Here is a fun fact: Europe hosts half of the number of systemically important banks.

The Financial Stability Board once in a while publishes a list of banks that are Global Systemically Important. These G-SIBs, 29 in total, are too big to fail and because of that designation they need to hold more capital than smaller banks.

European banks dominate the list of G-SIBS. Only seven European countries host these mega banks: France, the UK, Switzerland, Germany, Spain, Italy, and the Netherlands. There are thirteen European G-SIBs and I am sure you know some of them: BNP Paribas, Barclays, UBS, Deutsche Bank, Santander, Unicredit, etc. The US hosts only eight G-SIBS. JP Morgan Chase is the largest G-SIB and well-known. But I wonder if you know some of the other US-based systemically important banks: State Street? Bank of New York Mellon?

Another fun fact

Why is it that Europe hosts a large number of very large banks? Well, here is a second fun fact. The European G-SIBS owe their size largely to a single, obscure article of the European bank rules. Article 49 of the European Capital Requirements Regulation allows banks to expand: Expand into the insurance business and expand into other countries.

An infinite chain of banks

I hear you thinking, “What is wrong with banks expanding into other lines of business and into other countries? If British Petroleum and Unilever can sell oil, grease, and fat in various liquid and solid forms and operate on a global level, then why wouldn’t banks be able to sell a variety of financial products to an international clientele?” The answer is that banks that expand are risky. Banks are highly indebted and if they set up shop in a different country they do so with borrowed money: deposit money, your money. Now, if a bank like Santander can start a bank in Chile, there is nothing that prevents the Chilean subsidiary to expand into Peru. The Peruvian Santander subsidiary can expand into Bolivia and the Bolivian subsidiary could expand into … New Zealand. And so on.

Such an ever-expanding bank group, of course, is very risky. If all the Santander subsidiaries are wholly owned by their parent banks, then the owners of the ultimate parent holding bank, in Spain, bear all the risks of all these subsidiaries. That is a significant risk for sure.

Europe’s soft penalty for owning other banks

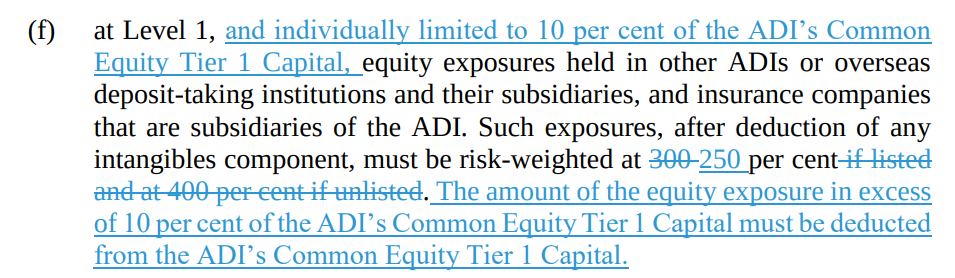

Luckily, bank regulations limit the risk of ever-expanding bank groups. The limits, however, vary across countries. The European limits in Article 49, for example, are very soft. So soft that it led to major controversy at the Basel Committee when it discussed the Basel III post-crisis banking rules. In the battle against too-big-to-fail banks, the US insisted on imposing strict limits on bank expansion. But France threw a major tantrum. Eventually, it got its way, thanks to, among others, Danièle Nouy. The resulting European ‘penalty’ for owning a bank subsidiary is a 250% risk weight. This is low. For example, New Zealand banks face a risk weight of 300% for shares they hold in listed companies.

By now you should understand that a simple rule can have profound effects on the global banking landscape. European banks dominate the G-SIB list because they benefit from a rule that allows them to expand. The US bank rules are stricter, which results in a diminished global presence.

Why APRA’s recent rule change matters

On 15 October, the Australian Prudential Regulation Authority (APRA) proposed a change in the rules on bank holdings. This rule may affect the Big-4 bank subsidiaries that operate in our country. Among the rule changes proposed by APRA, this one is important:

APRA wants to impose penalties on banks that own other banks. Instead of applying risk weights, APRA wants to impose a much stricter regime on bank holdings. It wants Australian parent banks to fully deduct (from their own equity) the amounts they hold in subsidiaries. Without getting too technical, a deduction is about the same as a risk weight of 1,250%. Bank supervisors use deductions (or risk weights of 1,250%) to stop them from investing in assets that are deemed risky.

