Treasury is forecasting near-term growth to be less negative than it thought when it released its last set of forecasts at the May Budget.

This is in part due to the country moving down Covid-19 alert levels faster than expected.

But looking to the medium-term, Treasury saw the economy taking longer to recover, as the effects of Covid-19 are expected to be more persistent and take a larger toll globally.

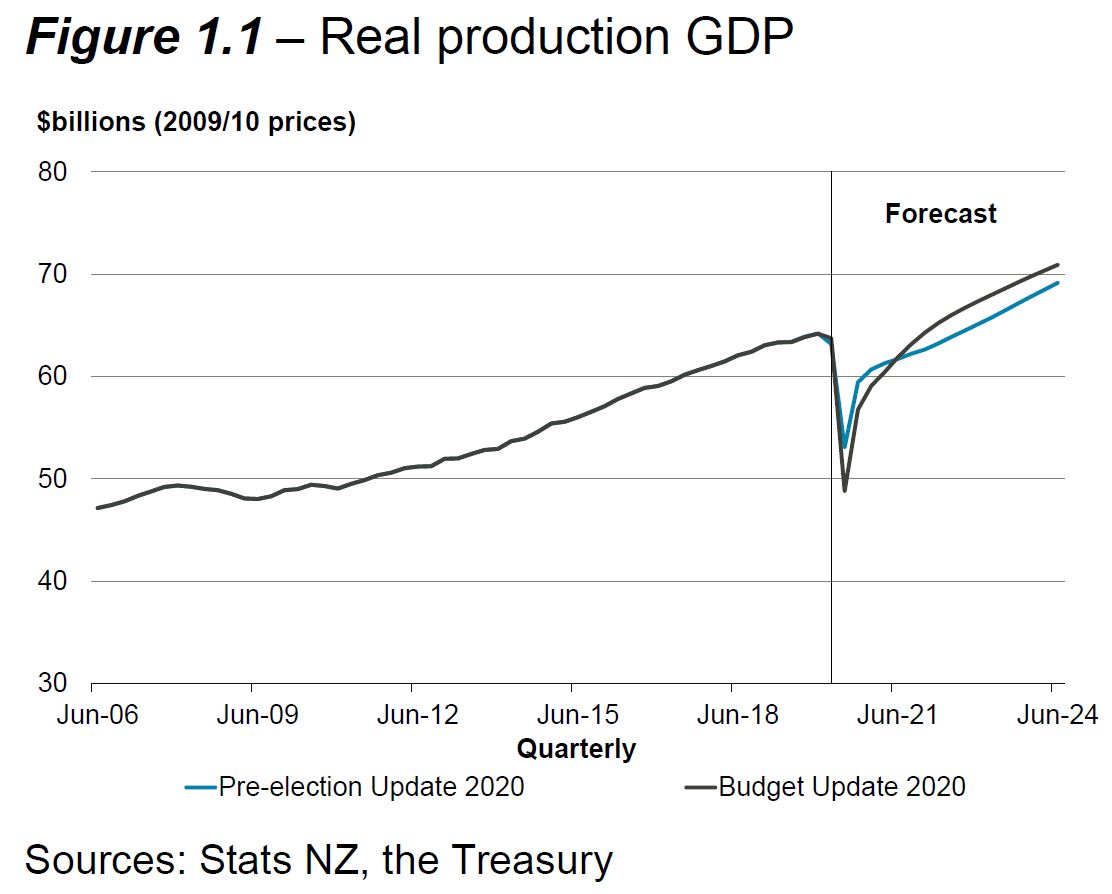

Treasury, in its Pre-election Economic and Fiscal Update (PREFU) released on Wednesday, forecast the economy contracting by -16.0% in the June quarter.

While this by far exceeds previous records, it’s an improvement from the -23.5% contraction forecast at the May Budget.

But looking ahead, Treasury saw annual growth averaging at 2.8% over its forecast period out to 2024, compared to 3.9% in March.

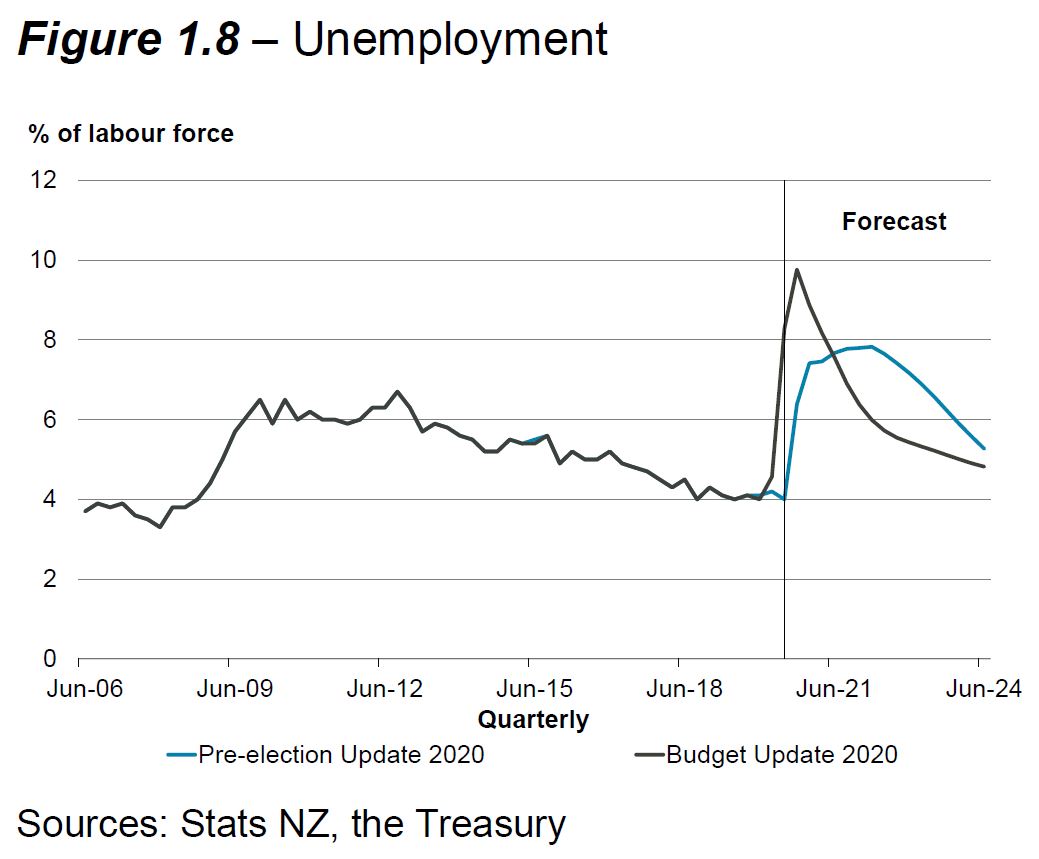

It saw the unemployment rate peaking at 7.8% in the March 2022 quarter. This is a lower peak, and one that comes later, than the peak of 9.8% forecast, in the Budget, to hit in the September 2020 quarter.

