Here's our summary of key economic events over the weekend that affect New Zealand, with news bank lending distortions are catching attention in both China and the US.

But first in the week ahead, all eyes will be on the American CPI data which comes out on Wednesday - and the following Fed speaker reactions. The US also releases retail sales data and PPI data this coming week along with a big sentiment survey. And the final big earnings reports are due for Q4. There will be the GDP result for Japan, CPI for India, and Australia will chime in with their January labour market update and the NAB January business sentiment report.

China is now on a full national holiday for a week (春节, Year of the Wood Dragon) and authorities managed to stave off a share market crisis before they closed in Shanghai (even if Hong Kong got the wobbles again on Friday).

In China, under official pressure banks are shoveling out the loans. Banks extended more than ¥4.9 tln in new yuan loans in January, a record high since comparable records began in 2004 and beating forecasts of ¥4.5 tln jump. Mortgages rose to ¥980 bln in new lending and corporate loans jumped by ¥3.86 tln. Meanwhile, "total social financing" which is a broad measure of credit and liquidity, also reached a record high level of ¥6.5 tln (NZ$1.5 tln), well above forecasts of ¥5.55 tln. But while the levels may be high watermarks, the growth isn't. In fact these expansions from a year ago are the least since 2004. That has led to calls to "do more".

In Japan, the Nikkei 225 Index jumped as much as 1.1% before settling only marginally higher at 36,897 on Friday, its highest level in 34 years as strong corporate earnings, a weakening yen and a dovish outlook on Bank of Japan monetary policy pushed the markets to these new heights. On Thursday, a Bank of Japan Deputy Governor said the central bank would not aggressively tighten its monetary policy even if it eventually decides to end negative interest rates.

In the US, the S&P500 closed above the 5000 index level for the first time. It was up +0.6% on Friday their time, up +1.4% for the week, and up +6% so far this year. And all this is in the face of rising bond yields which makes it a bit unusual. The Fed's 'win' in its battle against inflation while keeping employment growing is a key factor that profits remain robust. Investors seem impressed.

Meanwhile, lending by commercial banks to shadow banks ("Loans to nondepository financial institutions" in official language - line #26 in this data) topped $1 tln in January for the first time. It was up +12.2% in a year, although the big expansion came mid 2023. However, that surge caught the eye of the Fed who are watching for system risks from the big non-bank mortgage component.

In January, Canada added +37,000 new jobs in the month, a surprise because a decrease was anticipated. But +49,000 were part time positions and full time employment fell -12,000. Their jobless rate eased slightly on this data, also not expected. Unfortunately for them, their population grew faster than employment.

With China largely closed for its New Year holidays, commodity prices are likely to just meander along with little direction. But that won't stop chocolate prices racing higher on climate-related supply challenges. Cocoa prices were up +17% last week alone, to be up +42% so far this year alone, up +123% in a year and up +160% since this surge started in mid-2022. Chocolate is back only as a luxury item. Meanwhile sugar prices, which maxed out in 1975, aren't showing any similar acceleration.

Staying with commodities, the price of palladium fell below that of platinum for the first time since April 2018 as growing demand concerns and bets on stable supply weighed on the metal. The price of palladium is now at its lowest since mid 2017. Palladium (and/or platinum) is mostly used in catalytic converters for ICE cars.

Household spending rose +2.3% in December from a year ago in Australia. This was the smallest growth in household spending since February 2021. But that is before inflation was accounted for. Discretionary spending actually fell -0.6% (also before accounting for inflation). This data highlights how their cost-of-living crisis is affecting them.

The UST 10yr yield starts today at 4.18% and down -1 bp from Saturday. But that is up +13 bps from 4.04% a week ago. The key 2-10 yield curve inversion is little-changed at -31 bps. Their 1-5 curve inversion is still at -73 bps. And their 3 mth-10yr curve inversion is unchanged at -121 bps. The Australian 10 year bond yield is now at 4.16% and down -3 bps from Saturday. The China 10 year bond rate is unchanged at 2.45% and still looking quite manipulated - all other durations around it are still falling. The NZ Government 10 year bond rate is unchanged after a big run-up, at 4.91%.

The price of gold will start today up +US$1/oz from Saturday, holding at US$2024/oz.

However oil prices are still at US$76.50/bbl in the US while the international Brent price is still just over US$81.50/bbl.

The Kiwi dollar starts today at just on 61.5 USc and marginally firmer that this time Saturday. Against the Aussie we are unchanged at 94.3 AUc, and a 14 month high. Against the euro we open at just over 57 euro cents and also firmish. That all means our TWI-5 starts today at just on 70.9 and at its 2024 highs.