The consequence of the recently proposed APRA rule change is serious: a parent bank in Australia will hardly benefit from the growth of their bank subsidiaries: an additional dollar held in the form of equity in a subsidiary will no longer contribute to bank capital of the parent. Owning a New Zealand bank becomes almost … pointless.

Tall poppy syndrome

The tall poppy syndrome thus ensues: the proposed APRA rule discourages the growth of New Zealand subsidiaries, in particular when these subsidiaries are large relative to the parent bank. This is the case for ANZ.

In the short run, the New Zealand subsidiaries respond to the rule change by paying any excess cash to their parents. This is because the parent does not have to hold any capital against cash holdings (a zero risk weight means zero penalty), whereas a dollar held in an equity holding is fully deducted (and fully penalised). I am not sure if the Reserve Bank likes it when the New Zealand Big-4 banks repatriate cash to their Ozzie parents. Likewise, the New Zealand subsidiaries may move some of their business to the Australian-owned branches that operate in New Zealand. Again I wonder if the RBNZ thought about our banks surrendering control of assets to Australian banks.

A bad deal for the New Zealand financial system

The APRA rule change could also make the New Zealand bank market less competitive: ANZ clients may want to choose to do business with locally owned banks - which may not be ready to properly serve their growing customer base. Just look at UK contender banks, according to the Financial Times these are all suffering. Size matters in banking.

The result of the collaboration between the RBNZ and APRA on the proposed rule change is that the New Zealand Big-4 have been given a bad deal. Except for the US maybe, many other countries are more accepting of allowing banks to grow internationally. The New Zealand Big-4 banks now face limits to growth. This is perhaps sensible in the battle against too-big-to-fail. But a recent Basel Committee study shows that victories in the battle against large banks come at a price: their profits suffer, which constitutes a risk for financial stability.

Ultimately, the Australian parent banks may start to retreat, shrink, or divest their subsidiaries. The question then is: which banks will grow into the New Zealand market?

Selling out to European banks?

European banks are in a good position to benefit from the proposed APRA rule changes. Facing virtually no penalties for holding foreign subsidiaries, the likes of HSBC, Barclays, and Unicredit may want to expand into New Zealand. That could make the market more competitive. Maybe.

However, the idea of European banks entering into the New Zealand banking market worries me. European banks are hardly profitable. They may want to use the New Zealand market to prop up their loss-making European operations. I wonder if that is a sensible idea. To put it more bluntly: do we fancy Deutsche Bank operating on our turf, so that the people of New Zealand can support Deutsche’s floundering operations in der Heimat? I doubt it.

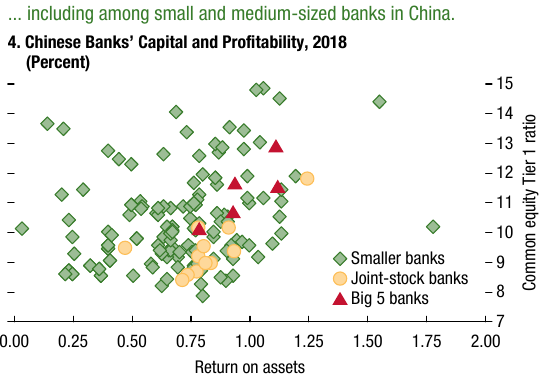

Some pundits think that Chinese banks may start to expand into our financial system. Perhaps, but such expansion hardly offers peace of mind. The latest IMF Global Financial Stability Report just documents how vulnerable Chinese banks are.

In all, it is likely that the proposed APRA rule change will alter the New Zealand banking landscape for good. It will become safer for sure, but the question is if the enhanced resilience of our banks will render the market more competitive. That is not obvious to me. Business may move to local banks that lack the capacity and expertise to deal with the needs of new customers, or business moves to banks that need profits to survive, which is a questionable proposition for sure.