“Government support, and a faster move to lower alert levels, has helped to cushion the initial impact on unemployment. However, unemployment is expected to rise over the coming quarters as border restrictions weigh on activity and fiscal support is eased,” Treasury said.

"Even when borders are reopened fully in early 2022, demand for labour remains subdued, particularly if travel behaviours and preferences change in the aftermath of the pandemic. The persistent effects of the COVID-19 pandemic are expected to lead to a degree of economic scarring, leading to structurally higher unemployment."

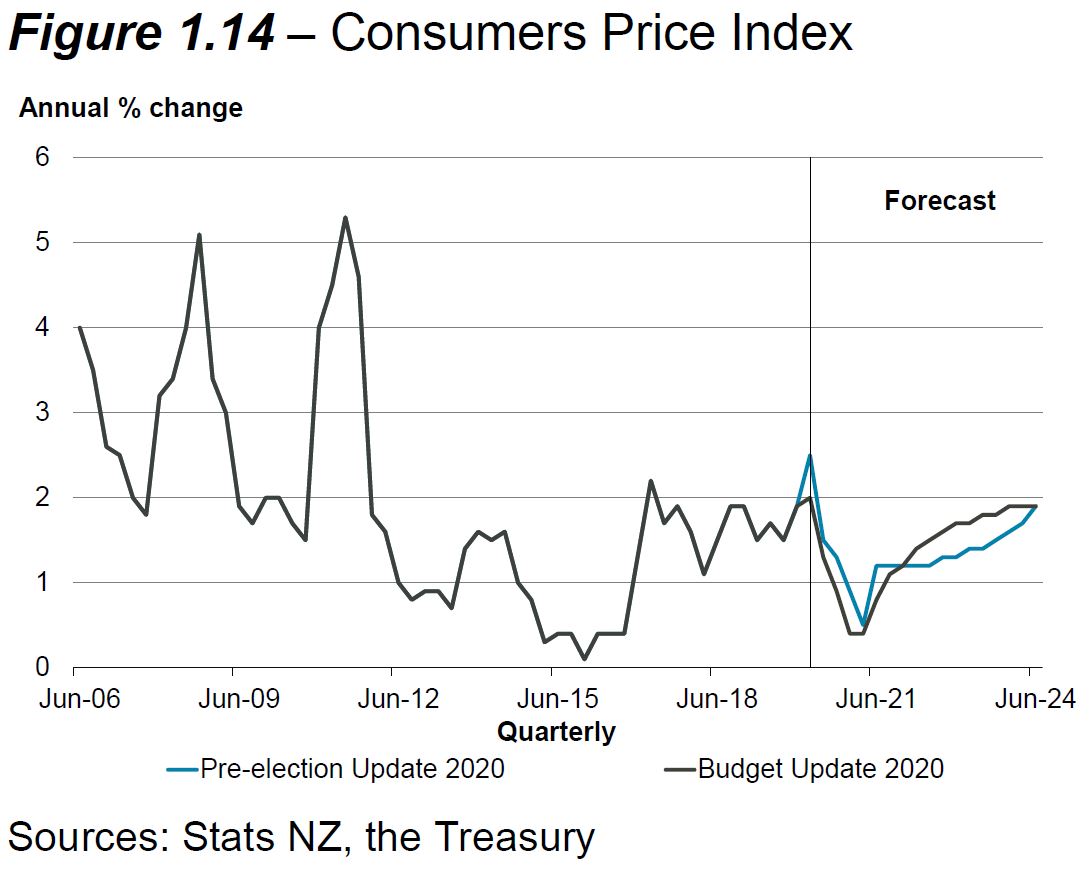

“A slower domestic recovery in the medium term, together with weaker commodity prices and a higher exchange rate, is expected to result in lower inflation compared to the Budget Update over much of the forecast period,” Treasury said.

However it said the Reserve Bank’s accommodative monetary policy (cutting of the Official Cash Rate and quantitative easing) would see annual inflation rise to 1.9% by 2024, hitting the midpoint of the Reserve Bank’s target.

