By Alex Tarrant

The government may soon face the difficult choice of changing New Zealand's tax structure to better incentivise savings and investment and further disincentivise property investment, Treasury says.

One of Treasury's immediate priorities is to review how savings and investment are taxed, while the Productivity Commission may also recommend tax changes to help make housing more affordable when it releases its report to the government on March 23.

Poor investment and savings performance in the economy was creating challenges for the government, including New Zealand's tax system, Treasury says in a flow chart accompanying a speech by Secretary Gabriel Makhlouf to the International Fiscal Association in Queenstown on Saturday.

"New Zealanders do not save as much as citizens from other countries. Additionally, the mix of savings may be distorted due to tax reasons. The Productivity Commission is investigating housing affordability and is looking at tax settings," Treasury says.

"Whether or not tax plays a major role in capital allocation is difficult to answer – New Zealand has a culture of property ownership (although perhaps this in itself is driven by tax)," it says.

"Ultimately, there is underlying concern with the allocation of capital in the New Zealand economy. If further work supports substantial reform, Ministers may face a difficult strategic choice between the current well-regarded model and something else," it says.

Changes in tax rates would affect incentives to save and invest: Higher levels of capital investment generally increased productivity and economic growth.

Meanwhile, the level of capital invested by non-residents was considered to be more sensitive to tax than the level of capital invested by residents.

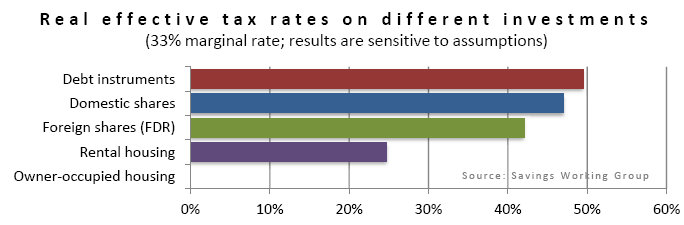

"Different patterns of capital investment, influenced by tax structure, can have different effects on economic growth. Because of the different regimes in place and the effects of inflation, income from different assets is taxed inconsistently," Treasury says.

"Debt instruments are taxed at the highest rates. Owner-occupied housing has a zero percent effective tax rate (no tax on imputed rents and no tax on the capital gains). Other investments fall somewhere in between these," it says.

In its 2010 Budget, the government moved to disincentivise housing investment by taking away property owners' ability to claim depreciation on properties with expected lifespans longer than 50 years, a move it claims has gone some way to achieving its goal.

Finance Minister Bill English has said the government is still looking at whether to index interest rates for inflation, which would make vehicles like term deposits more attractive, and mean property investors would not be able to write off as much mortgage interest against other incomes.

That works by only allowing the real interest rate - adjusted for inflation - be be taxed in the case of term deposits, and onlt the real mortgage interest allowed to be deducted against a property-owner's income.

Cold water on Tobin Tax

Meanwhile a Tobin tax, or a tax on financial transactions, was a solution looking for a problem, and has no place in New Zealand's tax system, Treasury Secretary Gabriel Makhlouf said in his speech.

The idea of a financial transactions tax has taken hold in the European Union, with French President Sarkozy calling for one to be placed on European finanical institutions.

"Nobel-prize winning economist James Tobin came up with the idea. The purpose was to reduce speculation in currency markets, which Tobin thought of as dangerous. Tobin came up with the idea soon after the end of the Bretton Woods system, before which each country maintained its currency within a fixed value of the price of gold," Makhlouf said.

The idea gained popularity after various “capital flight” scenarios in Mexico, Asia, and Russia in the 1990s.

"Somehow, the idea has been resurrected in the aftermath of the financial crisis as a means of raising revenue. Now it seems to be simply an attempt to target banks, or, in some circles, as an anti-globalisation measure. These views seem to ignore the difference between tax liability – who literally pays the tax; and tax incidence – who really bears the cost of the tax," Makhlouf said.

"To the extent the idea is supported by those who oppose globalisation, such support is misguided. Before his death in 2002, Tobin laid out his position [interview with Der Spiegel]:

I am an economist and, like most economists, I support free trade. Furthermore, I am in favour of the International Monetary Fund, the World Bank, the World Trade Organisation. [The Tobin tax supporters have] hijacked my name. ... The tax on foreign exchange transactions was devised to cushion exchange rate fluctuations.

"It’s fair to say that exchange rate fluctuations played next to no part in the financial crisis," Makhlouf said.

"In fact, countries like Iceland, with floating exchange rates and the ability to regain competitiveness by dramatic exchange rate revaluations, are in a much better position than a country like Greece, without the ability to devalue its own currency," he said.

"The Tobin tax is a solution in search of a problem, and we do not see a role for any such tax in New Zealand."

No cut in company tax

And don't expect any further reductions in New Zealand's company tax rate any time soon as the government needed to focus on its main priority of getting the books back to surplus in the 2014/15 year.