Anyone out there who can explain what’s wrong by being owned by unquestionably strong banks at just four hours flying distance from Aotearoa?

*Martien Lubberink is an Associate Professor at the School of Accounting and Commercial Law at Victoria University. He previously worked for the central bank of the Netherlands where he contributed to the development of new regulatory capital standards and regulatory capital disclosure standards for banks worldwide including Europe (Basel III and CRD IV respectively).

17 Comments

The answer is that banks that expand are risky. Banks are highly indebted and if they set up shop in a different country they do so with borrowed money: deposit money, your money.

I am not sure that applies - the US G-SIB I worked for in London had no interface with the Bank of England, offered no transaction banking facilities to the English public and as far as I know funded it's US operations from London with eurodollar credit creation factors. The US head office had a single branch office open to the public in Manhattan. Nonetheless, this bank proceeded to swallow Chase Manhattan Bank and later JP Morgan.

My story about the risk refers to the risk of double leverage. It is a risk identified by all regulators. Obviously there are risk mitigants, and banks and regulators manage that risk.

Quoting from the article :

The APRA rule change could also make the New Zealand bank market less competitive

The likes of HSBC, Barclays, and Unicredit may want to expand into New Zealand. That could make the market more competitive. Maybe.

In all, it is likely that the proposed APRA rule change will alter the New Zealand banking landscape for good. It will become safer for sure.

Unquote :

A bit confusing, but the fact is New Zealand is not going to get any home grown competion to the Big 4. It has to come from overseas only.

As long as the APRA rules make the banking scene here safer for the customers/depositors by strengthening the capital/reserves, which our own RBNZ is also attempting to bring, it is a welcome development.

Competition ? Hasn't happened seriously, may not in the near future.

"A bit confusing", I agree.

"The New Zealand subsidiaries may move some of their business to the Australian-owned branches that operate in New Zealand."

I am trying to figure out which Aussie banks here have branches, as opposed to subsidiaries; Branches and Subsidiaries being different things.

https://keydifferences.com/difference-between-branch-and-subsidiary.html

"I am trying to figure out which Aussie banks here have branches, as opposed to subsidiaries"

The big 4 Australian owned banks in NZ are all operating as subsidiaries in NZ.

https://www.rbnz.govt.nz/regulation-and-supervision/banks/register

Off the top of my head, HSBC in NZ is a branch of an offshore incorporated banking entity.

If they're a branch of an offshore banking entity, then they are not regulated by the RBNZ. Hard to imagine that happening in NZ with the big 4 banks operating in NZ. If that happened, that would mean the key regulator would be APRA. Look at what happened when there was an offshore regulator of a local lending operation with BCCI in the 1990's.

If you notice, HSBC is not on the list of banks supervised & regulated by the RBNZ.

HSBC is listed. It's under its full company name "The Hongkong and Shanghai Banking Corporation Limited". You are right in that it is operated as a branch.

My mistake. HSBC is on the list with a (B) denoting branch.

Interesting about ANZ Group which has 2 operating entities on that RBNZ list

1) ANZ Bank New Zealand Ltd

2) Australia and New Zealand Banking Group Limited (B)

Similar with Commonwealth Bank Group

1) ASB Bank Limited

2) Commonwealth Bank of Australia (B)

Westpac Group:

1) Westpac New Zealand Limited

2) Westpac Banking Corporation (B)

A change for good to my mind - I'd love to see our local banks expanding their customer bases.

A good article. The outlook doesn't look good for NZ banking customers. As to local banks stepping into the gap, I don't think so. Did the nationalistic thing for a while and put my business with the bank created by NZ politicians. They were OK for the plainest vanilla services but were just awful for everything else. I've returned to an Australian owned bank with no regrets.

To the Aussie bank bashers be careful what you wish for. We have a well functioning banking system with banks that held firm with minimal government assistance during the GFC. That's not the case with the European banks and it seems they are the laggards post-GFC. As for the locals, you might be badly disappointed if we have to rely on them to fill the gap.

