By Martin Hawes*

Older people often want their wills to make bequests to their grandchildren. This is often more difficult than it sounds but KiwiSaver can provide a very neat solution.

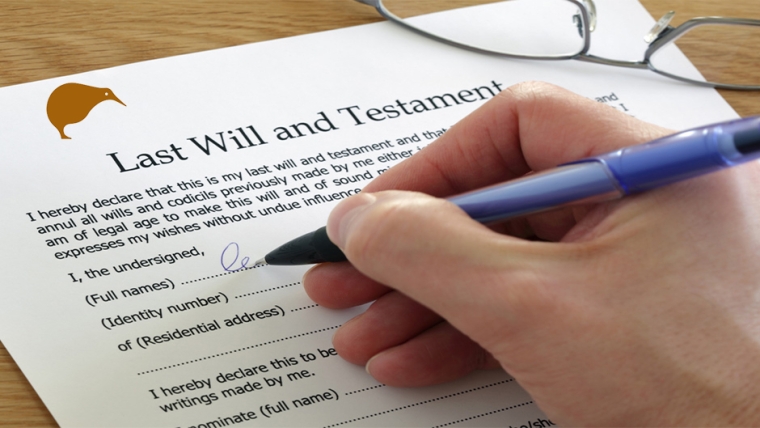

Writing a will seems to get trickier as you get older. Sure, nearly all of us want to leave most of our money to our children, but as we age there can be others who seem worthy of a bequest.

One of these could be a charity, something that we have supported financially or with our time and which we want to continue to support. This is important for a lot of us as we want to make a difference with what we leave behind.

However, it is grandchildren who really start to feature for many older people when they are writing their wills: they want to leave them money to give them the best start in life. The children will obviously benefit but as time goes on they can be less important – after all, most people who die at age 90 will have children who are close to 60; you would hope that someone at 60 had sorted their finances and were in a fairly good position by then.

But the grandchildren could be in that critical stage, perhaps aged 25 to 35 and really in need of some money to establish themselves. For children aged 60 some money is a good bonus; but for grandchildren aged 30, some money can be a good foundation to build strong finances for their whole lives.

For older people hoping to help grandchildren, the problem is that the great majority do not know when they are going to die and also they want to make bequests that will be for good purpose regardless of timing. It is possible that they die sooner rather than later and that could mean that funds need to be held in trust for years or even decades. Afterall, most do not want a three-year-old grandchild to get his or her hands on significant money (even though the local branch of Toyworld would be delighted!)

Enter KiwiSaver. KiwiSaver provides a neat solution for bequests to grandchildren and, without any need of a trust, allows for gifts and bequests to be made which will go for a good purpose.

The idea is that a bequest to a grandchild will be directed to KiwiSaver in the will and, over the years they are growing up, will become a significant sum. There will be little or no management, no trust required and there will be no difficulty with tax rates or concern about age of entitlement – the money will simply sit in their KiwiSaver accounts and grow.

Moreover, the money will be in KiwiSaver for a good purpose – not retirement which for grandchildren is far off in the distant future but the purchase of a first home. I think it important that they get the money while they are younger and use it to put their finances on a good foundation.

KiwiSaver allows withdrawals for a first home. Hopefully, the funds that were bequeathed to the grandchildren’s KiwiSavers would have grown to an amount that would make a good part of the deposit on that first home.

Leaving bequests to the grandchildren’s KiwiSaver accounts is very easy and cost effective: no trust need be established with decisions regarding age of entitlement or purpose for the money. They will end up with significant money that they must use only to buy a home.

For this, KiwiSaver serves an excellent purpose.

The only risk that I can see is that at some point there is a law change and the ability to withdraw money from KiwiSaver for a first home is no longer possible (meaning that the money has to stay in KiwiSaver until retirement). I doubt very much that this law change will happen: it would be a very brave (even suicidal) politician who would change KiwiSaver withdrawals in that way and I doubt they would stay long in office.

So, in essence, an older person’s will should be fairly easy to write and to execute: the bulk will go to children to do with as they choose. An amount could also go to a charity or the likes and there will then be an amount that could help the grandchildren into their first homes. That should make everyone happy – and, if you are the person making the will, here’s hoping that you have to wait thirty or forty years for anyone to see it happen.

