By Andrew Coleman*

The value of New Zealand real-estate and household wealth

There is no single best way to compare the value of the residential property sector with the value of other assets. There are several measures that are relevant to a discussion of the role of tax in the economy.

7. The separate value of debt and equity claims on owner-occupied and residential property, for the tax treatment of each of these claims is different.

8. The total value residential property relative to the net-of-borrowing value of all business and housing assets owned by households, as this indicates the relative importance of the housing assets in the nation’s private sector wealth.

9. The total value residential property relative to the value of all private sector business and housing assets in the country, as this indicates the relative importance of the housing assets relative to all of the assets in the country.

The first two sets of measures are relatively straightforward to calculate in New Zealand using data on the household balance sheet compiled by Statistics New Zealand and the Reserve Bank of New Zealand. The last set of measures are more difficult to calculate as different conventions on the treatment of debt claims on business can be adopted when calculating the size of the business sector. Internationally, it is common to compare the value of housing with the value of net household wealth, and these calculations are reported here, but other methods are possible. However, making international comparisons is fraught with difficulty as some of the data are compiled differently in different countries.

The data necessary to calculate the size of the residential property sector relative to net household wealth are available up to December 2017. The data necessary to compare the residential property sector with all private sector assets are only available up to March 2016. The following tables include data for both 2016 and 2017, plus earlier years to provide a comparison. In all but one case the tables are expressed in current dollar terms and not adjusted for inflation.

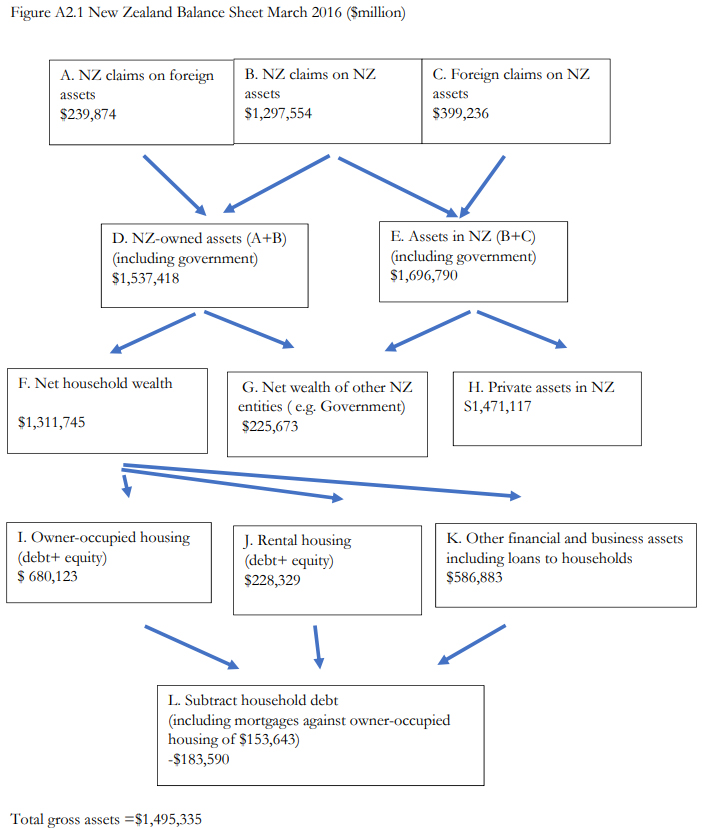

Figure A.1 outlines the basic calculations, using data from the Annual Balance Sheet compiled by Statistics New Zealand for March 2016, supplemented by data provided by the Reserve Bank of New Zealand. (The raw data are in Table A2.2) Three issues should be noted. First, the value of assets owned by New Zealand residents is significantly less than the value of assets located in New Zealand. For this reason the value of housing is a larger fraction of the value of household wealth than a fraction of the value of assets located in New Zealand. Secondly, the loan and debt statistics do not always record the sectors on which the claims are owing. This means it is necessary to add up the value of assets including the value of loans held by households and then subtract the value of debt owed by households rather than separately add up the total of debt and equity claims on different sectors. Thirdly, the value of business assets is based on Statistics New Zealand’s estimates of the value of the non-financial assets owned by business. It excludes the value of financial assets to avoid the way that financial intermediation inflates the value of the underlying assets in the economy.36

