The Economist called it “the West’s biggest economic-policy mistake” undermining economic growth and the public’s faith in fairness and capitalism.

The mistake the Economist is referring to is the misguided policies promoting home ownership which created the developed world’s most serious economic failure.

At the root of this failure is the application of planning rules that have restricted housing supply, particularly close to major cities. This has led to soaring rents and house prices in the cities, hindering workers from moving to areas where the most plentiful and productive jobs are located, and ultimately slowing GDP growth.

Lost wages and productivity

The real costs to the economy of constricting supply in US major cities was identified in an analysis by economists Chang-Tai Hsieh and Enrico Moretti in 2015. They found lack of affordable housing in cities like New York, San Francisco and San Jose (home of Silicon Valley) costs the U.S. economy about $1.6 trillion a year in lost wages and productivity.

The effect has also been studied in New Zealand by Peter Nunns whose 2019 research found that housing supply constraints caused by restrictive zoning rules in our major cities have played a large part in rising house prices. It has also had significant economic impacts by pulling labour away from high-productivity regions in New Zealand, in particular Auckland and Wellington, and increasing net migration of New Zealanders to Australia. Nunns estimated that the total economic gains from reducing housing supply constraints in New Zealand amounted to as much as $21 billion per annum, or 7.7 percent of GDP.

Soaring house prices a recent phenomenon

House prices have not always risen at the rate we have seen in recent decades. In fact, prices in most industrial economies prices stayed constant from the 19th to mid-20th century (Knoll, 2017).

According to Fessler and Schürz, it was only during the 20th century that owning a single-family home became a focus and a sign of making it into the rising middle class. After WWII property also became a major vehicle for wealth accumulation, driven by rising land prices. They argue that land prices increased due to deliberate policies to restrict land use plus incentives to encourage people to funnel more money into the mortgage market.

The increasingly exclusive club of homeowners has meant the only way for most people to get into the market is with parental support or by taking on large amounts of debt. This has also made the housing market volatile, with many financial crises, including the 2007 GFC, emanating from housing bubbles.

Exacerbating the generational wealth gap

As real wages stagnate and house prices continue to rise it has increased the divide between the typically older home owners and the young who are finding it tough to enter the market. It may even be causing a political shift with the Economist report arguing that “young people’s view that housing is out of reach - unless you have rich parents - helps explain their drift towards ‘millennial socialism’.”

The Wealth Effect

Rising household debt can be positive in the short term, by boosting economic growth and employment according to a study by the IMF. However, within three to five year those effects are reversed as heavily-indebted households are forced to rein in their spending. Economic growth is slower than it would otherwise be and the likelihood of a financial crisis increases.

Fessler and Schürz argue when combined with the challenges of an aging population and climate change the dream of the single-family home has become a major problem. And it is one which policy makers are terrified of confronting head on even if it is harmful for society and the economy.

Housing New Zealand

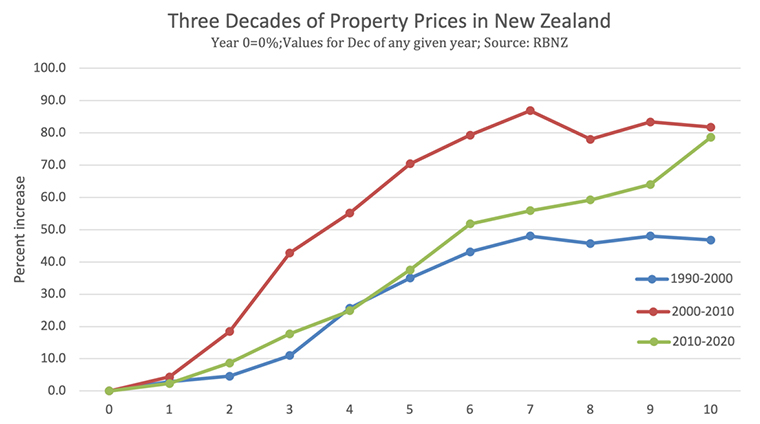

It is well documented that New Zealand now has one of the most expensive housing markets relative to income in the OECD, with Auckland the fourth least affordable city in the world (according to Demographia). While loose monetary policy has led to an explosion of house prices globally, Bloomberg describes New Zealand as “a poster child for the boom”.