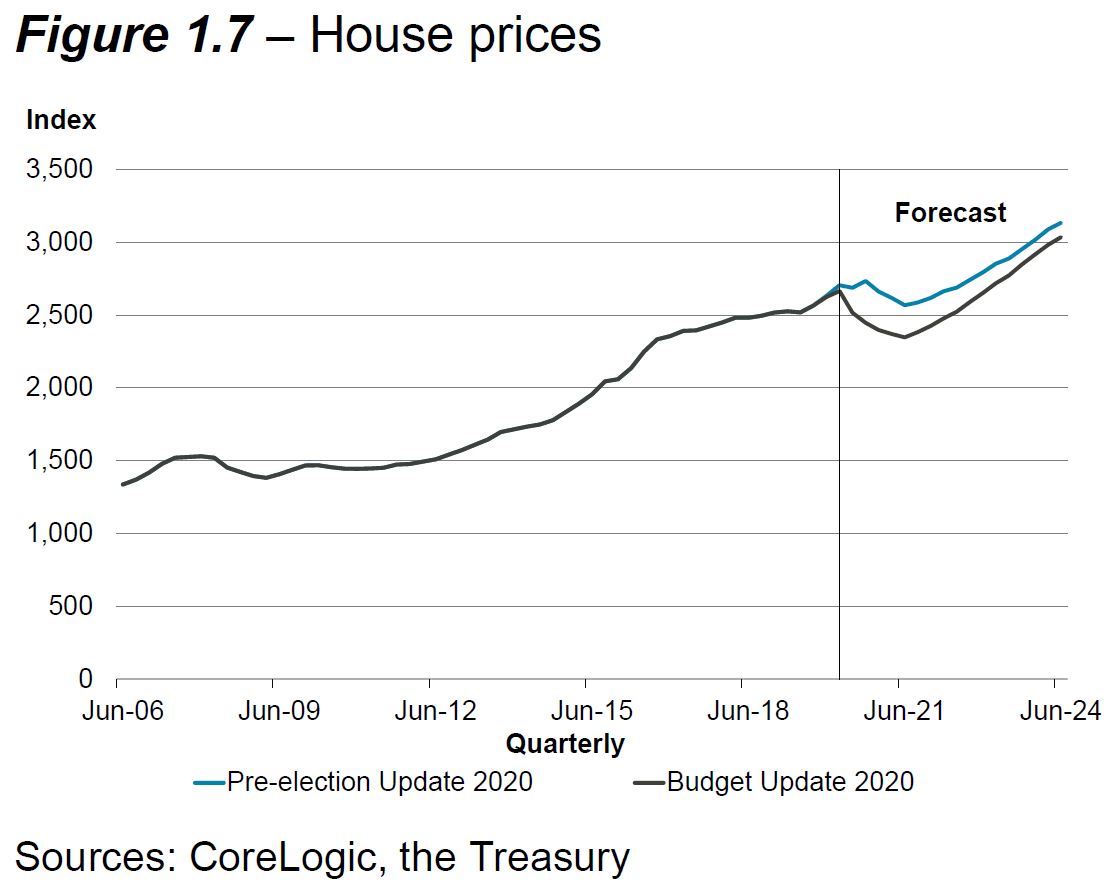

Treasury recognised the role of rising house prices in “supporting” the economic recovery.

“We forecast a period of weaker house prices over the year to June 2021, with prices falling -5.1% from their March 2020 levels, dampening consumption growth,” Treasury said.

“House prices then recover as net-migration rises, economic confidence recovers and monetary policy remains accommodative throughout the forecast period.”

Treasury said that “given the recent resilience in the housing market, there are upside risks to our forecasts if current sentiment is maintained”.

Importantly, the Secretary of the Treasury, Caralee McLiesh said there was “profound uncertainty” around Treasury’s forecasts.

Treasury made a number of assumptions, including one that following a period of New Zealand being at Covid-19 alert levels 2 and 3 in the September quarter, the country would stay at Level 1 all through 2021.

It assumed border restrictions would be lifted on January 1, 2022 - nine months later than forecast at the Budget. Finance Minister Grant Robertson said he hoped they’d be lifted sooner.

