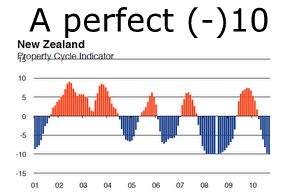

The property market continued in a 'downward spiral' in September, Mike Pero Mortgages and Infometrics said in releasing their Property Cycle Indicator (PCI).

“The nationwide PCI has dropped to its lowest possible figure, -10, for the first time in two years,” says Mike Pero Mortgages Chief Executive Shaun Riley.

“This latest figure suggests that house prices will come under further downward pressure in the coming months. House sales volumes in September were down 33 per cent from a year ago, the biggest annual fall since the height of the financial crisis in late 2008," Riley said.

“The Canterbury earthquake accounted for some of the renewed weakness, but sales activity weakened even if the Canterbury/Westland region is excluded," he said.

"Last month was the first time in over a year that the median house price has not been higher than a year earlier."

The Mike Pero Mortgages-Infometrics Property Cycle Indicator fell to a negative 10.00 in September, from -9.80 in August.

The Property Cycle Indicator is leading indicator of the housing market and includes three main factors: changes in the number of houses sold; changes in price; and the time taken for houses to sell.

Auckland remained steady with a PCI of -10.00 (same as in August) and Wellington lost ground, dropping to a PCI of -10.00 (from -8.87 in August).

Northland -5.87 (-6.71) and Manawatu/Wanganui -9.19 (-9.22) were North Island regions to show a slight improvement.

Canterbury/Westland’s PCI dropped further to -9.25 (a decrease from -7.87 in August), as did Nelson/Marlborough’s, with a PCI of -8.80 (from -7.40).

Central Otago was the only South Island region to gain some ground with a PCI of -3.89 in September, up from -5.45 in August. Rental inflation continued to edge higher in September, reaching 3.7 per cent per annum.

87 Comments

Let me guess...Kiwi peasants have discovered property does fall in price....well I never!....hello Mr Market...you here for the duration are you?...come to put the boot in have we...jolly good...start with the banks please.

"The nationwide PCI has dropped to its lowest possible figure, -10", so how come the graph goes to minus15 !?...and I guess the opposite view is " Well, it can only go up from here"

well they will keep falling in CHC if these aftershocks don't stop...that unless you like amusements rides as we seem to be on one gaint one at the moment.

Yep. Dunno who's gonna want to buy in the area for a while if they can avoid it [still waiting for a phone call from an EQC assessor]...

" The Mike Pero-Infometrics Property Cycle Indicator " ??? Excuse me if I chortle heartily into my Lapaz Batchoy bowl !

And it's negative 10 nationwide , but only minus 3.89 in Central Otago ............ Queenstown seceded from the nation or something ?

It's going to get worse once Mr Phil Goofy got his way of stopping foreign ownership. It will start with farm land and slowly spread to other types of asset.

But it cannot get any worse , 'cos the indicator stops at minus 10 ........ Worser more so than that isn't an option ............... Feel so much happier now that the Mike Pero-Infometrics Property Cycle Indicator has underpinned the property market . .............. Silly me , and I thought it was only minus 9.84 , not the full - 10 .

EQC assessor what are they, my mother is living in her garage, no sewage still ,no water, can't get a response from anyone, she rang last week they had her details mixed up with someone ulse, told her someone will be there by MARCH next year, only enough insurance to cover temp accomodation for 6 months so she cant afford to rent for two years and pay a mortgage, she has gone and registered for all the emergency response funds....heard nothing (like her neighbours as well- i guess that money is earning interest in someones account but not going to the people who need it) typical government response get there heads in the paper to begin with and all go hiding when the hard questions need to be answered.

They had a Australian magazine out there on Sunday taking photos of people living in broken houses, garages (she is not the only one) so another bad rampt for NZ overseas (and here is the tourism board saying all is good haha... joke).

Only good thing Civil defence going down street every week checking on people (these are volunteers- the ones at the top being paid Big bucks no where to be seen)

thats my rant.

