Here's our summary of key economic events over the weekend that affect New Zealand, with news questions are deepening about the Chinese economy, and how it will extract itself from the on-going funk - or whether it can.

But first, we are now in the heart of the northern hemisphere annual vacation season. Anything happening now is reactive to the general inactivity among investors, company managers, and regulators.

The week ahead will be somewhat light for key data releases, probably the most important one being US factory orders for July. And at the end of the week, the Powell speech at the central banker shindig at Jackson Hole, WO, will be closely watched. Locally, July retail sales levels will feature (via the electronic cards version), and in Australia there is little of substance on the agenda.

In China, they released foreign direct investment data and that remained modest in July with the main inflows coming from 'friends'. Western companies are now moving to the exits. And their central bank moves to keep the yuan value elevated for wider stability reasons means those leaving now are not getting hurt by the exchange rate

Meanwhile, China's Evergrande Group, once the country's second-largest property developer (Country Garden is now the largest), filed for bankruptcy in New York on Friday (NZT). It was a Chapter 15 bankruptcy filing meaning its actually a Chinese (Hong Kong) bankruptcy, a move that protects its US assets from creditors while it works on a restructuring deal elsewhere. Rival Country Garden is going down the same 'restructuring' path. In fact, Country Garden is to be cut from the Hong Kong Hang Seng index now.

And it is not only property developers reporting huge and widening losses. Chinese carmakers are too. Cutbacks are widespread among companies and across all demographics. Anxiety levels are rising.

Over the weekend it was reported that at least five local governments will be allowed to sell ¥1½ tln (NZ$350 bln) in bonds - to repay earlier debt from local shadow financing.

Later today, China will review its prime loan interest rates. No-one seems to be sure whether they will cut them or not, but a cut seems likely. More analysts are asking whether China's 40-year development boom is over - and what that means for investors. Ratings agency Fitch is nervous. They have had China's sovereign rating at A+ (Stable) for more than 15 year, but is now signaling that conditions are changing to the downside as they see it. The Fitch downgrade of the US sovereign rating (to AA+ earlier this month from AAA) has triggered a widespread reassessment of international yields. A China downgrade won't be seen positively either. (S&P is also at A+ Stable for China, and Moody's is at A1 Stable. Both have been at these levels for six years. For comparison, both S&P and Fitch have New Zealand at AA+, Moody's at Aaa.)

In Japan, CPI inflation rate was unchanged at +3.3% in July but this was notably higher than market expectations of +2.5%. Core inflation stayed above 3% too. Prices continued to rise for food which was up +8.8% in July from a year ago, compared with +8.4% in June. The latest figures are well above the Bank of Japan's 2% target, and for the 16th consecutive month.

In Canada, producer prices rose +0.4% in July from June, a big shift from the -0.6% decline in the previous month. This was their first rise of producer prices since October 2022. Year-on-year Canadian PPI is down -2.7%.

In Australia, their pipeline of investment projects has climbed to a new record high in 2023. The value of projects in the investment pipeline was worth AU$946 bln in the June quarter 2023, a +AU$180 bln (+22%) increase on the level prior to the pandemic.

The UST 10yr yield will start today at 4.25%, unchanged from Saturday but +9 bps higher than week-ago levels. Their key 2-10 yield curve inversion is still at -69 bps. Their 1-5 curve is unchanged at -97 bps. Their 3 mth-10yr curve is still at -113 bps. The Australian 10 year bond yield is now at 4.23% and unchanged from Saturday. The China 10 year bond rate is holding at 2.58% and its lowest since the temporary drop at the start of the pandemic in early 2020. Apart from that it is a 20 year low. And the NZ Government 10 year bond rate is down -1 bp, now at 5.08%. A week ago it was 4.90%.

The price of gold will start today at US$1890/oz and little-changed from Saturday. But it is down -US$12 from a week ago.

