By Alex Tarrant

The government-appointed Savings Working Group (SWG) has recommended the creation of a single, low-cost default Kiwisaver scheme, to be managed by an entity similar to the Guardians of the New Zealand Superannuation Fund.

As expected, it did not recommend compulsory Kiwisaver membership, but did recommend so-called 'soft complusion'. This is where all employees over a certain age are automatically enrolled in KiwiSaver but have the ability to quit.

In its submission to the government on how to improve the country's national savings rate, the SWG made a range of recommendations on Kiwisaver, fiscal policy and tax policy, saying the tax based needed to be broadened further.

Finance Minister Bill English said the only recommendation in the report government would not consider was raising GST from 15% to 17.5%.

“Otherwise, we are not ruling anything in or out at this stage," English said. Any immediate policy decisions were likely to be included in the Budget in May, English said.

When setting the Group's terms of reference, the government excluded possible recommendations on New Zealand Superannuation, which it has said it would not change, and broad taxation of capital gains or a land tax, which it had previously ruled out.

When asked about the SWG's comments in its report that "the tax base should continue to be broadened and tax rates kept low," - for which a capital gains tax and land tax would be lead contenders for - SWG chair Kerry McDonald said the Group did not have a view on those type of taxes because of its terms of reference.

"But you could imply a view within the framework of our overall recommendations. End of story," McDonald said at a media conference for the release of the report.

Later on Tuesday Green Party co-leader Russel Norman said a capital gains tax would be necessary to tackle New Zealand's savings problem.

“A tax on capital gains would remove the bias in our tax system making homes more affordable and help make the dream of home ownership a reality for more Kiwis,” Norman said.

"The Savings Working Group report found that without substantial tax increases, total government spending will have to decline each year in real terms for the next 30 years to return debt to sustainable levels, he said.

“Treasury and the Inland Revenue Department estimate that an additional NZ$4.5 billion could be raised from a comprehensive capital gains tax with an exclusion for owner-occupied housing. The additional NZ$4.5 billion will broaden the tax base, enhance its resilience, and be used to lower government debt to sustainable levels," Norman said.

'Urgent need to increase savings'

The SWG said there was need for an "urgent increase in national saving of 2%-3% of GDP annually" (NZ$3 billion to NZ$5 billion).

"[New Zealand] has borowed too much overseas. Net Foreign Liabilities (NFL), mainly debt, are 85% of gross domestic product (GDP), which is a similar level to the troubled countries of Europe. Australia is at 58% NFL," the SWG said in a media release.

The SWG recomended government create a single default Kiwisaver scheme comprising five funds for different age groups of investors. The manager of the default scheme would be similar to the Guardians of the NZ Super Fund, colloquially known as the 'Cullen Fund'. There are currently six default funds - see them in our new Kiwisaver section here.

The new low-cost default scheme would only invest in indexed-based shares and bonds, and would offer a limited number of of basic combinations for such investments, the SWG said in its 160 page submission to Finance Minister Bill English.

As reported earlier this week, the SWG did not recommend compulsory Kiwisaver membership, like in Australia but did recommend auto-enrollment of all new employees aged 18 or over who were not currenty enrolled in Kiwisaver, but with the ability for people to opt out.

It also recommended reducing the starting age of full Kiwisaver membership from 18 to 16.

Other Kiwisaver recommendations include:

- Spreading the kick-start payment (currently NZ$1,000) over a five-year period, and making payments contingent on ongoing contributions.

- Keeping the minimum employee contribution at 2% of earnings, but increasing the default contribution rate to 4%, with the ability to opt down to 2%.

- Not allowing employers to give non-KiwiSaver employees pay increases to compensate for not receiving KiwiSaver contributions. In other words, not allowing a "total remuneration" approach.

- Creation of an additional, low fee, ultra-low risk fund that invests only in short term government securities

Another option to be considered would be to increase the rate of member tax credits to NZ$2 for every NZ$1 contributed - either with no change to the current maximum annual credit limit (currently NZ$1,042), or in conjunction with a reduction in the current limit.

See the SWG's full report here.

Increase GST?

The SWG made a number of recommendations on tax policy "to remove serious distortions that favour housing and penalise interest income from basic savings products."

The Group said there should be a further shift away from income tax and towards expenditure tax (GST), with full compensation for people on low incomes.

An increase in the GST rate from 15% currently (up from 12.5% in October last year) to 17.5% should also be considered, the SWG said. However Bill English said later on Tuesday that National would not consider raising GST any higher than it is now. See English's full comments below.

In boosting interest income, the SWG said at a minimum interest income and expenses should be indexed at a notified standard rate for tax purposes that reflected the rate of inflation (eg. 2% per annum), and that asset cost bases for depreciation and, potentially, trading stock opening balances, also be indexed.

'Slash budget deficit much faster' - Govt savings first

In improving the national savings rate, the Group said the focus should be first on the government sector and shifting it from deficit to fiscal surplus of no less than 2% of GDP faster than the projected date of 2016. Raising the public sector's produactivity and productivity growth rate, from 0.3% to 2% per annum over the next five years and 1% per annum thereafter, would improve the country's savings situation and ability to handle financial shocks, the Group said.

"Government sector saving is an important component of national saving, particularly as government has more direct policy control over it and the ability to determine outcomes over a short time period. With significant productivity gains, the government has the option of either increasing government services or increasing government saving and thereby national saving," it said in the report.

"Given the merit of a quick and significant increase in national saving to mitigate New Zealand’s vulnerability, it would be logical to maximise government saving in the short term (as the area with the greatest opportunity for quick results) with a growing contribution from private saving complementing it in the medium term," it said.

English defends govt debt levels

Finance Minister Bill English later defended the government's debt levels, saying the absolute level of New Zealand government debt was relatively low by international standards, but the size of the government's deficit was now large by international standards, particularly this year.

"So we’re not overly concerned about the absolute level of the government’s debt – that’s in reasonable shape – but we are adding to it very rapidly. Our finance costs could double over the next three or four years from where we are now," English told media at Parliament.

The problem - taxes and house prices

One of the Group's key recommendations was that serious distortions in the tax system must be addressed quickly, McDonald said.

"Really it’s no surprise that we’ve invested a lot in housing and that our overall saving performance and investment in simple savings products – term deposits and so on – has been very much on the light side," he said.

Half of the growth in the price of houses from 2001 to 2007 was due to the tax distortion from the favourable treatment of property investment, he said.

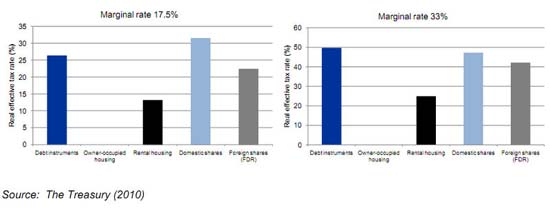

"If you put your money in [a] savings bank term deposit, something like that, your effective marginal tax rate was 50%. If you invested in a rental house, your effective marginal tax rate was 25%, and the return on your owner-occupied houses, which isn’t a matter of contention, was free of tax - so the real comparison is between investment in a rental house and putting your money in a simple savings product," McDonald said.

"You wouldn’t lie awake at night wondering why people are putting so much into housing investments," he said.

The chart below is from the SWG's report.

Here is the reaction from Finance Minister Bill English.

The Government will carefully consider the Savings Working Group’s final report issued today and any immediate policy decisions are likely to be included in the Budget later this year, Finance Minister Bill English says.

“This report will not only assist ministers in considering the Government’s next steps in building a stronger economy, it will also help an informed and open public debate on the national savings challenge facing New Zealand.

“The Working Group points out that New Zealand’s national savings problem has developed over a long period and it is unreasonable to expect it to be solved overnight. But it is a serious problem, requiring urgent attention.