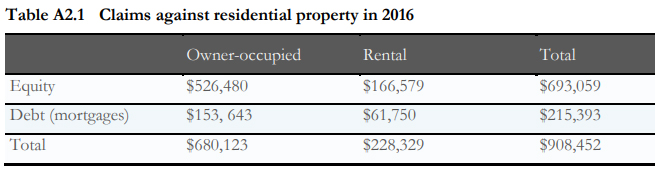

In 2016, the total value of non-financial assets in New Zealand, whether owned by New Zealand private entities, the government, or foreign entities was $1,697 billion (Box E). The value of assets owned by New Zealand entities including the Government was $1,537 billion (Box D). The value of private assets held in New Zealand was $1,471,111 (Box H), and the value of net household wealth was $1,311 billion (Box F). The total value of housing assets including both owner-occupied and rental housing was $908 billion (boxes I and J). Consequently, the value of housing assets in New Zealand was 69% of net household wealth, 62% of private assets located in New Zealand including those owned by foreign entities, and 53% of the value of all assets in New Zealand.

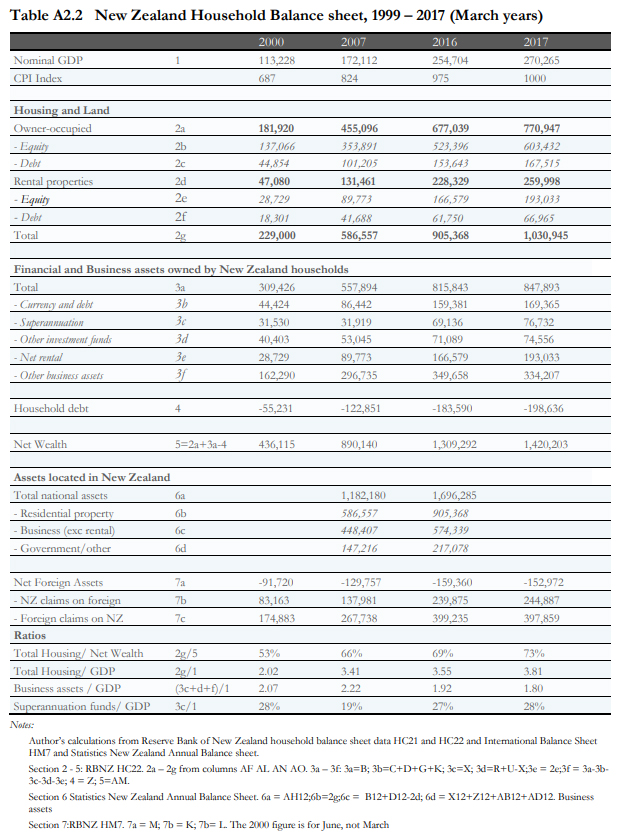

Table A2.2 provides a snapshot of New Zealand’s household balance sheets for March 2000, 2007, 2016, and 2017. All data are in contemporary nominal prices, $millions. The data show that between 2000 and 2017 the value of residential housing had increased from 53 percent of net household wealth to 73 percent, with most of the increase occurring between 2000 and 2007. Using a different metric, between 2000 and 2017 the value of housing increased from 2.0 times GDP to 3.8 times GDP. During the same time the value of business assets actually decreased as a fraction of GDP, from 2.07 to 1.90.

The value of assets held in superannuation funds increased decreased from 28 percent of GDP in 1999 to 19 percent of GDP in 2007, before steadily increasing back to 28 percent of GDP in 2017 after KiwiSaver was introduced. The value of other investment funds slowly decreased throughout the period from 36 percent of GDP to 28 percent of GDP. These funds – and the value of business assets in general – are now dwarfed by the value of housing in the economy.

