In uncertain times, people tend to save more. In 2020, with the pandemic raging and people concerned about both their health and their jobs, it’s not surprising that people spent less and saved more.

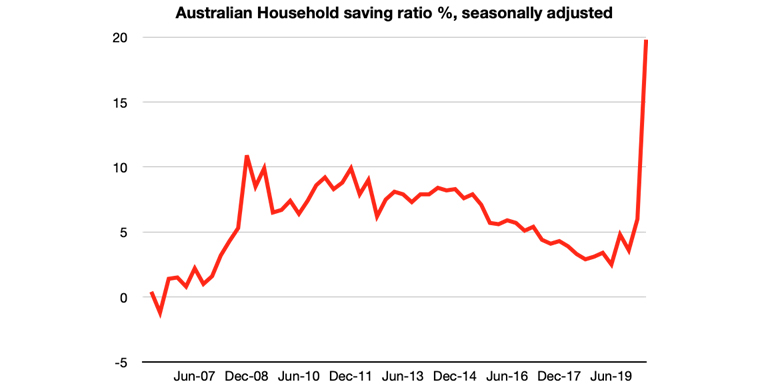

In Australia, the household savings to income ratio increased to a whopping 19.8 percent in the June 2020 quarter – up from 6 percent over the previous quarter. Even by March 2020 that saving ratio was starting to increase (up 2.4 percent from December 2019):

Source: Australian Bureau of Statistics

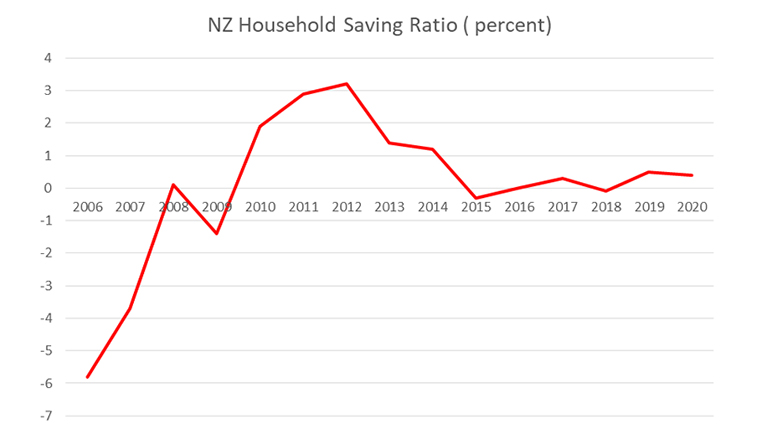

By contrast, according to Stats NZ, by March 2020 NZ households were saving less than the previous year, with Kiwis spending all but 0.4 percent of their disposable incomes.

A 2019 analysis by finder based on OECD data showed that New Zealand was in the bottom five countries for saving. It ranked number four, just ahead of Lithuania (-4.74 percent), Finland (-2.58 percent) and Spain (-1.94 percent). Switzerland took the top spot, with a household savings rate of 17.64 percent, followed by Sweden (16.43 percent) and Luxembourg (13.41 percent).

New Zealand’s poor showing is not a recent development, as in 1998 it ranked in the bottom three of OECD countries, just ahead of Denmark and Latvia.

Source: Stats NZ

Too much saving is not regarded as a good thing since consumption is such a big driver of economic growth. However, our persistently poor savings record puts New Zealanders in a very vulnerable position should they lose their job (or if interest rates were to rise).

Another recent survey by finder revealed that four in 10 New Zealanders have no emergency savings to fall back on. And only one in five Kiwis would be able to cover their living expenses for just one week or less if they lost their job.

The OECD data shows that households in the most-thrifty countries save on average 10 percent or more of their disposable income. While exact comparisons between countries can be problematic there do seem to be countries that are consistent “savers” while others tend to be “spenders”. Global Finance magazine points out “These ratios are important in a larger sense: how much people tend to save also affects a country’s tax planning strategy, its welfare provisions and social policies.”