"As a country, our reliance on foreign borrowing leaves us vulnerable to external shocks and means New Zealanders face higher interest rates – holding back our economy.

"Improving national savings is central to the Government's economic programme, which is designed to tilt the economy towards savings, exports and investment and away from excessive borrowing and government spending.

“As we said when the Working Group was set up last year, the Government has an open mind about what might be required to improve New Zealand’s level of national savings.

“Ministers will carefully look at the Working Group’s report over coming weeks with a view to picking up practical ideas that can feed into the Government’s economic programme and Budget 2011.”

Mr English thanked Working Group chairman Kerry McDonald and group members for their excellent work in providing a comprehensive report within a tight deadline.

The Government had deliberately set wide terms of reference for the Working Group. The only exclusions were New Zealand Superannuation, which the Government will not change, and broad taxation of capital gains or a land tax, which it has previously said it will not introduce.

“We are also not interested in considering another increase in GST, which the Working Group has suggested,” Mr English says. “Otherwise, we are not ruling anything in or out at this stage.

"The Prime Minister signalled last week that the Government is prepared to lift its own savings by taking decisions that reduce borrowing and get us back to meaningful surplus by 2014/15 – a year earlier than forecast.

“We are also considering options – such as the viability of the mixed-ownership model for four energy SOEs – that would reduce the amount we would need to borrow to pay for substantial increases in Government assets like schools, faster broadband and better transport infrastructure.

"They are just some of the steps the Government is considering to boost New Zealand’s national savings performance. The Working Group has provided a wide range of other practical options worth considering.

“By playing its part in lifting national savings, this Government will help to keep interest rates low and build faster, ongoing economic growth.

Here are comments from Green Party co-leader Russel Norman:

A tax on capital gains is one of the necessary components to addressing New Zealand’s savings crisis, Green Party Co-Leader Dr Russel Norman said today.

Dr Norman was responding to the Savings Working Group report which found that changes were essential to remove tax distortions that favour housing and penalise interest income from savings.

“A comprehensive tax on all capital gains except for the family home is the fairest, most effective way to encourage private saving and strengthen the Government’s books,” said Dr Norman.

The Savings Working Group report found that the tax system bias in favour of housing caused about half of the increase in house prices over the last decade.

“A tax on capital gains would remove the bias in our tax system making homes more affordable and help make the dream of home ownership a reality for more Kiwis,” said Dr Norman.

The Savings Working Group report found that without substantial tax increases, total government spending will have to decline each year in real terms for the next 30 years to return debt to sustainable levels.

“Treasury and the Inland Revenue Department estimate that an additional $4.5 billion could be raised from a comprehensive capital gains tax with an exclusion for owner-occupied housing,” said Dr Norman.

“The additional $4.5 billion will broaden the tax base, enhance its resilience, and be used to lower government debt to sustainable levels.

In addition, the Savings Working Group has drawn attention to the fact that our productive sector has suffered at the expense of the property sector due to this investment bias.

“A capital gains tax would address the unsustainable investment bias towards property, helping the New Zealand economy to return to earning its living from productive enterprise rather than speculative property investment,” said Dr Norman.

“Nearly every other country in the OECD has a capital gains tax. Australia has one. America has one. Until we address the property investment bias built in to our tax system, our productive sector will struggle and our savings levels will remain recklessly low.”

Here is the reaction from Labour finance spokesman David Cunliffe:

The Savings Working Group report released today makes a useful contribution to the urgent savings debate, but wrongly places too much emphasis on government debt and not enough on a sustainable and equitable path to higher private savings, Labour’s Finance spokesperson David Cunliffe said today.

“The report over-emphasises the role of public debt, and ignores any discussion of the impact of dramatically cutting public services further,’ David Cunliffe said. “Slashing billions of dollars from government spending and raising GST to 17.5 percent, as recommended by the SWG, would make the recession worse and would be unfair to Kiwis who are struggling the most.

“Labour notes National has quickly ruled out lifting GST again --- if it can be believed this time. Labour certainly won’t, and will actually be cutting GST to zero on fresh fruit and vegetables,” David Cunliffe said.

“Labour has also committed to making the first $5,000 of income tax free over time, and to closing tax loopholes and lifting the top tax rate above a comfortable six-figure threshold,” David Cunliffe said. “Any sustainable new savings policy must take account of the ability of Kiwis to participate. When Labour develops a comprehensive savings policy this year, it will do just that.

“Labour agrees that KiwiSaver should be broadened and strengthened, and notes the SWG is critical of Government moves to cut matching contributions to 2 percent and suggests resumption of a 4 percent option. Labour is carefully considering measures to strengthen KiwiSaver, including those covered by the SWG report.

“Labour also agrees with SWG calls to resume prefunding of New Zealand superannuation, which makes a vital contribution to building long term financial assets to cover future retirement costs.

“Labour in government used the economic growth to pay off debt and increase net worth,” David Cunliffe said. “Throughout that period National lobbied for tax cuts for the wealthy, which would have added upwards of five percent to gross debt.

“The SWG has also re-opened an important debate about removing tax incentives for property investment and improving the tax treatment of other forms of saving. Labour will carefully consider options in this area to ensure they are equitable, credible and sustainable.

“Labour will release its own savings package in the near future after careful study of the report and aims to lead the savings debate into the 2011 election.”

(Updated with English defending govt debt levels, second video, Cunliffe comments, McDonald comments on taxes and housing, Green Party comments on CGT, video of McDonald comments on capital gains and land taxes, English comment, link to full report)

155 Comments

Alex , do you have a link to the full first report of the SWG ?

Will have it for you shortly.

Here's the link at Treasury to the full report.

http://www.treasury.govt.nz/publications/reviews-consultation/savingswo…

cheers

Bernard

Yeah the GST rise sounds good! Phhh, Who likes riots?

Yeap raise GST make Kiwi saver compulsory and hold income tax....I'll dig out my old motorbike helmet

This is an interesting move. The Savings Working Group are asking the National Government to 'Nationalise' the Kiwisaver Industry. I can see a few idiology issues with that one.

And they are asking National to stop empoloyers using a total renumeration approach - wasn't it Labour that wanted that?

Another complicated financial structure to do what exactly? Provide people with some basic cash in retirement.

More bureaucracy. No thanks.

I'll throw out something completely different:

- Liquidate the overseas portion of the Cullen Fund completely and bring that cash back home (Total fund close to $18bln I think).

- Look at a Universal Basic Income to replace all welfare and superannuation payments. This should be set at a level similar to current superannuation.

- You could keep some incentives for saving such as no tax on unearned income.

- GST is a useful mechanism for regulating consumption but alongside that you need a CGT as well or preferably a Land Tax.

Have a nice day :-)

Simplicity has been a concept sadly missing from most of these "Working Group" vocabularies.

Couldn't agree more, raf.

raf is onto something, perhaps for a different reason than the one I see -

Investments have to reduce in value, over time, from here on. Hard to see the Dow stating where it is, kind of an artificial monument to optimism totally unrelated to reality.

Bring it home (just retire some debt even) while it's still up there?

Makes sense.

Powerdownkiwi, right on!

We have to stop confusing savings and investment. Saving is not spending money. Investment is a process of taking risk for a return above the initial investment.

Saving would be sticking money under the bed or in a world of continual inflation (see central bankers for explanation) investing in inflation linked government bonds. Paying down your mortgage could be considered saving also. You'll certainly save yourself some compound interest agony.

But frolics like the Cullen Fund and Kiwisaver are not saving....they are investments with a view to providing income in the future and long term capital gain (thanks to inflation, see above).