We've reached the bottom now :)

DrHousingBubble says again and again - it takes 2 years from the top of a bubble where the market first siezed up with stock and low turnover, and mortgagee sales started to rise - before the REAL price crash starts. Up till then, it's just prelimiaries.

At least in California, they didn't have glaringly obvious examples to learn from like the one they provided the rest of the world.

During those 2 years, interesting things were happening in derivatives trading. There were plenty of suckers ready to take the "long" side of the bet, right up till the real crash was becoming undeniable. Lehmann Bros just happened to be the slowest reacting institution - several other institutions succeeded in unloading their "about to take a fall" paper onto Lehmann's right up to days before they crashed.

Such are the perils of property optimism at the wrong time. Not to mention the people who bought their homes at the top of a bubble.

With $3 billion (I think it was) been paid off of NZers mortgages during this current fashion of debt repayment, that’s an awful lot of money. I can’t see house prices collapsing with that sort of money being defensively spent on them. Nevertheless I do think that house prices are way over the top in NZ. When you can pay $1million for a 110 year old working man’s shack in Grey Lynn(you could have brought it for $65,000 20 years ago), $2M for views of Orakei basin???? (it’s a sewerage filled basin!, it’s not the Waitemata harbour!) and $1.2M for four bedrooms in Mt Eden with a view of the sky tower, then values have clearly gotten completely out of hand. Hopefully property prices will adjust back to what actually gives a property its value and will go someway towards restoring some sanity back to the market. But I won’t hold my breath. A collapse will only happen if unemployment suddenly takes off IMO.

Good points, David B. But I'd ask the question "What would that $3bn have been spent on otherwise?"; and if the answer is substantially "on another/better/more expensive house", then the support mechanism may have just been taken away from the market.

Yes I agree with you it would have certainly kept the merry-go-round going! But if that $3bn was sufficient to stimulate demand and therefore increase prices, I wonder if its absence would equal price stability rather than an actual decline in prices? I don't know??

"$2M for views of Orakei basin???? (it’s a sewerage filled basin!, it’s not the Waitemata harbour!)"

When you put it like that $2 mil does sound a tad high, lol. But the thing to remember is the $2m pad in Orakei is the end product. Trendy city suburbs anywhere will always demand crazy prices from people who are making big bucks. The real madness is $400k for a 3-bed dive in deepest darkest west Auckland, as these mortgages are being paid by average working people who are living beyond their means.

"A collapse will only happen if unemployment suddenly takes off IMO."

Reading between the lines, the US and Europe are basically pressure cookers at the mo with governments drowning in unemployment and debt. The smart people are trying to protect wealth in hard assets (gold), the stupid are trying to manage their debt. My call is for something to go pop in the coming n.hemispere winter. Ireland, Greece, Spain.....when one goes the rest will follow.

If you think our housing market is bad... just go across the ditch and our neighbour countries. I spent two months in Aus, Singapore, Malysia and Hong Kong - in sinagpore and Hong kong, this year alone the average house price went up almost 20%...

Agreed. The sound of the Aussie and SE Asian property bubbles bursting will be absolutely deafening. Not too long to wait for it now.

In upper hutt, the RVs provided by QV are down across the board about 3-5 % from what they were in 2007. Upper Hutt only gets their RVs done every 3-4 years. Taking into account inflation, the values have dropped a lot, and properties around the area just are not selling.

There are a lot of cash buyers who are just waiting to mop up the property bubble mess, and pick up some nice cheap properties.

I'm one of those folks. I plan on buying in about 3-4 years time. I'm considering a bit of a stint working in "higher salary" Aussie before settling back down here again.

You and a whole lot of others! Nobody will buy now, even if they could, when they know prices will eventually be a lot lower.

That's why these days most people are intent on paying down debt and saving.

Actually a lot of people are still wanting to buy now. However it is the 'smart' ones who are waiting.

True, the problem though will be the world economic state by the end of it MIGHT make alot of people reconsider. Things are going to get SO BAD that even contemplating buying a house or borrowing from a bank in the next decade might just finish the last few optimists out there who fail to see what IS taking place and what is ABOUT TO take place. Seriously folks, keep you head down and your family close this next 10 years. You will see why

Therefore the 'smart' ones should be selling like mad.

