By Justin Yifu Lin*

Among its objectives are a doubling of GDP and average rural and urban household incomes relative to their 2010 levels.

These targets would require China’s economy to grow at an average annual rate of at least 6.5% during the next five years. While this pace would be significantly slower than the 9.7% growth the country has averaged since 1979, it is undeniably fast by international standards. And, given that China’s growth has decelerated every quarter since the beginning of 2010, some have questioned whether it is achievable. I believe that it is.

Economic growth results from increases in labor productivity caused by technological advance and industrial upgrading.

High-income countries, already on the cutting edge of productivity, must earn their increases through technological and organizational breakthroughs; as a result, their typical growth rate is about 3%. Developing countries, however, could potentially accelerate productivity growth, and thus GDP growth, by borrowing technology from advanced countries – that is, tapping the latecomers’ advantage, as China has done.

The question for China, after 36 years of catching up, is how much longer it can continue to benefit from this process.

Some scholars believe it has reached its limits. Using historical data compiled by the economic historian Angus Maddison, they show how other East Asian countries experienced a deceleration of economic growth after their per capita GDP reached about $11,000 in purchasing-power-parity terms relative to constant 1990 US dollar prices, or $17,000 in constant 2005 US dollar prices.

For example, in the five years after Japan reached that level, its economy grew at an average annual rate of 3.6%. In South Korea, growth fell to 4.8%. In Hong Kong, it slowed to 5.8%. Given that China is projected to cross the same threshold sometime this year, many believe its average annual growth over the next five years will fall well below 7%.

I disagree.

What this analysis fails to take into account is the fact that advanced countries are not sitting by idly; they are growing and making technological breakthroughs. And that creates opportunities for developing countries to continue to learn.

Those who predict a slowdown in China are correct to look at its per capita GDP, which is a reflection of a country’s average labor productivity and thus the level of its technical and industrial advancement. But the best indicator of China’s growth potential is not its per capita GDP relative to some arbitrary threshold; it is the difference in per capita GDP between China and the United States, the world’s most advanced economy. And on this measure, China has plenty of room for expansion.

When Japan crossed the $11,000 threshold in 1972, its per capita GDP was 72% of the US level. When Taiwan crossed it in 1992, its per capita GDP was 48% of America’s. The comparable figure for China today is only about 30%.

In 2008 – the last year for which Maddison provided figures before he died in 2010 – China’s per capita GDP was 21% of the US level. By examining how other East Asian economies performed when they were at a similar point compared to the US, we can estimate China’s potential for growth.

Japan’s per capita GDP was 21% of America’s in 1951, and in the following 20 years it grew at an average rate of 9.2%. In the two decades after Singapore hit that level in 1967, it grew at an average of 8.6%. And the story is similar in Taiwan, Hong Kong, and South Korea; in the 20 years after their per capita GDP were 21% of the US level, they grew at around 8%. There is no reason not to believe that China has the potential to do the same until 2018.

The Chinese economy’s current slowdown is the result of external and cyclical factors, not some natural limit. China has been suffering from the aftereffects of the 2008 financial crisis and plummeting export demand. From 1979 to 2013, annual export growth averaged 16.8%. In 2014, it dropped to 6.1%; in 2015, it dropped further, to -1.8 %.

This external drag is likely to continue, as politics in developed countries impedes efforts to implement the structural reforms – such as reducing wages, lowering social benefits, financial deleveraging, and consolidating budget deficits – needed to revive economic growth. Indeed, like Japan beginning in 1991, much of the developed world risks lost decades.

To achieve its growth targets, China will have to rely on domestic demand, including investment and consumption. Thankfully, it has strong prospects in both areas. Unlike developed countries, which often struggle to find productive investment opportunities, China can pursue improvements in infrastructure, urbanization efforts, environmental management, and high-tech industries. And, unlike many of its developing-country rivals, China has ample fiscal space, household savings, and foreign-exchange reserves for such investments. The investments will generate jobs, household income, and consumption.

As a result, even if external conditions do not improve, achieving 6.5% and above annual growth is well within China’s reach. In that case, the country will continue to be the world’s primary economic engine, contributing about 30% of global growth until at least 2020.

Justin Yifu Lin, a former chief economist and senior vice president at the World Bank, is Professor and Honorary Dean of the National School of Development, Peking University, and the founding director of the China Center for Economic Research. Copyright: Project Syndicate, 2016, and published here with permission.