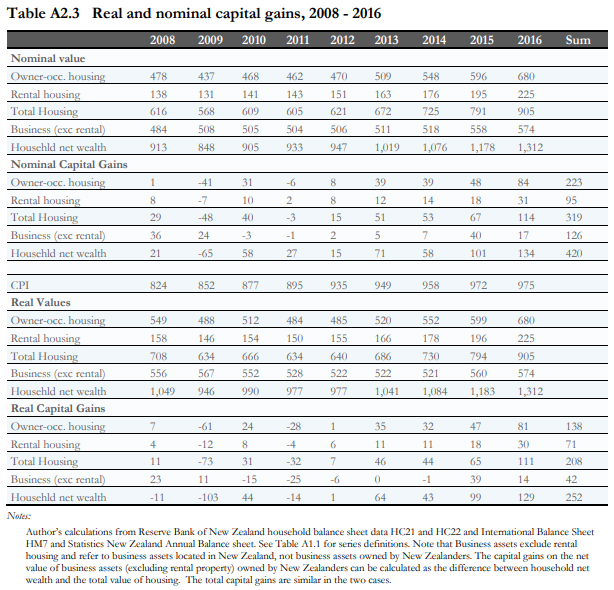

Table A2.3 indicates the size of the change in the nominal and real value of assets in the economy between 2007 and 2016. These are a proxy for nominal and real capital gains - they are not an exact measure, as part of the change in the value of assets reflects new investment.37 Between 2007 and 2016 net household wealth increased by $420 billion, of which $319 billion was associated with the increase in the value of real estate. In inflation adjusted 2016 dollar terms, the increase was $252 billion, of which $208 billion was associated with real estate assets. Real capital gains associated with other business assets were $42 billion. The capital gains from 2000 to 2007 were even larger: in 2016 dollar terms, the value of real estate increased by $368 billion, and net household wealth increased by $434 billion.

The large real capital gains experienced between 2000 and 2017 are probably not representative of the capital gains that can be expected in the future. The prices of many assets increase when interest rates fall, and this period was one when international interest rates declined to the lowest levels seen in a century. While asset prices increased in real terms in most OECD countries during the last century, real asset price increases of this magnitude are rare historically (Dimson et al 2013).

Non-residential capital stock data

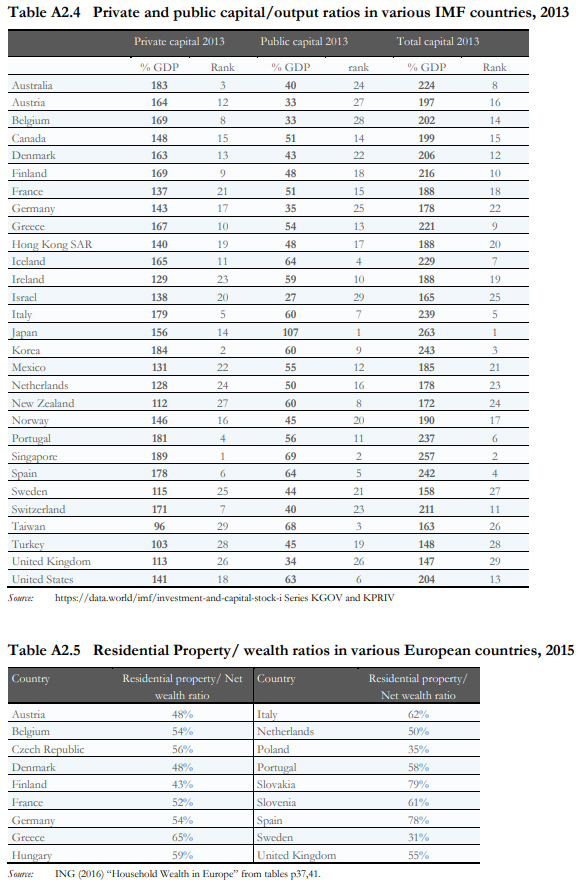

An alternative approach to measuring the relative size of New Zealand’s capital stock is to compare the size of the private and public capital stocks with other countries. Table A2.4 shows the size of the private non-residential and the public capital stocks as a fraction of GDP for 29 high income countries in 2013, using IMF data.38 In 2013, New Zealand’s private capital stock was 112 percent of GDP, 37 percent lower than average and the third lowest of the countries in the table. In contrast, New Zealand’s public capital stock was estimated at 60 percent of GDP, 8 percent higher than average and the 8th highest in the table.

