Advanced economies have been experiencing decelerating growth for a number of years with projections that this will continue for some time. So much so, that many economic commentators have described low growth as the “new normal”.

The underlying reason for the declining growth rates is widely debated although some of the obvious culprits are the massive increases in global debt and the persistent decline in productivity.

Whether these are the cause of low growth or merely a symptom of a wider issue is unknown.

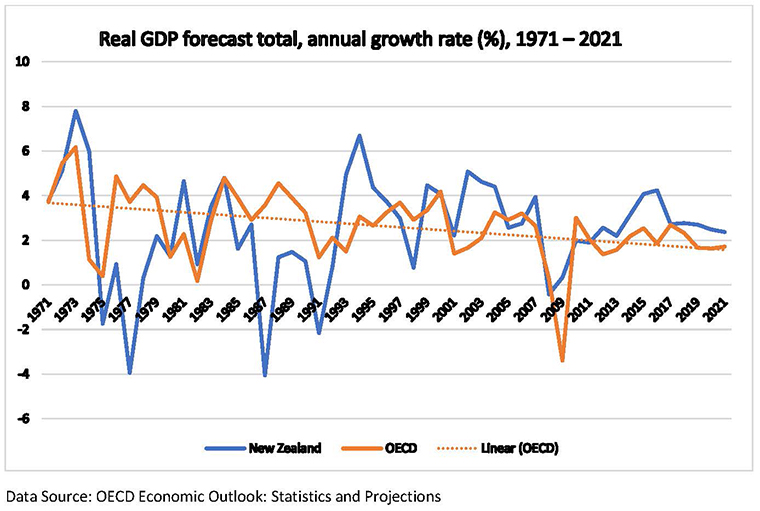

While it is often referred to as a recent issue, growth rates throughout the world have actually been declining since the 1970s.

The low growth theories

Some of the theories behind the slowing growth rates have included:

- Increasingly protectionist policies causing a slowdown in trade and manufacturing

- High levels of public and private debt

- Lack of investment at a company and government level

- Subdued productivity growth

- Growing inequality

- An aging population in advanced economies

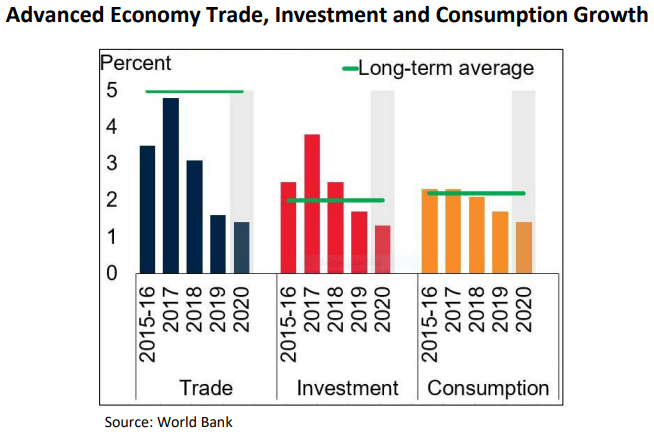

It is possible that all of these factors have a role to play. Certainly, if you look at the first three issues there has clearly been a significant decline in trade and investment, and also consumption since 2017:

A global avalanche of debt

Debt levels have been building around the world for the last 50 years. According to the World Bank there have been four “waves” of debt accumulation since 1970. The latest wave began in 2010 and is “the largest, fastest, and most broad-based increase in [emerging and developed economy] debt than any of the previous waves.”

One study has estimated that a country’s economic growth drops off significantly when debt reaches 90 percent or more of GDP. According to the study, countries with 60-90 percent debt have an average growth rate of 3.4 percent, compared to 1.7 percent for countries with more than 90 percent growth.

Currently the countries with the biggest public debt burdens – all over that 90 percent mark – include Japan, Singapore, the United States, and a good number of the European Union countries.

Private debt has also been accumulating at a great rate over the same period, but while increasing public debt can slow economic growth, it is only when individuals start deleveraging (and allocating more of their disposable income to debt repayments) that growth is dampened.

Falling or tepid productivity

One of the more concerning trends affecting most of the world in recent years has been the declining levels of productivity. Productivity growth has fallen globally from 2.3 percent in 2003-08 to 1.8 percent in 2013-18. And the impact has been broad-based, affecting more than 70 percent of advanced economies.

Many advanced countries have suffered from falling productivity for decades, a trend that has become more pronounced since the 1990s. This is despite rapid technological advancement over that period which is generally linked to higher productivity growth.

