Here's our summary of key economic events overnight that affect New Zealand, with news a sense of dread you might get looking at financial markets from the outside isn't being reflected in the activity of those markets.

But first the worrying news. We should note that American benchmark mortgage interest rates topped 7.5% last week for the first time since November 2000. 8% rates seem in sight. So it will be no surprise to learn that mortgage applications were weak there last week, down a sharp -6% from the prior week, and down -22% from the same week a year ago.

Holding that weaker theme, and after rising +180,000 in August, the pre-cursor ADP Employment Report of private payrolls was expected to rise +153,000 in September. But it rose just +89,000 which is a negative signal ahead of Saturday's US non-farm payrolls report. Weakness was shown in factory jobs, employment in the South, and by large firms. Analysts are expected the non-farm, payrolls to grow a modest +170,000 but there seems to be downside risks. At least the US Fed will like to see an easing. And equity and bond markets responded in that way with stocks up and benchmark bond yields easing back.

But not every indicator out today is negative. The closely-watch ISM services PMI shows no such weakness for September. Yes it eased slightly, but it is just off its six month high and expanding at a healthy clip. Employment held up, but if there is a weakness it is a sag in the new order expansion levels.

Having noted that, the new factory order data in the US for August came in much better than expected and reversing the slip in July. They were up +1.2% from the prior month, although only up +0.5% from a year ago.

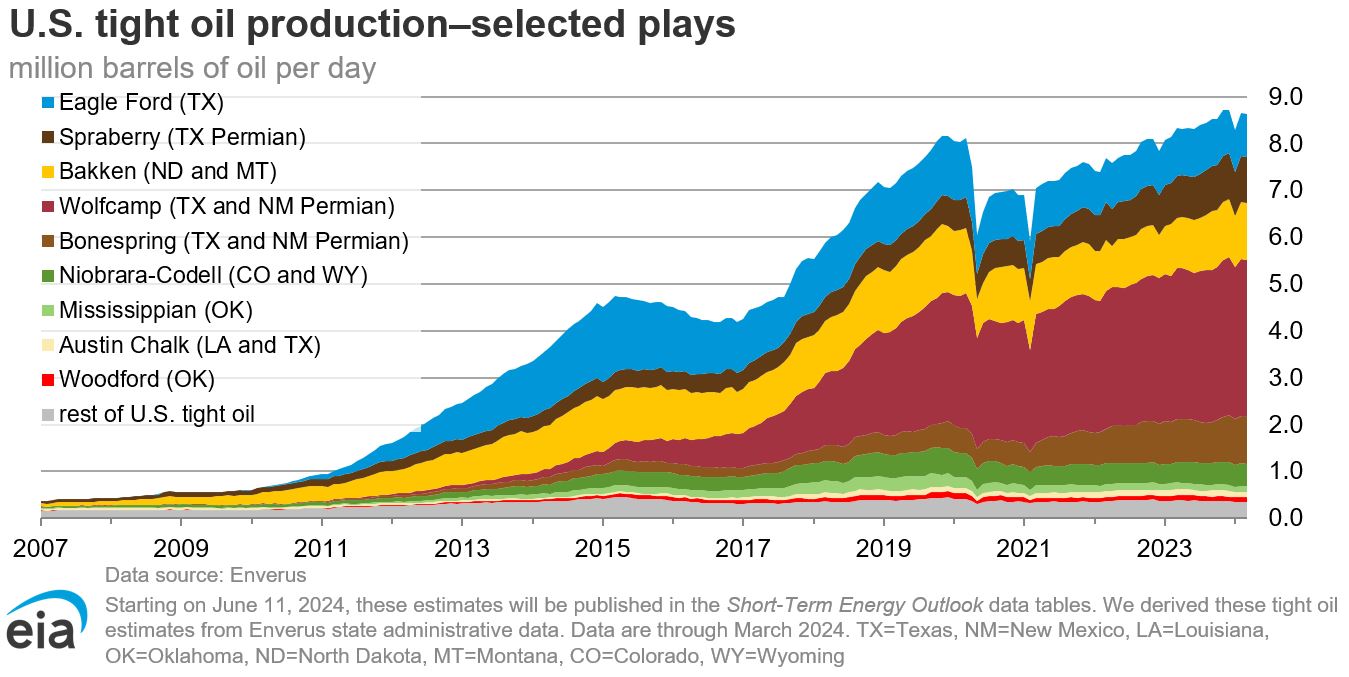

American crude oil stocks fell again last week, but petrol inventories jumped sharply. This surge has seen crude oil prices fall rather sharply today. The Saudi-Russian 1 mln bbl/day supply cut isn't having the impact they had hoped.

