Real Estate Institute figures for May show the housing market continued to slow in May and prices continued falling from their peak as the implications of the budget and very weak lending growth dragged on the market. Bernard Hickey argues below that prices will fall 15% from the peak. We welcome your view in the comments below.

(Updated with ASB comment about a weak market being more suited to buyers than sellers, real house prices being down 11% from the peak, Harcourts expecting bounce in June, Housing report video with my view on house prices likely to fall 15% from peak, My view below that house prices will fall 15% from their peak, link to Housing Affordability charts)

However, the Real Estate Institute said the figures showed there was no real reduction in residential property prices and that the market retained its strength.

The volume of houses sold in May was 5,206, which was down 17.2% from 6,291 in May a year ago. (See an interactive chart below) It was also down from 5,207 in April. The median house price fell to NZ$350,000 in May from NZ$356,000 in April and is now down 2.7% from an all-time record high of NZ$360,000 in March this year.

The median number of days to sell a property also rose to 43 days in May from 40 days in April and is in line with the 42 seen in May last year. See the full data pack below.

The REINZ/RBNZ stratified house price index, which smoothes out the effects of more houses selling in one segment than another, shows prices fell 1.4% in May from April and are now down 5% from their peak in November 2007. After inflation of 6% over that period, real house prices are now down 11% from their peak. See the full release on the stratified index here and see the full REINZ spreadsheet here.

The Real Estate Institute (REINZ) said the market had retained its strength.

“It is good to see the market retain its strength and prices stay stable during a period when some buyers would have been concerned about potential tax and interest rate changes,” said REINZ President Peter McDonald.

“It is good to see the market retain its strength and prices stay stable during a period when some buyers would have been concerned about potential tax and interest rate changes,” said REINZ President Peter McDonald.

“With tax changes and interest rates now settled, property investors are already talking about returning to the market to cater for the growing demand for domestic rentals,” McDonald said.

“While there has been some decline in turnover from the boom times of a couple years ago, during the past year nearly 67,000 homes were sold for a total of almost $27.5 billion so the real estate market is still very healthy."

ASB economist Jane Turner said the housing market remained very subdued because of uncertainty over tax changes in the budget and the prospect of interest rate increases.

"The median number of days to sell lifted to 42 days and is now just slightly above average levels, suggesting the balance is tipping in favour of buyers," Turner said.

"The changes to tax policy announced by the Government in May do reduce some of the attractiveness of owning rental properties. However, we do not expect this to translate into a landslide of sellers," she said, warning however that listings were likely to increase as workers left to live in Australia.

"New listings are currently at very low levels, and we expect to see a lift in listings reflecting the increase in permanent departures to Australia already evident in the net migration data, as well as a small increase in investment property listings," she said.

"The fundamentals for the housing market remain fairly weak over the next year. Along with the tax policy changes, rising interest rates and slowing net migration are also likely to reduce demand for housing. As a result, we expect the housing market to remain in favour of buyers over the second half of this year."

Meanwhile, Harcourts' Australasian head Bryan Thomson said anecdotal feedback in June showed a more normal level of activity after a weak May where sales volumes were down in four of Harcourts' five regions.

“Only our Northern region figures seem to defy the trend, however significant growth by our group in this region means our statistics reflect Harcourts’ offices achieving a bigger share of a smaller market, rather than this area bucking the national trend,” Thomson said, adding the inaction was caused by pre-Budget uncertainty in the minds of both buyers and sellers.

“Only our Northern region figures seem to defy the trend, however significant growth by our group in this region means our statistics reflect Harcourts’ offices achieving a bigger share of a smaller market, rather than this area bucking the national trend,” Thomson said, adding the inaction was caused by pre-Budget uncertainty in the minds of both buyers and sellers.

“Now the Budget is fact and the changes are not as dramatic as some were originally predicting, we would expect to see sales levels increase to more historically ‘normal’ levels over the coming months, especially once Spring sunshine replaces Winter cold and moisture,” he said.