Impact on the Government’s books

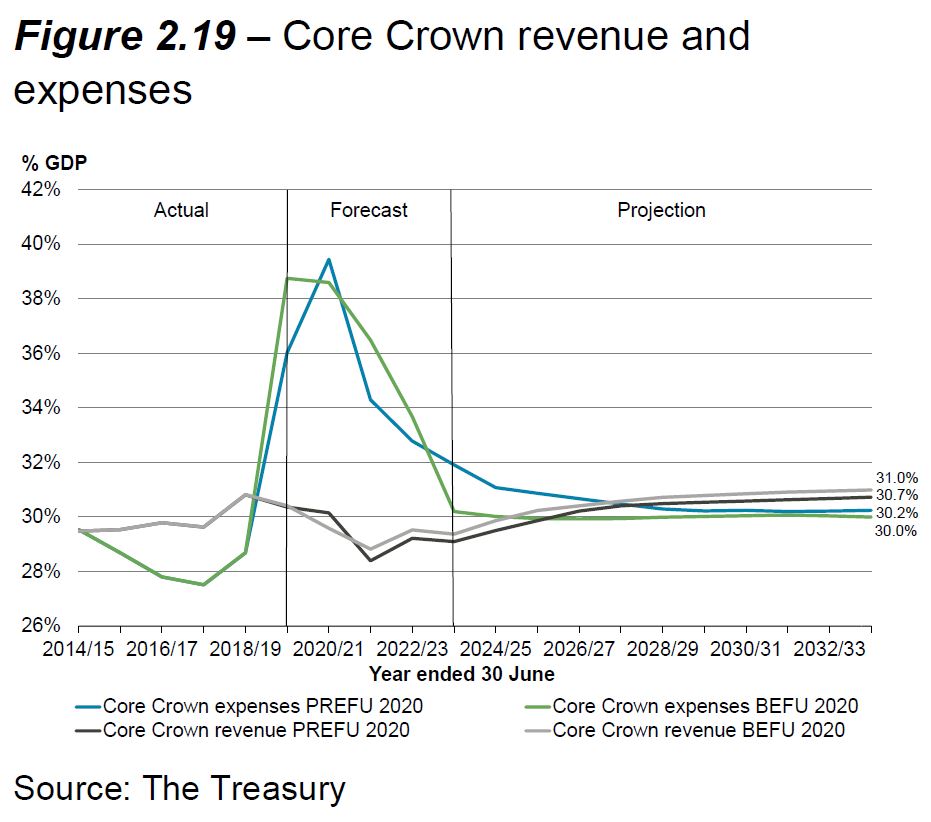

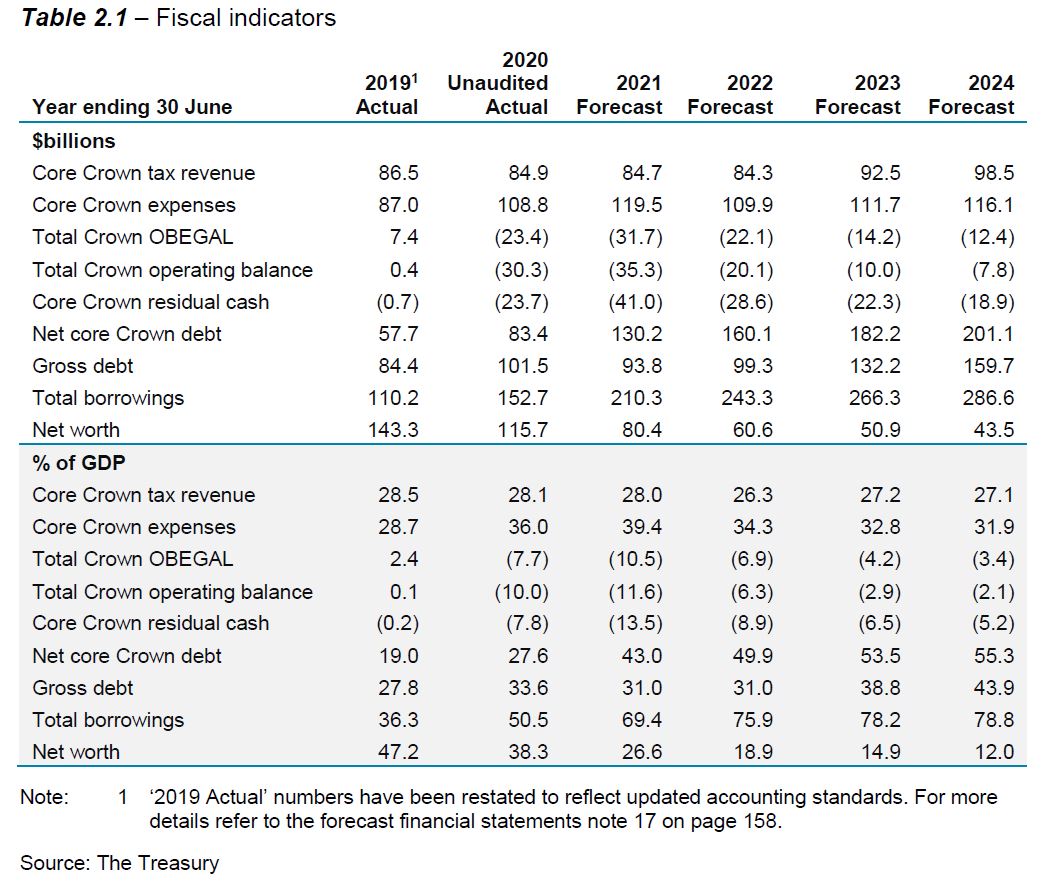

Turning now to the impact on the Government’s books, lower GDP growth in the medium term is expected to result in a lower tax take.

Tax revenue is expected to continue to fall in 2021 and 2022, but this drop is lower than forecast at the Budget.

In 2022, 2023 and 2024, tax revenue is expected to be lower than that forecast at the Budget.

Core Crown expenses increased significantly in 2020, as the Government launched a number of schemes to cushion the blow of Covid-19.

Treasury expected expenses to continue to increase in 2021, reaching $119.5 billion, before falling away as the Government’s support measures wind down.

Treasury forecast the size of the Government’s Covid-19 response shrinking in size a little from $62.1 billion to $58.1 billion, as the uptake of the likes of the wage subsidy, Small Business Cashflow Loan Scheme and Business Finance Guarantee Scheme have been slightly lower than expected.

Of this $58.1 billion, $14.1 billion is yet to be allocated. Robertson said he would only spend that money if he “absolutely” had to.

He stressed he would continue to take a “cautious” approach towards managing the books.

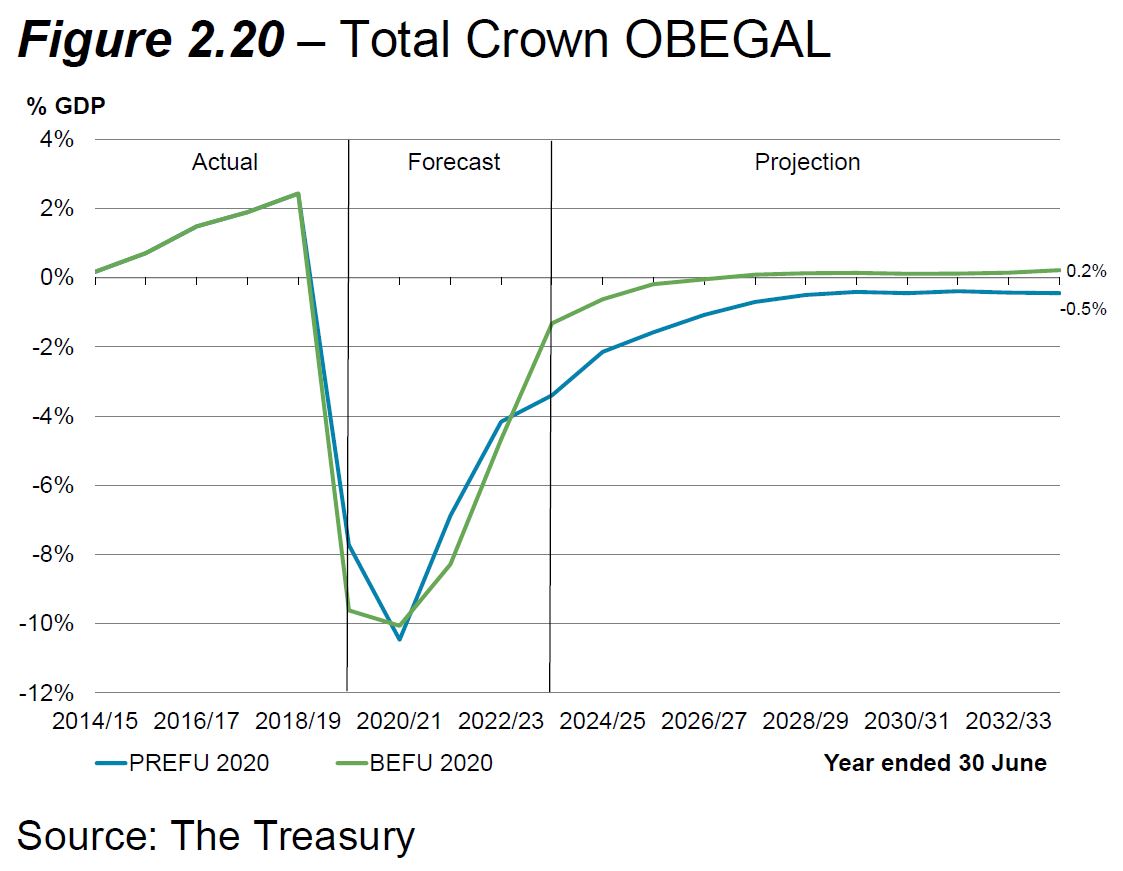

Turning now to how this affects the Budget deficit, this is expected to peak at $31.7 billion in 2021 - a higher peak than forecast at the Budget.