How much dough have people lost in investments in the last 30 years?....now where was that definition of insanity?

it's all falling into place nicely,the govt takes all of our income and hands back pocketmoney eg rest homes just enough for slippers and undies.south island can have german and american dairy farms,chinese the north island.

I don't mind 17.5% GST rate as along as we have a flat income tax rate of 20%. Nevermind that our black market will be booming!

I think this whole area of claiming back expenses for businesses needs a bit shake up in general.

There's way too much of it going on all over the place, property included.

Contractors setting themselves up as a businesses when just working in an office at another business, and then claiming back everything under the sun, that they use personally is a joke in my opinion.

And half the country will be unable to afford food - sounds lovely. But at least you will be rich and happy.

Yeap GST at 17.5.....cash will be King..

Ive already started. Im paying cash for everything I can. What they do with it is not my business. Its my small way of helping people escape from the cruel hand of the tax department and the waste of our government.

Big brother (IRD) is watching you!

Yep, I can relate to that. GST is simple but not necessarily equitable IMO. I could always understand it as a charge on goods, but was never sure about it as a charge on services. It simply makes a tradesperson's direct labour more expensive and makes it more more expensive for sole traders to administer their businesses.

I pay all my tax, Im just paying others in cash, it sometimes costs me but thats life.

My workmate got someone to paint his house 14K with invoice or 10.5K without. I guess it doesn't take a rocket scientist to figure which way....

Hope your workmate didn't pay without invoice.

I can't stand tax evaders.

They would no real excuse if someone robbed them, as they rob honest tax payers every day.

PS I don't like tax but do pay it all.

yeah, everyone love the tax department...

I think you mean, honest tax payers get robbed every day.

So do i ....BUT our own government is contemplating stealing our SOE's from us, not to mention the money stolen to bailout SCF in a corrupt GGS that's the only one in the world that covers investment gamblers + interest earned. I think i will let this one slide

Not to mention the number of times IRD have been given very good info on tax evaders only to put it in the "too hard, too small" basket. How do i know? Myself and some friends have dob in numerous people only to find absolutely nothing is happening to them. We are on the brink of going too the media to get action, phhh

Good on you justice keep doing what you are doing, definaetly go to the media.

Pretty short-sighted by the IRD not to act on a direct tip.

Exactly what i thought. We gave them figures and where to find the stuff and yet........I'm about to write to the Minister concerning the matter

read about the burying of the winebox.

The media dropped the ball before play commenced.

And never picked it up.

good luck

Yep I will second that.

Recommended read: Paradise Conspiracy by Ian Wishart

Be fair on the IRD they most likely get heaps of false allegations, revenge comes to mind and they have to weigh the evidence...they can gather.

The level of GST and taxes has more to do with government expenditure rather than savings.

Govt increases GST and reduces top tax, labour increases top tax and leaves gst, any tax tradeoffs are only temporary, taxes will rise. What about fiscal drag?

Money in the bank at 5% before tax, increase in gst and inflation puts paid to a return for the next 12 months. And to make up the loss will take another how many months?

Investing in the sharemarket should not be called saving, since when did we go from only invest in shares what you can afford to lose to investing in the sharemarket is saving.

We need people to save and while compulsion works it can back fire when retuns do not equal the white shoe salesmans spiel.

Until the marginal feel good factor of saving a dollar exceeds the marginal feel good factor of spending, we will not save.

Individuals save, not countries. Get the individual to save.

Have updated with comments from Greens co-leader Russel Norman calling for Cap gains tax

Raise GST to 17.5%.

You see that's the problem with these types of reports and why they are really just a waste of time and money. Having just put GST up to 15%, it is simply not politically or economically possibly to raise it again by another 2.5% anytime soon. So why even bother to suggest it? It's unworkable and the suggestion is almost pointless. We need things we can do from today to increase savings, not something that might have to wait 5-10 years.

What we need from these types of reports are pragmatic doable solutions that actually work in the world we inhabit. Not pie-in-the-sky, it all looks good on paper waffle. Sadly we get far too much of the later in this country from these types of reports and far too little of the former. This just looks like another thing that the Australians do better. We probably should have asked for and paid them to come over and do the report.

I doubt even Geoffrey Rush or Colin Firth could keep a straight face with lines like this:

"The Government had deliberately set wide terms of reference [sides splitting] for the Working Group. The only exclusions were New Zealand Superannuation, which the Government will not change, and broad taxation of capital gains or a land tax, [because these would presumably have narrowed the tor too much and had no positive impact on the problem?.... sides still splitting.] which it has previously said it will not introduce.

“We are also not interested in considering another increase in GST, which the Working Group has suggested,” Mr English says. “Otherwise, we are not ruling anything [oh please, stop it ...] in or out at this stage."

Laughter, so good for the soul.

As for the prime recommendations, I'll leave them for a rainy day - they gotta be good for something.

Have not read report, but is the issue of domestic savings being displaced with foreign savings, that is behind the following comment made to me by an experienced independent economist, addressed:

"For the banks in NZ, their interest and repayments cash-flows come in the form of NZD, and their big outflows are USD and Euro. That gives them a strong vested interest in stability or appreciation of the NZD, it makes them very unhappy about depreciation, and keeps them relaxed about the carry trade."

?

Cheers, Les.

Bill English: "Read my lips - no new anything".

That is a very interesting comment at the bottom there Les. I will let that one digest for few days.

Something I have been wondering about lately is this carry trade. If it is so great and 17x our GDP exists in the FX trading game, I assume most of it driven by the carry trade, then who is paying the interest on this money?

Does it not cause an upward spiral in the money supply?

Scarfie - have a squizz at this:

http://www.rbnz.govt.nz/research/bulletin/2007_2011/2010sep73_3cassinowallis.pdf

The majority of trading is yield driven, which ever way you cut. Hence the need to drop the OCR, and then use a money supply volume control of some sort, eg. good old LVR. Using price of debt (OCR) is flawed and in one aspect fundementally, because it directly works against the intent of it's purpose. (The sooner we sort that intent thing the better, but I digress and play on words a bit.) Have a look at a discussion I had wiv' d' lads (Matt S, Fred) here down from my comment at 05 Jul 10, 1:03pm:

A simple piece of reasoning that illustrates that use of interest rate actually increases price inflation. No surprise really, interest rate is price of debt, or credit, so if you increase the price of it....anyway. The dynamics involved however means that doing so creates cycles, which does not need to happen and is not desireable, unless you are a speculator, of course. Next, have a think about this engineering analogy that illustrates more flaws in the OCR regime:

"Take the economy as modeled by a hydraulic pump and the OCR mechanism is a differential-pressure actuated input flow control valve. The differential-pressure is determined as the difference between the pump output (read via CPI) and a system set-point pressure, the PTA's CPI band. Inertias in the flow control valve and in the pump create one aggregate component of response-lag. However, the differential-pressure signal is moderated by the inclusion of a damper (a gas accumulator say*) in the control-signal transmission line. This creates another lag ('pure time delay') which is essentially the 'blunting' effect of fixed rate loans. Hence the price signal is corrupted and the market is not made aware of conditions that the price signal is meant to communicate, in a timely manner. (But NZD changes value hits almost instantaneously, funny that.)

* http://en.wikipedia.org/wiki/Hydropneumatic_device - an appropriate degree of damping reduces instability brought about by under-damping. BUT, systems become similarly unstable if control signals are over-damped - because they do not meet their purpose of correcting output, via modifying input."

If we put this in Austrian speak, (I think) they are very keen on pointing out the difference between price inflation and money supply inflation, and how the latter begets the former. With the OCR 'price signal' based mechanism we assume money supply inflation (demand) can be sensibly controlled, indirectly, by changing the price of debt. Perversely this is not the case, see above, hence it'd be good to compare a plot of OCR, private-debt growth, the three inflations and currency. We maintain the PTA target by killing tradeables, actually using NZD as a moderator on tradeables and export margins. All the while non-tradeables goes blithly onward and upward.