“Certainly initial feedback on June indicates sales this month will be more in line with what we’d typically expect for this time of year."

My view

New Zealand's housing market is running out of puff, judging by these figures.

Volumes are down 17% from a year ago and the demand that did surge through in early 2009 is now ebbing away as interest rates rise and rental property investors digest the impact of the changes in the Budget 2010.

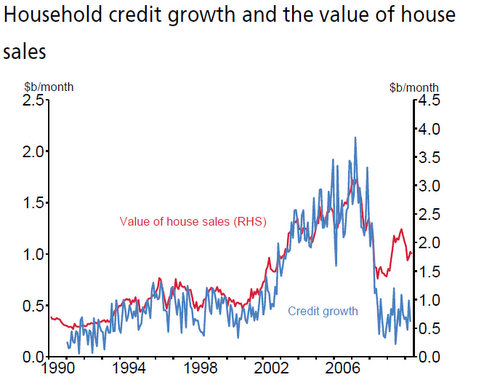

The best indicators of what might happen next are in the most recent bank lending figures. This chart here shows just how connected the housing market and housing credit growth has been.

The red line represents the value of house sales each month, which surged to as much as NZ$3 billion at the peak of the housing boom, while credit growth to households rose to just over NZ$2 billion at the peak. They tracked in line throughout the housing boom as credit pumped air into the housing bubble.

However, since the Global Financial Crisis erupted in mid 2008, that relationship between credit growth and the value of house sales has broken down. The gap between the value of house sales (the red line) and the value of credit growth (the blue line) is the size of the saving that New Zealand households are now doing. Currently New Zealanders are saving around NZ$1.5 billion a month. That is money that's not being spent on new housing, renovations and the consumer spinoffs that go with it. We have shut down the ATMs in our houses.

The Reserve Bank highlighted this chart when it said New Zealanders were saving more, rather than pushing more money into housing and consumption. Many home owners are repaying their mortgages faster than they have to, or are 'trading down' by selling expensive houses to buy cheaper houses and repaying the difference.

The comments from ASB's Jane Turner about migration are also interesting. As more New Zealanders head across the Tasman for work, the net migration surge that helped the market rebound last year is sliding away. That will kick one prop out from under the housing market.

In early 2008 I argued that house prices would drop 30% from their peak over the following two years. That didn't happen as the Reserve Bank provided lending support to the big banks here, Australia's government provided a deposit guarantee, the Official Cash Rate was slashed from 8.25% to 2.5% and our unemployment rate stayed relatively low. An extraordinary effort by the powers-that-be prevented a collapse. I revised my forecast last year to a 15% fall in house prices from the peak and over a longer period.

The artificial pumping of air into the market through late 2008 and early 2009 helped hold prices above their 'natural' level during the crisis. Now the artificial air is leaking out after the crisis, the housing market is starting to subside, albeit slowly.

The 'natural' level of house prices that is sustainable over time is best measured by affordability. Our measure of the proportion of after tax median pay needed to service an 80% mortgage on a median house is still around 60%. Household income levels are still well over 5 times house values in many of the big cities. That is plainly unsustainable, particularly as the credit that fuelled the bubble is slowly withdrawn.

Today's figures show the stratified measure of house prices is down 5% from its November 2007 peak and down 11% in real terms once inflation is taken into account. I still think we've got another 10% to fall in actual terms. That may take a few years. Meanwhile, real prices will fall even further. Once the inflation surge of late 2010 and early 2011 is taken into account, real house prices are likely to be down almost 20% by the end of next year.

That may shake the faith of the ever faithful who have sworn by housing for years and who mocked the doomsayers like me.

See the full REINZ press release below.

Despite pending tax changes and the anticipated rise in the Reserve Bank OCR there was no real reduction in residential property prices or the number of sales in May, according to figures released today by the Real Estate Institute of New Zealand (REINZ).