By 2024, the deficit is also expected to be higher at $12.4 billion - a worse position than the $4.9 billion forecast at the Budget.

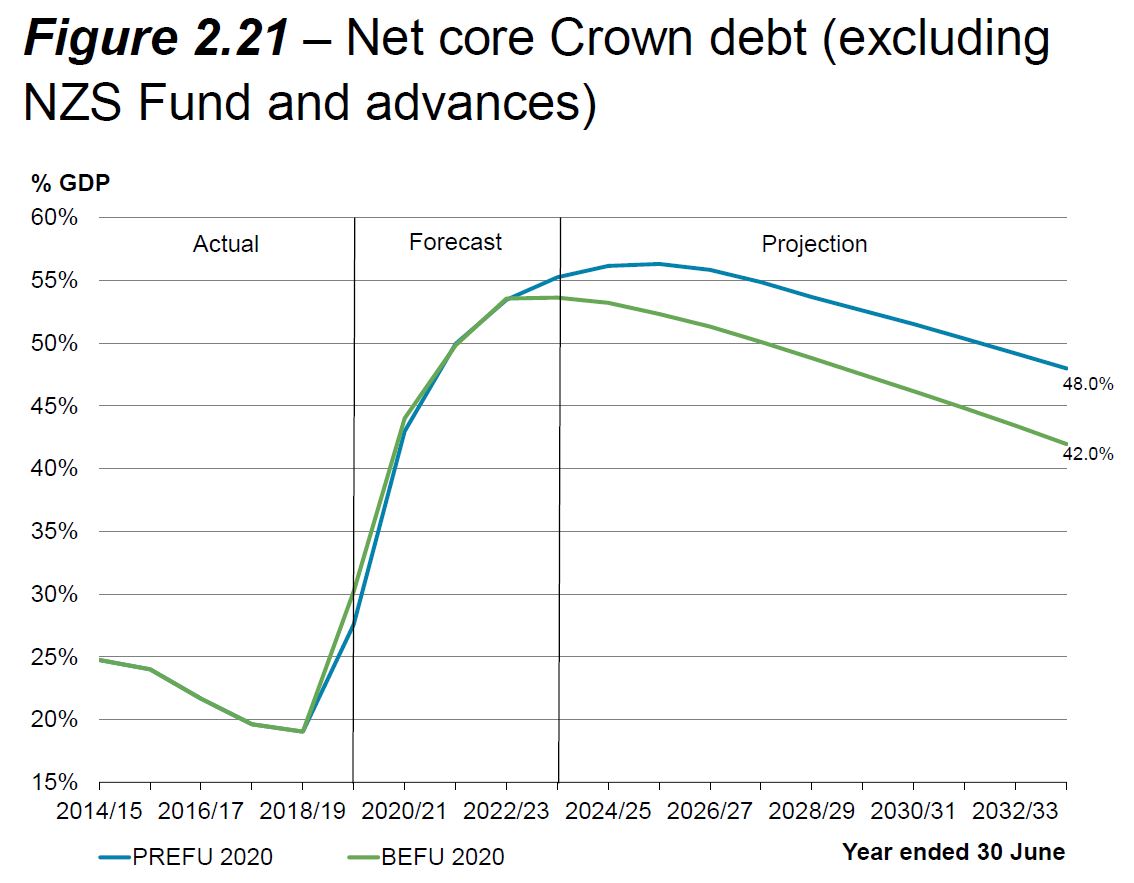

All this means net core Crown debt as a percentage of GDP is forecast to be higher come 2024, than forecast at the Budget.

It’s forecast to track up from 27.6% in 2020 to 55.3% by 2024.

From there, Treasury projects it tracking downward slower than previously forecast.

128 Comments

It’s confirmed, housing is going to save us.

And immigration - "House prices then recover as net-migration rises". Sadly this Govt seems happy to maintain the current low-productivity ponzi-scheme economy.

It strikes me that there's another genre of house buyer; namely those who buy/accumulate houses not to live in themselves, nor as a particular investment........

Instead they see property more as a status symbol; a signal to society that they're successful and wealthy. And they're not inclined to sell their much-prized status cheaply.

What I'm getting at here is that the accumulation of houses/property seems to have become an entrenched form of "conspicuous expenditure" in New Zealand - for the well-heeled who like to flaunt their tangible assets.

Frankly, I view conspicuous expenditure as a form of vulgarity....... indulged in by shallow people with small minds....... in order to impress other shallow people with similarly small minds.

TTP

That comment is like a drug dealer telling people that taking drugs is really bad !

Talk about Bipolar?

Nurse got the meds mixed up?

Hi Chairman Motor Moa,

I'm sure you'd be boasting about "My property portfolio......" if you had the wherewithal to build one......

TTP

Yeah, mine bigger than yours!

You could well be correct. "conspicuous expenditure" certainly seems to have taken hold in NZ in the last couple of decades. Last century wealthy NZers by and large didn't flaunt their wealth as is becoming increasingly common - they drove relatively plain cars and lived in relatively plain houses. Functionality was preferred to ostentatiousness.

Treasury is expecting net migration to reach 35k by June 2024. It won't be the worst thing if we restrict entry to genuine skill shortage areas in high-value sectors bringing in less than half the Key-era migration levels.

Also, wouldn't it be better if we used migration to grow both the economy and productivity by 1) focusing on bringing the right skill-mix this time around, and 2) making the big-ticket public investments we're seeing in infrastructure and workforce upskilling an ongoing commitment and not just a Covid recovery plan.

Correct - it's not just at lower levels either. There's a bunch of white collar professions on the regional skill shortage lists (think accountants) that probably need reconsidering, given we still have universities in main centres pumping out new accountants.