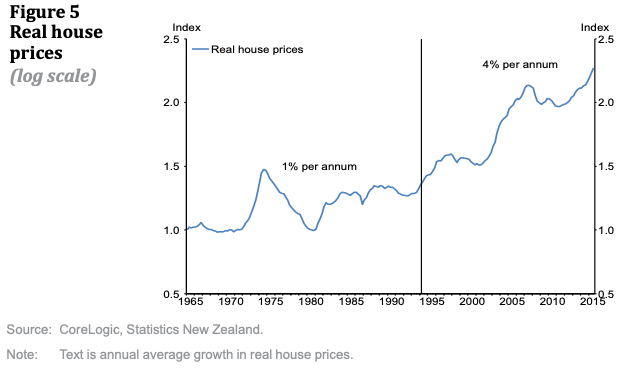

Real house prices increased an average of 1 percent per annum from 1965-95 then jumped to 4 percent per annum from 1995-2015.

Source: RBNZ

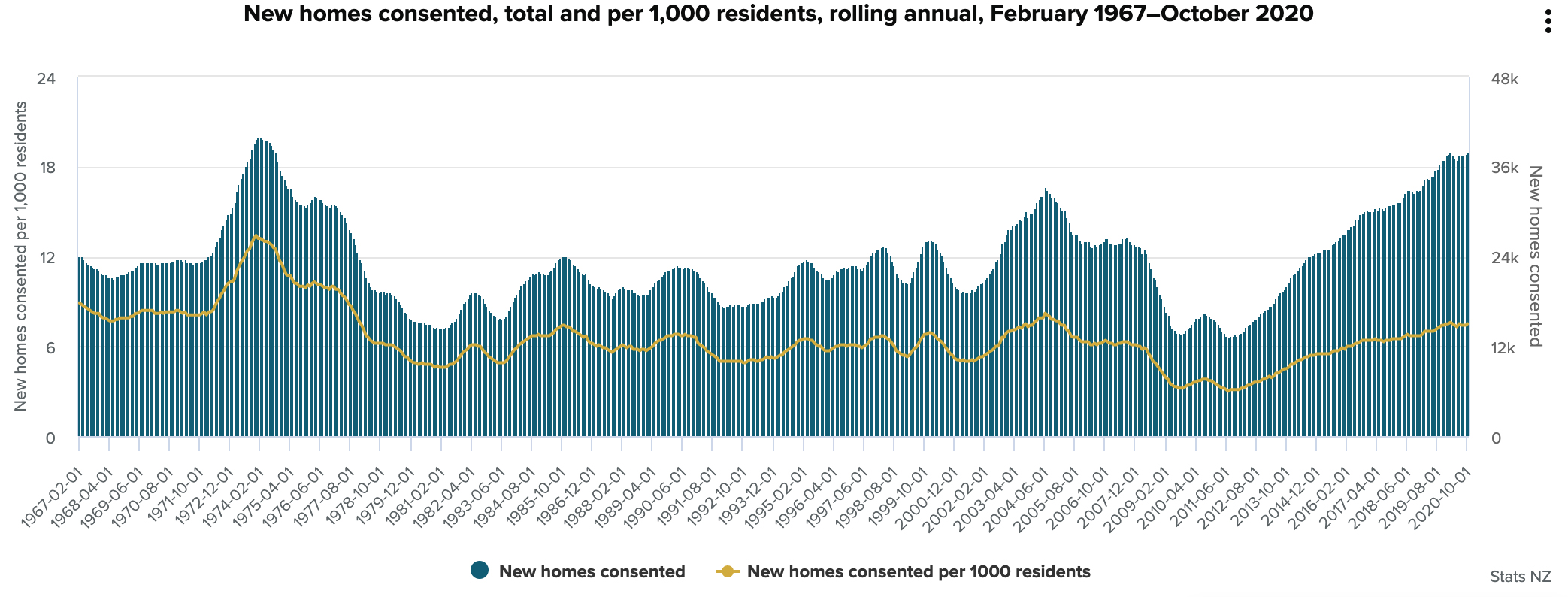

Home ownership is increasingly out of reach for many and ownership rates are now the lowest they have been since the 1950s. Home owners are also getting older: for those aged 25-29 years homeownership has dropped from 61 percent (in 1991) to 44 percent (in 2018). For those aged in their late 30s the rate has dropped from 79 percent to 59 percent over the same period.