And oil prices are holding at just over US$80.50/bbl in the US. The international Brent price is now just over US$84.50/bbl. These levels are a net -US$2 lower than week ago levels.

The Kiwi dollar starts today slightly softish at just on 59.2 USc. Against the Aussie we are little-changed at 92.6 AUc. Against the euro we are marginally softer at 54.5 euro cents. That all means the TWI-5 is at 68.4 and down a mere -10 bps from Saturday and the same over the past week.

The bitcoin price is a little lower again today and now at US$26,127 and down -0.5% from Saturday. But for the week it is down more than -10%. Volatility over the past 24 hours has been very low at just on +/- 0.4%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

38 Comments

Pure supposition here but did President Trump introduce a let’s say correction to the balance of global trade with concern to China, that has been sustained to a point that has realised outcomes such as above. At the time it appeared what was being questioned was whether the USA needed the world as much as the world needed the USA. And then of course along came Covid, grist to the mill.

Bit of a mixed bag coming out of Australia. They have much the same construction cost issues as us and massive exposure to China but the never seem to get the wobbles.

Will this time be different for Australia? Last recession for them was 1991!

Even with recession I see Australia as being in a better position long term given their natural resources and mining sectors (vs NZ with the anti farming, anti mining attitude). If there is future growth then it’s reasonably safe to assume that Australia will benefit. I think long term NZ will continue to fall behind, and become poorer and poorer. Dumbing down of education will also play its part.

"If there is future growth"

Quote of the century.

Knock on is a question: Behind what?

In existential terms (and there are no other in the long term, as Keynes pointed out) New Zealand is far and away the easier place to live. Not many blot-hole-seekers in Alice...

I was discussing with a friend yesterday that the serious financial concerns occurring in China may affect NZ property in two contrasting ways:

- Either a Chinese recession would involve enormous amounts of capital flowing from countries all around the world (including NZ resulting in lower property prices) to pay off debts in the mainland or,

- Enormous amounts of capital leaving China to be squirrelled away overseas (including NZ resulting in higher property prices) to prevent the CCP from seizing assets.

Does anyone have any insights on this? Our discussion was inconclusive, we don’t know enough on the issue.

All the growing economies are making it hard for money to be taken out from the country.

So it will be interesting to see how this pans out.

NZ real estate is highly reliant on money coming in from over seas. Once the sentiment is taken away, the drop in values will be sharp and long.

God save NZ.

Not just RE - think dairy and associated activities.

Add a Nat/Ac Govt and a blow torch will be applied to option 2.

Puts some context to Lux's "foriegn buyer" brain fart.

Eludelux.

foreign reserves cannot be used to shore up your domestic issues. the very fact there is large chinese reserves offshore is systematic of domestic excess liquidity that had to be absorbed by large trade surpluses. it is not too different to japan after their asset bubble in that their offshore asset holdings had no bearing on the domestic debt issues and the subsequent zombie companies that emerged. the offshore reserves are only good for future imports, and any domestic debts will have to be settled either by more domestic govt borrowings or other forms of taxes (again look at japan and govt debt - the other option would have been to tax or inflate away the debt, i.e. taking it off private hands)

it is a common fallacy that large offshore reserves can shore up domestic debt. it cannot.

I’ve been wondering the same! Maybe it depends how many Chinese who have bought property here also own overpriced property on the Mainland… I doubt anyone has bothered collecting figures on that.

It won't be long before Fitch and Co will downgrade New Zealands credit rating.

It does have that feel to it, I expect that the big four aussie banks may well see downgrades as well, its par for the course as the economy rolls over and provisions get used then increased. One wonders what the Sept Financial Position is going to uncover, we keep hearing of holes in several departments.

The big four Aussie banks are all controlled by the usual US and Euro suspects. They also pay big money to the rating agencies every year. They do not pay them to give the wrong answers.