And we wonder why we have problems.

Cheers, Les.

Have updated with section on McDonald comments on taxes and housing

"One of the Group's key recommendations was that serious distortions in the tax system must be addressed quickly..If you put your money in ....your owner-occupied houses, which isn’t a matter of contention, (it) was free of tax ...McDonald said."

So make it contentious! Tax the implied equity in owner/occupied houses. If you want to get politically squeemish about it, make the tax free thresh-hold equal to the average national house price, say today @ $342,000. Over that, any 'savings' ploughed into an over median property gets that portion taxed at a rate to normalise it with, say, an investment in 1 year Government Bonds.

Excellent - simple.

Why do these over-rated "advisors" have so much trouble coming up with commonsence, concrete and simple ideas/solutions?

And, then, when one of the members does have an innovative idea (such a Gareth Morgan's Big Kahuna), the matter has to be raised (by Gareth) OUTSIDE the officially produced WG report - as (in this case) discussing the welfare side of the ledger was not a part of the Tax Working Group's terms of reference. Typical bureacratic nonsense.

Key does seem to lead with a greater degree of bureaucratic BS than most politicians. All this Working Group carry on makes me even more and more suspicious. With Helen Clark there was no question about who she was or what direction she'd take. She was fundamentally what I think of as a "patriot-type" politician - in it because of a set of beliefs (whether you like them or not is anothe matter). Ronald Reagan also seemed to be one of those sorts, as did David Lange.

But, why is JK in the job? He's certainly no revolutionary or visionary - and he's definitely not a Repulican, given he restored titular titles. The only reason I've heard given as to why he went into politics - is because when he was a kid he said to someone, "someday I'm going to be PM".

So his ambition didn't spring out of admiration for a politician past, or having a "calling" to statesmanship, or a civic idealism.... but rather all I've read anyway suggests he simply set a personal "goal" for himself as opposed to "for the country" per se.

And with his earlier secondment to the NY Fed, I do wonder whether he was encouraged by the banking fraternity to head home and take on this change in career direction. Given how quickly he came up the Party ranks, I also wonder what he personally donated to the National Party to make that happen. Nothing illegal about that, of course, just curiousity.

Like Obama was - JK was a bit of an unknown 'new entrant' - and both are proving themselves as quite weak in the area of change management/change leadership.

Kate,

You raise interesting points. John's already said if he loses the election he will leave politics. In some ways that is refreshing when compared to the career politicians like English or Goff who could do with some time out in the real world. So you could argue he doesn't care either way. It's no loss to him, he's enjoyed the ride and being PM and is set for life.

I'm hoping for some more fire and focus from the Greens this year otherwise I'm not too excited about what's on offer.

And if that happens I also guess he'll leave NZ - along with his knighthood, of course!

I get the feeling JK really thinks of NZ as too small and (dare I say it... boring!). Whereas Helen holidayed in the Southern Alps - John heads to Hawaii. It sort of "says" something.

hey kate,

drop me a line directly @sustento.org.nz

Helen also holidayed abroad Kate. Often in Sth America/Europe - usually walking hiking trails there.

Ms Clark's favourite holiday was a chalet in the Swiss alps .

That will be fine with Kate, Gummy, so long as Ms Clark didn't own the chalet! :-)

Ms Clark's supporters conveniently overlook the fact that she is a financially wealthy person , and has a taste for the finer things in life ........ I admire her for that.......... . But Helen's fans rip into JK for being a " rich prick " !

Roger, what is the definition of "rich prick" ?

Walter : It was Michael Cullen's expression ...... And judging by his policies , and introduction of the 39 % income tax , I'd guess that a " rich prick " was anyone earning over $NZ 60 000 / year ............ Those indulgent , decadent ladies and gentlemen on $ 1200 per week . Lucky , lucky bastards !

HC is worth a couple of Million? (Property?) JK 50million plus? so a difference in scale.....plus is she rich or is she and her husband rich? bearing in mind neither have children and both have good salaries and both are BBs having some substantial assets isnt that surprising.

That aside yes it isnt nice.....I see nothing wrong with JK's success.........

regards

"Why do these over-rated "advisors" have so much trouble coming up with commonsence, concrete and simple ideas/solutions?"

They weren't picked to be objective i would say. Check the party membership on all of them or corporate connections. The whole thing was a charade like the last one

John 1:18pm

The last thing we need is for people to save. With fractional reserve banking for every $1 placed in the bank this allows the bank to lend (probably) $100 so it's no wonder our country is so indebted.

Look at grand parents and their life's savings slowly being eroded by inflation.

Inflation IS the root of all economic evil! So........why does our government allow Bolly from the RBNZ the target of 3%? when the target should in fact be 0% at all times?

But when you aim for 0% inflation it is very hard to justify charging interest like the banks do.... hint hint

Inflation is part of the debt/interest money system. That's why I laugh some much when I hear bankers and politicians going on about inflation. It's programmed in people!!! Public money issued free into circulation would actually be deflationary. Funny that.

deflationary? So if we all got given 100 thou from the government print tomorrow you think the price of milk and butter and bread would go down? Please clarify

er no. the price of commodities is more of a global issue and to bring prices down locally we would need to institute a local quota allowance which is possible but not what I am talking about here.

when new money comes into the economy it comes via a commercial bank issuing a new loan. this "money" is debt with interest attached. That interest does not actually exist in the current money supply so new money must be created to pay that interest OR money from the current supply must be used.

the former leads to inflation, the latter to bankruptcy...this is also known as the business cycle.

introducing new money from the public without interest removes the need for new loans (and therefore new money) and therefore removes the inflationary bias.

a very good explanation of this can be found by watching "Zeitgeist Addendum", a fabulous movie available on YouTube. I watched it with my kids the other night and they got it straightaway. I highly recommend it.

"introducing new money from the public without interest removes the need for new loans (and therefore new money) and therefore removes the inflationary bias"

And who do you give that "out of thin air" money too Raf? How do you stop them charging interest at some point? Your STILL talking about creating something from nothing. I too have watch all of the Zeitgeist films and they miss out some key factors in the economic one.

Something of value must first be created and money (paper tender) has no value. Gold atleast has a REAL value due to it's use in technology and how much actual labour must first go into getting it. It makes more sense to create a currency from something with value that has a 'finite' supply. Creating dollars is not finite which leads to another key point: Population growth! A limited currency would also limit population growth and economic growth. THIS is not something many will accept as it actually obeys the fundumental laws of Nature. The human race doesn't yet accept that the earth and all it's resources IS limited and so must we as a species

"introducing new money from the public without interest removes the need for new loans (and therefore new money) and therefore removes the inflationary bias"

And who do you give that "out of thin air" money too Raf? How do you stop them charging interest at some point? Your STILL talking about creating something from nothing. I too have watch all of the Zeitgeist films and they miss out some key factors in the economic one.

Something of value must first be created and money (paper tender) has no value. Gold atleast has a REAL value due to it's use in technology and how much actual labour must first go into getting it. . It makes more sense to create a currency from something with value that has a 'finite' supply. Creating dollars is not finite which leads to another key point: Population growth! A limited currency would also limit population growth and economic growth. THIS is not something many will accept as it actually obeys the fundumental laws of Nature. The human race doesn't yet accept that the earth and all it's resources IS limited and so must we as a species

So many questions!

- You can introduce new money through a Universal Basic Income or through direct Public spending (you don't need PPPs).