I am rooting for more business tax automation and Xero's R&D to cleanse our regions of bean-counters and pencil-pushers in the foreseeable future.

Unfortunately, that profession won't be taken off the regional shortage list since the most-popular accounting master programme brings upwards of 50k to universities in tuition fees per intake.

When a housing crisis is the "bright spot" we know we're in for a great time. We need a capital gains subsidy on houses to save the economy!

Amazing they are proud of their 'Bright Spot' when they were elected on the back of the promise of affordable housing

Phonies.

Labours new war on the poor.

Yep but they wont see it and still they will vote them in, and still moan about the house prices going up whilst they lose their jobs.

Be interesting to see the hypothetical point where the poor actually wake up to the daylight robbery inflicted upon them by the full (viable) spectrum of the NZ political class and the RBNZ.

Pretty clear the whole political spectrum won't touch it. No way are National about to tax second homes, build heaps or call for LVR restrictions.

Well, who gives them an alternative that is not worse? Only TOP, perhaps.

It's unfortunate it's so hard to get them in the televised debate, given the valuable perspective they bring.

I do wonder why TOP are not making more noise. Housing dominated the last election, the inequality has gotten worse since and not a peep.

Do themath, do not be surprised if capital gain is followed by mortagee defferal to stimulus the housing market.

This is going to be interesting.

Australias economy is the opposite. Its recovering better than anticipated, bar housing.

How two countries so intertwined and so close together can have opposing fundamentals, yet both come out the other side is beyond me.

Agreed, really interesting to see how this plays out

Indeed

Economy in Western Australia is booming due to the price of iron and other metal raw materials.

An IT guy at my work left for WA for another IT job in a mining company , he earning 3 times more than his previous job.

Cases like these remind me of what my econ professor at uni said about the Aussie economy: despite having a good combination of skills, knowledge (think top-ranked universities) and financial capital, it punches well-below its weight because it lacks proper deployment of all those strengths.

A great example is the role Aussie plays in the global lithium supply chain. The lithium ore exported by Aussie companies (most with significant foreign ownership) makes up 0.53% of the value of a finished EV battery with the remaining going to downstream players elsewhere. The opportunity to multiply proceeds attracted lots of press and numerous business cases from multiple public agencies and private investors but hardly resulted in action.

"Holes and Houses" are how thinking Aussies describe their economy. Many of those high paying jobs have been lost to automation and it's definitely not the economic miracle many think it is. Water security is becoming a major factor and it has a bloated state sector. Like Ireland, it's GDP per capita is overstated.

The new high paying jobs now aren't in the mine pits, they are IT jobs in setting up and maintaining automation system.Resource planning is another area (know when to dig, how much to dig and when not to dig)

"When not to dig" being another term for controlling supply and demand, thus price? Even mining can be "seasonal work".

WA IT job ads cap out at about 120/hr or 220k/yr, similar to NZ.

IT jobs in nz went off a cliff day1 of lock down and very very slow to recover. I know a lot of people who are looking. It's really bad in NZ right now for IT roles.

We'll have to disagree on that one. Maybe it depends on the role but from where I'm looking there are plenty of good opportunities at the moment.

There is a growing list of job postings for IT workers with experience in critical areas such as network, architecture, database, etc. Those missing out are new entrants, recent migrants and junior-level service workers.

Opposite experience here. From lockdown we have been outrageously busy with customers adjusting to remote working, and picking up lots of new business.

that is down the WA premier, under the new rules rio tinto and BHP require you to reside in WA, no more fly in fly out to other states.

some states are using borders and covid free status to their advantage, pity our government has not thought of that

"it emerges BHP and Rio Tinto have heeded the State Government’s calls to favour local workers or stipulate interstate employees must move to WA."

Australias economy is the opposite. Its recovering better than anticipated, bar housing.

Be careful with the propaganda from the RBA.

The RBA can be trusted much more than the real estate lobbied RBNZ.

Agreed,martin north from the dfa channel covers some of the shenaghns from rba and other institution s quite well,time will tell.

Well that's easy to see actually, given the stark differences in both central government and central bank responses.

We locked everything down and fired up the debt engine -> result is more debt and bigger economic shock in order to save lives. RBNZ QE = $100billion.

They slowed some things down but never locked down fully across the country and have only experienced strict lockdowns where ze virus has gotten out of control - e.g Melbourne. RBA QE = $30billion.

Australia's economy is ~7 times larger than ours. When we also give the markets 3.3x the stimulus in absolute terms, in relative terms that's a sugar hit 23 times as large!!!

So it's no wonder debt-fueled assets like housing have shot up here and have decreased there. And given their central government didn't dampen economic activity as much it's no wonder their real economy is doing better as well.

They also have a capital gains tax on property which places some downwards pressure on 'housing investment for capital gains' strategies

So it's no wonder debt-fueled assets like housing have shot up here and have decreased there. And given their central government didn't dampen economic activity as much it's no wonder their real economy is doing better as well.

Don't be so sure about that. The real damage to the Aussie economy is among the SMEs (F&B, construction, basic services) and I don't think you can measure the real impacts yet. Also, the sheer scale of the Aussie public sector is mind boggling with people working for district, city, state and federal organizations. Many people employed on reasonable incomes while doing SFA and little accountability (except the cops, military, teachers, and frontline health workers).

Don't forget the Aussie's gargantuan dirt exporting sector that is seeing record high prices and volumes. The sector brought in over AU $230 billion a year in royalties and corporate tax to various levels of governments last year plus the several tens of billions in GST and personal taxes.

More people losing their jobs in the broader economy across the ditch are picking up shovels and heading to the mines. ABC has been doing success stories on lecturers and civil engineers finding their calling in the outback. This may bring quicker recovery but ruins their long-term productivity and national security plan with greater economic dependency on China and commodity prices.

Such a lazy and flawed comment, you should have saved your time. RBNZ's QE is $100b by June 22 if needed and we aren't anywhere close to that currently. The RBA has bought $156bn of bonds so far and will continue to buy. The RBA is also lending directly to banks via it's TFF program which I believe is up to $250bn by 2021 (the RBNZ hasn't launched this yet).

The RBA has bought $156bn of bonds so far and will continue to buy.

