By Gareth Vaughan

Can banks boost their household deposit funding by increasing their deposit interest rates?

This is a question the Reserve Bank ponders in its latest Financial Stability Report. And as you'd expect, the answer is yes.

The Reserve Bank analysis concludes that a 100 basis point increase in the six-month term deposit rate lifts the level of household deposits by between 1% and 1.5%, or $1.5 billion to $2.4 billion, after four to six quarters.

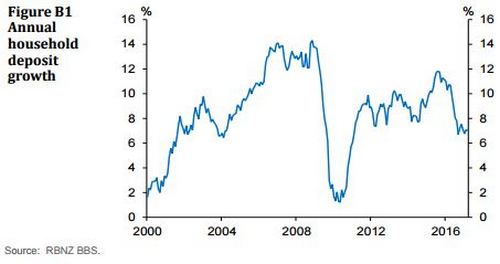

Household deposits represent 40% of New Zealand bank funding, according to the Reserve Bank. However, over the past two years annual growth in household deposits has slowed to 7% from 11%. For banks, who need deposits to help meet their Reserve Bank enforced Core Funding Ratio requirements, this is a serious matter. A drop in deposit funding also tends to send the major banks overseas, cap in hand, thus increasing their exposure to international risks that can hit the cost, and even availability, of funding.

Some of the slowdown in household deposit growth is due to an increase in business deposits and wholesale deposit accounts, the Reserve Bank suggests, with this reflecting a "natural flow" of deposits through sectors of the economy as payments and money transfers are made.

"This could be associated with the increase in household consumption growth in 2016, and there is also evidence that households shifted from investing savings in bank deposits to other investment products. This is likely to reflect households seeking greater investment returns in other assets, such as equities," the Reserve Bank says.

The Reserve Bank modelled how demand and supply shocks affect household deposit growth. In its model, a household deposit demand shock is assumed to be driven by banks’ relative cost of funding. For example, when it's more expensive to borrow money overseas a bank therefore wants to attract more household deposits. In contrast, a household deposit supply shock stems from households, and is deemed to be a change in household risk preferences.

"Other factors such as relative asset returns and volatility, income growth and consumption growth also influence demand and supply dynamics, and these factors are identified by the model as ‘other shocks’," the Reserve Bank says.

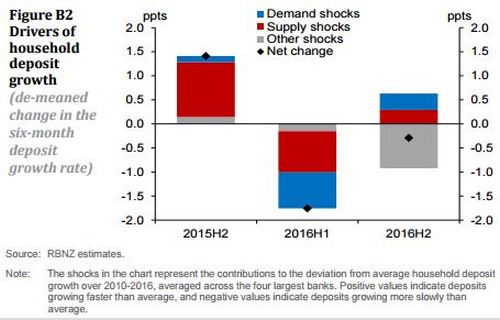

Figure B2 below highlights the contributions of supply and demand factors to six monthly changes in household deposit growth during 2015 and 2016.

"The analysis suggests that in the second half of 2015, above average household deposit growth was largely attributable to a strong supply of deposits. However, household deposit growth fell below average during the first half of 2016, as both deposit supply and demand weakened. During this period, the gap between credit and deposit growth emerged and banks increased their reliance on offshore funding. In the second half of 2016, banks tried to close the funding gap by increasing deposit rates and households shifted towards holding more deposits. However, deposit growth remained below its trend level due to ‘other shocks’, for example, strong household consumption growth," the Reserve Bank says.

Additionally the Reserve Bank used a second model to estimate the cost to banks of borrowing via deposits. This model assesses the sensitivity of deposit levels to deposit interest rates.

"This model estimates that a 100 basis point increase in the six-month term deposit rate increases the level of household deposits by [between] 1% to 1.5% ($1.5 billion to $2.4 billion) after four to six quarters, after controlling for economic and financial conditions. It also shows that the overall level of retail deposits, which includes household and business deposits, increases by less in dollar terms than household deposits in response to an increase in the deposit rate," the Reserve Bank says.