The reasons behind the declining rates of productivity are widely debated but there is little consensus. Productivity is an important piece of the low-growth puzzle as declining productivity results in a lower standard of living and is the most important determinant of economic growth.

Impacts of an aging population

Another important factor that tends to support economic growth is increases in the size of the labour force. However, a worldwide decline in fertility rates coupled with an aging population means these are unlikely to prop up growth in the future.

The proportion of the population aged over 60 is expected to increase in almost every OECD country between now and 2050. It’s likely that this will have a dampening effect on economic growth. However, according to the National Bureau of Economic Research, an aging population in itself only moderately slows economic growth. This is because it is generally balanced by people working for longer and policy responses such as increasing the legal retirement age.

Is low growth such a bad thing?

There have been calls in some quarters for a change of focus from the insistence on continued high growth. Low growth may mean people work fewer hours or use fewer resources, but that may not be such a bad thing. The flipside though, is that falling GDP means fewer resources are available to invest in education, infrastructure and social security. At a time of rapid technological advancements, low growth also means less investment is available, which in turn leads to slow capital investment in new technologies and infrastructure to support future growth. A low growth economy also means it is easier for countries to slip into a recession, which only compounds the low growth environment.

What can we do about it?

There are recent signs that the slowdown may be stabilising, however, the consensus is low growth is likely to stick around for some time.

While monetary policy has supported growth in recent years for advanced economies, including New Zealand, in the words of the IMF Chief Kristalina Georgieva “it will not be the saviour of economic growth”. In many cases, there is also not a lot of room to continue to cut rates in order to support weakened economies.

The best bet for the world is to solve the persistent productivity puzzle or to recalibrate, adapt and learn to thrive in a new low growth environment.

*Alison Brook is from the Knowledge Exchange Hub at the Massey University campus at Albany, Auckland. She is on the GDPLive team. This article is a post from the GDPLive blog, and is here with permission.

33 Comments

Yes...and its not hard to see why...Baby boomers retiring...population growth stalling...more debt than you can shake a central banker at...time to relax and enjoy life....while you can..

This is obviously Trumps fault.

Reinhart and Rogoff got savaged for their study that found that high public debt lead to lower economic growth. Now that high public debt is a fait accompli, are their findings being quietly accepted?

Hate using such an overworked metaphor, but aren't compliance costs the elephant in productivity's room? If you keep adding laws and regulations at the pace governments have been over the last ten years, surely this will affect productivity? No one talks about it. Maybe we are not allowed to.

To be fair there's a difference between constraining socialisation of cost of production and constraining productivity, it would pay not to conflate the two...

BS - there's been a lot of thinktankery funded by those who would short-term prosper, at the expense of everything/everyone else.

It is the limitations of a finite planet we are up against, much as you might like to blame some 'other'.

And productivity - given that labour represents less than 1% of work-done globally - is all about the efficiency with which fossil energy is applied to work. And that runs into the Laws of Thermodynamics. Sorry, you're looking in the wrong place.

Appropriate pen-name, but.

I agree. The state socialists are slowing strangling the workers & creators in the private sector with regulation beyond belief. This is not just a NZ phenomenom. Excessive regulations are strangling most western cultures as the big bad capitalists try to get away with murder (so they tell us). Somewhere in there is a balance. Another thought I had was the housing of the single person. The cost to house two people is almost the same as it is for a single person. As our relationships have decayed and many end up on our own, the full cost of the one person household is becoming very clear. It is very expensive indeed.

I was talking to a friend of mine last year. He said that one of his clients (he fixes PC's) was in his late 70's - his pension pays for his rates, insurance and his health insurance. If he wants to eat (or anything else) he has to pay for that out of his savings. That clarified my view that you buy a house that meets your needs not your ego - I pay lower rates for the same services. My sisters rates are twice mine - but she gets no more in terms of services - simply because she lives in a bigger house in perhaps a "better" part of town. That has reinforced my view to buy assets (shares / bonds in my case) that create passive income rather than a larger house.

Health insurance for someone in their late 70's would cost quite a lot I imagine. Most people of that age don't have health insurance and don't really need it in NZ.

As our property is mortgage free, we intend to postpone our rates of ~ $5,700 p.a. until we either sell or die. There is no reason why rates should force us out of our home.

Postponement of rates payments for residential properties

A rates postponement on a residential property may be an option, as long as you have the required equity in your property.

Criteria for postponement of rates

You must meet the following criteria to be considered for rates postponement:

You must be the current owner of the rating unit and have owned the property for at least two years.

You must use the rating unit solely as your residence.