Nah mate, the smart ones sold out around 2007, before the bubble burst.

Only the dumb and the desperate - usually the same people - try to sell in a collapsing market.

Yup.... Mr Market has Noddy by the short ones...the peasants have stopped being stupid...the bank bosses are on the streets drumming up loans business...jeez they'll be in tears soon...Bolly is badgering the Beehive blowhards to change the law to allow the banks to go after the hot money again cos the banks have said they have to!...what next!....I guess we could expect Key to 'make an offer we can't refuse'.....borrow more and splurge or I put your taxes up....now that would be funny. Goofy has had to rush out the pork for votes Labour promises programme early because his voters are all off to work for Jewleeya and join the ALP...bugger.

Any day now we will be told saving is bad and debt is good....oh, we have been!

what is that crap you're spouting there, Popeye?

hard to figure out what you're actually trying to say...could you break it down to just everyday gibberish perhaps?

I have a friend buying in Nappa Valley Ca at one 6th of previous sale.

I think he has overpaid

Napa

AndrewJ - smart overseas (read Chinese) investors will be buying in the USA rather than downunder. They are surely near the bottom, we still have a way to fall

"Chairman Moa" is one of the best names I've heard for a while

I'm waiting for another insightful Rodney DIckens article

the word will have already reached china about Labours new policy to shut out o/seas investors..to the chinese this will read " nz shut to investment...don't like asians" or such..which actually might just be a good thing.

me names Goff and I'm off!

We have recently had a sale today of a property in Auckland just gone unconditional. Thought we would get $865,000. Got $815,000, that was $100,000 more than what it cost pre - 2003 boom. It is a stickey market but only the very expensive and the poorly situated or poorly presented are not selling.There are definately people wanting to make purchases.

Was it worth $1000 per week to rent, muzza? If not, the buyers still paid too much.

i'm one of them !!

My carpet layer is not short of work. He says that there are quite a few people who have decided to do up their existing house rather than try and sell and buy in this market particularly with the RE fees as a further dampener that they will not recover any time soon.

It is very comfortable in a pair of old shoes when the new ones may pinch your toes or rub your heel .

"Last month was the first time in over a year that the median house price has not been higher than a year earlier."

And I was convinced they are constantly falling for last 3 years...

"The Mike Pero Mortgages-Infometrics Property Cycle Indicator" !!

That bit sounds funny enough by itself, but this bit's even better - "The Property Cycle Indicator is leading indicator of the housing market" !! Ha ha ha ha, stop, you're killing me!....

So Infometrics are talking down the market. Weren't these the guys who said in mid 2009 that by mid 2012 house values would be up by more than 20%

I think the number they used was 24%.

I guess they feel pretty silly right about now.

Will it be a spiral that gathers speed?

Its interesting looking at the graph. The frequency of negative sentiment in the graph has been much more intense and frequent since 2005 than over the 2001-2005 period.

Since 2005 there have only been short sharp little bursts of moderate positive sentiment.

the graph simply represents the once in a lifetime silliness that occured from 2001 to 2005

A 'downward spiral' - that explains why we're starting to get those 'please can we buy your house' flyers in the mailbox again and houses are selling in less than 2 weeks for more than they ever have before. Must depend a bit where you are.

You've heard of " Desperate Housewives"...well, this is the new followup series called " Desperate Real Estate Agents"

Latest statistics indicate the Auckland City market is performing well with regard to sale prices, while volume is low due to the lack of homes on the market. Here is the median price history for Auckland City over the last few years for the month of September:

2010 $525,000

2009 $516,500

2008 $450,000

2007 $480,000 Many think this was the peak but it has since been exceeded

2006 $427,900

2005 $408,000

2004 $385,000

Give us the source of your stats. so we can all have a good look through them SK. Anyone can make up fugures from their own 'digging'.

Bob - yes there aren't many good houses for sale. We went to a open home in Ponsonby - 46 people were there and sold within 4 weeks - for two arms and two legs plus one kidney!