Houses, again…

Unsurprisingly, given the county’s focus on housing, New Zealanders are great borrowers. According to Stats NZ households borrowed $10.2 billion in the March 2020 year, amounting to approximately $2,000 for every person in New Zealand.

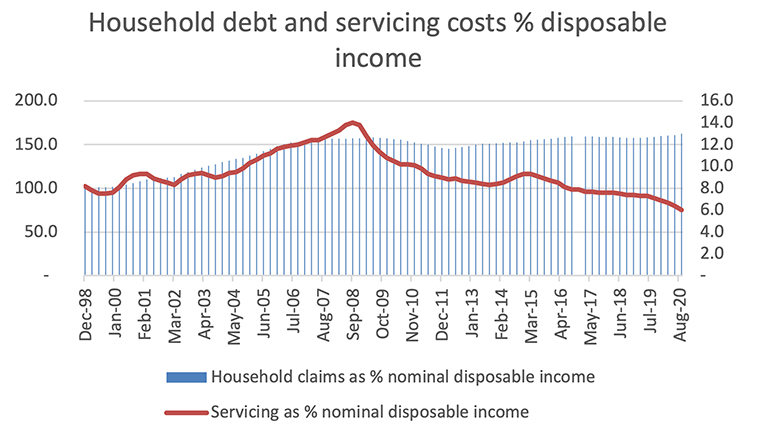

Net borrowing represents the difference between saving and investment and New Zealand households have been in a net borrowing position since 2013. However high levels of debt do not by themselves explain the poor saving rates as debt servicing rates have trended down over the same period.

Source: RBNZ

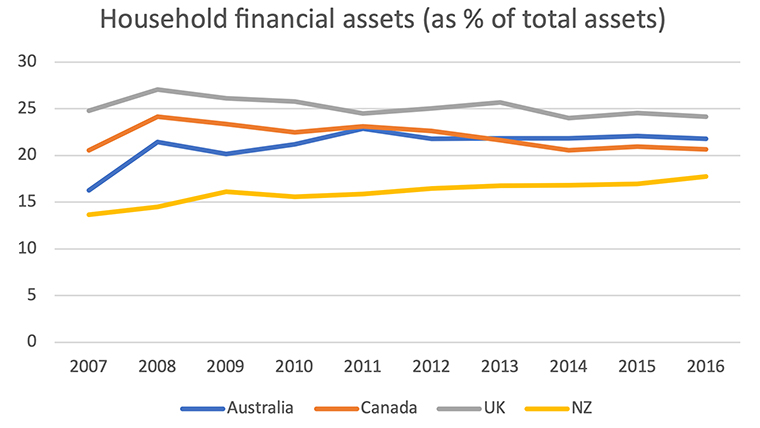

According to a Reserve Bank report from 2007 (just as KiwiSaver was introduced), New Zealanders spent similar proportions of their disposable income on housing as households in Australia, Canada, the UK and the US. However, they invest less in terms of financial assets.

Source: OECD

Investment in property has traditionally been preferred over other financial assets. However, this doesn’t account for the lack of saving for many groups. According to Stats NZ homeownership rates for younger people have fallen significantly since the 1990s and declined slightly for those aged 60 years and over. Overall homeownership rates are lower than they had been in 70 years according to the 2018 Census.

Are our incomes too low for us to save?

Low income, or low disposable income, does not seem to be a predictor of saving. Some of the lowest-income countries have the highest rates of saving. New Zealand’s incomes sit in the middle of OECD countries (17 out of 34 countries) when adjusted for purchasing power. In terms of disposable income growth, we rank equal with Australia. According to Stats NZ, our net disposable income increased 4.6 percent in 2020.

So why don’t we save more?

The RBNZ report suggests that for people on lower incomes, being able to access universal superannuation at aged 65 years is probably a factor.

Although debt servicing costs have fallen significantly, debt has also been easier to accumulate through mortgages, credit cards, and “buy now, pay later” facilities. All of which may have made it easier for us not to save.

Other than that, the RBNZ article pointed to a variety of other reasons which may account for New Zealanders reluctance to save:

- Student debt creating a culture of “debt acceptance”

- Lack of a saving culture in NZ and the lack of investor role models

- Low levels of financial literacy about products other than property

- Reluctance to seek external financial advice

- Pressures to consume.