International comparisons of housing wealth

It is not straightforward to make a comparison with other countries as other countries present their household balance sheets differently. However, it appears that New Zealand has a relatively large fraction of its wealth held in housing assets – and a low fraction held as other assets. The following comparisons are with Australia, the United Kingdom, and various European countries.

Australia

In March 2017, residential land and housing was valued at $A6312 billion, or 64 percent of household wealth, compared to 73% in New Zealand. In 1999 and 2007, the ratios were 57% and 62%.39 The value of housing was 3.65 times GDP, compared to a ratio of 3.81 in New Zealand. The ratio of non-housing assets to GDP was 2.04, compared to 1.44 in New Zealand.

United Kingdom

In the year ending December 2016, the value of UK residential buildings owned by households was £1,521 billion, with an additional £3,866 billion in land. Non-financial corporations owned an additional £227 b worth of dwellings. If the land associated with these dwellings was valued in the same ratio as household land, the associated land value would be £576b. (Households plus non-financial corporations account for 98% of dwellings.) The total value of residential property can therefore be estimated at £6296b. This is 63 percent of the value of household net worth.40 The ratio of directly held household property wealth/total wealth is 54%

Other countries

The quality of published data for other countries is uncertain. The OECD has published some cross-country tables calculating household wealth, but retirement savings are included in the tables in an inconsistent manner which devalues their approach. It was not possible to reconcile the OECD tables with the national data for Australia and the United Kingdom, for example: in the latter case non-housing assets worth close to 25 percent of household wealth were excluded from the calculation.

In their publication “Household Wealth in Europe,” ING (2016) compiled data on household property wealth and household wealth for various European countries in 2015 (see Table A2.5). Most countries had ratios between 50 and 65 percent, and the Eurozone average was 59%. Spain and Slovakia were the two exceptions with ratios in excess of 75%. Their calculation methods are unknown, although their ratio for the United Kingdom is consistent with the data in the U.K. national accounts.

New Zealand and international property price increases

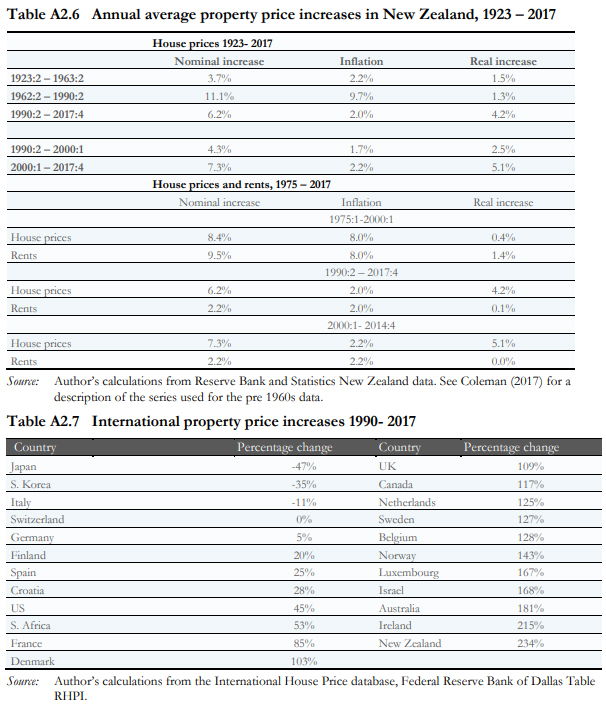

Table A2.6 presents information on average house prices and rents for New Zealand from 1923- 2017 from a variety of Statistics New Zealand and Reserve Bank of New Zealand sources. From 1923 – 1990, average real house price increases were 1.4% per year. Since 1990, the average increase in real house prices has been 4.2 % per year, with most of the increase taking place since 2000. In contrast, average rents have scarcely changed since 1990.