It depends on whose body-bits they were! If they were from someone who'd sold off, say, their $5m home, then bought at $1m and releases cash, that will pull up the middle, for a while; until those top end houses run out of buyers at-the-price, and start to come towards the middle. Then the middle will then fall away again, in the face of, 'but I could get so much better for not much more, higher up'

ummm don't think so - in this particular case, it was sold to an overseas buyer (no they weren't chinese)

REINZ data - readily available to all.

You are very creative with these complex scenarios you manufacture to support your ignoring of the facts.

Actually; I don't ignore 'the facts'. It make absolute sense to me that as the higher-priced houses are stress-saled out/ traded down or just plain old sold, to avaoid the ther on-going property fall, that the median price will rise. So for me, the higher the median goes, coupled with falling turnover, the more it indictaes to me the stress in the market, and it's continuing direction ~ ulitimatley,down. Then, the median will follow.

(PS: Have another read of the above article. It says, excatly that. It encompasses price, volume and time, and whilst emotively captioned " downward spiral.." is pretty much spot on)

This has been pointed out many times on interest.co.nz - average prices are being artificially 'pulled up' by desperate sellers of high end homes selling them at a heavy discount (like the was $8m, just sold for $5m story).

Although this may make sense to you its not necessarily mathematically correct. Median averages are used rather than mean averages to reduce skew and those high end homes would have been part of previous statistics at their higher price. In 2007 there's an $8m sale and 10 x $1m sales for mean of $1.636M/median of $1M. In 2010 there's a distress sale $5M and 4 x sales of $1.2M for a mean of $1.96M/median of $1.2.

So turnover has dropped 50%, both median and mean have increased for 80% of 2010 sales and yet you deduce that this means prices are "...continuing...down..."?

I only did one year of university statistics so could be wrong, but it seems like there's a few potential flaws in your assumptions.

Perhaps you should have done a year of English, at uni., as well, Bob. Then you would understand my final words ...".. ulitimatley,down. Then, the median will follow."

And re the dominant trend ?: It is reverting to the mean ( look at the graphs section of this website, for instance). It is therefore downwards, as we are above long term trend at the present, and will revert ,by either time decay or nominal fall.

You ignore the facts, figures and the method used to provide them - stratification.

From the RBNZ:

Using a suburb-level dataset from the Real

Estate Institute of New Zealand we use stratification techniques to adjust for

compositional change and derive a timely and robust measure of housing

prices for New Zealand. Results suggest this stratified measure produces

estimates of housing price inflation that accord closely with the accurate but

less timely figures obtained from the QV Quarterly House Price Index.

Stratification works against your post, if anything! It confirms that stratified, higher priced, properties are the ones selling, not the medium to bottom end ( as they were). So doesn't that tell you something? The 'rich' and smart are getting out; the less wealthy are stuck with what they have, and will stay put. That leads to a continous fall, as those that have to sell (to relocate, repay debts or whatever) do, and at prices the market will pay ie: look to rental equivalents or wdisposable income for that baseline.

I'd prefer to get my figures from the Reserve Bank - rather than Mike Pero.

I thought you said your source was the REINZ (10.25am)? But, hey, I'll take the RBNZ figures. Give me a link, and I'll have a good look through them.

Page 8 of this one has your Auckland City results - the ones where the movers and shakers live!

That's not the RBNZ link! And besides, it has Auckland, at $450k in Sept 2010. Where is your $525K? It's for Downtown City. Pretty selective stat. What's wrong with Metropolitan Auckalnd - 3 times the turnover, and $455k. But, hey, if you want to base your strategy on Downtown Auckland ( maybe that's your market!), fill your boots.....

@SK - those are straight medians, not stratified medians. REINZ only use the stratified medians to calculate their house price index.

However the problem with stratified medians is that they are designed to account for a change in composition - which can mean that in practice they mask what is actually happening in the market - stratifying removes the natural weighting by giving each status an equal weighting in the median calculation. It hides the problem of compositional shift even more than a straight median.

Sure, some house types in selected suburbs are selling and selling well - but the vast majority aren't - and the lower end of the market is just not moving at all.

Sure in

(apologies, repeated post due to slow internet connection!)

$525,000 602

Page 8.