- Interest can still operate within the economy either in its current form but reduced or simply as a savings and loan format. But interest becomes a fee rather than a compounding beast.

- This wouldn't happen overnight as you would need an incremental change. Imagine a blood transfusion (clean money for dirty debt).

- Monitoring the money supply would be the main tool (using banks core asset ratios to tighten bank credit as you introduced real money.

- Yes fiat money is fiat money but one step at a time :-)

- In the fullness of time (balanced budgets, current accounts etc) we could attach our clean, domestic supply of money to a basket of commodities/resources.

And they lived happily ever after :-)

Inflation is not the root of all evil Justice it is just something that needs to be factored in when you decide to hold cash at the bank that the money's value will depreciate - even after interest and less tax on interest the money becomes worth less in terms of buying power so why do people hold onto cash?

Shooting for 0% inflation is also futile not because it's not an admirable goal but because banks wouldn't make a profit and if banks cannot make a profit then they would be forced to actually work and invest the money in profitable businesses that make a profit to pay interest.

As the situation currently stands banks can make a fortune simply lending out money to home owners who take all the risk not just in terms of a house price depreciating in value also in-terms of being bailed out by government (tax Payers) if it all goes pair shaped - why would they wont things to change?

If John Key was serious about creating growth for NZ he would simply aim for 0% inflation and get banks to invest deposits in local and overseas' business markets in order to make a profit and pay interest to those depositors - that is what bankers used to be skilled at doing in the old days before they became lazy.

At the moment banks are simply robbing Peter to pay Paul and in the process selling our housing property writes to overseas interests whom lend the banks money. These overseas banks lend money which is no-doubt secured through mum and dad property ownership writes.

"Shooting for 0% inflation is also futile not because it's not an admirable goal but because banks wouldn't make a profit and if banks cannot make a profit then they would be forced to actually work and invest the money in profitable businesses that make a profit to pay interest."

I think that was my point!

Also Inflatiion is created due to paying out interest on currency. Paying out interest is NOT essential unless your charging interest on debts. This creates a ponzi scheme in currency where your dollar just keeps getting devalued and so forcing up prices to cover the costs of debts. Inflation is evil! We only tolerated it because we ALLOW banks to rule the world, not our governments. You do realize this right? Banks rule, not governments?

Justice. Correct. Inflation is many things but primarily driven by an expansion in the money supply relative to production in the economy. Interest drives the need for expansion in order to pay the interest.

One only has to look at the Davos ensemble and see who is running the show. Bankers meet with politicians and give them the good news. The Obama administration is like a Goldman Sachs alumni team.

Not quite what the Founding Fathers had in mind.

The economic system we have has to have an inflation rate of about 2~4% to be stable.......

There is also a train of thought that to get/keep un-employment at an acceptable figure ie <7% you need inflation at about 2~4%.

So hence why the Pollies are so petrified of deflation....

regards

Have put in comments from Labour's Cunliffe.

More coming soon

Russel Norman of the Greens says...........

“A capital gains tax would address the unsustainable investment bias towards property, helping the New Zealand economy to return to earning its living from productive enterprise rather than speculative property investment,” said Dr Norman.

“Nearly every other country in the OECD has a capital gains tax. Australia has one. America has one. Until we address the property investment bias built in to our tax system, our productive sector will struggle and our savings levels will remain recklessly low.”

Yes and their property bubbles are worse than ours. Get a clue you half-wit!

You get a clue! Their crisis along with ours was caused by CHEAP CREDIT, NOT a CGT!

Too much cheap money made their CGT's irrelevent but that would not be the case here in NZ right now would it? CGT needs to be highest tax people can pay!

Russell is 100% right and here's why. There will not be another credit crisis in the near future allowing ridiculous speculation of prices on housing.

The only weakest link is the RBNZ who would rather see the banks win at any cost, hence they never intervened into the crisis in the first place with substantial OCR rises during 2001-2006. Bolly and his idiot crew only care about the keeping the banks earning, they care nothing for the real finances of ordinary people.

David, statements like yours is when traditional ideology behaviour interferes with healthy brain power - nothing makes sense.

Their property bubbles are worse because they had very low OCR's which meant cheap easy to get, low risk credit....On the other hand some states such as Texas had strict lending rules and as a result didnt have the property bubble to burst......

Is a CGT "THE" answer, no, but from the looks of it it cools the market a bit.....so it as the desired effect but not the degree.

What you want to maintain is a reasonable OCR and tight credit lending criteria such as a max of 80%....

And note it isnt just RN saying this....quite a wide spectrum of economic thinkers also seem to think its a good idea.

BTW, US credit cards I think had an interestrate of 7%!.....let alone cheap mortgage rates of like 2 or 3%....

regards

Yes private debt levels are awfully high.....but.....government debt levels are quite low when compared globally. We also have hard assets which mean people will take our IOU (unlike Iceland, Spain, Portugal, Ireland, Greece).

Did I mention Japan was downgraded last week....the 3rd largest economy in the world....Yen is actually higher than when the announcement was made.

Feels like the gremlins have been let loose to scare everyone. There are no answers here, merely more questions.

Our government debt per head of population is enormous The old "its low compared too other countries" is a major cop out due to the fact most of those coutries are bankrupt!

Around $40,000 for every man, woman and child in this country. Now add to that our personal debt and hey presto! wer'e looking screwed.

Justice,

I want to make the point that there is a danger of the shock doctrine (see naomi klein) being applied here with forced asset sales etc. So I want to make clear that in terms of overseas investors NZ is not flashing danger lights anymore than it has for the last 5 years.

One thing I would say in John Key's favour is that he is trying to tackle this issue. Unfortunately Labour just sat back and enjoyed the feast. I think the simple difference is Michael Cullen (and by extension Helen Clark) had very little financial nous.

We have a mountain to climb for sure but all is not lost just yet.

I'm no fan of Queen Helen and her useless failed teacher crew Raf! believe me But............I'm afraid JK and BE have either been kidding themselves or the general public or both. We ARE in a very dire situation which selling a few SOE's for peanuts is hardly going to solve. They need to get real, be honest and make cuts everywhere while hitting PI's hard

Justice : Are you sure of that figger ? ....... I thought that gumnut debt was only $ 4000 / head of population , but private debt ( dairy farms and rental houses mostly ) was near ten times that .

$186B / 4 million peeps = $46,500 each soul living in NZ owes in overseas debt I thought?

Yup , but the majority of that debt is private , not gumnut . ........

.......... hey , whilst I've got your attention , how's aboot a wee trip down mammary lane :

After visiting NZ in February 2005 the Swedish PM Goran Persson stated of his meeting with our PM ( translated into English ) : " Clark explained that the reason NZ tax rates are not as high as Sweden's is historical , the social democrats have not been in power long enough , yet . "

.......... ahhhhhh , Helen Clark ....... wasn't she lovelly !

LOL........I don't miss her . I hear she has opened a paint gallery recently under her own name?

URL?

Cant find data thats up to date but what I can find is in 2009 the debt is 9k per person, but that includes all debt...

Govn debt appears to be around $4k per person with private debt over double that...

Another site says 12k for total debt....

http://www.nationmaster.com/graph/eco_deb_ext_percap-economy-debt-exter…

So I suspect your $40k per person is way OTT.....can you justify it?

OZ seems to be $40k....

regards

National debt is around 186 billion. That includes like Gummy said ALL debt government and personal. Your 9 thou for personal is way low

Go too the RBNZ site

But public debt is low.....screaming that the debt is too high and Govn has to fix it when its mostly private debt makes no sense.

regards

Let's remember that we are talking about a monetary system that is almost 100% debt. In a world with $55trln worth of derivatives (most off balance sheet) and with the worlds largest economy with a $14trln national debt, we are in danger of missing the point here.