The bitcoin price starts today at US$48,128 and up +1.1% from this time Saturday. And this new higher level is its highest since December 2021. Volatility over the past 24 hours has been modest at just on +/- 1.5%.

Daily exchange rates

Select chart tabs

The easiest place to stay up with event risk is by following our Economic Calendar here ».

40 Comments

https://www.nzherald.co.nz/nz/debt-to-income-aucklanders-need-almost-20…

Patten said that banks have been only able to give out loans that are four to five times borrower incomes due to how costly it is to repay the loan with high interest.

However, when interest rates were as low as 2.5 per cent, banks were able to lend loans up to nine times incomes.

Therefore, the Reserve Bank said it wants to put in DTI restrictions now to prevent big loans being dished out during the next cycle of low interest rates.

Let's underline, interest rates are only back in a historically normal range. Using the term "high" is a mistake. The last ten years were artificially low to protect the global asset bubble.

DTi is coming. Better late than ever. Anyone who has not already done so, should restructure for the new "normal"

🍿

The current rate by itself may not be historically high, but the repayments at the current rates are historically high..

A frequently overlooked fact that changes the dynamics considerably.

High payments are caused by historically normal rates and speculatively bloated prices/debt. Which one should get the bullet...?

This seems a reasonably balanced and fact based report on a policy that aims to hold house prices down. I'm surprised it got past the Herald senior editorial team.

Agree. It will be at odds with the messages that Tony Alexander and OneRoof keep promulgating. God I hate nzherald.

'Next cycle of low interest rates'.....lol It cannot be denied theres certainly an appetite for low rates ... but how reasonable is that expectation ?

The tone of comments here on interest.co indicate a lot of hopeful wishes for low rates. Predictions based on need (maybe desperate need) rather than analysis.

As for me. I have no opinion which way rates will go

This is a good read

https://www.theguardian.com/science/2024/feb/11/atmospheric-river-pacif…

Atmospheric river storms are getting stronger, and deadlier. The race to understand them is on

Was always going to happen. More energy trapped in biosphere means more evaporation, bigger storm systems carrying more water.

Household Belt-Tightening: Will the Trickle Become a Flood?

The top 0.1% will weather a recession just fine, but that will offer cold comfort to the other 130 million American households.

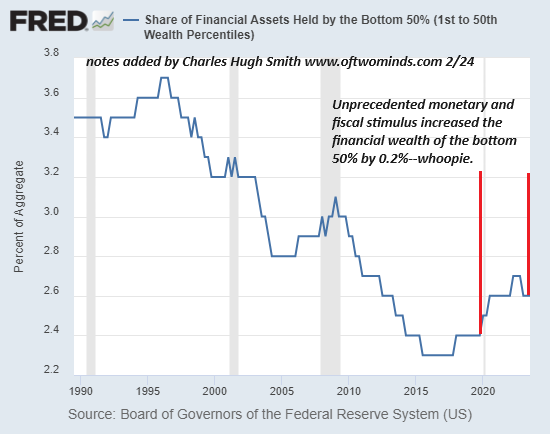

It seems at least some households are realizing they need to rein in spending. This reality is obscured by statistics which distort the financial security of average households. As always, we have to separate the top 10% who collect 40% of the income and own about 90% of the financial assets from the bottom 90%, as the top 10% distort the risks faced by the bottom 90%.

If we include the top 10% and look at all households, the average looks fine, because the wealthiest few skew the median and average upward. If we take total household wealth and divide by the total number of households, it gives the impression that households are doing great--look how much wealth the average household owns.

But this is a distortion. Remove the top 10%'s wealth and income and then re-do the calculation, and then repeat it for the bottom 50% of households. You end up with a much more accurate and much less rosy snapshot of American households' relative precarity. As the chart below illustrates, the share of financial assets owned by the bottom 50% of households rose a meager 0.2% to 2.6% despite trillions of dollars of stimulus flooding the economy.

{kind=link}

$2.7 Trillion Buys “Spectacular” GDP

Fresh GDP numbers came in and it was a blowout. The kind of blowout that only a $2.7 trillion government deficit can buy while the private economy crumbles around it.

Another couple blowout GDP reports like this and Americans will be living under an overpass.

This week the CBO published an optimistic outlook for the US economy/budget deficit/debt, which is based on laughable assumptions (no recession or inflation for a decade, sliding interest rates) but even with the rosiest of assumptions here is the trajectory of US debt/GDP Link

Bank of Japan Deputy Governor said the central bank would not aggressively tighten its monetary policy....