It seems 2008 overshadows 1987? It shouldn’t! The latter saw the demise of the BNZ and all the Australian Banks represented here took severe, major hits. From that dawned a whole new financial landscape. The trading banks set about recouping from their sitting duck type current account holders and escalation of charging for every day services, fees in other words, just got strapped to a rocket. Then the rise and rise of the second tier, ie finance companies for the risky speculative stuff. RSL should have given due warning but it didn’t. In the good old days we had five solid trading banks, savings banks and building societies. Then popped up Trust Bank, ASB, Countrywide, United and Post Bank. Where have all the flowers gone?

Interesting stuff alright, not that I fully understand it, but the gist is (I think) that the regulators (APRA) are trying to make their banks safer. Not so bad you would think? But watching the big boys in the US, Europe & now China play their games, as the article implies early on, all is not equal, which the writer suggests (I think) is for good reason. My own limited understandings also suggest this might be the case. But like all things there are two sides of the coin (3 if you count the round edge). Safe? Savy? Or both? One thing is clear to me this side of the GFC, the Americans seem to have the best of both (all) worlds, when they crash someone pays (Lehmann Bros, Bear Stearns etc) & they suck it up (like we're doing this week with the AB's). But they also seem to limit their bank wanderings around the globe, which also limit their liabilities in tough times (every decade or so) as well as being (now & before) the most profitable banks on planet Earth. The Europeans are so scared of their own shadows that nothing seems to change & they are, as a result, struggling (missed out completely?) on the up side over the past decade. The Chinese? Well Beijing prints debt & passes it round & orders the others to pass it around - or you will die. From my seat in the South Pacific China looks like the best ponzi scheme ever invented.

"the gist is (I think) that the regulators (APRA) are trying to make their banks safer."

Yes, I agree with you. The last thing APRA wants is their Australian banks having to inject a large amount of capital (relative to Australia parent bank capital) into their NZ subsidiaries (due to RBNZ increased capital on NZ banking subsidiaries), when the Australian banks need capital themselves. The Australian parent banks might need to retain capital, if there is a recession and loan losses pick up.

The NZ subsidiaries might need to retain capital or require a capital injection, if there is a recession in NZ and loan losses pick up. One way of getting a capital injection into the NZ subsidiaries without a capital injection from the Australian parent banks would be to sell some new shares in the NZ subsidiaries to the public to raise funds via a NZSE stock market listing. Not sure if sufficient capital could be raised though.

Nothing to do with tall poppies.

The answer is that banks that expand are risky. Banks are highly indebted and if they set up shop in a different country they do so with borrowed money: deposit money, your money.

I am not sure that applies in every case - the US G-SIB I worked for in London had no interface with the Bank of England and offered no transction banking facilities to the English public and as far as I know it largely funded the US operations from London with eurodollar credit creation factors. The US head office had a single branch office open to the public in Manhattan. Nonetheless, this bank proceeded to swallow Chase Manhattan Bank and later JP Morgan.

dont think the threat of other banks setting up here is a valid argument for letting the big 4 continue taking us for a ride.more like an argument for bringing them into line.

Yes, whats wrong is the amount of NZs income being drawn out of the economy by our cousins. NZ is perfectly capable of meeting domestic funding demand through NZ owned instititions. Banks siphon rentier profits from the productive economy. Better that those profits remain here to be reinvested for the benefit of us all.

Very interesting article. It doesn't discuss in much detail the >10% trigger on APRA's capital proposal, which I presume will strongly encourage the Australian Banks to cap their equity in NZ to 10% with any lending growth here no greater than that of the Australian operations so as to stay at 10%.

So the RBNZ's capital proposals require more capital in NZ, which pushes up the capital held, which then potentially triggers yet more capital deductions as a result of this. What is the cumulative impact on the ANZ from RBNZ/APRA proposals who are roughly 20% weighted to NZ? It must be pretty ugly.

The big 4 are all over the 10% cap. My story focuses on what happens at the margin: what is the value of an additional $ of equity in the NZ sub for the Oz parent? Very little!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.