An ageing population has also seen the size of New Zealand households shrink – further exacerbating the housing shortage. According to Stats NZ in 1951 the average household size was 3.7 and in 1981 was 3.0. Today that figure is just 2.7. Consents for new homes are up with the numbers of houses consented in 2020 the highest for 46 years, however they are still below 1973 levels on a per capita basis.

Source: Stats NZ

As in other Western countries politicians on both sides of the political divide have supported house prices. CoreLogic’s head of research Nick Goodall said there were consistent messages from the current Labour government about the need to protect property wealth. This is not surprising as the majority of voters are homeowners meaning there is currently little political will to address the issue.

However, despite being politically unpalatable, the tide may be changing. Governments throughout the Western world face increasing anger at the shortage of houses and soaring housing wealth inequality. At some point they will have no choice but to address the housing affordability crisis that almost no homeowner wants to solve.

*Alison Brook is from the Knowledge Exchange Hub at the Massey University campus at Albany, Auckland. She is on the GDPLive team. This article is a post from the GDPLive blog, and is here with permission. The New Zealand GDPLive resource can also be accessed here.

124 Comments

Soaring house prices is a common phenomenon all around the world.

No government has found the right tool to suppress the increase.

Now, with a rise in the cost of building material, we may see an even sharper curve.

House owners would be happy knowing their investment decision was right.

On the other hand, every other house in the street went up and changes nothing but more tax rate and more mortgage paid to the bank, leaving the wealth effect questionable.

The real reason behind increases up to now has been land prices. This can easily be seen by comparing new house prices in cheaper areas like Christchurch with those in Auckland - no more expensive to build but the land value difference is huge.

Higher materials prices certainly don't help, but with some meaningful policy changes they can be counteracted and more by reducing land prices.

Jay

"No government has found the right tool to suppress the increase."

The reality is that governments (central banks) have created the situation.

Quite simply, QE (and other tools) to support the economy both post-GFC and Covid meaning lower interest rates for which asset price (including housing and equities) inflation and lower returns on TD are some of the consequences.

Raising interest rates will suppress the increase, but at some cost to the wider economy and it seems that central banks are prepared to largely continue to wear those current consequences.

However, the outlook is for raising interest rates such as RBNZ signaling of rises in the OCR and is reflected in bank's longer term interest rates as signaled by Kiwi Bank and Westpac.

The days of significant house price increases will for some time simply become BBQ talk reflecting on the past.

The reality is that governments (central banks) have created the situation.

Yes and no. The govt and the central banks work in tandem with the commercial banks who are gifted with the authority to create money at will under very benign constraints (all of which is underwritten by the sheeple anyway).

I thought that house prices weren't the RBNZ's mandate so why hold them accountable?

Everything they've done is for 'financial stability' and stable employment....

I thought that house prices weren't the RBNZ's mandate so why hold them accountable?

Correct. I find their whole existence quite weird. Almost like the Christian churches during medieval times.

Yes I just posted something similar to this below - that I wonder how far in the future before we look back at this present time and think, wow, how wrong did we have it and why didn't we do something to stop the rot.

The powers of society are strong and I just wonder what is going to be the tipping point for those who are getting screwed by the current system.

Following the likes of Wall St bets etc, there is some seriously bad energy around with a desire to crush the current system and asset holders. One wonders if that energy gets mobilized in large numbers, just how quickly this house of cards could come crashing down.

Doubtful that'll happen. Kiwis renouned for apathy. Easily paid off. Look at lockdown last year. No protests. No... kiwis were stoked to be paid to stay home and live their best life.

If things get a bit hot the govt will just start buying people houses and giving them out for nothing.