So... when will commentators stop writing stories about the inevitable return of conventional monetary policy in Japan? Surely it must be getting boring after all of these years and column inches?

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

{kind=link}

British farmers who have been thrown under a bus by Brexiteers take their protest against cheap imports to the Port of Dover. But perhaps they should be angry with the Brexiteers who told them everything would be great for British farming back in 2016?

It's hard to admit you got suckered by smooth talking politicians promising the world.

We'll see similar with this coalition, so far Big Tobacco, the fossil fuel lobby, landlord's and the ICE roading industry are the only winners. National stood on a platform of addressing the cost of living, let's see how well that ages.

Any word on the tax cut ..all I hear is crickets outside?

Farage wasn't even that smooth talking. A bellicose idiot, reminiscent of the news anchor from V for Vendetta.

Reminds me of Seymour and Winston.

Plenty more winners to come.

https://www.rnz.co.nz/news/in-depth/508914/lobbyists-are-back-at-parlia…

Democracy?

I know farmers in the UK and they were all for leaving the EU. Different story now, but they were most likely mislead at the time.

There was almost unanimous consensus from professional economists and bureaucrats that this would happen. People preferred to believe the magic solution offered by the culture-war anti-woke brigade with no actual plan. Sound familiar?

Every time they come in, my costs go up. When will NZ learn?

It's not just British farmers protesting. EU farmers are too https://www.bbc.com/news/world-europe-68249099

Sky city and the banks really need to pay lobbyist more and get this pesky money laundering and anti terrorism financing legislation removed. It's really not fair is it.

Yes and more Pokie machines for Sky City..the place is a actual delight to visit ..full of smiles, but well managed so problem gamblers allowed in.

Good old Sky Shitty, never been back even once since working there for a while. Never worked for a company whose profits where like $380m at the time to be so tight.

A handful of 8 million dollar fines might change sky's attitude....lol ...DIA needs to up its game...likely its been seen as a pushover by many sectors for too long...start biting chunks out of those laundering /not reporting I say....lol

China is showing its biggest problem again - its leadership has run out of ideas. I repeat - worst thing they have done is abolish term limits, Xi isn't as smart as his predecessors, instead is becoming a strong man. Soon the blame for all their problems will be pointed at foreigners, just like every strong man (Putin/Trump are the current batch).

70% of household wealth is held in property.... My guess is that many of their wealth management products are property funders, so there goes the other 30%

There are going to be some very angry Chinese, some may go hungry and that will bring back memories.... i am not sure that will translate into attacking Taiwan... not sure the young have such a death wish.

Attacking Taiwan would be China's downfall.

It is hard to guess which countries will be profitable long term.

It would be countries with good demographics and which can attract foreign investment and those which have access to resources unhindered by Green parties.

Ms Leung said after her poster was destroyed, some 200 pro-Beijing demonstrators surrounded her and fellow Hong Kong protesters.

No not in Hong Kong but at Auckland University 2019. Don't be so sure. Imagine how fanatical some of those young Chinese students are that haven't made it out of China yet and 20% plus Youth Unemployment does strange things to a young mind.

Disagree, China are still flying like an eagle while the rest of the western world tries to pull them down to join the pigeons on the ground fighting over the crumbs. Big changes coming in the world order in the next 10 years. The USA had their time and squandered it, no empire lasts forever. The problem is that the USA cannot even accept their own election results these days so slipping to #2 in the world is going to be war.

People risking their lives to get into US of A. People risking their freedom to get their money (and family) out of China and Russia.

Who has the winning strategy again?

Have you seen the videos of Chinese nationals coming through a hole in the Mexican border fence to the USA. Straight to border patrol post to claim asylum. Then vanish into the ether. Soon there will be another Great Wall Of China. But it will be built to keep people in. Berlin style.

Nov 23 "More than 24,000 Chinese citizens have been apprehended crossing into the United States from Mexico in the past year. That is more than in the preceding 10 years combined."

Have you been to China recently? I was there last year and the economic mood is sombre to say the least. Downright negative was the general outlook I had from most. There are pockets of growth, but a lot of it is still stuck in the old economic models of property and infrastructure, where they have overbuilt in both over the last decade or so. Those industries are where a most of China's capability and finance is centred, so as they slow down, so does China.

Half of my family over there are semi-employed now, a striking difference to 5 years ago where they were all employed or ran their own businesses.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.