The whole world is awash with debt....all new money that comes into the supply (minus $4bln for NZ) arrives in the form of debt. Once that happens the clock starts ticking. It's been ticking for a long time in NZ and nothing has ever been done about it.

We must reform our money system from the ground up. Believe me, anything less is like shuffling deck chairs on the Titanic.

agreed

Where's the real 'boldness' of ideas from these working group clowns? Is this the best they could come up with? Half the people on this comments chain have bolder and better ideas!

My god, these people are the most unimaginative group of suits that it's no wonder this country is going down the tubes! Were they not paid enough? Phhhh, isn't that the excuse these elitists use?

Ive shared my ideas and so have many others here. One thing is for certain. If we do not start thinking and IMPLEMENTING radical ideas that work and rebalance the wealth and remove the "me me me want handout" culture in this country then we are stuffed.

They key point is anything that works....let alone radical.

regards

There's now a second video in there with further comments from McDonald at the press conference

Cheers

Alex

Hot off the MEA presses:

Terms of reference blight SWG report

The exclusion of a capital gains or land tax from consideration has prevented an accurate assessment of measures needed to promote savings by the Savings Working Group (SWG) say the New Zealand Manufacturers and Exporters Association (NZMEA). The SWG detailed the tax differences between assets and other forms of investment but was prevented from drawing the logical conclusion. There is little point tinkering with savings vehicles while large tax harbours still exist.

The SWG estimated that the tax system bias in favour of housing caused about half of the increase in house prices over the past ten years, and that this distortion encouraged “investment in housing rather than investment in more productive assets that would have lifted productivity and potentially lifted exports.”

NZMEA Chief Executive John Walley says, “The major reason we see a see a low savings rate at the moment is that borrowing on a property is the most tax advantaged way of building wealth. Unfortunately this method of growing wealth also increases our foreign borrowing (as the banking sector chases the lowest cost of funds, and in the process overvalues our currency) and starves our productive economy of capital and margin which would otherwise be available.”

“There is little point in the Government commissioning working groups to investigate these problems if they are going to restrict their findings. Just about a year ago we heard from the Tax Working Group that a capital gains or land tax is needed; burying our heads in the sand is not going to fix our problems.”

http://www.realeconomy.co.nz/148-terms_of_reference_blight_swg_.aspx

Les, I think its a government ploy. They know damn well we need a CGT and LT but are buying time with these lame ass working groups so as to get their OWN finances (loopholes)in order first before they lead the flock down the road to tax.

Look at the whole Family Trust rort! First players in were MP's and government public servants and they will be first out if not already. Ask Bill English!

One word of caution about a CGT. It has to be implemented as from a specific date. If it is implemented at the top of the property cycle, and there is a property bust just around the corner, it will collect zero tax for the next 20 years. PI owners will carry forward losses for any number of years if not quarantined plus offsetting income, otherwise forever if they are quarantined. The best solution is a "stamp duty" or "transfer tax" on the purchase and transfer of ownership of property.

Back date it! Problem solved. Make the taxable date back to 2005 ;-)

Many PI's ( the real ones) have no interest in selling EVER so how will the TT or SD get them?

You need to force the sale so why not make all direct rental income taxed at a higher rate ...say 50%? This will effect rental costs 'initially' for tenants I'm sure due to landlords trying to get back but in the longer term they will have to sell because average tenants incomes will not come close too covering the mortgage plus taxes

Better yet, just make it a comprehensive capital tax - as per Gareth Morgan's suggestion.

You pay more of it on the upside (gains) and less of it on the downside (losses).

Introduce it while lowering taxes on labour and profit.

fine by me

Iconoclast, I don't have a great handle on macro economics, but would stamp duty be better than a CGT? It seems to me to be less complex and probably easier to administer.

The call for CGT from some here seems to be more about envy than anything else. Your sage advice would be welcome on stamp duty v CGT. :-)

Casual Observer

In several earlier posts I have made the point that investing in property is a proxy for investing in inflation. It follows that a CGT on the property asset class is a tax on inflation. It follows that Central Governments then have a vested interest in continually inflating the economy. A good "Tax System" has to be both certain and simple, and a CGT regime is neither certain nor simple if it embraces all asset classes. Could be simplified if limited to "Property Capital Gains only". The one problem from a revenue point of view is it assumes inflation will continue for ever. As mentioned above, the timing of the implementation of a CGT is critical to its success. If implemented at the wrong time it would be a complete disaster. I'm located in Melbourne. They have both taxes, a "Transfer Tax" in the form of stamp duty, and a CGT which excludes the family home. CGT doesnt collect much tax whereas the individual states are addicted to Stamp Duty because it bring in $billions every year regardless. And it is a huge disincentive to "flick" property.

Thanks. I just wondered if I was missing something as I don't understand why the call from Goff, Kate etc if they were serious, isn't for stamp duty. :-)

If you look back over the last couple of months you will find the "authorities" are flying kites around the idea of a CGT, and everyone is slowly warming to the idea and its getting a bit of space dedicated to it, while I'm the only one saying it doesnt achieve what it's intended to achieve, if anything at all, other than increase the bureacracy.

Do you think the powers that be ever come here and read this stuff?

They would be stupid not too so............no probably not. We don't necessarily have to make OUR CGT complicated at all. The simple fact is the economy is being destroyed by property hoarders and lack of real business investment. Any ideas (simple as possible ones) that go to rebalance this are desperately needed. Question is do we have a government willing to tackle real problems with real solutions? You and I both know the answer to that one don't we? So we face the reality for the time being ( a decade more or so I'd say) that things will only get more dire. World governments are just not willing to take on the Global banks and their economic interests which are seen as more important than the community at large

Would not stamp duty not be even more simple. It won't create an industry for 'exemption compliance' like a CGT would as there are always some exemptions in the various CGT regimes around the world. On a falling property market CGT as a money earner is not a certainty. As iconolast pointed out, stamp duty revenue happens regardless of what the property market is doing. It is a sure bet as a revenue earner - but that is not to say I agree with it.

CO. I think a capital gains tax should be a mechanism to stop bubbles not a revenue stream.

In that regard Aj, it hasn't worked anywhere else in the world so why would it here?

The people are getting played....da dah once again..!

English..".no intention of further GST increase....or CGT..".......but the threat is enough to get people thinking about a partial sell off of SOE's.........they want us to scream for it.... the reaction to the idea when floated two weeks back was generally poor and so Billy Bob see's a little threatening language as reasonable to get the masses on the same page.

It just shits me that Key and English have come through the back door with this and in fact have managed us into the position...(you recall English's late year interview saying he was comfortable with the level of borrowing..Key sanctioned it also).......instead they could have gone Public ...argued for the partial sell off as the desirable option and afforded us the honesty we appear to be deemed not worthy of.

Tactically the dynamic duo's handling of this matter was woefully managed given that they have no real opposition to speak of....why the need for the chess game...Billy...why ...? because it conforms to the nature of what you perceive is politics.......they should have been more honest when they demoted you the last time.

you'll get over it .............i did.

You forget your dealing with two of the biggest gutless wonders in politics!

"Why are you such a poor saver peasant?"

"Cos if I save I pay heaps in tax and my savings get debased every year."

"Is that the only reason?"

"Hell no...I aint got no spare cash to save cos my rent is stonking friggin high"

"Why is that?"

"Cos the landlord borrowed heaps from a bank to chase the property price up the wall and now I gotta pay more rent cos he has to pay more interest"

"But the landlord can deduct the interest as a cost."

"That don't stop him charging me heaps more does it...and I gotta pay more friggin taxes so he can get to deduct the interest"

"So it's just the two reasons then?"

