Here's our summary of key economic events over the weekend that affect New Zealand, with news the 'final' week of shopping is here for the holiday season and most analysts are focussed on what that reveals about economies worldwide.

Also in the coming week the American data releases are mostly second-tier but there will be special interest in their PCE inflation, durable goods order levels, and a set of housing data. Japan has a big set of releases including from the Bank of Japan, and their inflation rate. Canada and the UK will also release inflation data. But of course everywhere hints about retail sales activity levels will be sought out

But first, China released a wide set of national data over the weekend. In the official data none of their 70 largest cities reported any house price growth based on housing resales. Overall their housing index was said to fall -0.2%, but sales of new units are low and now quite problematic. Sales of used units are showing much larger declines than the index they released, both month-on-month and year-on-year. In fact they are now heading for a multi-year retreat, the first they have had.

Going the other way, China reported that electricity production was up +8.4% in November from the same month in 2022. That supports the better than expected industrial production data they also reported, up +6.6%.

And also gaining were retail sales. Although very little changed from October, the jump from a year ago is an eye-catching +10.1% - at least until you realise the base was very stunted and they were just contemplating easing Covid restrictions. Correcting for that, the year-on-year gain seems to be about +4%.

China is getting ultra-sensitive about talk of economic problems - and their Ministry of State Security is on the case warning officials and commentators about not holding the Party line about the country's "bright future". And in Hong Kong the Party is putting on a show trial for an imprisoned publisher.

Meanwhile, foreign patent holders are finding that Chinese courts side with local companies and will chop royalties agreed in existing deals that they subsequently don't like.

In the US, retail shopping this year is even more focussed on the online sector. Turnover in traditional bricks & mortar stores is expected to just be level in volume terms.

Meanwhile an early look at their PMIs shows services rising while factory activity is contracting. The sharpest increase in new orders since July is pushing their dominant service sector to a quicker expansion, but the reverse is the case for manufacturing where new order levels are retreating.

The NY Fed Empire factory survey sank sharply in December from its unusual rise in November. But the longer term trend is still in place for a gradual move up from its deep negatives at the start of the year.

Meanwhile, overall American industrial production made a minor gain on November from October but is still slightly lower than year ago levels. Manufacturing output (led by business equipment), which accounts for 78% of total production, rose by +0.3% from October, marginally missing market expectations of +0.4%.

Canadian housing starts took an unseemly dive in October as they dropped to just a 213,000 annual pace and far below the expected 257,000 pace, or the 272,000 pace in October. For them, this is a huge and unusual miss probably reflecting the impact higher interest rates have on multi-family housing units.

And in Australia, the extent of bribery and corruption in China's environmental regulatory system is laid bare in the collapse of a public company there.

In India, export levels are neither growing nor retreating significantly. They were up in November marginally from October but down -2.9% from year-ago levels

In the eurozone, the early PMI surveys show activity is falling at an increasing rate in December and that is true for both their factory and services sectors.

Two of the world's largest container shipping groups stopped using the Red Sea and the Suez Canal. Germany's Hapag-Lloyd and Denmark's Maersk both said the dangers are too great at the moment and have instituted temporary halts. They have now been followed by two more European shipping lines, MSC, and CMA-CGM. This will put a giant spoke in global trade as more than 10% of world trade depends on the Suez Canal.

The UST 10yr yield has fallen slightly today as things settle down in the new levels, now at 3.92% and little-changed from Saturday. The key 2-10 yield curve is more inverted, now by -53 bps. And their 1-5 curve inversion is now inverted by -103 bps. And their 3 mth-10yr curve inversion is unchanged at -146 bps. The Australian 10 year bond yield is now at 4.08% and down -1 bp from Saturday. The China 10 year bond rate is holding down at 2.65% and a three month low. And the NZ Government 10 year bond rate unchanged from yesterday at 4.67% but down -31 bps from a week ago.

The price of gold will start today unchanged at just on US$2033/oz and that is up +US$36/oz from a week ago.

Oil prices are marginally firmer from Saturday at just on US$72/bbl in the US. The international Brent price is now at US$77/bbl.