"This suggests that higher deposit rates could cause funds to transfer from business deposits to household deposit accounts. Overall, the analysis suggests that household deposits are likely to be sensitive to interest rates, and banks may be able to attract some additional household deposits by increasing deposit rates. However, total retail deposits are relatively insensitive to deposit rates."

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

15 Comments

Who knew !

not holding my breath on banks increasing deposit rates to any great degree, they treat depositors quite badly compared to borrowers

Yes they do and I can't imaging banks going off shore "cap in hand" - for goodness sake, these are multi billion dollar money making machines. They go like Arney - "To hell with you"

so take your money elsewhere.

There is no money to take beyond the circulating note and coin float amounting to ~$5.3 billion out of ~$410.00 billion of banks' assets offset by digital bank ledger deposits, which cannot be retrieved. Just for reference the latest RBNZ S10 banks: balance sheet data records total note and coin assets at $735 million.

Much like the Eurodollar market.

“But the eurodollar market was also unique in that it relied heavily on interbank transfers for liquidity flow. As an interbank market, each individual participant would be free from the encumbrance of maintaining a large stock of liquid currency because the liability counterparties operating here were also banks that disfavored currency. Unlike banking regimes that were traditionally funded on deposits of real persons, this interbank market had little need for currency since each of the interbank counterparties were better served with just changes to accounts. That ultimately meant that transfers inside the eurodollar market were nothing more than bookkeeper entries on balance sheet ledgers rather than the actual transference of physical currency (let alone gold). It also meant that these ‘dollars’ were themselves intangible bookkeeping entries far removed from anything resembling legal tender.” Read more

thats what many of us have done that is why they now struggle to get local deposits, go fiqure did they not factor that in

It seemed nutty for banks to be covering local lending with foreign borrowing so I went looking for the haircut that applies. If I got that right (RBNZ Liquidity Policy Annex) the haircut is just 5% for foreign currency on top of whatever other haircuts apply. For monthly average USD/NZD rates between Apr-08 and Mar-09, the low was .52 and the high .79 - a bit more than 5% variation. Yes, I know I picked a stressful period there, but isn't that the point?

Thank-you RBNZ for this lovely little article on your modelling behaviour......I find it refreshing when you take your clothes off and expose what I always thought was your underlying problem......mind you a nice wee 3 day break on the Queen and most people will have forgotten how shrunk up that body part is!!

New Zealand’s banking system relies on funding from international wholesale markets due to low domestic savings in the economy.

Exactly. From Mar 16 to Mar 17 Figure 1.2 (page 3 (5 of 58) records Annual change in the stock of market funding - the fsr-May17-data package details those cumulative values at plus $119.0 billion for foreign funding versus $0.3 billion for domestic alternatives.

There wasn't much collective bank effort expended to defray foreign borrowing risk with alternate funding sources.

this article only talks about attracting new term deposits. One factor not considered at all in this article is that for people who are or will be rolling off 4 or 5 yr term deposits in the near future, the current rates are very low. So the question is: with the rates being so pathetic, what do I do? To reinvest it now with these low rates/ OBR being introduced without my approval/ a newly introduced one month notice break period/ Kiwibank NZ post guarantee gone/ rising concern about the banks prudence..... I am reluctant....

Yes got 10 months to go on a pretty big sum currently getting 4.6% return that has carried me through record low return rates for investors. It will be interesting to see how things are positioned when it comes out, hopefully better than the present situation or I wouldn't know what to do with it.

Rising interest rates for depositors is fake news

Probably not, the longer term rates have already risen but they are still 0.5% below my current investment. Will not take much of a rise to get where it was. The longer term rates will rise further and it will filter down to the shorter term rates. Hoping to get 4.6% for 1 to 2 year terms or better.

so am I, but ASB just dropped their rates and 4.15 is the best for 2 years, BNZ no better, was 4.2; so I rolled it over@3.55 for 6 months, hoping for that 4.5...next time; but it probably won't happen.

Rising interest rates for mortgages is also fake news.

The global trend is still zero real growth, resistance to re-flation, and at best flatlining interest rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.