And apart from oil, some other commodity prices are sharply lower today, notably for coal, and for wheat. All up, inflation relief.

In Japan, the Markit services PMI was revised higher to 53.8 in September from 53.3 in the flash estimates, a 13th consecutive month of good expansion in their service sector. In South Korea, their latest factory PMI improved nicely as well, almost taking them out of contraction. It was an improvement that wasn't expected. Despite deep-seated cultural rivalry, it helps Korea that Japan is doing much better these days.

In China however, office vacancy rates are now higher than they were under the country's severe zero-COVID restrictions, delivering a further blow to the nation's struggling property sector. They now top 27% in tech hub Shenzhen, 21% in Guangzhou, and a still-high 18% in Beijing. It was running 16% in Shanghai. New projects will be a very tough sell when vacancy rates are so high.

Global passenger air travel is still recovering fast and is back to 96% of 2019 pre-pandemic levels. But the gains are uneven, dominated by radical changes in the nature of Chinese air travel, huge jumps in domestic travel there, and offset by very large falls in their international travel. The Chinese have become stay-at-homers. Asia/Pacific travel has a very long way to go yet to return to pre-pandemic levels.

The UST 10yr yield starts today down -7 bps from yesterday at 4.74% as a correction sets in. Their key 2-10 yield curve is again less inverted from yesterday at -33 bps. Their 1-5 curve is now at -71 bps and unchanged. Their 3 mth-10yr curve inversion is more inverted today at -66 bps. The Australian 10 year bond yield is now at 4.58% and down -5 bps from yesterday. But the China 10 year bond rate is unchanged at 2.71%. The NZ Government 10 year bond rate is up very sharply, up +12 bps at 5.63%.

Wall Street is making a bit of a comeback after yesterday's slump, up +0.2% in Wednesday trade. Overnight European markets closed mixed. Frankfurt and Paris were little-changed, London was down -0.8%. Yesterday, both Hong Kong closed down another -0.8% and Shanghai was still closed for their National Day holidays. But Tokyo suffered a huge -2.3% fall. And the ASX200 ended down another -0.8% in its Wednesday trade. But the NZX50 was luck to end little-changed and still escaping the carnage so far.

We follow the Fear & Greed Index weekly, but we should perhaps note that it has jerked suddenly in the 'extreme fear' mode yesterday and today.

The price of gold will start today at just on US$1820/oz and down another -US$4 from yesterday. This is another new low since February 2023.

Oil prices have slumped -US$5 lower at just on US$84/bbl in the US. The international Brent price is just on US$86.50/bbl.

The Kiwi dollar starts today at 59.2 USc and up +20 bps from yesterday. Against the Aussie we are softish however, now at 93.5 AUc and down -20 bps. Against the euro we have slipped marginally to 56.3 euro cents. That all means our TWI-5 starts today at just over 69.4 and down -10 bps.

The bitcoin price has moved marginally higher today from yesterday, and it is now at US$27,524 and up a minor +0.4% from yesterday. Volatility over the past 24 hours has been low at just on +/-0.8%.

Daily exchange rates

Select chart tabs

The easiest place to stay up with event risk is by following our Economic Calendar here ».

79 Comments

I think all those "higher for longer" zealots are severely underestimating the risk of something big breaking. I think we will be cutting rates again before the middle of 2024

Doesn't supply and demand come into it?

If less people borrow, isn't there more money looking to invest? Or are bonds etc unlimited in demand?

While they might cut, it may only be 100bps in total. IMHO Higher For Longer does not necessarily mean no cuts, it just means we are not going back to where we were. We are not going back to low rates.

What the central banks say is often more relevant than what they do. Since early 2021 they've been making all sorts of noises; don't be spendy, save your money, etc. "Higher for longer" is just another mantra, to detract people from being overly bullish in their spending and pricing practices.