The Kiwi dollar starts today at 62.1 USc and little-changed from Saturday. But it is up more than +1c from a week ago. Against the Aussie we are still at 92.6 AUc. Against the euro we are still at 57 euro cents. That all means our TWI-5 starts today just on 70.4, unchanged too and +20 bps higher than a week ago.

The bitcoin price starts today at US$41,922 and up a mere +US$31 (<0.01%) from this time Saturday. A week ago it was at US$43,699 so a -4.1% drop since then. Volatility over the past 24 hours has been modest at +/- 1.2%.

Please note that we have normal weekday service this week until Thursday when we transition into holiday mode. Then we publish our content at a lesser intensity, more focused on holiday reads, reviews, and catch-ups. The advertising that powers much of our sustainability is already on holiday-mode, so this is when we really appreciate the vital support of readers. If you can support us during this commercially fragile time till the end of January, the team at interest.co.nz will be very appreciative.

Daily exchange rates

Select chart tabs

The easiest place to stay up with event risk is by following our Economic Calendar here ».

22 Comments

Govt taxes y/y increase 10.2%. Economy is cool but govt continued strict tax collections. Tax policy clearly not helping the macro monetary policy. (稅收政策顯然沒有和宏觀貨幣政策一起發力反而對著幹)Link

Interestingly, almost all of the growth comes from VAT. Other taxes from corporate tax, consumption tax, & income tax are down from 2022. On the same time, social security spending increased from 13.7% in 2021 to 15% in 2023 Jan-Nov. It seems Lou Jiwei's projection coming true. Link

This Bloomberg article suggests that analysts are increasingly worried about the trade implications of China's shifting of domestic investment out of the property sector and into manufacturing. Link

The UST 10yr yield has fallen slightly today as things settle down in the new levels, now at 3.92% and little-changed from Saturday