Tax Incentives for Saving

As Milford Asset noted in 2017, many New Zealand households believe they will achieve a comfortable retirement based on their savings plus NZ super. However, they may not reach this goal without significantly increasing their contributions.

They proposed allowing people to make tax-deductible contributions (or contributions out of pre-taxed income) up to a certain amount each year. This has been the approach taken in Australia, the US, the UK and Canada – all of whom have a higher savings rate than New Zealand.

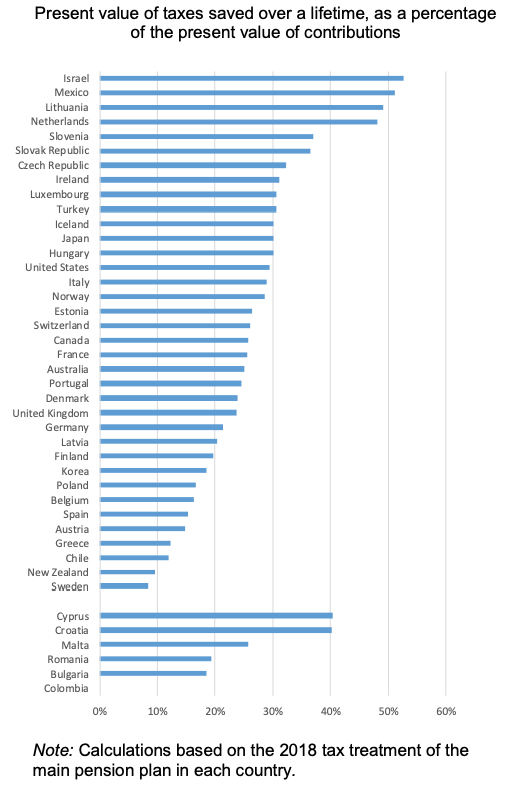

In 2018 the OECD reviewed the literature on the impact of financial incentives on retirement savings. They found tax incentives had been effective tools to promote savings for retirement, particularly for middle to high-income earners. While less effective for low-income earners, they do seem to increase their overall savings.

The publication also noted that while Kiwisaver (at that stage) had been a success in terms of participation across all income groups it has had a negligible effect on national saving.

Tax Advantage provided to an average earner

Source: OECD Financial Incentives and Retirement Savings

Having sufficient financial savings to meet lifestyle goals is not only objectively a good idea, it is also linked to improved mental health and wellbeing.

Given that New Zealanders are currently not saving enough to achieve day-to-day financial resilience, let alone for their retirement, the time may be right (if not overdue) for the government to consider using tax incentives to boost household savings. Doing so may be the only way Kiwis will be able to achieve the lifestyle they aspire to in the future.

*Alison Brook is from the Knowledge Exchange Hub at the Massey University campus at Albany, Auckland. She is on the GDPLive team. This article is a post from the GDPLive blog, and is here with permission. The New Zealand GDPLive resource can also be accessed here.

41 Comments

The RBNZ report suggests that for people on lower incomes, being able to access universal superannuation at aged 65 years is probably a factor.

Indeed: the weekly couple pretax payment set at $768.92 annualised requires a $19,991,920.00 deposit earning the ANZ Serious Saver 0.2% p.a. rate to replicate it.

Audaxes,

I doubt that. Most Kiwis would simply not be able to make that calculation, which is sad.

WOW when you put it like that it show how wacky things are getting.

The big question now is will we return back at somestage to longterm average or will things keep getting twisted to keep everything in a bubble while we devalue anyone holding cash and how long till we start to face Venezuela type problems.

When you look back in history Venezuela used to be top10 richest country and now look at them.

I think this is hardly about choices, surely people on lower incomes simply do not have the disposable income to make saving a valid exercise. Saving cash while assets go to the moon is not going to get them anywhere even if they were able to.

I think national super argument is a distraction, its just a benefit, banish it now and all retirees would simply convert to unemployed benefits or similar.