"Me sister aint got no savings left either cos she went and borrowed heaps to buy a pile that aint much better than a shed...her interest costs are up the bleeding wall...and she aint allowed to get no bloody deduction is she?"

"Just the three then?"

"You want a smack in the gob don't you?"

LOL spot on. the game as it really is

Thats little parody is gold Wolly.

Reminds me of the minimum wage argument. What happens to the McDonalds worker on the minimum wage who buys maccas of breakfast, lunch and dinner. He calls for the minimum wage to increase to $15, but the price of Big Macs has to increase due to higher labour costs. So he is no better off.

Try telling that one to Sue Bradford though!!

Try telling that one to most people! They just don't get 'inflation'. Particularly how bad 'wage inflation' is even though it sounds great. Or house price inflation for that matter and how that effects the cost of living.

Have you an alternative you would like considered Sore L....?because I tell you people are ready.........some are.

Some meaningful politics would begin with redefining Social Welfare....an ideology clung to by the long term stupid and those who would curry their favor......

It truly is out of control...................it lives.

Guys , all your problems will soon be solved , with the formation of a new political party ................. headed by Sue Bradford & Hone Harawira ....

........ Yippppppppppeeeeeeeeeeeeeeeeee ! .................... .... Yipppeee ? .......

...... Bugger !

Oh man, I can actually see that happening.. but not this year as they would be too late

What the heck has the Maori party in common with the Nats ? The coalition never worked properly. The party looks just after money - Harawira after the people - plus. I actually like that guy, representing he’s people. Brownlee, Joyce what a bunch of …….

...... the Maori Party were merely JK's " Plan B ", to go to , if cousin Rodney decided to ACT up . .......... JK was shrewd , don't let the tail wag the dog .

Hope your health issue gets resolved ok Sore Loser. I enjoy your posts.

Hope all goes well and you resolve the Health issues SoreL....it seems at this stage contempt is not enough ....and the tit suckers will hold the balance of power as long as it's there to suckle.

Good luck SL.

Sore Loser : Keep us posted on how it goes .

......You've elevated ranting to LEVELS THAT REALLY GET BERNARD HICKEY ANNOYED !

Well done , buddy . Best wishes from the GUMMSTER .

Justice, you are on to it my friend, as you rightly indicate, what needs to be done is to slap big taxes on everyone who has obviously made too much and reduce all to the lowest common denominator, then we will have equality like in Cuba. And we(at least those still in NZ) will all live happily ever after knowing that we haven't allowed anyone to get a bit ahead of everyone else. Utopia!

If your utopia includes a few people trappling over the many to own the most homes via government loopholes, corruption and loose credit then yes I will take Cuba any day. Owning more property does not make the country richer nor the owner smarter so why encourage it? All wealth transfers must be reset The last decade was a horrendous wealth transfer to the parasitic stupid. Party is over Muzza

People can own multiple property if the choose but not without paying their fair share of taxes including on CG's. The fact is capital gains are just as bad as inflation, the two are connected and kill the economy in very similar ways.

Actually I was thinking more about the mum and dad investors who own a few properties and have made a bit of an effort to get ahead and to have something when they retire from their business. But, never mind comrade, you keep striving to level everyone down a few pegs and support the Greens and/or Hone H, who are the real reds these days.

Sorry, I'm a CIBR's man. No political party membership. The people you speak of are very very few in number. Infact most will not retire or have a business to retire from IF we don't do something about the problem Muzza. Can you not see that? You can call me "comrade" all you like but the simple fact is even Cuba have a better healthcare system than us. Doctors still make regular household visits at no cost to their citizens and they get paid diddly also but ........they know they never entered medicine to get rich in the first place . It's called having a sense of "community" (interesting word that) or "tribe mentality". You look after the tribe and THEY will look after you right till death. I'm no fan of Castro mind you. Just the people of Cuba

Totally agree that people should not be made to feel wicked and punished for making a bit of an effort to get ahead and have something when they retire. On the contrary, that is an attitude which should be celebrated and encouraged.

The problem is that the present tax system ensures that the best way they can do that, is to buy houses rather than invest in something which will help to deliver national economic growth, such as an export industry; so that there is a contradiction between individual and public interest. It's not the individual's fault if they respond to that by choosing the path that is in their interest rather than the national interest. It is the Government's job to ensure that individuals pursuing their own interest also promote the public interest. Treating savings and productive investment more favourably than purchasing on credit and unproductive investment would do that.

Muzza - "a bit of an effort to get ahead"

Of what?

Seems to me, you don't understand the real world. It's finite, and your 'ahead' just means less available for those who follow.

But I guess you're one of the linear brigade?

Growth can go on forever, exponential no problem? 3 times the people on the planet soon, than when I was born, all wanting to 'have something'. (your words)

Yeah right.

Sooner (rather than later) it had to hit the wall - all exponential growth does.

There's not enough something left.

The old 'left' want everyone to have a share, but (listen to Sue Bradford on Nine-to-Noon the other day) don't acknowledge limits.

The old 'right' want to have the majority share, and mostly don't accept limits (some will, and will be playing accordingly - their problem is that storing 'wealth' as '1's and '0's in bank computers, may be of little use where we are going.

Both are operating in an obsolete mind-set.

Powerdown, I thought I lived in the real world, but must admit nothing is so clear anymore since I saw the Matrix

"The Combined Trade Unions says that the increase of 1.7% in wages for last year falls far short of price increases of 4%. Figures out today from Statistics New Zealand showed salary and wage rates, which include overtime, grew 1.7% percent in the year .."tvnz

The currency was debased a good 3%...so wages actually fell by more than 1.3%!

This year the debasement will be over 5%...whether Bollard reads it into inflation or not.

Savings 'working' group. hmmmm did they actually do any (work) between sauage rolls and coffee?

Does it really matter? The govt had ruled out a number of ideas before they even got started. An interest.co.nz Working Group would probably come up with a better set of ideas but again, what would be the point if this (or any) govt doesn't have the stomach to implement changes anyway? These various working groups feel like they are a waste of tax money.

Oh but they will have the stomach for something rest assured and it won't be pretty. These group sessions are really sly. It about preloading public opinion so they can do some more drastic moves. National have always used this ploy. Get a socalled independent group of 'experts' (yeah right) look at the problem and rule out the REAL needed measures to address the problem (CGT, LT, property bubbles fuelled by idiot reserve bank governors) so they have to focus on OTHER alternatives that are really more in line with their own political side of thinking so as to keep power next election.

That sums it up I think

National cant wait to put a few band aids over a massive festering wound in hope that it goes away. Beats actually treating the cause of the problem.

You hit the bullsey ..you can bet in three years when we are in deeper doo doo..it will be 20% gst.and a cut in personal income tax..that of course wont be quite enough to offset the drop in the standard of living.Untill we stop chasing our tails this same ole same ole will keep churning out from the Beehive why?..because they have very little in their creative thinking to do any better...and of course any real change might upset the gravy train..."Anticipate and prepare?" Or "Wait till the storm hits?"...I expect the fall in our standard of living to speed up from now on.As oil gets more expensive.And Electricity costs get ramped up.

Yeap, I'm even starting to think they are using the most hated GST rise idea as "the ploy" to push more people into the KS 'benefit scheme. Force people into private company fee based savings plans would suit National would it not?

As usual we are being played

Suasage rolls and coffee, more like champagne and caviar on their daily rates.

No different to the property rort, consulting to the govt is a rort on the taxpayer, never have so many consultants achieved so little, well on parwith the rest of the cosulting communuity, who have a superior sense of infalability at our cost.

Suasage rolls and coffee, more like champagne and caviar on their daily rates.

No different to the property rort, consulting to the govt is a rort on the taxpayer, never have so many consultants achieved so little, well on parwith the rest of the cosulting communuity, who have a superior sense of infalability at our cost.