We can't really make any assumptions about the speed and breadth of any future rate drops, because it's impossible to foresee just how serious the next economic crisis might be.

I'm not sure who expects the OCR to go back towards zero and mortgage rates to be below 3% again, but I don't imagine it's many people. I expect mortgage rates to come back down to between 4-6%

At the upper end of your band you could join us HFL zealots. Welcome to the club, mate.

HFL? Not even back to average yet.

Hey, "something breaking before the end of 2023" was my mantra, lol.

Do you repeat it every night as a ritual..

Air China plane?

Yeah moral.. just borrow up large.. rates will be dropping soon.. you're definitely not a hazard..

Chin up mate, you'll be picking up a 3 Beddie in Grey Lynn for cents in the dollar before you know it!

If you can dream it you can do it.

I do love the banter on this site.

That's the spirit

I'm unclear on your point. If rates remain higher for longer then that means more pain (for leveraged). If something big breaks then that means pain, possibly more than if rates remained higher for longer.

Or are you saying that rates will be cut and that will avoid something big breaking too - making all the warnings of higher for longer redundant?

Very sound logic. There will be significant pain whether rates are HFL, or slashed aggressively.

I think it just changes where the pain is spread. Higher for longer affects the over-leveraged, big crash and dropping interest rates affects people who lose their jobs.

Okay thanks, I agree with that, but I still don't get the jab at those saying interest rates higher for longer. It seems to me warnings of either scenario are valid and that is coming from someone who has been surprised the RBNZ has actually raised rates as much as they have (given their track record of finding any and every excuse to lower over the last 20+ years).

Higher for longer would assume inflation is tracking at a similar rate. Therefore, there should be upwards pressure on wages.

Short term pain with higher rates, but wages should pull away quicker from the burden of debt in the medium to long term.

3% pay rises over 10 years reduces a debt burden amount (ignoring principal payments) by 25%. 6% pay rises by 45%.

Wage inflation is being knocked out with immigration. Everywhere I look I see PDK being proved more correct with us not being able to afford to maintain existing infrastructure - people suggesting councils should borrow more rather than raise rates to maintain status quo!

I've been wondering how much longer the can will be kicked down the road for (debt increased). It's already been a lot longer than I'd have guessed, but then I was surprised at the compliance with lockdowns (having heard them doing it in China and saying that would never happen here).

It seems like the system is jamming in immigration right now (and for the past 20 years) not ready for this.

What has caused the big drop in oil price overnight?

I wonder if given the US indexes look to be the issue, it is related to the speaker of the house being removed and current bumfight over that.

Bumfight?! 🤣

Yep the fight over who's bum gets to sit in that seat.

The temp has already kicked Pelosi out of her office. The Republicans are a scary bunch of fascists at the moment.

Chaos. It is weapon of choice of Trump, and his disciples have wilfully immersed themselves in it.

Yep another January 6th on a National scale, what could be better for the USA ? Time to put all those firearms to good use.

It says they're not aligned - Nuland Kagan stirring for war since whenever (certainly well involved in Ukraine from 2014, probably earlier) vs Gaetz whose move has stalled funding/supplying Ukraine meantime.

Which says the Elite aren't cohesive which says the anti-vaxxers were wrong which says nobody is looking at the real existential issues facing humanity.

" nobody is looking at the real existential issues facing humanity." The political factions amongst the elites are too fragmented, and have been for too long. Self interest has dominated world wide as the politicians have usurped the process in their favour. Even in NZ many out side politics argue for extended terms for politicians, instead of just demanding they get the job done!

330 Million people to choose from and Trump and Biden are the best they can come up with. Really its a sad reflection on democracy and hence democracy is crumbling over there now. The 2024 election is going to be hell on earth if it ends up being Trump vs Biden again.

To be fair, only 8 Republicans were part of the 216 members who voted McCarthy out.

That doesn't absolve them of responsibility for doing everything they have done that led to this, or sat by and did nothing while it went on.

The other 200 odd Republicans should have cut a small side deal with the democrats. A few bombs for Ukraine to drop on Ukraine in return for 8 votes. A handful of Democrats in red leaning seat could have shown their centrist credentials.