I was wondering why the tax take has gone down so much. Inflation should have significantly increased PAYE revenue due to bracket creep, and GST revenue due to increased prices. Maybe company tax has dropped a bit, although we still have reasonable annual GDP growth at the moment. The government books should be in great shape shouldn't they?

Without getting any numbers, isn't gdp figures like at least quarter old? We prob were still held up by property, dairy and forestry in the first quarter but all those have dropped a lot now. But the tax take is a prediction for the year, so if things stay as they are now then that prediction probably allows for a declining 2nd quarter and low 3rd and 4th.

Tax is only applied on business profit - not revenue, so unlike wages for individuals- a business can earn absolutely nothing - or worse make losses. These losses mean they can claim provisional tax (already paid) back from IRD and apply last years losses to cancel out this years profit (if there was one).

The scale of the tax issue probably underscores the depths of trouble that businesses are in - because inflated input costs have burned their margin. All that is left for IRD is tax on wages ….. wait till unemployment starts to creep up and that hole will only get bigger …

If the news we are allowed to see out of China is bad then the real situation will be 10x worse. Don't forget they have blocked release of youth unemployment data.

Time to keep those youths busy with a war.

Their mates can't even beat Ukraine, it would seem like a crazy move, not that that has ever stopped anyone...

Wow that's a bit of a simplistic answer. The Russians are not fighting the Ukrainians, they are fighting the rest of the world. If the USA had not stepped in with support it would have been all over in a couple of months. The Russians are just running a war of attrition now, the Ukrainians are literally going to run out of men to fight it. Its just a question of them running out of manpower or the 2024 USA election going the wrong way and the Americans will pull their support. Sooner or later the rest of the world is going to get sick of pouring money into Ukraine regardless, its like Yemen, years later it just disappeared from the news.

Did you used to be Carlos?

Sorry to hear this Mr Boris Zwifter.

I see that the humble sausage shop you are minding for the Wagner Boss in St Petersburg, is not doing well, coupled with your plummeting Ruble and lack of flush toilets......and being justifiably bereft of international guests??

Dont worry, you and your people WONT be forgiven for rapes and child butchering, until around 2063.

Anyway back to Interest topics and not Swifter's failing Ruski Butchery (apt as!!)

- Ukraine will become a military behemoth in coming years. They are smart and engineeringly able/minded people.

They also have the flush toilet advantage over the Russians, the Russians hated this wonderful new invention, booming in their previously compliant satellite state the most!

Look what tragedies, the evils of jealously can bring......

UKR Miliary industrials and clean energy/nuclear power will be big there and investible, as soon as the R-Orcswipes are swept into the Dustin of history.