I side with John Armstrong at the Herald on this report...the recommendations are timid...it's as if they watered it down to not upset Bill English...the 2025 Taskforce received loads of criticism and they didn't want to go down the same path.

I forgot Mary Holm was on this group. No wonder KS was top of the agenda. She was hardly objective about it. She clearly has no idea where the government gets the $1000 dollar top up and other 'benefits" (no better word describes it) from in the first place or should i say "from which people"?

Today my now ex coworkers and I were laid off and I'm the only one of us not to be in Kiwisaver. Time will tell whether my decision was good or bad.

Yes, let us know. Sorry to hear you lost your job (if you liked it) ;-)

It sucked but paid well. Because I wasn't in KS I saved on my own so came out okay. But I'm not sure how many of my fellow workers saved at all besides their KS contribs. Most of them have a lot of debt and are pretty worried now.

they should be

........ tried milking cows ? ....... I've herd that it pays well , but sucks big time .......... Good luck , Simpleton .

Tax on international purchases of residential property & CGT on all second homes (investment properties and baches) before a raise in GST please.

'NZ at 'dire risk' of financial crisis'

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=10703400

"The report contained a recommendation to consider new regulations to vary the amount of capital banks must hold in reserve depending on economic conditions in order to help prevent unsustainable economic booms".

Wot, no "financial efficiency" objections .... c'mon, surely not.

"They included indexing savings tax rates to inflation and reducing the tax rate on portfolio investment entities like KiwiSaver schemes so they are up to 10 percentage points below savers' marginal tax rates."

Damn it, I'll have to read the whole report now. You never know there might be something else lurking around in there that makes sense, like:

" .... consider new regulations to vary the proportion of foreign capital banks use depending on economic conditions in order to help prevent unsustainable, dickhead situations like we fecking well got now, because people who have been employed to govern didn't because they believed price of debt would be sufficient to regulate/moderate credit growth and it wasn't. Surprise, surprise." (Dozy lot.)

Sigh.

Wake up. Kiwis..Seen what's happening in Egypt? Anyone see that coming? You put this kind of high-handed club man with a tie and defensive body language in charge of THINKING and you'll get what you deserve.

The days of preaching from the pulpit are over.

A great many of the popoulation are being disenfranchised by their inability to engage with the communications of the day. It's tempting, I know, to believe that what you read here is the general view. It is not. You're not hearing the general view. We are a fraction of the population, about to be surprised, sooner or later, by the majority we are screwing.

The youth in Egypt are sick of hearing the General's view , preaching from the pulpit ....... And they're sick of the grinding poverty ........ And that has what , to do with NZ ? .....

..... The only screwing going on in NZ is the property investment rort and government bail-outs , which are dicking the majority of tax-payers who are steady and responsible .

yeap agree Simpleton I have a kiwisaver and my wife has a retirement one at her work (dollar for dollar) hers she can take out whenever she wants after being in it 5 years (so we pump as much as we can into this, and put 4 % in kiwiwsaver). Problem people have with kwiwsaver, if you say lose your job (sorry about that) and have saved up 20-30-40-50k you still cant touch it if you really really need it without pulling your pants down and bending over.

Maybe they need to relax the rules around this a bit, as jobs are not for keeps nowadays, and it is always at the back of your mind that it may happen to you with Mortgage, Kids etc you can afford to have funds somewhere you cant touch as you may be out of work 6-12 months.

The UK is also calling for a report in to retirement savings.

But the problems are much deeper because to provide a decent income in retirement, individuals need to save around 15% of their gross earnings throughout their career (including employers’ contributions) and most families, even on incomes of £40,000 a year find that impossible to do. The cost of buying a home and providing for children leaves little or nothing left to save

I would imagine the 15% figure would also apply here?

http://www.citywire.co.uk/money/encouraging-retirement-saving-how-mcfal….

One of the strengths of the SWG report is how it lays out the facts plainly, including a strong emphasis on the risks of our present debt position (net foreign liabilities NFL of 85% of GDP) triggering a severe crisis. That aspect seems to be getting some attention in the media. Although I have only skimmed it so far I already learnt a few things:

1. That NZ essentially has no company tax - the "company tax" is more a withholding tax and that income is not taxed again when disbursed to owners. In all the debate last year about the company tax rate, somehow that crucial point was not emphasize. NZ and Australia are the only two countries in the world with this system. In other countries, companies pay tax (I think 28% in the US) and when profits are disbursed to owners, it is taxed again under income tax. No wonder we have so many companies.

2. That when Australia introduced compulsory super, the state pension became means tested and already only 55% of retired people receive the full pension. This is surely far more important to the future economic impact of the scheme than the debate over whether the compulsory super lead to genuinely new savings, the apsect normally emphasized by the media.

3. That our NFL deteriorated steadily over quite a long period, from 5% to 85% of GDP over 1973-1993. Perhaps suprisingly it has not deteriorated further since then, despite large current account deficits. Why is that? Would it be feasible to get back to 5% over the next 20 years?

4. That our wealth relative to income is very low by world standards. Presumably, if you include the nominal value of our houses, our wealth looks better. What are we supposed to do, borrow against our houses to make productive investments? Sure.

The SWG may well be right that we urgently need to save another 2-3% of GDP annually, but they don't estimate what each of their recommendations could contribute to this goal. What are we supposed to do, implement a few things, measure the savings change, then do some more if necessary?

To save more we must spend less. The report makes some recommendations on how to make saving more attractive, but (apart from the GST increase) not how to make spending less attractive. Actually, it is not the spending per se that is a problem, but nonproductive spending. Is that argument that a dollar saved (and hence spent in the meantime by someone else) will be used more productively than a dollar spent?

It is easy to work out that if you want to live off your nest egg in retirement, you should save about 20% of your income over your whole working life. Many pension schemes overseas do involve that level of savings. We have a long, long way to go.

Robert,

3. Essentially we have borrowed our GDP for the last 20 years. We have spent and consumed more than we have sold for a long time. The recent return to trade balance/surplus is great and due entirely to record commodity prices.

However to repay that debt we would need the currency to be about 20% lower for a good 10 years or so. That's a very rough number but that would lift exports and reduce imports by enough to pay down that debt. Then we simply live within a balanced budget. Easy!

Let's ge the blame out of the way: everyone from the RB, Treasury, Politicians, Bankers and Borrowers are to blame.

I've done this exercise with many people through my work as a budget service advisor. When people have accumulated a lot of debt there are usually only 2 options: pay it back slowly over time whilst maintaining a sound budget or declare personal insolvency or bankruptcy. The latter means you will not get credit again but for some the former is impossible.

So we need to split that into two:

1. Spend less and leave some for repayment. This means the economy will contract as consumption reduces. Many business owners (especially in retail and hospitality) will already be seeing this. This will in turn cause businesses to crash and unemployment to rise. The private sector cannot create new jobs in this area and demand falls. New jobs can only come from the export sector.

2. We must lower our currency to rebalance the current account deficit. There is only so much we can cut from the import (consumption) side just as we still have to pay our mortgage/rent, food, power and other bills.

In a nutshell that is what we need to do. As for saving? Well how can we save when we are hugely in debt? We cannot. Or should I say that some can and others cannot. In essence, saving is really the repayment of debt as opposed to the reduction of consumption.

All the shuffling around is not going to help the big picture.

If you want people to stop spending then raise GST, cut tax on all savings but be prepared for the economy to contract as you start the big debt paydown.

We must lower our currency to rebalance the current account deficit.

Indeed. Would be interested to hear your opinion on how to achieve that and on why our currency remains stubbornly high given our deteriorating fundamentals.