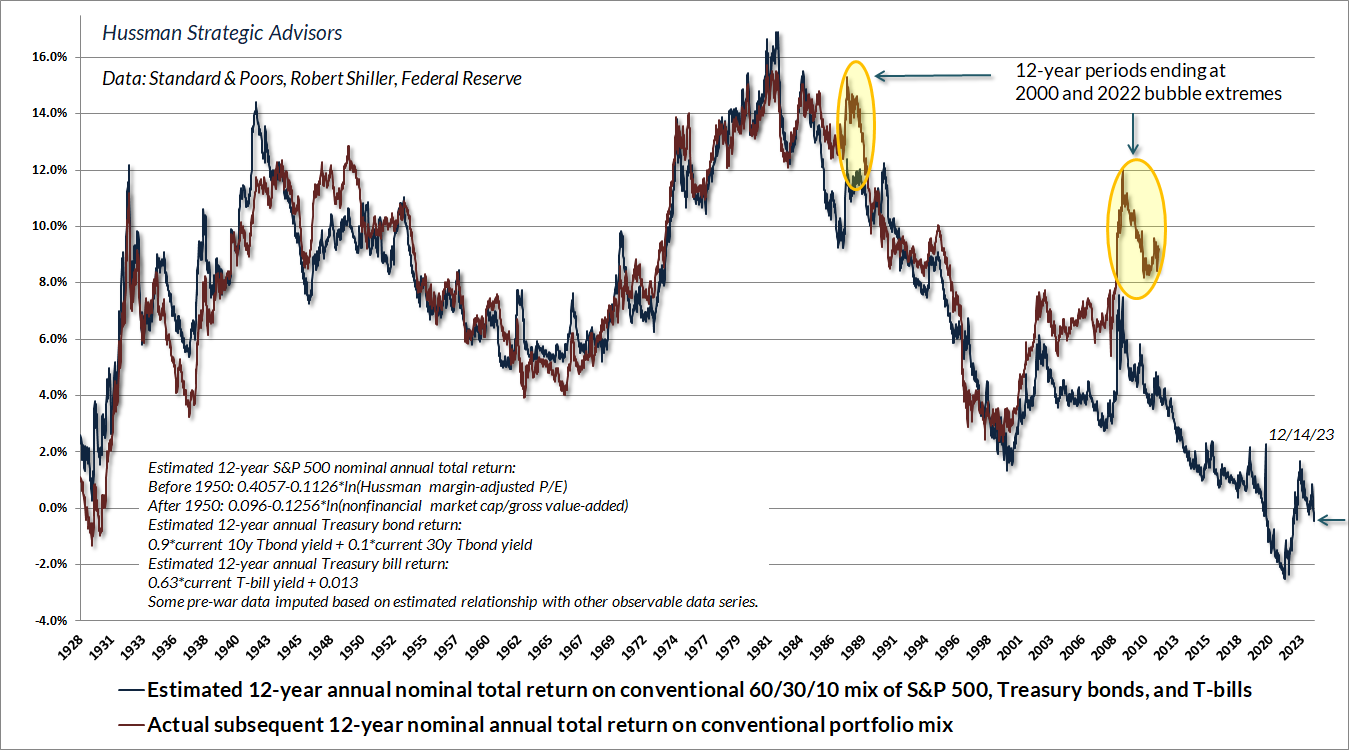

In my view, the expectations for coming rate cuts rely heavily on the expectation that core inflation will continue to retreat without interruption. That may turn out to be true, but by our estimates, the markets have more than priced in that outcome already.

Consider the 10-year Treasury yield. Historically, the entire total return of Treasury bonds, over-and-above Treasury bill returns, has accrued when the 10-year Treasury yield has exceeded the weighted average of core CPI inflation (0.25), nominal GDP growth (0.25), and the 3-month T-bill yield (0.5). The chart below shows the yield of the 10-year Treasury bond compared with this and a slightly broader benchmark. When bond yields have been below one or both of these benchmarks, bonds have lagged T-bills, on average. At present, the yield has dropped back to levels that I’d characterize as acceptable but moderately inadequate. The recent decline in bond yields has already priced a further retreat of over 1% in core inflation, nominal GDP growth, and short-term interest rates. While we may in fact see that improvement, the bond market, in my view, already relies on it.

The same is true for expectations regarding the Federal funds rate. By our estimates, the broad data are consistent with a relatively unchanged Fed funds rate in the coming year, in contrast to expectations of multiple rate cuts. There’s enough uncertainty in the economic outlook that we wouldn’t rule out Fed easing, particularly in response to emerging recession. Still, our baseline expectation is more muted than the enthusiasm we observe across Wall Street.

Reflecting a combination of steep equity market valuations and inadequate bond yields, we currently estimate negative prospective 12-year total returns for a conventional passive portfolio mix invested 60% in the S&P 500, 30% in Treasury bonds, and 10% in Treasury bills. As usual, investment outcomes over shorter segments of the market cycle will largely depend on the uniformity or divergence of market internals, but from present valuations, investors should not be surprised if conventional, passive investment portfolios continue on a long, interesting trip to nowhere.

{kind=link}

Merry Christmas to Mr Chaston and the team. Interest.co is the best.

I suspect the band of common taters make DC's eyes roll about much of the time. But you provide an excellent forum for us, and thanks. And thanks to the other common taters, well mostly. I learn heaps.

+1 always a range of perspectives & views which stimulates thinking & reflection processes. Often a valid critique of political & economic policies, across the spectrum.

I wish all hosts, contributors & commentators a safe & enjoyable holiday break with their families.

Best of all sites for the comment stream. Great discussions.

Merry Christmas and a happy new year to all. Be well and safe over the summer season.

Well said KH! How about rewarding Interest with a contribution ?

I wonder which Kiwisaver fund had the best returns for 2023? Would be a good story to close the end of year with..

Almost definitely Ark Nikko. It had a horror show in 2022, but this year gained around 80%

"Meanwhile, foreign patent holders are finding that Chinese courts side with local companies and will chop royalties agreed in existing deals that they subsequently don't like."

Those big corporations who exported jobs and manufacturing to make bigger profits are learning that the quality of Government is crucial where they send their technology. Cheaper in the long term to keep the technology, jobs and manufacturing capability at home. Better than building your own competition.