Wow - I had never thought of superannuation like this. More reason to encourage people to self-fund their retirement and means test superannuation. Thanks Audaxes.

Seriously the author believes that an ANZ banking survey provides scientific evidence of improved mental health and wellbeing

" it is also linked to improved mental health and wellbeing."

Another recent bank survey shows that eating too many Easter eggs can be damaging to happiness.

Everything successive New Zealand governments do encourages people not to save, but to buy houses. KiwiSaver was intended to encourage people to save (for retirement). But the [insert brand] Government, and everyone else, knows that house prices rise faster and more certainly than most PIE funds. So the first-home buyer can, and indeed is encouraged to, withdraw from KiwiSaver all but $1000:

your contributions

your employer's contributions

the government contribution

interest you have earned

fee subsidies (if you got these).

And on top of that, there can be a $10,000 Government kickstart to buy one's first home.

How would that $10,000 Government grant fare if, instead, it were used to kickstart every 18-year-old's KiwiSaver by locking it into an aggressive fund till the age of 65, and were augmented by at least prohibiting (again!) the withdrawal of subsequent Government contributions and fee subsidies? Go one step further, and stop taxing that KiwiSaver (Hey, just like a house) and see how it runs!

What would Occam say Alison?

Perhaps:

"Raise interest rates, and people will save more and borrow less"?

Any tax change is just waving the starter's flag for the accountants, lawyers and assorted liars of the land.

Is this a late April Fools joke? The RBNZ has lowered interest rates on deposits to an all time low and there is even a question why people aren't saving. My TD matures next week and I won't be putting my $'s back in the bank at 1.0%.

But households are saving, even at banks. In the year to February (and therefore through the pandemic), household balances at banks rose by +9.3% to $201 bln, an increase of +$17 bln. That is far more than earnings rose. True, they are no longer saving with interest-bearing accounts. And perhaps, in an unexpected way, that is encouraging saving? If you can't earn interest, and if the background economy is dodgy, the thinking may be you had better put an increased amount of your income aside for a rainy day. The evidence is strong overseas too. In Denmark where they got negative interest rates for a while, bank account savings rose faster in this period, not slower.

It seems a negative incentive (uncertainty) is an even better motivator for saving than a positive one (higher interest rates).

Yes but term deposits reduced by $23b in the last twelve months....kiwis are saving but not committing these funds to the banking system...lendin short to the banks who then lend long if this accelerates we are in big trouble

Yes but term deposits reduced by $23b in the last twelve months....kiwis are saving but not committing these funds to the banking system...lending short to the banks who then lend long.... if this accelerates we are in big trouble

Dp

You'll have better access to the info than me, but how many of those savings are Off-Set Loans? Or Fully Drawn Advances waiting to be applied?

I'll suggest my Offset Account Balance earning net 0% p.a, even in reduction, is counted as savings, when in fact it's just backing a residential property mortgage - an increase in the stats on both sides of the national balance sheet.

As I've repeated suggested NO ONE should be paying down debt when it's this cheap; no one. In fact, we should all be borrowing every cent any lender will offer us and NOT spending it.

If you have spare liquidity, save it - offset it if you can - and keep your powder dry.

The trouble is, many are 'saving' their current and future money in non-liquid asset speculation, as well as 0% bank accounts.

WHEN things toughen up, lenders won't be keen on lending, and it's then that stored cash; drawn facilities, becomes valuable.

When banks purchase a borrower's loan contract (promissory note) they credit their IOU's, masquerading as deposits, into his or her account.

Not surprised. Overseas research (somewhere in Scandinavia I think) indicates that lowering the OCR encourages higher saving levels, which is totally counter productive to it's intentions. Apparently people (particularly those on fixed incomes) feel vulnerable and save more to protect their income stream. As I have been saying for years now, for this and a bunch of other very obvious reasons; the RB model that lowers the OCR as the CPI lowers is very flawed. So much so, that I find it hard to believe that those who formulated the policy did not know exactly what they were doing.