"While further company rate cuts may be desirable in the future, in the short term our primary constraint is, of course, fiscal – the need to balance tax revenue with government expenditure. The Government’s strategy is to achieve surplus by 2014/2015, and accordingly, in the short term anyway, reductions in the corporate income tax rate are unlikely," Makhlouf said.

"The second constraint is how we think about alignment between tax on different types of income, and how far we can deviate from the goal of alignment while still retaining income neutrality," he said.

"In an uncomplicated world we would want to align the top personal income tax rate with the corporate income tax rate. Because they are both final rates, we know a six percentage point difference between the top personal rate and the trust rate distorts behaviour and is unfair – the Government changed that in 2010.

"We can live with the current five percentage point difference between the company rate and the top personal rate, with the trust and top personal rates aligned. This is because for New Zealanders, the company rate is an interim rate before any extra tax is paid on dividends. But with a larger non alignment between the company rate and the top personal rate the timing advantage of operating as a company starts to bite," he said.

21 Comments

Show the effective tax rate on companies, even better then property JMO. Funny govt wants more savers, so it can get a better bang for buck on it's negative real rates. About time they started looking at the revenue stream, in the futile attempt to "balance the budget", and "return to surplus." In spite of that that a 2.5% decrease in revenues came from Key's vote buying policies. Or in other words 1 out of every 3 dollars of govt borrowing, is because of Keys vot buying.

In its briefing to the incoming minister, the IRD reported the government’s tax take as a ratio of gross domestic product fell 4 percentage points since 2007. Little told the select committee about 2.5 percentage points of that was due to government policy, with the remainder stemming from the country’s recession.

All disincentivising property investment acheives is a reduction in housing construction and an increase in rents - both of which we have seen in the past year or so!

The disincentive to reduce unproductive speculation in property must involve reducing the velocity of property trading - those that buy when a market is in an upswing hoping for a quick profit are the biggest problem - but long term investment must be encouraged and not discouraged.

A capital gains tax for property owned for less than 2 years could be appropriate but for property owned longer than 10 years CGT should be 0% perhaps with a sliding scale in between.

Enforcement of existing tax rules regarding assets bought with the intent to resell, should be suffcient, rather than introducing a new tax.

The existing legislation needs to be redrawn, with clear boundries, rather than the subjective tests applied in this area currently.

Just the threat of disincentivising property investment by a government is enough to keep me away from buying another property to rent out Chris... if you are investing over the long term (which I am) you don't like the government changing the rules every time they have a turn in office.

I mean if they took away depreciation write offs and ring fenced property losses and brought in a law that for tax deductions you could only recognise loans up to 70-80% of the CV for writing off the interest (much better idea than disputing over inflation rates that keep changing every year and no need for still more IRD bureaucracy), I would cope with that... (all of which btw would increase rental prices) but then, in their great wisdom (and need for more tax dollars) what else will they come up with...?

meanwhile in another small nation far far away...

"Norway is moving closer to a housing bubble as the central bank’s strategy of cutting interest rates to weaken the krone spurs credit growth and bloats property values.".

"Meanwhile, private debt burdens continue to swell. Household debt will reach 204 percent of disposable incomes this year, the central bank estimates. That’s the highest level since at least 1988, when the bank started compiling the data. In the 1980s, just before a housing collapse triggered a 40 percent slump in average Norwegian house prices, the private-debt ratio was about 150 percent,Morten Baltzersen, director general of Norway’s FSA, said in an interview last month.

House prices, which haven’t declined on an annual basis since 2008, jumped 7 percent last month to a record, according to the Real Estate Brokers Association. Property values have risen almost twice as fast as disposable incomes since 1992, central bank data show. Shiller, who is also an economics professor at Yale University, warns property prices in Norway“have gone up more than they ever did in the U.S.”

and real boot in the RBNZ bum!

"The financial regulator last year pushed through guidelines for banks, urging them not to grant loans that make up more than 85 percent of a property’s value. DNB ASA, Norway’s biggest bank, is “definitely applying the new guidelines,”

Of course while the RBNZ is playing puppet to the banks with the LVR joke and the OCR and the Basel BS....we have us a bubble being blown while at the same time throughout most of New Zealand the house building activity has ground to a halt...death stalks the suppliers....tickets to aus are being picked up by skilled workers...they have had a guts full of the manner in which this govt has put the GST hammer down on their lives.

The banks do not care whether the fools who buy their credit drugs, are building new or buying old...it's all profit to them and they have the advantage of owning the govt and running the RBNZ...the outcome is a bubble...yes it's localised in Auckland but the last farce started there as well.

Young Kiwi have got to see the forest here..they have to understand their futures are being bought by the banks with the ok from the Beehive and the Terrace. Serdom for life if they stay in NZ.

Re LVR joke. I bought my first house in 1984 with a 90% loan and may others I know did the same by the time they added in the 2nd mortgage to Building Society and the capitalised Family Benefit.

