in the international container freight picture.

We developed a range of likely outcomes for the average size of container ships, the number of unique ship visits to New Zealand each week, and several other factors that flow on from these (see how later on). Scenarios ranged from very large ships and few weekly visits, requiring high levels of infrastructure investment from a few major ports, to the opposite, where less investment would be required, and more weekly visits (possibly to more ports) were likely.

Our analysis suggests that by 2030:

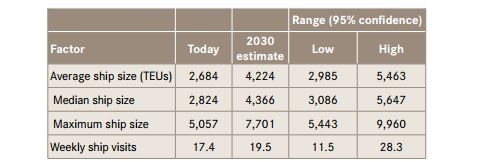

• The average size of international container vessels visiting New Zealand is likely to rise to between 3,000 TEUs and 5,500 TEUs.

• However, ports will need to plan for far larger vessels than this. Median ship sizes may be as high as 5,650 TEUs by 2030, while maximum vessel size could reach 10,000 TEUs although a number around 7,700 TEUs is more likely. Vessels carrying 7,700 TEUs are approximately 330 metres long and have a draught of around 14.5 metres.

• The number of unique ship visits to New Zealand will likely range between 12 and 28 a week, a change from 17 a week today. The mid-range scenario suggests around 20 visits a week, up slightly from today.

What this means for New Zealand

• Competition and choice should remain reasonable: Concerns that vessel size growth will leave New Zealand reliant on just a handful of ship visits a week seem unjustified. Even as ship size increases, the number of weekly ship visits is still most likely to rise because of growth in merchandise trade and containerisation. This is good news for New Zealand exporters and importers, as competition will likely be stronger than some are concerned it may be, keeping prices lower.

• Port infrastructure will need to accommodate larger ships and more exchanges per visit: It will not make sense for all ports to upgrade for larger ships. Ships may well dock at fewer ports per visit to New Zealand, while the number of container exchanges per ship visit and per port visit will rise. Shipping lines will be looking to minimise the time spent in port, so better crane facilities (more, larger and faster) will be required in ports that service larger vessels, to allow quicker turnarounds.

• The net effect on freight costs for New Zealand businesses is uncertain: Larger vessels are estimated to reduce costs per container carried dramatically. But if fewer New Zealand ports are served by international vessels, a lot of freight will need to be moved by road, rail or coastal shipping within New Zealand. If this is done inefficiently, this may actually raise the transport costs for businesses located longer distances away from the smaller number of ports served by larger container vessels. On the other hand, businesses located close to major ports would benefit from the far lower international shipping costs. i.e. there may be winners and losers among New Zealand businesses.

How we modelled growth

We examined data from a number of sources including Freight Information Gathering System (FIGS) data gathered by the Ministry of Transport. This data revealed a wide range of trends including average, median, and largest visiting ship size (in TEUs), number of unique visits per week or year, total TEU capacity of container ships visiting in any given time period and so on.

From this data, we were able to identify historical growth rates and averages across a number of different factors. We then used these figures to set upper and lower bounds for a Monte Carlo analysis using 100,000 iterations. Monte Carlo analysis allows us to model the likely change in each factor and to determine the combined impact of different factors on the likely shape of international container shipping in New Zealand by 2030.

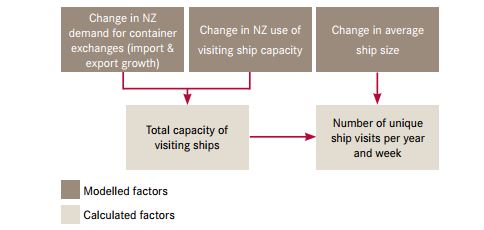

The logic of the model is set out in the diagram.

We modelled the three brown boxes to determine the outputs in the beige boxes.

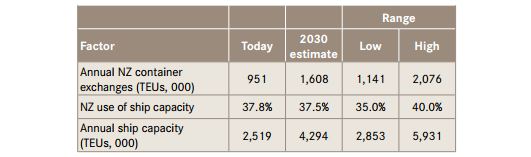

• Change in NZ demand for container exchanges: New Zealand currently exchanges around 951,000 containers a year. i.e. imports containers (either full or empty) and exports containers (either full or empty). Growth in this number will be determined by New Zealand’s expected merchandise trade growth rates, and the extent to which the trend toward increased containerisation continues.

• Change in NZ use of visiting ship capacity: For the June 2015 year, the capacity of ships visiting New Zealand was 2,519,000 TEUs. This implies that containers imported into and exported from New Zealand accounted for around 37.8% of the capacity of the ships servicing New Zealand (951,000 / 2,519,000). i.e. New Zealand ports are among a larger group of ports included on a typical itinerary that usually includes Australia as well. Over the last three years, this usage figure has hovered within a narrow band of 35.8% to 39.1%. This means the total capacity of all ships (not individual ship size) servicing New Zealand has grown in line with our demand for exchanges. Clearly this is a range that ship operators find profitable or it would not continue.

• Change in ship size: The size of the average ship servicing New Zealand has grown 4.3% a year over the last eight years. Some of this change is the natural trend toward larger, more efficient ships, and some of it is because of excess capacity due to the downturn in China, and before that, the GFC.

We acknowledge that there are some relationships between the brown boxes that are not explicitly modelled. For instance, ship size and NZ demand for container exchanges are related, but this link is weak. World shipping capacity growth is driving the size of vessel visiting New Zealand (bounded by our current port infrastructure) far more than NZ demand for exchanges. Similarly, there will be a link between average ship size and NZ use of visiting ship capacity such that the latter stays within a financially sensible band. But these factors could both be moderated by simply reducing the number of weekly ship visits to New Zealand if shipping lines felt the need.

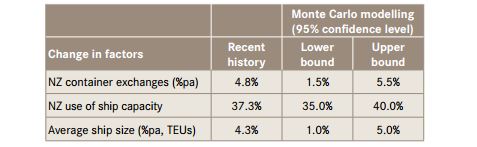

Our Monte Carlo analysis used the following ranges to model the likely outcomes for 2030.

In the case of ship size and container throughput growth, we assumed that recent growth rates were toward the high end of the likely band, in line with discussions with players in the industry. However, it is possible that continued global weakness, if it persists for several years, may increase the average ship size visiting here even more. And if better than-expected gains are had from the signing of the TransPacific Partnership Agreement (TPPA), growth in demand for container exchanges could be even higher than in the recent past. We have made some allowance for this, as well as for growth to be at the low end of the spectrum.

The analysis using these parameters yielded the following results:

• Containerised trade (exchanges) is expected to reach between 1.14 million and 2.08 million TEUs by 2030, with a mid-range estimate of 1.61 million, which implies growth of 1.2% to 5.3% a year.

• New Zealand’s use of TEU capacity of visiting ships is expected to remain in a relatively tight range from 37.2% to 37.9%.

• The implied annual ship capacity will see growth to between 3.01 million and 5.59 million TEUs.

David Norman is an Industry Economist at Westpac Insitutional Bank. This article is a re-post from here, and is used with permission.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.