David people are not saving in the true sense of the word. People are in debt up to the eyeballs so its not savings, its an emergency fund if your able to scrape it together in case your job suddenly goes tits up I don't call that savings. Savings is when your debt free and have money in the bank. Up until now its been pointless saving because you want to put the money against your mortgage. What's the point in saving when your earning less than what the mortgage rate is AND your getting taxed on it as well !! Perhaps if the government stopped taxing the crap out of your savings it may be worth it but with the current TD rates its all a total waste of time saving anyway. The only place to get a decent return is to buy a house......

Waive tax on the first $10k received as interest from deposits (all kinds) with Banks here in NZ. That would be a good place to start.

Another false dichotomy by dave chaston..

The reason why banks are full of deposits is because they are creating mega amounts of credit to fund asset inflation. You make it sound that mum's and dad's are depositing record amounts of money into the banks. Why would they when money is pretty much worthless.

Money is not worthless and I think I would rather have a few hundred thousand in the bank than nothing.

Yeah, this idea that money is "worthless" is quite mad.

Not "worthless", just on it's way to eventual collapse due to the constant debasement that is going on. So not "worthless" yet.

It will never be worthless, what will happen is at the time of the collapse your fiat will be converted to a digital currency and no it will not be Bitcoin. All Money apart from Gold is created out of thin air. Governments just look at the total dollars in circulation and digitize it and the sensible thing would then be to cap it like Bitcoin. Bitcoin doesn't work, you cannot have a currency that gets "lost" thats simply is not going to work.

When the RBNZ have have told us not to save, but to spend, to take on debt.

You expect Kiwi's to save, not a chance in hell..in a million years. Just saying.

You have to have disposable income to save. A great many Kiwis are living hand to mouth and having to sacrifice a lot to do that.

If you have some disposable income and could save for a house, what is the point? House prices rise at a rate nearly orders of magnitude greater than many more could ever hope to save. Adern has publicly stated that this ever increasing house price rise regime will be preserved, so you may as well enjoy life or get out of NZ to somewhere you have a realistic chance of getting ahead. Any savings should be directed to getting out of NZ.

Even those with their own homes may well be better off selling at these prices and take off overseas where houses are cheaper and wages higher. I very much doubt that they would be worse off financially.

House prices are now so high that only a small number of people could ever hope to pay them off in their lifetime working in NZ.

Get real!!!!!

A good explanation of how sectoral balances affect private savings here. He tells us " In order to achieve a sustained level of net private saving, which seems to be important to the health of the domestic economy in a fiat money system, a country either needs to run a sustained current account surplus, or a government budget deficit, or a mix of both"

https://www.economicsjunkie.com/sectoral-balances-and-private-saving/

Thanks. A very interesting paper. It is going to take a bit of chewing over to fully appreciate.

For us to be able to save then there must be a source of money to save, and only the government can be that source when it runs budget deficits. NZ runs current account deficits which drain income from the economy and banks can only create assets and liabilities in equal measure so cannot add to our net savings.

Only the government can create 'net financial assets' for our savings. This is all explained by MMT and Sectoral Balances. Economist L. Randall Wray tells us this,

If the government always runs a balanced budget, with its spending always equal to its tax revenue, the private sector’s net financial wealth will be zero. If the government runs continuous budget surpluses (spending is less than tax receipts), the private sector’s net financial wealth must be negative. In other words, the private sector will be indebted to the public sector.’

It is impossible for the government sector and the private sector to run surpluses at the same time. If the government deficit provides the private sector surplus then implications for the economy should be clear. When we add in the third sector (Rest of the World) it can be seen that the three sectors always have to balance overall. In other words, as Professor Randall Wray points out, it demonstrates the ‘important accounting principle that the sum of deficits run by one or more sectors has to equal the surpluses run by the other sector(s)’. Therefore, surpluses and deficits will always add up to zero. As such, in a graphic representation, it will be easy to see that they balance identically as a mirror image.