Is this the data source?

No, that's the result for a single operation. https://www.rba.gov.au/statistics/tables/ Go to the excel sheet A3.1

Actually, my numbers were wrong, see if you can spot it!

Check your facts before impugning others.

err, they were all facts except the one error which i fessed up to

As my old professor said it's the exceptions we are interested in - we were trying to create valid sampling routines to create statistical models of hearing.

I guess it all depends on banks continuing to lend same multiples in NZ. I wonder if they're pulling back in Aus yet.

I guess it all depends on banks continuing to lend same multiples in NZ.

NZ has always been a cash cow for the Aussie banks. Because they're somewhat removed from any public accountability, they've been able to get away with whatever they like. The NZ govt, RBNZ, media, and public have been generally too docile to recognize it.

we know where the bright minds are going to move to soon

We're already here mate!

well if OZ do what they say they are to drag them out of this, then I suspect tickets to OZ will be in hot demand once the borders open back up. Meanwhile in little old NZ you can buy a house at 10 times your income, but no worries the interest rate will be really low, which may help you if you have no job.

Have owned investment properties in both countries. The differences in the behaviour of the 2 housing markets is not surprising. There are systematic differences to real estate investment between the 2 countries, such as differing tax treatment, including capital gains tax and stamp duty in Australia. These are significant costs to buying and selling and work to depress turnover and growth. Also a significantly more robust, employer funded superannuation system in Australia, so less reliance on property investment to fund retirement. New Zealand has experienced a greater drop in interest rates than Australia due to Covid, and so a proportionately greater stimulatory effect on prices. Housing shortages also more acute in NZ.

Good points. Their excellent super scheme could be quite a key factor.

Yip...get the immigration/ housing ponzi up and running again to save us.

I think the virus has exposed what a house of cards this economy really is.

A house of cards made of houses.

A house of cards made of houses that are built like cards

Forget about our GDP. Thanks to the record high in our housings, NZ self worth will surpass all old records. We are so rich, tomorrow we can buy another nation.

No need to be so dramatic Moa. They're simply referring to the power of the wealth effect. They explicitly state the relationship between house prices and consumption.

Which benefits the minority, that is house owners. It’s such a shortsighted and lazy approach to a recovery.

Which benefits the minority, that is house owners.

No. The dogma is that the wealth effect is supposed to support everyone. And I believe it. When bubble economics is running at full steam, everyone gets a piece of the pie (employment, revenue, higher margins), even if you don't have skin in the game. When people spend more than they earn; trade-up on cosnsumption; or spend on 'nice to have' products and services, it's good for the economy.

The dogma is pretty narrow, however. Higher productivity and more export income (coupled with affordable housing) would benefit more of society far more.

Higher productivity and more export income (coupled with affordable housing) would benefit more of society far more

Completely different issue.

Not unrelated. Treating property as a subsidised, risk-free investment does not encourage investment in productive business at all.

Wealth effect or wealth illusion?

The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax. Link

Great stuff Audaxes. The wealth effect does work until it doesn't. And ultimately it's an illusion.

The old trickle down economics...we still trying to beat that drum?!

You actually believe that?! Hey they have a position at the RBNZ open, you would fit right in.

J C,

Wow, I had heard rumours that believers in trickle-down economics still existed, but I doubted it-until now. And do you also believe that the earth is flat?

"Profound uncertainty."

Great little caveat or get-out-of-jail card slipped into the propaganda by the Treasury.

But I am fine with that. I think any forecasting needs such a caveat in such volatile times.

Don't know about you, but 'profound uncertainty' to me suggests that confidence in their own forecasts is extremely weak.

Yeah.

And I wouldn't be confident if I was them either. As usual, too optimistic. Consciously or unconsciously, instructed or not, they will be willing to please their current political masters...

good point. If uncertainty is profound, by definition you cannot forecast anything. By stating this, the Treasury should have refrained from giving a scenario, but should have published multiple scenarios and saying that they are unable to determine reliable likelihoods of which one will play out given the uncertain times we are living at present.

Yep agree, multiple scenarios

Housing bright spots Auckland Hamilton Tauranga Wellington and Christchurch lol

...but housing is our economy. Without asset price inflation we would have to face the facts on a range of issues from low productivity to poor infrastructure.

What happened to "Labour are going to make house prices more affordable?" Was it a blatant Lie?

Yes. Just like the Key government. Neither major party is at all serious about addressing the issue.

But only one promised 100k houses and affordability that the state could easily deliver on, and failed.

Deal with the planning related issues, RMA, intensification, and kiwis will have to accept over time that our 1/4 acre dream is just that, more likely to be an apartment near a transport hub.

They import a million new people without our permission. They don't build enough houses pushing prices up so our kids futures are ruined. They charge us more taxes to provide medical care, roading, housing etc to accomodate the extra people. Our public services are stretched to breaking point. Our lovely clean and clear beaches are now full of people and are litter strewn? Our clean waterways are no more. Our wages do not increase. In what way does the average kiwi benefit from government policies?

You need to start a political party.

Apex Andy......for PM. I will vote for you. I owned 3 stand alone houses in central Akld between 1994 and 2015 and I am still furious about what has/is happening!

Key promised affordability. And he promised RMA reform. All we got was relatively meaningless tinkering over 9 years.

Each major party is as bad as the other.

Instantly added 2.5% to the cost of building through GST increase. Saddled the country with an extra $50 billion in Government borrowing for an "Earthquake" which by the time you take out the insurance coverage only really cost the Government ~$14b. Wait a minute......What's the big Australian bank profits extrapolated over 10 years? $3b - $5b p.a.? $30b to $50b over 10 years? Where did John Key end up when he left Parliament?

But only one promised 100k houses and affordability that the state could easily deliver on, and failed.

Lol. I don't think it was really as 'easy' as you suggest it is.

A big part of the problem with Kiwibuild is that the government was deliberately giving the work to private developers. This ensured prices would never be "affordable" because those private developers required a profit margin, and the government didn't want to step in and build the houses at-cost because that would drive the private developers from the market. It seems the government were not serious about the up-front investment required to achieve truly affordable economies of scale through prefabrication of houses, or adapting the planning and inspection regime to allow prefabrication to become the primary method of building houses (ie, build entire walls with plumbing and electrical intact offsite and then slot into place with a crane).