There was a young lady who begat, triplets named Mat, Bat and Tat, it was fun in the breeding, but hell in the feeding, when it was found there was no tit for Tat. But here it is certainly tit for tat. The goats think, in terms of the nation’s stability and benefit, it is more of a priority to exact retaliation on the elephants for the impeachment motion on Biden triggered by his son.

not often a typo makes it so much better :)

I think I may now refer to bumfights only.

I hear there are a few every night downtown Auckland.

Hard to say but the oil production cuts are likely the producers pre-empting global economic sad panda times. Expensive to store surplus oil.

Did you read the article?

WTI Tumbles To 1-Month Lows As Gasoline Demand Plunges

BUT, Gasoline demand continues to plunge, breaking well below 2022 seasonal levels on both a weekly and four-week average basis last week.

In fact, that actually puts it at lowest seasonal level since 1997 and nearly 1 million barrels a day below the 5-year average

Sky high pump prices are clearly weighing on demand...

The great age of US oil may be coming to an end with a cultural shift from big engine vehicles to more efficient, newer models.

You have data on that?

https://www.statista.com/topics/1721/us-automotive-industry/#topicOverv…

'as U.S. consumer demand has been shifting to larger vehicles over the past few decades'.

Note the % shift when discussing EVs - % of themselves rather than % of the whole...

But there is a long lead-time, and the US is a nation of SUVs for a long time to come. Diesel shortage is the more interesting question? Without it, no transportation, no economy.

Pepsi will still be delivered Profile.....

DP

Possibly the first time in history (at least that I can recall) that the tradfi fear and greed index is in extreme fear, but the crypto fear and greed index is at neutral (49). One year ago is was mostly reverse, with Crypto Fear and Greed at near record lows (under 10 even)

Global passenger air travel is still recovering fast and is back to 96% of 2019 pre-pandemic levels, dominated by radical changes in the nature of Chinese air travel by very large falls in their international travel

I flew to Europe with Air China via Beijing for the first time, for the simple reason that their prices were thousands cheaper than Emirates or other leading carriers.

And how did it compare?

Not as good, especially food and beverage wise but what I really care about is the lie down flat seats so that I can sleep, and these were fine. I would definitely recommend for the price.

Good on ya. Personally, I wouldn’t go anywhere near Beijing these days.

Well, seeing the Great Wall of China was definitely worthwhile the stop (also the Forbidden City & Tiananmen square)

I find that a flight getting to its destination and landing safely is the number one thing.

Because... so many flights crash in flight...? (sarc)

"The NZ Government 10 year bond rate is up very sharply, up +12 bps at 5.63%."

But 6 month TDs for plebs are only 5.8-5.9% (at the big five banks) or 5.9-6.05% at the likes of Rabo, Heartland, Cooperative.

Hmmmm!

Govt investment as risky as the banks - maybe should be higher :-)

So gazzillons of 30 yr mortgages written in the States for 1-2% range and now rates at 7-8%.

Bank mortgage books must be bleeding money

How long before the next bank crisis then?

Aren't they all packaged up in bundles and sold off to other organizations?

Government-Sponsored Enterprise (GSE): Definition and Examples

The aggregate loans of GSEs in the secondary market make them some of the largest financial institutions in the United States. A collapse of even one GSE could lead to a downward spiral in the markets, which could lead to an economic disaster. Since they have an implicit guarantee from the government that they will not be allowed to fail, GSEs are considered by critics to be stealth recipients of corporate welfare.

In fact, following the 2008 subprime mortgage crisis, Fannie Mae and Freddie Mac received a combined $187 billion worth of federal assistance.9 This large sum was intended to mitigate the negative impact that the wave of defaults was wreaking on the housing market and the national economy. They were also placed into government conservatorship. Both agencies have repaid their respective bailouts since then, though they remain under the control of the Federal Housing Finance Agency.10

GSE mortgage pool prepayment risk (negative convexity) is currently mitigated by rising term interest rates.

A bit above my pay grade - but i my theory correct? i.e is bleeding big times due to 30yr mortgages at the previous super low rates? And is the bleed big enough to cause another bail out?

Yes.

Wait what? The Big Short again? Nah I must be a dunce.