Banks are always working stress tests on their books (looking at impact of price movements, effects on UMI caluations for interest rate increases etc).

Its not a lend and hope game like you think it is (mind you it was in the BNZ in late 1980's in the corporate world and we know what happenned there).

From what I can recall most banks failures have been due to either rogue FX / money market traders or in the corporate space (DFC / BNZ).

Wolly

you might be able to give me the name of the bank that fell over due to retail / residential lending issues?

Egad I jeft out an eff..."serfdom" it should have been.

This report above about govt having to fiddle the tax to boost savings etc etc...so much hotair...the banks will not allow the govt or RBNZ to take way the property cash cow...any move toward saving would impact bank profits from the bubble...yes saving would be a wiser prudent pathway but it will not happen because of the control the parasites have.

It is that control and the bubbles which dictate where the economy will go, not Key and not English.The rest of Cabinet can be ignored. Even Joyce is but a pawn in the game.

Wolly,

Have a look at banks profit streams over last 30 years or so.

Back then most profit was made by interest margin topped up by FX profits.

Now interest margin income is only about 50% of total income with profit from Savings products, Insurance products, service and other fees etc

Banks no longer need pure growth in credit growth to survive, infact most have said there will be little to no credit growth (I.e. balance sheet growth) for some time.

Kinda blows away your arguement

A fresh breeze can be good in the garden!...what they tell you is not what they mean you to know...and what we know is only a fraction of what they are up to.

I still claim the best lifestyle is one without debt to a bank..or any other loan shark.

If that were a Kiwi culture thing..if it had been for the last 60 years...we would be up there alongside other debt free wealthy nations...sadly we are addicted to credit...we and the govt.

Totally agree that a lifestyle without debt is better than on with it.

However it is not the debt itself is the problem rather the level of it and why its been taken (to cover gap between income and expenses which is bad debt) whereas a mortgage could be considered good debtas you a purchasing as asset (like a business buying a piece of machinary tio increase production would be considered good debt)

However no debt is good debt if you can't service it.

Where is the bubble if house prices on only just getting back to 2007 levels (and in some places not yet there) and credit growth is nil (have a look at banks balance sheets).

If prices rise and bank credit does not then those prices can not be fuelled by credit? or have I missed somthing again?

I don't think a bubble needs credit.

A bubble is when investors pile into an overvalued class of asset. Just because they didn't borrow from a bank to do so, doesn't mean the asset class is not overvalued.

But wasn't the last housing bubble created mostly by cheap and endless credit?

With an asset class with a large entry cost of housing most people would have to borrow (whereas you could get into goats a lot easier?)

True...the Tulip bubble was based on assets or cash....and the promise to pay. Those were the days...I still have some bulbs left.

You could always plant the tulips and give the flowers to your local bank branch to brighten up their banking chambers?????

"I am an economist and, like most economists, I support free trade. Furthermore, I am in favour of the International Monetary Fund, the World Bank, the World Trade Organisation".

Oh dear. Not what you want in control, given that we're well into the last 'doubling'time of them all.

Ultimately, if landlords can't recoup, they'll pass it on to tenants. The same ones being made to work for less (sorry, be more productive, silly me), the same ones going to be expected to add a profit payment to their power-bills, and for whom needed commodities - food, water, energy - will cost ever-more. And who presumably will still be taxed.

It was Mac, wasn't it? The turtle at the bottom of Yertle's stack?

PDK, the NZ middle -class has an endless stream of money... if the Nats assume, then it must be fact. I say keep squeezing the uslesess bastrds until the pip squeaks, then squeeze a whole lot more. It's time the middle-class realised it's not about them, but about making the the rich richer! And so it should be, who else is going to buy expensive French brandy?

chuckle.

It's gotten way past that. You don't keep a growth-requiring system afloat pandering to 1% of the population, when you're geared up for economies of scale. It's a fiscal oxymoron.

I'd say the middle class is quietly worried, and consolidating itself flat out. The folk through here are all on the intelligent side (regardless of what they do for income - doesn't seem to matter) and none are about to lash out.

I'd say the Nats know we're about to see the real global crash (we saw an extend and pretend, but not a fix) and that compared to their current take - and current account deficit - things are about to get very very worse.

Does David Shearer have any fresh ideas , such as a looksie at the land tax concept ...

........ or is NZ Labour sticking with the CGT policy , which worked so well for Phil Goff ?

Maybe the key to incentivise savings and investment and further disincentivise property investment is for the financial sector to get its act together.

The reality for many property investors is the hard work involved in directly investing in property, the risk of bad tenants, and a return not significantly better than many other investments still far outweigh the negative perceptions associated with managed funds and listed companies. When will the financial sector start to realise that they need to ensure realistic returns for investors and address the insane salaries of many CEO and senior managers, over inflated management fees, and a culture and practices of which Hotchin et al are just the tip of the iceberg.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.