The government also seems too scared to do anything about the building materials monopoly and associated BRANZ red-tape that we have in NZ which (mostly needlessly) drives up prices.

Good to see Treasury acknowledging the 'profound uncertainty' in their forecasts. Bank economists could learn a thing or two.

Fritz

Interesting Westpac +7%, Treasury -5% for housing next year.

My point isn't what their forecast is, it's whether they provide caveats. Treasury do (right approach), most of the banks don't (wrong approach). I thought Westpac were especially foolish in lurching in the opposite direction without a caveat.

And this is still putting a bright spin on it...

Have to stick with the naritive that it isn't all doom and gloom to keep the masses happy.

'We forecast a period of weaker house prices over the year to June 2021, with prices falling -5.1% from their March 2020 levels, dampening consumption growth,” Treasury said.'

From March have already gone up by 10% to 20% if not more so if they mean 5% from March level could be much higher from current level which ate much up from March Level.

Having said it seems doubtfull seeing how strong the housing market is.

'From March have already gone up by 10% to 20% if not more'

???????????????

I’m calling bullshit on those figures mate.

Market has gone up after lockdown and houses that were going in Eastern beach, Pakuranga area for 900000 near around are going for million plus or minimum high 900s, so has increased.

So is correct if treasury feels that houses will fall by 5% from March level than all the gain from March till now plus loss of 5% as predicted loss will be big.

This implies that all those buying house now will lose money as definitely if buying now is at a price which is much more than March price, as market is hot and being sellers market.

If we are still selling at March price than does it mean that market as of now is not booming ?

Feel many are still in denial mode that housing market despite lockdown and panademic has moved up and booming. Will be best if one accept the facts though in future may fall after all subsidies and stimulus ends but for now is hot and many houses are being sold at very high price - beating all earlier record.

so expensive housing is a "great problem to have" after all.

Robertson wouldn't be out of place in the centrist faction of the National Party.

Very conservative.

This is who Labour is supporting instead of poor kiwis. He took risks, but labour ensured he didn't really take any risks. He cannot lose under Jacinda?

"In a space of 6 years, Gary built a 14 property portfolio worth $10 million dollars"

“House prices then recover as net-migration rises, economic confidence recovers and monetary policy remains accommodative throughout the forecast period.”

New Zealand clearly has a problem of moral character in its political and central banking leadership.

Rather than living within our means and investing in education and innovation, it's all about inflating house prices, redistributing wealth upwards, and importing as many people as possible to prop things up.

Poor character. Complete disregard for the legacy we leave.

Can a country have moral character? I think that can only belong to individuals.

I referred to individuals.

But the character of those people in power to a significant extent mirrors that of the nation as we keep voting them in. And more than 85% of people who vote, vote for either of the two major parties, who demonstrate similar characteristics.

I guess that's the crux of the moral problem eh. We've long since ceased saying "what about the legacy we leave?" and replaced it "won't somebody please think of us ma and pa investors?"

Personal responsibility fell by the wayside. Extraction from others comes first.

Oh yes, sorry I was speed reading. Probably not possible for it to be any other way considering history and circumstances though.

It can have a religion, so why not?

What’s religion got to do with morals?

Many people's religion is in fact their morality - it dictates what they distinguish as right or wrong

I just watched an auction for a two bedroom unit that had a pre-auction offer of 1.1M. It sold at the auction for 1.35M, going up by $500 at times, it took a long time. Last year I would have thought it would sell for around 1M so taimaiakka0 may be right about how much things are going up.

https://www.barfoot.co.nz/property/residential/auckland-city/epsom/unit…

Forecast of GDP is a joke

GDP been falling in growth terms, for 3 years. Yet magically it will go back above 2.7% for next two years after 2021. why? Productivity miracle or more people imports?

GDP will grow after disasters. It is not as miraculous as you think.

broken windows fallacy

Why a fallacy? lets assume you have a farm that produces at maximums crop capacity of 100. in Year 2, you do some magic and produce 1 more unit, your GDP increases by 1%. NOw you have a a terrible year (year 3), frost, etc, you only produce 20. A drop of 80%. in year 4, you have a little bit better and produce 30. Still very terrible, but your production has increased by 50%. So when you base year drops drastically due to some external factors (natural disasters, pandemics, wars etc) you can expect growth in production if those events are passed.

Sorry, I mean the fallacy is the 'wow factor' of growth after the tragedy. It's growth, but only after a tragic event and drop in economic growth.

As you alluded to, it's quite easy to get growth after such an extreme event.

All those landlords who sold up a year or so ago thinking they were doing the smart thing sure have egg on their faces now. It's quite a tragedy.

Famous last words? Who knows Zachary.

I still expect a financial crash in 2021 or more probably 2022, that will bring the housing market down significantly.

But that's my best guess, which could easily be wrong.

So who knows at this point in time who has made the right or wrong calls.

Fritz their should be a correction in asset class both housing and stock and best guess is from November / December and if it starts worst will be in April when moratge holiday ends.

You might be right, or not.

I might be right, or not.

It's fun to try, but forecasting is a fool's game!

You could be right there Fritz

I'm just going to come out and say I was wrong about a property crash. What I did not factor in is how much the government was prepared to artificially prop up the housing market. I seriously expect the mortgage holidays to be extended, possibly indefinitely until the point the bank owns all of your house and at which point they will sell it from under you. This will still not cause a crash because the effect will be staggered and spread over decades depending on the equity you had to start with and by then immigration will just gobble up the bank sales. Nothing is going to change for future generations, this is not the new normal, its just the same old normal. The end game is the top 1% own everything and everyone else rents.

I agree. I underestimated our ability to keep reshuffling the deck chairs indefinitely rather than face any sudden shocks. I think the wage subsidies will be extended indefinitely (both here and overseas), likewise the mortgage deferrals. It won't just be zombie companies, it'll be a whole zombie economy.

So between now and next June (official) unemployment is going to double, CPI inflation is going to be virtually non-existent, real estate prices are going to fall yet GDP growth is going to leap into life.....right.

Heroic assumptions?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.