The postponed rates will not exceed 80 per cent of the available equity in the property. The available equity is the difference between our valuation of the property at the most recent revaluation and the value of any debt against the property if you have insured the property for its full value.

You or your authorised agent must apply.

Conditions of postponement of rates

We recommend that you ask for advice from a financial adviser on the impact of postponing your rates and if it is a good option for you.

We will postpone payment of the residual rates (what is left after any optional payment) if you meet the criteria.

We may add a postponement fee each year to the postponed rates. The fee will cover the period from when the rates were originally due to when they are paid. The fee will not exceed our administrative and financial costs of the postponement.

The postponement will apply from the beginning of the rating year when you apply for postponement, although we may backdate the postponement application, depending on the circumstances.

Once the postponed rates are equal to, or greater than, 80 per cent of the available equity in the property, no further rates will be postponed. Any postponement will apply until one of the situations listed below occurs, at which time the postponed rates (and any postponement fee) will be immediately payable:

on your death

you no longer own the rating unit

you stop using the property as your residence

a date set by us in a particular case.

You can pay all or part of the postponed rates at any time.

You can choose to postpone a lesser amount of rates than the full amount that you would be entitled to postpone under the policy.

Postponed rates will be registered as a statutory land charge on the rating unit's title.

For the rates to be postponed, we will need evidence each year, of your property insurance and the value of debt against the property, including mortgages and loans by way of a statutory declaration or declaration.

Interesting comment, LJM. There are many effects government has on business, but, to my mind, one of the biggest drags on wealth creation is central and local governments assuming they have a direct role in this pursuit. Because they then blunder around in what they take to be the fields and influences of wealth creation, they start to see themselves as entitled beneficiaries of any such achievement. And seeing themselves as both causes and beneficiaries of wealth creation, they then help themselves to greater and greater amounts of what's created - and squander vast amounts of this - whether or not they have, in fact, had any positive hand in progressing productive enterprise. Visit any small centre in New Zealand and marvel at the lavish offices and other accessories that local councils and their client organisations provide for themselves. There are very rarely any businesses in the locality with facilities to compare with these of their tax-masters.

It’s nothing more than theft by bureaucrats with a sense of entitlement.

Its neoliberalism that is to blame. The retreat of the 'state' has been a steady feature since the early 1980s and has increased in momentum till the present day. Like it or not the state is the biggest conglomerator of spending power and if it is declining due to diminished tax take etal then it is surely going to drag the growth potential of an economy down with it. Corporations don't buy many aircraft carriers or submarines...or fund entire education systems...

Your bias makes your comment pointless, the facts get in the way of your story:

NZ Tax Revenue % of GDP show a massive spike in mid 80's from 28% to 36%. It was back at 28% in early 2000's but growing, dropped again after the GFC, and now recovered to?? 28%. Household debt is a problem, and government $ spending grew steadily throughout, even when GDP growth was low with a couple of 1-2 year exceptions. We gotta manage our spending.

Link: https://tradingeconomics.com/new-zealand/tax-revenue-percent-of-gdp-wb-…

OECD data on Tax to GDP ratio (obviously slightly different data set) also disagrees with you: since 2001 OECD average has sat around 33%, dropped 1% after GFC then lifted 2%, so above 2000's. NZ data for the same period hit 36% during the previous labour govt, dropped at the GFC to 30% but now back to 32.7%. Search "Revenue Statistics 2019 - New Zealand - OECD.org"

Where is the massive decline in government tax take you claim to be the cause of declining world growth, perhaps you should be blaming government spending priorities instead.

From 1990 to now public debt went from 50->20% of GDP. Private debt did the opposite jumping from a low base to ~90% of GDP. NZ now has one of the lowest public debt to GDP ratios of all the developed nations.

Seems to me like an inevitable result of *too much* capital in the system. No matter how much extra productivity is available, when there's too much capital around, those opportunities for growth will be snapped up -- and because there's so much capital seeking a return, the price of those growth opportunities will be very high, as we see in the current equity markets. When the price of your investment is high, it's hard to actually make a profit.

The problem is that we've structured a lot of things, like pension schemes, around the assumption that reasonable rates of return on capital are natural and inevitable... but in the process, we've flooded the financial ecosystem with so much capital that the very returns we were assuming are undermined.

I agree, I have for a longtime now been saying that saving for retirement is a bad thing...infact retirement altogether is a bad thing...stop working you lose your mind to dementia from lack of challenge.

"'stop working you lose your mind to dementia"' - probably true because after retirement I started reading and making comments (sometimes in the reverse order).