*Martin Hawes is the Chair of the Summer Investment Committee. The Summer KiwiSaver Scheme is managed by Forsyth Barr Investment Management Ltd and a Product Disclosure statement is available on request. Martin is an Authorised Financial Adviser and a Disclosure Statements is available on request and free of charge at www.martinhawes.com. This article is general in nature and not personalised advice. Summer competes with banks and other KiwiSaver providers.

14 Comments

A side benefit to the original thinking undoubtedly, but a damn good one. Rather than actual grandchildren we are aware of the trustees of an independent trust vesting the capital into kiwisaver for the beneficiaries. Very good solution, very happy outcome for all involved, no more running costs, tax returns etc etc etc.

You mentioned the risk of a law change preventing use to buy a first home.....that is the problem with KiwiSaver. Wasn’t the idea floated about making KiwiSaver an annuity? The govt will find a way to tinker with the system to benefit themselves. Better off to bite the bullet and set up a trust in my opinion.

Don't you have the same (greater ?) risk that the Government will tinker with trust rules too. They have been an avoidance rort forever, so that may be more likely. And trusts become an accountant/lawyer gravy train.

True, however I am guessing lots of politicians have family trusts too. Therefore I would put more faith in the fact that they will act in their own self interest and leave the rules intact. KiwiSaver is another story....

I too are as cynical and suspicious as you of any one government’s intervention and/or political expediency. Trouble is you cannot possibly predict all the fish hooks and impediments that might be thrown into the soup. You have to set course and hope to navigate as fail safe as you can. Main attraction of Kiwi Saver is that at least the funds invested therein remain always under your title, all that is needed is the selection of an efficient and secure provider. In terms of trusts though, sad to say, there is far too much history of litigation, from a simple misunderstanding to actual nefarious come fraudulent behaviour. A quick scan through the high court lists will illustrate that well enough.

All you have forgotten about hardship withdrawals on Kiwisaver accounts.

I had a person who owed me approximately $10k, which thankfully in my case a kiwisaver withdrawal came to the rescue.

I'm not sure there's limit to hardship withdrawals, however one might like to consider Kiwisaver isn't idiot proof and open to abuse.

Even better, one of the currently considered options is to be able to use your first home drawdown to buy a home you don't live in i.e. an investment property.

As for making it impossible to draw down on at all - for those of us who are decades away from retirements, it would function effectively as an additional tax, on top of our student loans, on top of our regular tax and on top of the tax we pay on the bits left over after all the others bits are spent - GST. We don't have high enough wages to keep eroding people's take-home pay and locking some of it up for decades to an age they might not even live to is illogical. At least the first home drawdown offers some relief.

Government intervention is a risk in just about everything financial - starting with residential property rentals and on to family trusts. I think the likelihood of government stopping young people withdrawing their KiwiSaver funds to buy a house would be very low

This is exactly the situation I found myself in a few years ago, I had $?k for each of my young children and worked out the best way to invest it for them and their future was to put it into KiwiSaver. I was quite chuffed with myself for figuring this out, for all the reasons stated in the article. Then I started to question the rules around KiwiSaver and withdrawing funds to buy a first house. No one I spoke to could give any guarantee around future access to the money for this purpose. Waiting til the age of 65 was not an option for me as I want to help them into their first homes. In the end I invested the money into one of my own commercial investments and I pay a monthly amount into each of their KiwiSaver accounts, in excess of the return I get on the money. When they are ready to purchase a first home I will gift them directly the $?k plus they can use whatever money they have access to via KiwiSaver

First Home Buyers have had such a raw deal of late that I imagine there would be blood on the streets if any government dared to withdraw the kiwisaver house-deposit withdrawal scheme.