The Saudi-Russian 1 mln bbl/day supply cut isn't having the impact they had hoped.

Saudi and Russia continue to squeeze the US wrt to oil markets: Saudi Arabia and Russia said they will continue with oil supply cuts of more than 1 million barrels a day until at least the end of the year. Saudi and Russia announced their plans in separate official statements but clearly coordinated. Riyadh has slashed crude production by 1m bpd and Moscow by 300k bpd in additional to earlier cuts made with other OPEC+ nations. Link

US shale producers will be loving these cuts thank you very much.

I didn't say anything about increasing production, i said they will be loving the OPEC output cuts. Who wouldn't be happy that your competitors cutting production giving you higher prices, when your costs are also dropping.

But to your point, US shale production appears to be increasing quite steadily, almost back at the pre-covid peak. I wouldn't trust anything published on zerohedge.

https://www.eia.gov/energyexplained/oil-and-petroleum-products/images/u…

{kind=link}

Weakness was shown in factory jobs, employment in the South, and by large firms. Analysts are expected the non-farm, payrolls to grow a modest +170,000 but there seems to be downside risks. At least the US Fed will like to see an easing. And equity and bond markets responded in that way with stocks up and benchmark bond yields easing back.

Something was due to break. Bond market bear steepening forecast such an outcome?

V large decline in Chinese international travel. And stocking up on oil and gold…

Pulling up drawbridge and Luzon rests his revenue plans on the buying RE here?

Common naivety and downright BS

China is preparing for a world divided by war

Hopefully there won’t be busloads of Chinese tour groups in Kyoto when I am there in December. Mass tourism has been having not just an awful impact on the travel experience in Kyoto, but also on the lives of the locals there.

Funny how the Chinese are the problem and not yourself as a tourist? Hopefully you are Japanese and live in Kyoto otherwise quite the comment.

I talked about mass tourism. I’d say Americans if it was Americans. Quite a different beast to individual travel. And actually, yes, my wife’s family are in Kyoto.

It’s always been a very popular place, but it’s the mass tourism over the past 10 years (excluding covid lockdowns) that has really had negative impacts on both the travel experience and life for locals.

A tourist is a tourist in my books..there is no difference. Do your bit and stay home then...that's one less mass tourist.

Lol, completely ignoring the family aspect

LOL..maybe the Chinese are visiting family as well??

You beat me to it. Every tourist is now a mass tourist. I'm sure there's a hundred million reasons why each one is special.

https://explorersweb.com/traffic-jams-on-everest-ethical-or-not/

It’s always been a very popular place, but it’s the mass tourism over the past 10 years (excluding covid lockdowns) that has really had negative impacts on both the travel experience and life for locals.

Tourism has been a boon for the Kansai economy but understand your sentiment about Kyoto. Central Osaka (Shinsaibashi, Namba, etc) has benefitted massively from tourism spend - Chinese being the key driver obviously.

it is a Chinese tourist problem because they have a pack mentality through their tour groups. Much in the same way Europe has a UK bachelor party problem.

I had to tell a bunch of Chinese tourists to shut up in a Japanese restaurant earlier this year because they weren't respecting the etiquette of the place. Many signs around Japan and Korea now just for Chinese tourists and on general mannerisms.

This isn't racism, it's systematic on how a lot of them travel. Talk to Chinese and they will be upfront about it and embarrassed, much like they are about the fuerdai

Mass tourism is the problem ..check out downtown Kuta or British in Spain.. just sounds like you are cherry picking too fit your narrow agenda.

Where I grew up near a major tourist town it was busloads of Japanese tourists in the 80s and 90s with massive cameras dangling around their necks. Now its Chinese with cellphones. Plus ça change...

Highly recommend watching this uk tv show from 1998 about the different cultures (uk, german, us and japanese) while on holiday (filmed secretly with some stooges added for fun)

https://m.youtube.com/watch?v=3BmJni9bBOA

To sum up.

Brits...pissheads who get along and have a laugh at themselves

Americans... a bit whiny and boring

Germans... suspicious and aloof

Japanese... courteous and open but ruthless when it comes to people acting differently

‘Last stand of the Stock Desperados’:

https://www.macrobusiness.com.au/2023/10/last-stand-of-the-stock-desper…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.