New Zealand banks have the lowest level of non-performing loans in the OECD and a return on equity that's double the OECD median, the Reserve Bank says.

A useful table published in Wednesday's Financial Stability Report (see below) details where NZ's banking system measures, across a range of metrics, against Organisation for Economic Co-operation and Development counterparts.

This shows the NZ banking system has the lowest ratio of non-performing loans to gross lending in the OECD at just 0.6%. The OECD median is 4.4%. NZ banks also come in lowest in non-interest expenses to gross income at 42%, versus the OECD median of 62%. And local banks place fourth in terms of return on equity at 18.6%, almost double the OECD median of 9.2%.

Noting NZ ranks high on profitability metrics, the Reserve Bank suggests this may indicate the banking system is efficient in its use of assets based on return on assets, capital and resources.

Analysis by interest.co.nz shows NZ's big four banks topped a range of countries benchmarked by the Bank for International Settlements, in terms of net income as a percentage of total assets, at 1.53% in 2015.

"The profitability metrics may partly reflect the high degree of concentration in New Zealand’s banking system. However, banks in New Zealand appear to be relatively efficient in the core intermediation role of receiving money in the form of deposits and recycling that money via loans to creditworthy borrowers. The cost of intermediation in New Zealand, measured by the spread between the weighted average retail lending rate and retail deposit rate, is below the average of 20 OECD countries in the sample," the Reserve Bank says.

Efficiency of New Zealand banking system relative to OECD peers, at Q2 2016 or latest data

(%, unless specified)

| N Z | OECD median(a) |

OECD maximum |

OECD minimum |

N Z rank(b) |

|

| % | % | % | % | ||

| Profitability | |||||

| Return on assets(c) | 1.4 | 0.8 | 1.9 | 0.1 | 8 (of 26) |

| Return on equity(d) | 18.6 | 9.2 | 19.2 | 0.3 | 4 (of 26) |

| Non-interest expenses to gross income(e) |

42 | 62 | 76 | 42 | 1 (of 24) |

| Intermediation | |||||

| Spread between loan and deposit rates(f) (basis points) |

233 | 278 | 996 | 115 | 9 (of 20) |

| NPLs to total gross lending(g) | 0.6 | 4.4 | 37.0 | 0.6 | 1 (of 26) |

| SOURCE: European Central Bank, IMF, registered banks' Disclosure Statements, private reporting, RBNZ SSR | |||||

| Notes: (a) Median of the sample of OECD countries for which data available for each metric. (b) 'New Zealand rank' is scaled so that the top ranking country is the most efficient for that particular metric. (c) Return on assets = (net annual income before tax / average total assets) x 100; a measure of banks' efficiency in the use of assets (d) Return on equity = (net annual income before tax / average total capital) x 100; a measure of banks' efficiency in the use of capital (e) Non-interest expenses to gross income = (net annual operating expenses / (net annual interest income + annual non-interest income)) x 100; a measure of the banks' efficiency in the use of resources. (f) Spread between loan and deposit rates = (difference between the weighted average loan rate and weighted average deposit rate, excluding rates on interbank loans and deposits) x 100; a measure of the cost of intermediation. (g) NPLs to total gross lending = (total non-performing loans / total gross lending) x 100; a measure of banks' allocative efficiency. |

|||||

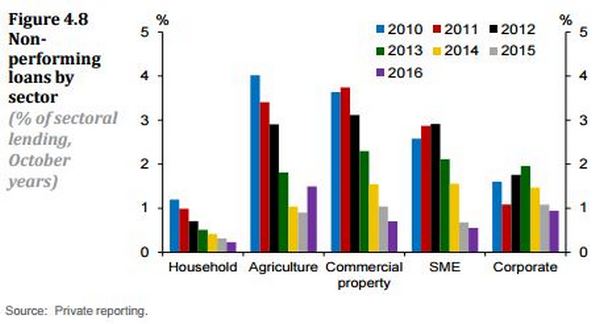

The chart below also comes from the Reserve Bank's Financial Stability Report.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

2 Comments

However, banks in New Zealand appear to be relatively efficient in the core intermediation role of receiving money in the form of deposits and recycling that money via loans to creditworthy borrowers.....," the Reserve Bank says.

What part of our credit based banking system does the RBNZ not comprehend? Read more

RBNZ: pls note the high return to equity of banks in nothing to brag about, it is a failing.

A return on equity of 18.6%, means they are overleveraged, or underpaying depositors, or both.

With that return to equity they can fund high credit growth of 9% and pay a 4% imputed dividend.

Being able to fund 9% credit growth is causing NZ issues, so perhaps time for RBNZ to impose a countercyclical buffer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.