https://gimms.org.uk/fact-sheets/sectoral-balances/

A few weeks back a small but significant glitch was spotted in the central bank monetary matrix. New Zealand’s PM, Jacinda Ardern had finally decided she’d had enough with runaway house prices being fuelled by easy central bank money...Just like 1989, when NZ was the first country to adopt explicit targets for inflation, this innovation could be the first deep rumblings of what could become an earthquake in the way central banks conduct monetary policy worldwide....Ultimately, as NZ has found, having too much of a good thing can be a bad thing. I expect central banks around the world to follow NZ after the next ruinous, but inevitable crash....For everyone loves an asset price bubble – until it bursts!

https://www.macrobusiness.com.au/2021/03/albert-edwards-nz-property-cra…

It is the banks which create the money for housing not The Reserve Bank. QE is an interest rate mechanism, it is not money for the banks to lend. The Bank of England explains here,

"This article explains how the majority of money in the modern economy is created by commercial banks making loans. Money creation in practice differs from some popular misconceptions — banks do not act simply as intermediaries, lending out deposits that savers place with them, and nor do they ‘multiply up’ central bank money to create new loans and deposits. The amount of money created in the economy ultimately depends on the monetary policy of the central bank. In normal times, this is carried out by setting interest rates" https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

The Reserve Bank must also agree with this as it has the video from the BoE on its own website here. https://www.rbnz.govt.nz/research-and-publications/videos/money-creatio…

Yes. But are they really going to be brave enough to kill the Ponzie. Ardern has publicly stated that she will not countenance house price falls. I doubt that you can hold them stable at these levels. The only stable markets are those operating with open, full and fair competition. In our market every factor is corruptly set to reducing supply and increasing it's cost, while ever increasing demand through out of control immigration. Do you think when Covid has past, that the government will keep a very tight lid on immigration? Here is I how I see it playing out. 2.5 years to election . They will try to put the brakes on house price prices somewhat in the meantime and ease off this pressure towards the election. Close to this time the borders will open up again and there will be the beginnings of a reawakening of house price rises. Trying to cynically pander to the hopes of all.

If governments keep up this let nothing fail it will not end well as what is the point in working hard and smart when others get a free ticket.

I have a feeling they now know this cannot go on so we will soon start to see business closures increasing above GFC levels and mass layoffs as businesses face a supply and credit crunch that will make 2008 a picnic.

What should of happened last year still may still happen or will they just keep the money printers and stimmy checks going forever.

Either way we will see a meltup or meltdown and most will be wiped out even tho they will feel rich with boosted asset prices it will have to be paid back thru taxes and longterm costs blowing up.

New Zealand desperately needs to provide a tax incentive to contribute to kiwisaver. When I worked in Australia I really admired their fully functional superannuation system. It actually totally works! Why are we so far behind? Would a government, any government(!) please get it sorted. And just copy the Australian system in whole, that should save the cost of the working group to get to the same recommendation.

I totally agree. I lived in OZ for several years and loved their Super. system. You gave me a laugh as you have it right about the working groups and committees this would involve if the Govt hete were looking into this. It"s a 'no brainer' - just ask the Aussies.

Looks like NZ savings are much better during National's tenure.

Labour shills deserves what they get.

Labour are always attempting to run budget surpluses which destroy private savings. Taxation cancels money, while government spending creates it. Government debt is the surplus money that the government has spent into the economy and has accumulated in the banking system as our savings. The government likes to remove this money from the banking system and hold it as bonds. All that QE does is return this money to its owners and the governments debt then disappears.

Stop debasing our money and maybe people will save.

Tax incentives to save are a very good idea.

Again its another problem that is easily solved. Instead of TAXING your savings how about the government PAY you additional interest that is structured like Kiwisaver, the more you save the higher the interest rate they top you up over what the banks are paying. Of course you would probably need some legislation to then stop the banks from paying you no interest !!! Bottom line is however is that the government just wants more and more tax every year so you cannot win, what they give you on one hand they will just take even more from the other.

Still haven't had anyone asking the question:

What is it they're 'saving'?

Digital representations of future purchases. is what they think. As always, I ask what that possibility is?

Last I checked, you can't eat digital representations.....

My attempts to save are taxed to death (and don't get me started on FIF tax . . . .). No surprise that all that is left for an investor is residential property.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.