Breakfast briefing: Worries about China's economy grow

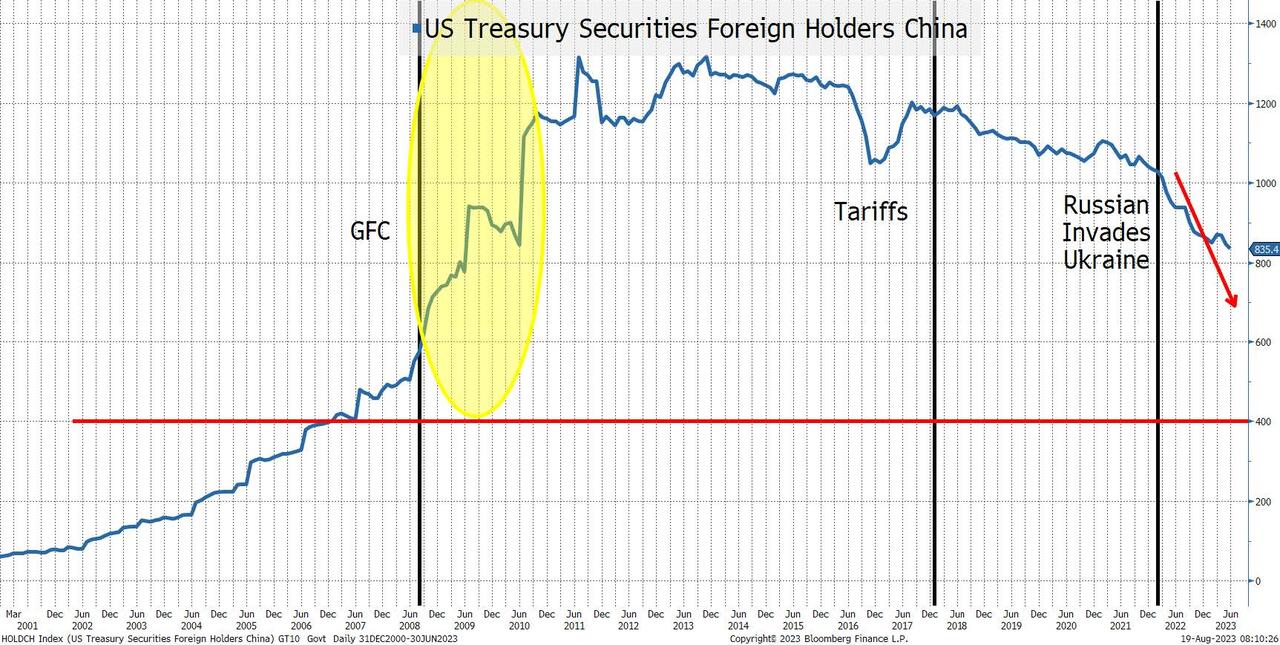

China won't be financing the US or NZ's trade deficits for much longer.

{kind=link}

BERLIN, Aug 16 (Reuters) - The German government has retreated from a plan to legally commit itself to meeting NATO's 2% military spending target on an annual basis, a government source told Reuters on Wednesday. Link

(Re)consider Hong Kong. Seriously. It's replacing Switzerland for offshore banking since the US took over there. It handles all global central bank digital currency payments – including the PRC's – through mBridge, which it developed. It's part of the Greater Bay Area, the world's leading science and technology hub whose GDP will hit $2.8 trillion in 2027. Best of all? The US can't get at your money. Needn't even know it's there. Earning 3%-4% after tax and inflation... @GodfreeTrh https://open.substack.com/pub/herecomesc Link

Brilliant. Put our money in China to stop the US getting it!

Banks have to continue selling securities to raise enough liquidity just to repay small amount of previous emergency borrowings (in the aggregate). In this environment, not in any position to lend so they aren't. Credit crunch still going after five months. Nothing has changed. Link

"India Poised to Secure Unprecedented Deal: Potential Purchase of 9 Million Tons of Russian Wheat at Reduced Rates" Link

What? Now your sources are random Russian propagandists on twitter?

You're better than this Audaxes.

Possibly we could all wait and see what unfolds. It could easily be true. Russian wheat production has leapt up since the Marxists stopped telling the farmers which day to plant and harvest it.

Just checked. It is on Reuters and MSN as well. So it is obviously a pack of lies.

I don’t doubt it’s true - but it takes a propagandist to frame it as ‘trade victory for Russia!!’ rather than ‘Russia forced to sell wheat at a discount’.

adx has sources & sauces. The latter are often, highly seasoned.

Informative read but I don't feel it really addresses the major issues of 'where it the money coming from' for the boomers' last hurrah.

Super’s Baby Boomer tipping point has arrived

The financial system has been moulded by the post-WWII generation. As the silver tsunami of retirements is upon us, we should expect it to be entirely reshaped.

https://www.afr.com/companies/financial-services/super-s-baby-boomer-ti…

Good article - aligns with Dalios Changing World Order and The 4th Turning theory.

China was a massive beneficiary of loose economic policy around the world. Now those free dollars are finding their way back to higher cash returns at lower risk. You can't base a sustainable income model on property development and speculation, ask the bankrupt from booms past. New Zealand is a local franchise office of Evergande et al.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.