6 Comments

'Japan’s per capita GDP was 21% of America’s in 1951, and in the following 20 years it grew at an average rate of 9.2%.'

This is cherry-picking.

Since its peak around 1990, Japan has been on a long downward slide that mimics the Nikkei:

https://in.finance.yahoo.com/q/bc?s=%5EN225&t=my&l=on&z=l&q=l&c=

Frantic money-printing by BoJ in recent years has bolstered the share market but has not fixed the underlying predicament caused by too many people and not enough resources.

China is now in a similar boat (too many people, not enough resources) but also has a severely messed-up environment and rapid overheating (literally) to deal with. And has a Japan that is starting to look desperate and is rearming in preparation for war as a neighbour.

Sorry Justin, China is corrupt to the core. Unfortunately New Zealand has embraced the corruption. At the corporate level , the unwind has only just begun, whether the state allows these companies to fail now or continues to prop them up only time will tell. The bankruptcy of Guangxi Non ferrous metals group last week is an indication of how weak the Chinese economy is. And once again there is that company Shanghai Pengxin, whose former chairman of its primary subsidiary the state backed Pengxin International Mining Li Tong currently under investigation by the State. Li Tong previously Vice President of the state backed Guangxi metals.

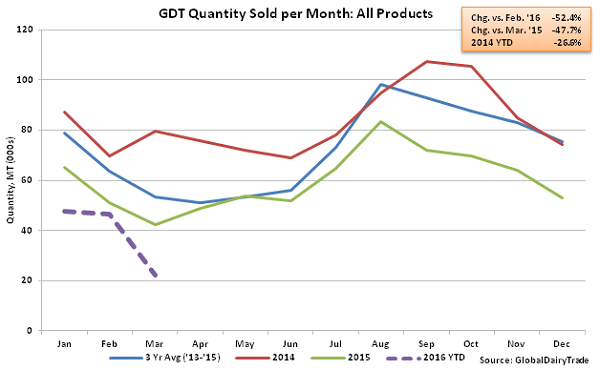

"We are turning negative on China's dairy sector," Mr Leung said. "While raw milk prices have rebounded a little in recent months, we don't expect a meaningful recovery in 2016 because, one, there is still an abundant global supply of raw milk, and, two, prices in China are still much higher than overseas."

Imported milk cheaper: The price of imported milk from New Zealand was 34 per cent cheaper than China's domestic product, and this included import tariffs, sales taxes and transport costs, he said.

http://m.smh.com.au/business/hsbc-negative-on-chinese-dairy-consumption…

{kind=link}

We remember Sandy (rarabank), but the news from many on the ground there has started to turn.

https://m.youtube.com/watch?v=-wo5TznA5as

Dear leader may never be back if this keeps up. What just happened?

We do miss the cooking..

http://www.bloombergview.com/articles/2016-03-28/investors-are-in-denia…

Back in 2009, as China unleashed a massive fiscal stimulus and investment spree in response to the global financial crisis, the rest of the world was all too willing to believe the impossible. Aided by consultant research predicting decades of explosive growth, companies placed huge bets on China and expected to ride the never-ending boom to riches.

Amid the gold rush, they bulked up to sell China t-shirts or tons of iron ore. They urged their governments to sign free-trade deals with Beijing. Commodity producers heedlessly expanded capacity, believing that 10 percent growth would continue indefinitely. Consumer brands rushed to set up flagships in third-tier Chinese cities. Shipping companies scrambled to build new fleets to meet an expected explosion in global trade.

However, as with so many previous bouts of irrational exuberance, this time wasn't really different. The ruthless rules of supply and demand still applied. And now, the longer that painful decisions are delayed, the harder they'll become.

.... companies and countries alike need to face up to their own irrational exuberance. Whether it's failing to diversify, spending recklessly on the back of high prices, or taking on too much debt, fundamental mistakes can't be blamed on China. Doing so only delays the inevitable.

Few investors seem to fully appreciate the balance-sheet reckoning that is coming. Failing to address the global supply glut only increases the risk of a larger correction. We know that because this time isn't different: The bill always comes due.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners. To contact the author of this story:

Christopher Balding at cbalding@phbs.pku.edu.cn

http://www.zerohedge.com/news/2016-03-28/america-hits-rock-bottom-citie…

We have been doing it for Years...now someone is emulating us.

We also give em a home and a motorbike.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.