Incidentally, in the 1950s and 1960s a married couple would initially rent a property while both worked to save up a deposit for a house ( I'm talking about those who weren't born with a silver spoon ). They would then probably buy either a new or an existing "group house" ( e.g. a Neil or a Universal ) in for example Manurewa West which was then a respectable working-class suburb. After a few years they may decide to 'get ahead' and trade their house for a dairy which in those pre-saturation-by-supermarket days afforded a good income from working say 16 hours a day 7 days a week. Their initial house mortgage would have been replaced by a loan over the business by one of the wholesalers whom you would buy your stock from ( usually Gilmours or AWL ). The idea was to work the dairy until you paid off this loan....usually about 3 years. The couple would then sell the dairy and have a deposit large enough to buy in a more upmarket area, say Howick, if they were willing to take on another mortgage, or they could elect to go back and buy in their original neighbourhood and buy mortgage-free. Some couples would make 2 or 3 dairy purchases over a working life and do pretty well. And yes, they would bring up children along the way, helped by the fact that there would be intervals of some years between each dairy.

Reminiscent somewhat of a cartoon in the wonderful Punch when it was still about. Two senior banker types one saying, in our day the ambition was to pay off the mortgage, nowadays the ambition is to get one.

I haven’t read all the comments in detail as on my phone. But you can also get at your KiwiSaver money if you leave NZ ‘ permanently’. I’d imagine some would see their KiwiSaver as a good way to fund their OE.

Worst decision they could make but in the eyes of a 20 year old I would understand

A great suggestion, and a good way to direct the money towards a good purpose. The other risk would be that you set up your will, but your grandchildren buy a house before you die and before you have a chance to change the will. That would leave the money locked in KS until they retire.

Early withdrawal of KiwiSaver funds under COVID-19

KiwiSaver is a voluntary, work-based savings scheme, designed to help people prepare for their retirement. The primary legislative objectives of KiwiSaver are to:

• encourage a long-term savings habit and asset accumulation by individuals,

• increase individuals’ well-being and financial independence, particularly in retirement.

The policy drivers for the implementation of KiwiSaver were the perceived low levels of private saving for retirement and a concern that middle-income New Zealanders, in particular, were at risk of experiencing a substantial drop in their living standards during retirement.

However, an IRD study into KiwiSaver, found evidence to suggest that KiwiSaver has not been successful in improving the accumulation of net wealth for its members and that KiwiSaver members actually accumulated less wealth compared to non-KiwiSaver members.

The IRD cost and benefit analysis also showed that each taxpayer dollar the Government spent on KiwiSaver, only resulted in additional savings ranging from 20-38 cents for the target membership.

The study also showed that the primary incentive for people joining KiwiSaver was for the employer contributions.

For those made redundant under Covid-19 and facing long term unemployment, KiwiSaver has become a luxury that is neither consistent with their reason for joining, nor their changing priorities.

This raises an important question as to whether KiwiSaver members should have early access to their funds outside of the current withdrawal criteria which are; (a) reaching the age of entitlement for government superannuation (age 65 but likely to keep increasing), (b) first home buyers, (c) financial hardship, (d) moving overseas permanently (excluding emigration to Australia) and (e) serious illness/permanent disability.

Individual’s best interests can only be served if they get the best possible return on investment applicable to any given world economic scenario. The KiwiSaver rules are currently forcing people to remain exposed to a risky share market producing negative returns or to remain with cash tied up in a fund that isn’t working for them.

KiwiSaver funds have suffered huge losses recently and those losses are unlikely to be recovered in the share market within a long term economic recession.

In the current situation, the cost of debt far exceeds investment returns, so reducing or offsetting debt is a prudent alternative to continued exposure to the volatile share market.

Other alternatives to consider are; diverting KiwiSaver funds into businesses or other investments which are safer or afford more control and liquidity. Some have been forced to retire early and they should not be forced to wait for their retirement funds. Others might wish to invest their funds to re-train or up-skill for new careers.

In summary, my belief is that for many, KiwiSaver is no longer fit for purpose in the post Covid-19 recession. The IRD study showed that even in boom times KiwiSaver was out-performed by alternative investments and that for taxpayers, the costs of KiwiSaver out-weighed the benefits. There is no incentive for those no longer enjoying employer contributions. There are many ways in which KiwiSaver funds can now be put to much better use in order to achieve the original objectives of asset accumulation, individual well-being and financial independence.

If you are interested in pursuing early withdrawal of your KiwiSaver funds outside of the current rules, then please sign my government petition at:

https://www.parliament.nz/en/pb/petitions/document/PET_97690/petition-o…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.