Auckland CITY.

ie:

not South Auckland.

not Waitakere

PS the figures are a combined effort as reported here on this site

http://www.interest.co.nz/news/rbnz-and-reinz-introduce-new-house-price-inflation-measure-update-1

It's not CBD auckland, its central auckland. Have you ever been to a city?

This includes Pt Chev, Ponsonby, Grey Lynn, Parnell etc etc.

ie some of the wealthiest parts of the city where smart investors hold properties.

In any case - when you look at those figures generally - they are positive in nearly all areas of Auckland.

Spot on, SK! Exactly....where the 'wealthier' and smart people are ...selling.....that's why the median is higher. See? It means very little in isolation.

(PS: That REINZ report is just that. REINZ stuff. No RBNZ collaberation in it. Just R/E propoganda ie: no mortgagee sales or 'non market 'priced sales in the stats. etc).

Oh, and if you say 'that for every seller there has to be a buyer'. Concider this: No matter how much I want to buy a house on Paratai Drive, I won't be able to....unless someone wants to sell?

So you agree the figures that I originally quoted are correct.

And you agree that there are markets within markets.

And you agree that in Auckand City people are happily buying and selling, prices are rising - there is no more land being created in Parnell is there? These people are unpeturbed by the possibility of a sawmill closing for example.

This is my perspective, and why I'm bullish on property in Central Auckland.

I'm not sure what your perspecitve is to be honest?

I note the source of your figures from the REINZ; one of many published statistics. And, as I suggested to you, there are markets in market ( to use your words). Whether people are 'happy' buying and selling , I can't say. I don't know what they paid or what there circumstances are ( For instance. The article here yesterday re the people who paid $8m for their property 5 years ago, just sold for $5m odd, are probably 'not happy'). And the land in Parnell will always be relative to the price of land elswhere. It may be more or less in demand, but the price will reflect a comparative price in a neighbouring suburb or location etc.

And my perspective remains; New Zealand has too much debt. Property related, non productive, speculative debt, that the Government is progessively going to rebalance away from that property sector. If you choose to ignore that fine. But you are fighting a much bigger party than just little ol' me on this website!

Expensive property and empty land fluctuates much more than lower priced property. Stuff over $2M is not selling unless discounted heavily. Central Auckland stuff under $1M is selling for more than it ever has. The CBD is a completely different market.

Sure there's too much debt, but the root cause is not speculation or property investors etc. etc. It's a direct result of the RMA and the Government will not be able to 'rebalance' the economy away from property until they do something about the RMA. Auckland is unique in that the moment you step over the CBD boundary all land becomes zoned low density residential. Look at any other city and see if there's 1per 500sqm or 1 per 375sqm density 1km from the center of their downtown. This drives up prices in Auckland and consequentially elsewhere.

I don't want to pay $800k to live in a reasonable house a reasonable distance from town, but the alternative is 1.5 hours of commuting a day, so I do. This is not speculation - it's supply and demand.

But why BUY it, bob? Just rent it. Like is, your paying $1000+ per week, interest-only plus outgoings, to live in a place that would cost you, what, $750 per week to rent? Why not spend the other $13k p.a. (Let's not even think about the $32,000 in costs when you want to 'move'!) on good wine, trips to Thailand or whatever ( or even, God forbid, save it) ,than pay it to the bank in interest!

You seem to have completely and utterly missed the point. I'm not interested in argument about owning versus renting. I'm interested informed discussion on the reasons for high house prices and solutions to this problem outside the usual endless interest.co.nz witch-huntery.

Although can't help pointing out your red herring question assumes no equity, cheap rent and no [warning: obscene word follows] capital gain - the $800k inner suburb house is worth a lot more than it was at the 'peak'. Everyones situation is different, not everyone is financially or emotionally better off renting.

Bob: If people don't buy on uneconomic terms, the prices fall! And equity has an implied cost, regardless of the amount of borrowing .It's called alternative application of capital. A house costs 100% of it's price, no matter how it's funding is allocated. And most people would be better off renting, regardless of when they bought their property;as it's about current funds usage. Can't you see that? If you sold your $800k house at current market, ( you'd know better than me what it would fetch) and banked it, less the rent, you would pay, you must be better off? Capital gains are an illusion that are likely to have vanished. Capital losses are just as likely now.