So let's sort how we prosper without damned growth, for crying out loud. This is a GOOD thing in a world that needs us to stop destroying and using it as if we have a spare planet in the cupboard under the stairs.

New Zealand is addicted to low quality growth and successive governments continue to use high levels of immigration to prop up such growth. All the while productivity lags and GDP growth per capita is near non-existent. So the growth we're getting is hardly making us prosper.

It's not just us

Yes to this, PocketAces. The problem, though, is to square any kind of steady-state with growth-dependent debt. Perhaps we'll recognise that the creation of money is actually creation of debt, much of which can never be redeemed. So we are imprisoning ourselves while imagining that we are gaining an increase of freedom.

"Whether these are the cause of low growth or merely a symptom of a wider issue is unknown"

Bollocks.

It's been known and examined and written about for years. Here, by me and others, for one.

We are cresting over the top of the Limits to Growth graph. Economists may well be confused, as may all those who believed them, but this is a physical world, energy-driven. Had to peak hereabouts.

https://dothemath.ucsd.edu/2011/07/can-economic-growth-last/

read it and weep - and ask Interest.co why, with all it has had put in front of it, it still puts this stuff up? .

NZ can still pack in a lot more people to keep our economy growing (albeit via low quality growth) hence our lazy governments driven by their sponsers will keep doing what they're doing until the wheels fall off or we all say no.

Indeed. Thats why the COL is the govt.

Indeed.

What would be great would be for the author of this article to be challenged to rebut the analysis of Tom Murphy in that link, if indeed as an economist she still wants to claim there are 'unknowns'.

While monetary policy has supported growth in recent years for advanced economies, including New Zealand...

If author is going to assert this main stream assumption rather than challenge it, I would think the majority of Interest commentators have more insight, at least collectively, into this problem than the she does.

I think low interest rates, QE and high risk weighting on business loans have a lot to answer for. The main issue with these is it disincentives making a profit with your business or starting a new one to do so. The get rich scheme is to get people or entities pay you ever larger amounts of money for your assets (regardless of if your a property investor or CEO with stock options) with the likely that the buyer will be able to on-sell the same asset for more later. Someone actually starting a business and trying to make money of its profits is going to struggle to make anything like what the asset traders are making and ultimately question if it was worthwhile.

“While it is often referred to as a recent issue, growth rates throughout the world have actually been declining since the 1970s.” - Gee, I wonder what could have happened then that made unproductive assets more attractive than productive investments.

Since the 70s compare the global gradual increase in minimum wage & working conditions to the global gradual decrease in productivity. Probably make a nice symmetrical "X" on a graph I'd imagine.

see my reply/post above.

If labour is less than 1% of the work done on the planet, labour productivity is 'noise'. It's not the digger driver, it's the digger by 99:1, and all you can do is make the digger more efficient. As we have nudged up against the thermodynamic limits (see my linked article above) the remaining margin for future improvement, declines. Economics is away back with Adam Smith. It's the Invisible Fuel-Injector, now.

Greed will always find the way, right now it's pushing the world to realisation that 'efficiency/cost cutting' more $ to keep in elite's pocket.. let's put/push the productivity to the largest Nation population on the planet..a bit coughing eh? right now with this nCov19 - next target? similar excuses? India, Brazil, Indonesia or back to USA? hmn...Reset is not desirable by those ruling elite, so? pass it on for generations to come, reset the starting point from the negative interest territory...Leave it to those next century problem somewhere else, problem is.. with that sort of mindset? you don't have to wait too long. It's door knocking now.

Alison

I see no mention in the theories list of decreasing net energy .

This has a considerable following showing strong correlation with declining productivity and compensatory increase in debt. It has good explanatory power to interprerate what we see.

There is a large literature see Hall, Jackson on de growth and blogs such as Morgans net energy surplus.

It makes sense to me that the fossil fuel economy is now acting as a drag on the world economy pending the required restructure

Economic textbooks are the only reliable source of what is causing low growth ..........

The main cause of low economic growth is weak aggregate demand. ... If slower growth is due to weak aggregate demand (e.g. due to low confidence, over capacity ,and weak purchasing incentives ) then the low growth rate will give similar effects to a recession.

I would suggest that there is some deflation underlying the general unequal / erratic fall in commodity prices .

The lax monetary policy we have by the US Fed and most other central banks is on purpose. The Fed, like most Central Banks, is too afraid to raise interest rates. They want to keep the good times rolling. Or at least, the good times in the stock market rolling. Sooner or later all good things must come to an end - IMO when it does, it’s not going to be pretty.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.