Yes, apathy, and British-style reluctance to make a fuss.

I think another factor is that most of the people still with some distant hope of clutching the last rung of the ladder are not going to take time/energy off work/saving to launch a campaign to make the Govt listen. They are throwing everything into clinging on and hoping their luck will change.

And below them is a mob of despair with little energy to initiate some kind of revolution (it's not that bad yet).

So for the next few years the current situation is quite sustainable, politically, but will lead to a slow strangling of the economy as young talent leaves and expensive hospitals fill up with boomers.

Stupid FOMO comment of the day at the top of the comments section, it has become a trend now.

We are building at an unseen rate yet open homes are empty and two consecutive months of falling prices have started to change sellers expectations, less and less houses go to auction and asking prices are down, no matter what your agent tells you nor what the government or central banks do, when people believe prices are too high and now even banks do, it is matter of time for them to come down. It is happening as we speak.

I'll put my hand up as a homeowner who wants to see this solved. I don't benefit from house prices increasing and wouldn't really be impacted by house prices falling - I will still own the house I live in with the affordable mortgage I have right now. If I ever wanted to upgrade, falling house prices work in my favour.

The only people who truly benefit from house prices rising are those with multiple houses, who have the lobbying power to claim the rest of us stand with them, and to convince the gullible their interests are assigned.

Amen

Ban slumlording, 2 house max, resident only

Two? So immediately the potential is for half the houses in the country to be owned by landlords. The rational solution is not to restrict property ownership, but to tax the potential or imputed income from all assets, including the family home (rent saved plus capital gain), like any other income. Then property owners would have to decide whether one, two, or half a dozen houses was the best place to invest their money.

Ah, the old Gareth Morgan "tax the enjoyment of owning your home" theme. No wonder his party disappeared!

Simplest fairest and most economical sound way of solving the problem. Most are to thick to understand.

Cool counterargument. Pretty much every economist agrees this would be better for society, the reason it's not already implemented is because it's not a vote winner, so politicians don't push it.

I agree, I have equity but it’s meaningless as I can only realise the gain by moving somewhere cheaper. Happy to see houses fall at least 20% to take us back to pre-COVID prices. Cheap credit is driving the boom with buyers being encouraged to buy up to their borrowing limit rather than what they can truly afford. Now that investors are backing off all we need is loan to income restrictions. Once credit is restricted to 4 times income, prices will have to fall as sellers meet the new market.

That’s fine from a your own selfish perspective but there’s many FHBs that purchased after covid and no they don’t want to see a 20% decline.

At the end of the day people only really care about things that affect themselves.

Actually, the selfish perspective is not Waikatohome's but of all those who ignored the predictions at the beginning of Covid of a house-price fall and leaped into the market. They must be sacrificed for the greater good.

I don’t think it’s selfish. If people borrowed at a level they can afford and it is their home they are not affected. If prices fall the next house they want also falls so no worse off. Only those that bought to make money will get caught and they are the ones that fuelled the bubble.

There's no reason why a Government couldn't bring back State Advances Loans of 3%, through Kiwibank for any FHBers who have purchased in the last 5 years, fixed for up to 30 years with no pre-payment or negative equity penalties. Would be a much welcome apology.

See my earlier point - this is a classic example of people with multiple properties trying to bring the rest of us behind their interests. The reality is a 20% decline would have a negative impact on a few thousand recent FHBs who may be in zero or negative equity, and positive impacts on a few million potential FHBs, future FHBs, and those wanting to upgrade. The sob story of the FHBs is used to push the agenda of landlords. Your final sentence may say more about you than the rest of humanity.

"At the end of the day people only really care about things that affect themselves."

Really? Perhaps that is your perspective, but its certainly not mine.

Yeah the people that want houses to fall 20% make me laugh because they know its not going to happen now but I guess typing a few words to the effect makes them feel good. What looks far more likely is house will in fact go up 20% in the next 12 month, in fact is a given unless all the already advertised price increases on the 1st July on all building materials are reversed again a few months later.

If enough people want it, it can be done. It just takes a little political will to address the problems.