ONLY LOSERS RENT!

And those on welfare.

Those who choose to own their own home in this environment pay for that choice, by paying more than the rental equivalent. Those who rent ,get paid for the choice they make, by that same calculation. As time goes on, we shall progessively see more people having to do what they 'have to do', rather then what they 'choose to do'. That's when the price falls will kick in with gusto!

THINK OF ALL THE CAPITAL GAINS LOSER RENTERS MISS OUT ON!

Wait. It is still 2006, right?

2006 already ! How come I've still got the 2003 calendar up ......... ? .............. Oh yeah , that's right , " Miss Valvoline's " air bags ........... Hoooooooooo haaaaaaaaaa ............ !

I suspect not Nicholas - the government is already concerned that deleveraging too quickly will threaten the recovery. And what is more, the government has stated that it will not make property investing too difficult, as it does not want to be in the rentals business itself. So although we are agreed that there is too much debt, we will not be driving a precipitous path to remove it. At least not on purpose.

I suspect not Nicholas - the government is already concerned that deleveraging too quickly will threaten the recovery. And what is more, the government has stated that it will not make property investing too difficult, as it does not want to be in the rentals business itself. So although we are agreed that there is too much debt, we will not be driving a precipitous path to remove it. At least not on purpose.

I'd suggest that Key's remarks ( if that's what you refer to) are more in the vein of Steve Keen thoughts ~ link below ~ ie: GDP falls as debt velocity falls. It doesn't follow that 'the Government is concerned about the rate of deleverging". In fact, Bill English noted that "we have to continue to save for many years" as I recall. As far as 'the rental business' goes. Maybe they don't .But it makes no sense for people to pay more to own the same property as it would cost to rent it, if there are going to be no or limited capital gains to justify it. It's just a further 'waste of productive capacity' that goes overseas as interest payments.

http://www.debtdeflation.com/blogs/2010/10/19/deleveraging-deceleration-and-the-double-dip/

Nicholas, you're right but that common sense - if everyone has the same common sense approach we wouldn't have any issues such as wars, diseseas, huge gaps between the rich vs the poor etc...

Infact we mighn't need a government !!!! or we may just remain as monkies...

Yalza, those mortgage loan approvals just keep getting worserer and worserer.....for the 3rd successive October week they have been below the 5000 level:

http://www.rbnz.govt.nz/statistics/monfin/c16/download.html

This time last year the LOWEST approvals week was about 6500.........

nor is there any sign of a spring pick up in the number or value of approvals, as has been the case in previous years

Another great piece from the Unconventional Economist:

http://www.unconventionaleconomist.com/

Some meaty support for Hugh P's views in there

MiA ,,,,, compulsory reading for all, thank you

I concur with NA..... did a quick calculation of the city fringe apartment and the rent I pay for it, vs buying the property, when it sold at a mortgagee auction 1 month ago.

To cut a long story short, I am $150 up per week by renting, as opposed to our mortgagee auction purchaser, based on a 20% deposit and a 7% mortgage over 20 years ..... and I didn't even include apartment maintainance in my calculations !

To all those property bulls out there, there will not be "plane loads" of overseas buyers rushing in to buy your crap, leaky, cold and damp over-priced properties. If I was them, i would be heading to the US, where there are alot more "realistically priced" properties and the property market is near or at the bottom of the cycle.

Saying the US market is near or at the bottom is purely speculative. The country's property bubble has popped spectacularly but it may have a lot further to fall. The US is not out of the woods yet. Those buying there now are simply speculating that the worst of the falls have passed.

Front page of the Herald today has corrected by figure for Auckland central.

Revised up from $525k (which was apparently so hard to believe) up to $536,200k

And what else did it say? " You can buy a house...but can you afford to have a family" and "..You wouldn't want to lose your job...". We are getting to the really exciting bit, now! Where people ( eg: the MSM) start realising just how unaffordable property is. Then.....It's all downhill.... Sell now, whilst you still can, SK!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.