Could be an interesting start to next year. CPI is due Jan 24, if that were down to 0.75% for the quarter or lower, it’s within the RBNZ target when annualised. It would be very hard to justify causing a recession and unemployment with CPI within target and falling. A rate cut could be on the cards just a few months after the RBNZ saying they won’t cut in 2024! If they don’t cut and people lose their jobs when inflation is within target or even deflation, the RBNZ could look very stupid, and so could the National party for removing the employment mandate.

What sort of drop in inflation do you think would give the government pause for swinging the axe through/taking the freeze off of the public service?

None, they need it for their tax cuts and ACTs ideology. The tax cuts will be slightly inflationary however - although most of us will just add it to the mortgage payments rather than spend it.

Yes, it will be an interesting year, but why did you curtail your focus to inconsequential minutiae? Same mistake the Labour caucus will continue to make (some of the Party seem to know more).

Nonetheless, the 3-Clown Circus will be entertaining, in a sad sort of way.

Merry Christmas all,

China in focus this morning,

- IP - The rest of the world knows that any licensing arrangement with China is on their terms, want to play? pay.

- Graft - we cannot not throw any stones. Tried to get any infrastructure built? "Koha" for Cultral Impact Assessments is VERY much part of the NZ story, and it is for exactly the same reasons and at a similar scale.

- Pollution - honestly, hearing people talk about NZ "doing it's part", it's just beyond comprehension how dim these people must be. Pakistan is seeding clouds to get drizzle so they can BREATHE, it's a sad indictment.

US, not much comment in regards to how important it will be to reduce rates in 24. Essential maybe. "In the fiscal year ending on September 30th 2023, interest payments on America’s debt totalled some $660bn, up from $475bn the previous year."

Given that, the housing market looks like it will have a strong late 24 but we are now at a servicing ceiling I think so not much growth.

Strange selection for the rotating quote at the bottom of the page just now:

As prime minister I want to see urgent progress in this area [child poverty]. That is why we will be introducing measures and targets to ensure our policies across government are making a difference to the lives of children.

~ Jacinda Ardern

A policy statement rather than a witticism/something to ponder? Cf. the one I got for this page:

It’s a recession when your neighbor loses his job; it’s a depression when you lose your own.

~ Harry S. Truman

https://www.nzherald.co.nz/nz/prime-minister-christopher-luxon-under-fi…

This month, Luxon confirmed his Government would axe payments to te reo-speaking public servants, criticising those who took the bonuses.

”People are completely free to learn for themselves,” he said.”That’s what happens out there in the real world, in corporate life, or any other community life across New Zealand.

”I’ve got a number of MPs, for example, that have made a big effort to learn te reo ... they’ve driven that learning themselves because they want to do it.

”In the real world outside of Wellington and outside the bubble of MPs, people who want to learn te reo or want to learn any other education actually pay for it themselves.”

However, Luxon did not follow his own advice. After repeated requests, the Prime Minister’s office confirmed taxpayers paid for Luxon’s own classes using a budget offered to the leader of the Opposition.

”As leader of the Opposition and a potential prime minister at the time, developing better skills in te reo was highly relevant to his role,” the spokesman said.

From my experience, private sector CEOs have their language training paid for or subsidized by their companies. NZTE / MFAT staff do not pay for their language training out of their own pockets.

That article was briefly open to comments, and it wasn't going well for the Herald.

That's also because it wasn't about developing Reo Māori skills from scratch, but being compensated for a lot of specialist knowledge that very few people have (that goes way above and beyond just language). I've hired Reo Māori translators before, and it costs about the same as any other translation work.

I'd anticipate that the 'bonus' being paid was very small in comparison to the amount of highly specialist work being done in return. Each agency would've have made that bonus back in a week not having to engage specialist translators and advisors as contractors and consultants. To quote the article:

“I think if you’re in a government agency and you’re engaging with iwi Māori, or you are working with Māori communities where te reo Māori is used as a primary language, then it would be really relevant to make your public service accessible for that community.

“There are many situations where for people working in our public sector and public agencies, te reo Māori will be a very relevant skill for which they should be remunerated.”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.