Even after a 20% fall we would have an expensive housing market compared to other parts of the world, the idea that such a drop is impossible is insane.

I've only just bought, and I want real house prices to fall for the good of society. I jumped in the peak of a bubble, we shouldn't sacrifice an entire generation to protect me from my own stupidity.

Ah the typical neoliberal fallacy, let make the poor believe the rich man's problems are also their own.

“If I ever wanted to upgrade, falling house prices work in my favour.”

Really? How do you figure that?

Its math. If all the houses across the board fall by the same percentage amount then the amount you need to borrow to meet the difference when you upgrade decreases. The obvious problem is that it works the opposite way if prices increase by the same amount, that's when you want a really expensive house or as much money as possible in a house. Sound familiar while prices are going through the roof ?

You obviously haven't heard of negative equity, that would explain a lot of your comments.

Nobody in NZ has heard of negative equity, it doesn't exist. Prices continue to rip it up. Anyone who purchased even as little as a year ago now has little risk of going negative. Even if there are falls, housing is a long term game, you know prices are going to double by the time its paid off.

Dp.

If a $500000 house falls 20% it goes down by $100000. If a $1000000 house falls 20% it goes down $200000. The gap becomes $400k instead of $500k. The rungs on the ladder close up in a falling market. Everyone wins, apart from those selling at the top end and those that bought as a gamble, sorry, “investment”. I lost 17% on a house in the uk in 2008, I wasn’t worried as it meant the one I was buying was also cheaper. Owner occupiers who can afford their mortgage repayments have nothing to fear.

mfd,

At 76, i am of the generation that has benefitted hugely from rising house prices, so I accept that I am bound to sound somewhat hypocritical when i say that I too find the current situation absurd and unhealthy. I have owned a house since i got married in 1969, as did everybody else I knew. We simply wanted somewhere to live and bring up our children. I was able to borrow no more than 3 times my salary and my wife's income wasn't counted.This was in Scotland.

Fast forward to today and I apparently 'made' over $1/2million in the past 12 months. My younger son's home in Auckland is now 'worth' some $3m, but should they wish to trade up, they would have to find say $5m. This is insane. We know that QE was never about getting money to business, but to pump up the property and share markets, thus promoting additional consumer spending-the long discredited 'trickle-down' effect. That too is nuts.

f I ever wanted to upgrade, falling house prices work in my favor.

Buying and selling in same market so irrelevant. In you case you haven't quite thought this through

Boring...

The only answer is for the government to build a LOT of housing

Back to Kiwibuild?

?

That wasn't government building housing. It was the private sector, with some government underwriting.

The answer is simple, the GOVERNMENT needs to build much more housing.

there uses to be 100 dollars and 10 houses.

now, there are 1 million dollars and still them 10 houses.

Yes, and to borrow those 100 dollars it used to cost you 20 cents per year. Now you can borrow 1 million and it'll still cost you 20 cents per year.

So.... The price of everything hasn't changed at all. It's just that wages have been undercut relative to assets in a big way. And since wages are paid in your local Fiat currency, one could surmise that the purchasing power of that currency has devalued spectacularly. So, if it's printed by a CB, borrow cheap and buy anything and everything that's not tied down. Used cars, lumber, Dogecoin, NFTs, the Mona Lisa's ugly sister, next year, as the finance minister just discovered, everything will be more expensive, or rather, the dollar borrowed today will buy more than the dollar borrowed tomorrow. And you can safely call the interest rate bluff, because, should CBs lose control of the rate, the least of your problems will be your ability to pay interest. It will be sourcing basic foodstuffs and medicines.

Just central bankers doing what central bankers do.

The only way this ends is economic collapse and hyperinflation and I reckon it's now inescapable.

When it happens one can only dream the angry mob hunts down those responsible.

No point leaving your wealth anywhere they can get their grubby hands on it to devalue.

Likewise there is no point trading your precious working years for their worthless remuneration.

I do wonder that if in 30, 50 or 100 years from now, people will look back at the current system and central bank policies and simply shake their heads.