The median residential property price eased back to $350,000 in May from $356,000 in April and sales of 5,206 were only one down on the 5,207 residential properties sold in April even though the winter is usually a quieter period for the real estate market.

“It is good to see the market retain its strength and prices stay stable during a period when some buyers would have been concerned about potential tax and interest rate changes,” says Real Estate Institute of New Zealand President Peter McDonald. “While slightly down on the April figure and the March median of $360,000, the May median is still 3.7 per cent up on the median price of $337,500 in the same month in 2009, so we are still not seeing any significant fall in property values,” says Mr McDonald.

“With tax changes and interest rates now settled, property investors are already talking about returning to the market to cater for the growing demand for domestic rentals.” “Nationally the number of median days to sell increased from 40 to 43 but varied across the country from as high as 67 in Central Otago Lakes down to just 35 days in Southland,” he says.

The total value of residential sales, including sections, in New Zealand in May was $2.27 billion, an increase on the April total of $2.24 billion. The breakdown of the values of the properties was 195 for $1 million plus, 601 for $600,000 - $999,999, 1311 for $400,000 - $599,999 and 3099 under $400,000.

While changes in the median price vary across the country and there were falls in some areas, in 10 out of the 12 districts the increases in the median price ranged from 1 up to 10 per cent when compared with the same month last year.

Auckland residential sales, including sections, accounted for $1,082 million of total sales in May. Sales in Canterbury/Westland and Wellington were the next greatest at $260 m and $240 m respectively.

“While there has been some decline in turnover from the boom times of a couple years ago, during the past year nearly 67,000 homes were sold for a total of almost $27.5 billion so the real estate market is still very healthy,” says Mr McDonald

Your views? We welcome your comments below.

Volumes sold - REINZ

Select chart tabs

9 Comments

Happy to help Chris J ;)

cheers

Bernard

Les,

The Uridashis and Eurokiwi issuance market is dead.

http://www.interest.co.nz/charts/credit/eurobonds

We really are saving more here, which is good.

cheers

Bernard

Les,

I don't think the RBNZ has taken the pressure off the Core Funding Ratio. If anything, the pressure is increasing over the next two years as the RBNZ increases it from 65% in April to 75% in April 2012.

I think without the Core Funding Ratio the RBNZ would have had to tighten earlier and harder.

cheers

Bernard

Norm

Loving your Nom' d'plume

cheers

Bernard

Gingerbreadman, Anonymous

I argued in March 2008 that nominal house prices would fall 30% by the end of 2009. I was wrong. They fell around 10% at their worst and then rebounded. I changed my forecast in early 2009 to a fall of 15% from the peak.

I think we'll get there in the end.

cheers

Bernard

Steve,

You make some good points about construction and council costs. There is a real supply side problem which governments (both local and central) need to work on.

The land cost issue is another thing though?

Section prices need to fall sharply and should be governed by markets.

We'll see

cheers

Bernard

Steve,

That's interesting, but they would have to fall a long way to make a real difference.

The gap between floating and 2 year fixed is still around 150 basis points.

Also, you'll find the banks aren't keen to fire up the lending again. The Reserve Bank's Core Funding Ratio and the extra cost of borrowing offshore for longer terms is seeing to that.

To give you an example, BNZ sold some bonds yesterday at 98 basis points over swap rates. There's not a lot of room to cut their fixed rates there.

Here's the story from Gareth Vaughan with the details.

http://www.interest.co.nz/news/westpac-eyes-issue-more-nz5-bln-covered-…

cheers

Bernard

Also, for those looking for evidence on the falling swap rates, which act as the basis for longer term fixed mortgage rates, check out this chart set on our site.

http://www.interest.co.nz/charts/interest-rates/swap-rates

We love our charts at interest.co.nz !

cheers

Bernard

FYI to Anonymous.

I will be routinely deleting the YA CANT LOSE WITH xxxx MAAAATES comments. It was funny once.

Now it's boring.

And I'm no fan of capital letters. Let's steer clear of the shouting.

cheers

Bernard

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.