By Alex Tarrant

Surplus, GDP and debt forecasts put forward from Treasury in Budget 2011 appear "more optimistic than achievable," Barclays Capital economists say.

Treasury is forecasting government will return its books to surplus in the 2014/15 year, with net public debt hitting a peak of 29.6% of GDP in 2015. Most commentators have labeled the forecasts, which also predict wage growth will be about 2% above inflation over the next three years, as optimistic, although the government has come out in defence of Treasury's predictions.

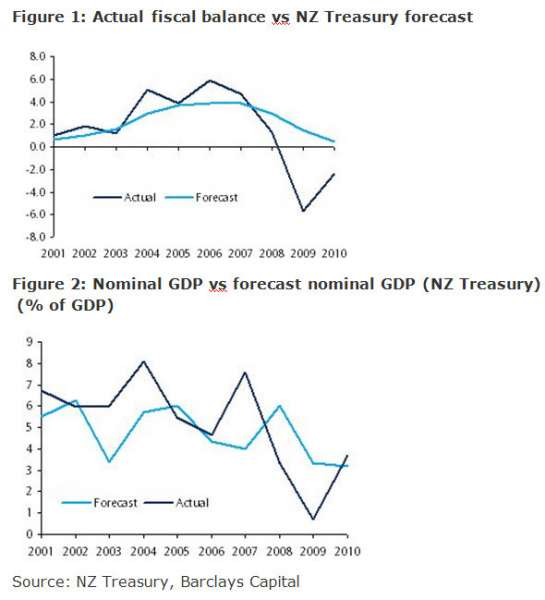

While the Treasury consistently underestimated the fiscal surplus between 2003 and 2008, it had since consistently underestimated the subsequent deficits, Barclays Capital economist Joaquin Vespignani said in a research note on the budget.

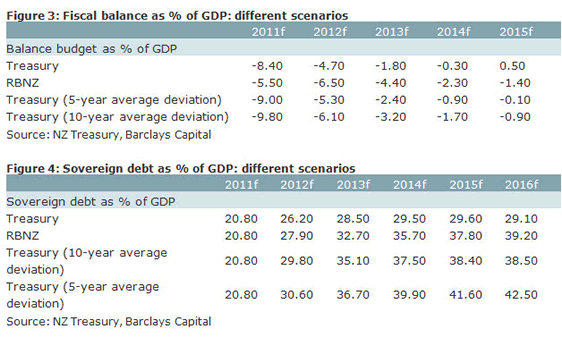

Barclays Capital economists calculated the average error in Treasury forecasts over the past five and ten year periods, with calculations showing the debt track could be worse than expected, and in line with more pessamistic Reserve Bank forecasts.

"We amended the NZ Treasury's current forecasts for the fiscal balance by adding the average errors in its forecasts over the past 5 and 10 years. These errors have averaged 0.6% per ammum over the past 10 years and 1.4% pa over the past 5 years," they said.

Barclays economists also estimated the impact of Treasury's forecast deviations on net sovereign debt.

"Applying the 10-year average forecast error results in a sovereign debt load as a % of GDP of c.38% by 2015, while the 5-year average error produces nearly 42%. These estimates are in line with the latest's RBNZ's estimation," they said.

The Barclays economists also charted Treasury's government fiscal balance and GDP forecasts with the results, saying Treasury had underestimated surpluses, but had been too optimistic on deficits:

Key defends Treasury

Meanwhile following criticism of Treasury's forecasts, Prime Minister John Key last night moved to defend the predictions.

“There has been some commentary about the Treasury’s budget forecasts for jobs and growth, suggesting they are too optimistic. Treasury’s independent forecasts are in the pack of other forecasts. In fact, a number of them have described the budget forecasts as conservative," Key said at his post-cabinet media conference on Monday.

"Remember, Treasury is forecasting 1.8% growth in the year ending March 2012, and 4% growth in the year ending March 2013. That is not aggressive compared to previous recoveries," he said.

"If I was just to have a look briefly at the forecast comparisons that other banks have got, ANZ says: ‘We think the Treasury has been a bit conservative in this regard, and we see upside risk to the tax revenue numbers’; BNZ says: ‘Can we thus get the growth forecasts by Treasury needed to achieve the revenue objectives? – the answer, probably. Our forecasts for economic growth are not significantly different to Treasury’.

“Deutche Bank says: ‘These forecasts are a little bit weaker than our own, and thus a prudent base for the government’s fiscal planning’; Goldman Sachs says: ‘overall, Treasury’s economic forecasts are broadly similar to our own’; Westpac says: ‘if anything, the Treasury’s economic assumptions seem fairly conservative’."

13 Comments

I actually think Treasury's GDP forecast's are viable (although I think 1.8% this year is somewhat high - I'd expect closer to 1%). 4% for the next year with the ChCh rebuild seems reasonable.

It's their wage growth and unemployment predictions that I really struggle with

So it seems you can more accurately calculate growth by first calculating how wrong Treasury is.

Awesome.

When NZ talks about growth they talk about a low NZD vs. the AUD. but that is changing by the hour and the export led recovery will lose momentum. I can imagine why Mr English is already talking the NZD down, but the market does not want to hear him.

The budget is all about AUD strength. So it can fizzle in a blink

So let's have a guess where the OCR is going, then.....

Would you agree.... nowhere.

I had your suggestion of 'maintaining that kiwi advantage over the aussie' in mind; so for me it's...0%. The RBA can't be too far away from an about-face either, given their property market tremors. eg: "Surfers Paradise - Currently down 9.5% from peak. Expected further decline for 2011 is 9-15%. Sunshine Coast - Currently down 9.0% from peak. Expected further decline for 2011 is 9-15%

Unless we see wage increases, the areas/sectors with inflation will have to be matched with areas/sectors in deflation.....so yes, no where OR deflation....and then the OCR could even be cut.

Even talking about core inflation (instead fof CPI) at 3% as opposed to <2% isnt hyper-inflation territory by a long stretch.

Personally I think JK is selling us a pig in a poke....sadly I suspect enough will fall for it (unless ACT starts to do very well and voters run) to see a National second term and then we get shafted...3rd term? cant see it.....I expect JK etc will do a lot of swinging the the right "dragged" [not]-kicking and screaming by ACT.

regards

Steven - I agree with your prediction. The "optimistic" economic predictions will not be fulfilled, sometime in their second term National will then be "forced" to make unpopular cuts (especially when ACT led by Brash are part of their govt, with circa 6-7% of the vote) , then they'll get thrown out, especially if there is a more inspiring alternative to Goff by then

Barclays's analysis has merit but like the Treasury advice ignores or discounts the impact of rising oil prices causing lower GDP, and higher inflation and unemployment.

Unlike a UK government report obtained by The Times which projects a drop in UK GDP of 1.7% for 2 consecutive years compared to baseline assumptions, higher inflation and unemployment if oil prices rise by 102% (already 50% above Oct 2010 levels)

there is a very oily elephant in the room.

more here

Now assuming that the market is always correct, it is sending a clear massage that NZ rates are going higher, they are being priced in and it is a bit expensive to be wrong this market.

It's expensive to be wrong in any market, michael :) And what makes a market? Different points of view.....

Nicholas, I am in the same page,

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.