Deep down, its pretty obvious the system we're using isn't working and isn't going to work, yet central banks are doubling down (or more!) because they can't admit they've got it wrong and change course.

Change course to where exactly?

Collapse is baked in, they are simply trying to delay it

Failing fast is better than failing slow.

We’re attempting to fail as slowly as possible which is going to create needless suffering.

"Is NZ’s real estate obsession hampering our economic growth?"

Not hampering BUT is the only economy courtsey government and RBNZ.

"Alison Brook finds that rising anger at the shortage of houses and soaring housing wealth inequality will mean that public officials will have no choice but to address the housing affordability crisis that almost no homeowner wants to solve"

Alison Brook, you are 100% correct both government and RBNZ have willingly allowed themselves to be cornered and are in a situation where they will always be blackmailed, if they try to control the ponzi.

It was a mess earlier and now it has become so big that both Robertson and Orr will not be able to control, now they do not want to and in near future will not be, even if they want to. Have created a monster that they themselves have no control.

Mr Orr has been wrong earlier by removing LVR as the need at that time was to support existing home owner and not promote new buying frenzy, specially when knew that OCR will touch zero and now again Mr Orr is wrong by not going after speculator by stopping access to interest only loan.

Interest Only Loan should not be completely banned as is needed in time of emergency but should be stopped for new home purchase and existing interest only could be phased out over a period of time.

Wait and Watch when every month house prices are touching new numbers despite three months since introduction of so called housing policy and reintroduction of LVR. How long will they Wait in anticipation ???? May be hoping that some day it has to pause by itself, so why rush and allow speculators to plunder and let house price reach a point from where even 10% to 20% fall will be meaningless.

It is positive that now many journalist and experts have realised that Mr Orr and Mr Robertson to suit their narrative have created a FRANKESTEINS MONSTER.

Mr Orr in early May was suppose to act but postponed till end of May and in May announced that their is no need to act, if their was no need to act, why did he not announce the same in early May, why waited till 26th May, when the script was already written.

It is late but even now can act and salvage but they themselves want to create a situation where the risk will be so big that no one will touch the ponzi.

She loves power so much she will never upset the home owning voters including previous National supporters who support her. On top of that we owe her our loyalty as after all she saved all our lives last year. Or so she says.

If you want that to change, it's worth writing letters/e-mails to your MP, and/or Megan Woods as the current Minister of Housing. You probably won't get a very constructive reply, but it's one thing we can do to let them know we want action. Otherwise, they remain afraid.

https://www.parliament.nz/en/mps-and-electorates/members-of-parliament/

Ha ha nice one. I wrote to Megan Woods three months ago, no reply.

I don't think she would listen anyway, comes across as an arrogant know it all

That's a shame. I got a reply from my late December e-mail in late January. Mostly outlining what they have already done and planned to do.

Still worth doing though - why would they change their opinions if they're not exposed to different views? You can bet that landlords are lobbying hard, there needs to be an opposing force.

No, you'll be wasting your time writing to MPs about this, except maybe a few of the Greens. Most of them into the housing frenzy themselves:

https://www.stuff.co.nz/business/property/300310944/property-investors-…

You are correct and also herself have made enough to be set for life and now planing future as know that most probably will be the last term but does she cares as have made so much that could not have imagined five years back.

House obsession will continue as everyone who can make a difference be it politician, expert, bureacrats or media, they all have vested interest as own one or more house. So this obsession will continue till something drastic happens like peseant revolution in 1900s and only this time will be replaced by non home owner.

Some Data

Number of Private Dwellings in NZ

Year 2000 Total = 1,444,000

Rentals = 426,000

Owner Occupied = 1,018,000

Year 2020 Total = 1,863,000

Rentals = 618,000

Owner Occupied = 1,245,000

Increase in Population = 1,000,000

Increase in Dwellings = 419,000

Inrease in Owner Occupied = 217,000

Increase in Rentals = 197,000 (mainly high rise apartments)

Data from NZ Stats

https://figure.nz/chart/bOXOzYWW8RyIotwx

Change in count of occupied private dwellings in Auckland, New Zealand

This is why they want a walkway over the Harbour Bridge

https://figure.nz/chart/Rkbfb9bCsCZEKk5l

Interesting numbers - we've got an obsession with property and landlord'ism.