The Federal Reserve Bank of Dallas compiles property price data for 23 rich countries. Their database, the International House Price database, has data back to 1975. Table A2.7 shows house price increases between March 1990 and 2017. According to their methodology, New Zealand house prices increased by 234 percent in real terms over the period, the largest increase of any of the countries in the table.41

The 1990 start date is chosen so the change in New Zealand property prices could be compared with the change in world property prices since the 1989 tax reforms. It should be stressed that New Zealand property prices were near a cyclical low in 1990. Over the whole period 1975 – 2017 New Zealand house price increases were not as high as those in several other countries. Indeed, New Zealand had the third smallest property price increase between 1975 and 1990, in part because New Zealand house prices experienced a cyclical peak in 1975.

Notes:

36. For example, if a business has assets worth $100m and borrows $40 million directly from households, the assets of the economy are the $100m business asset and the liabilities are a $40 debt claim and a $60m equity claim held by households. If the households deposit the money in a bank, which lends to the firm, gross business assets in the economy are the $100m business asset plus the $40m loan held on the bank’s books, and gross liabilities are the $60m equity claim held on the business plus the $40 million debt claim on the business held by the bank plus the $40m million claim on the bank held by the household. On most occasions it is useful to net out the debt claims associated with financial intermediation to calculate the underlying asset position.

37. The total value of new residential construction between 2007 and 2016 was $60 billion, excluding the value of newly developed land. Approximately half of this construction is estimated to replace existing building. The total increase in the real value of housing over the period was $208 billion. This suggests capital gains accounted for over 70 percent of the increase in the value of new construction.

38. The data is sourced from the website https://data.world/imf/investment-and-capital-stock-i Series KGOV and KPRIV.

39. Data from Australia Bureau of Statistics Table 5232.0 Australian National Accounts Table 34 Household Balance sheet, Current prices. Series A83728305F (housing value) A83722648X (net worth).

40. Data from the Office of National Statistics, The UK National Balance Sheet, Table C

41 This increase is slightly higher than the increase calculated using Statistics New Zealand and Reserve Bank data. New Zealand would still have either the highest or second highest increase in the table if the New Zealand data were used. The International House Price Database is used to ensure consistency with the way the data are compared across countries.

* Andrew Coleman is a senior lecturer in the economics department at the University of Otago. He's also principal advisor & economics lecturer at Treasury.

7 Comments

We may very well find out this year who gets caught with their pants down because they sit on assets inflated not by production, but by artifice.

Or we just see massive inflation, as per the normal

Indeed. All hype & not much substance on paper.

However, NZ Inc is still a sort after place to live, as witnessed by the hoards in the immigration queues at Auckland Airport most days. This is premeditated by both sides - ours & theirs. Our laws & attitudes are perceived as being quite weak (internationally) and therefore we are an initial target to get in on 'the best of the west' before moving on to bigger & brighter things. Having spent some time in Asia, if I were them, I'd be trying my hardest to get here as well.

Sought, hordes, ...:-)

Look at all those $ worth of assets we can tax now!

Kiwis have been screwed over for the last 20 years. Hordes from the third world have arrived and kiwis now have the highest homeless rates in the OECD. These homeless people are exclusively Polynesian and European. In 1992 the population was 3.3M and 25 years later its tipping 5M. In 25 years 1 new university has opened to accommodate the population swell and the skills shortage; not training people has meant that the local heart surgeon is an immigrant now trained in Bangladesh or Calcutta. Reductions in funding for kiwi students means tertiary institutes run at a loss if they train kiwi students but run at a profit if they train international students (who are on a ticket to residency status) and therefore some of the more enterprising institutes have realised that its easier to tell kiwis to P off so they can run a profit on the internationals. If your a kiwi student and your marginal you will fail but if your an international you will pass because the bottom line is profits keep institutes going, and the funding deficit for kiwi students will exist so long as a fee cap exists for domestic students.

Excellent article, so we are going to tax inflation? Nice business model

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.