Having banged the immigration drum here since I first joined, I have given up

An examination of those numbers tells you immigrants do not build new homes

They don't have the time. It takes (up to) 3 years to build a customer-specified house

That tells you they squeezed the incumbents out and created the shortage

Behavioural Economics will explain to you that, that process has escalated the prices for existing land and having escalated it, the price of that existing infrastructure will not go down. Nobody willingly sells for less than they paid. The 2019 price level is the "set in concrete base-line" for the Ardern mis-step that caused a 25% blow-off in spite of immigration levels collapsing

Insanity really - Nz isn't being well governed, nor has been for the past 15 years or so.

We've made nominal GDP figures look good, while destroying the quality of life and prospects for younger people that are born here.

Makes you wonder about the performance of Auckland Super City.

Was the idea poor

Or the characters implementing it worse?

There's a strange paradigm that leaders see the world at present - where its more about short term popularity than longer term sustainable/utilitarian thinking.

Perhaps its because people living in democracies seem to be filled with fear, resulting in FOMO and the need for instant gratificaiton as opposed to making sacrifices now that will make society better in 10, 20, 30 years....from now.

Inequality ... right, okay.

If this government manages to create a housing value crash, and they're certainly trying, then that's our SME sector in a lot of trouble because most SME funding is secured over owner houses. It's just the way it is; banks like houses as security, and many businesses have no other security.

Also, the wealth effect is huge for consumption: destroy that, destroy consumption.

But I hope Labour do it: because that's the end of Labour; most kiwis do own houses, they, especially all the first home buyers over last four years, will not be voting for a government that destroys their equity.

Yes. But if you're going to base your economy around credit-driven asset bubbles, it's eventually going to bite you on the ass in some form or another. There is an argument that Australia and NZ could be exceptions to historical evidence of what's happened elsewhere. How (and if) it will unfold is going to be fascinating.

So effectively the economy is high on cheap debt, and anyone who tries to take it away gets thrown through a window.

For Joe punter, SME, debt is cheap so long as the bank notes security being residential property.

Thats why when you walk in for a business loan, you leave with a home mortgage.

I might believe you if the all beneficiaries of the 20% munificence over the last year had borrowed up and spent that 20% rise on consumption, and the SME businesses had borrowed and expanded their production by 20%

They haven't

So what you're saying is that bringing sanity back to an economy is not a good idea? Or am I confused.

MH - you are an interesting character; you never change your stance. What is, seems to be what is. That isn't the way my circle think; we question most things, most of the time.

Here is a link to what will REALLY destroy your 'equity':

https://www.amazon.com/Blip-Humanitys-self-terminating-experiment-indus…

I challenge you; read that - all of it - and ask yourself: Is my understanding of 'equity' correct?

Then tell us how you went.

That 2050 termination date again PDK. Funny but I took a guess on 2050 years ago now but it still depends on whether we can change the current trajectory or not. 2050 is really based on the status quo and the human race continuing without change which is the far more likely scenario. Clearly however the likes of Covid has demonstrated that a virus beyond our control has the potential to dramatically shift the date. Should the worlds population suddenly stall or start to decrease it rapidly pushes out our use by date.

This article is of course spot on and something that a few of us have been pointing out for decades now.

But it is wrong when it makes a general statement about 'all' the west having this problem, and soon as it mentions the USA talks about California as if that is representative of the US.

We know it's not as the likes of Texas have median multiples less than half that of California.

It is only a recent phenomenon that the median multiples have increased. Until the early 1990s, NZ and Texas's median house price multiple was 3x income, and texas's is still close to that while NZ is approximately 8x and Auckland 10x.

All this increase is due to Govt. land-use policies, namely the restrictive use of land.

Further, I've never seen so many other restrictions in the system at the same time. We have restrictions in land, labour, materials, logistics, LVR's, and soon increases interest rates Plus, there will soon be much-needed changes to the building code, resulting in extra materials and labour costs.

I'd read a few years ago that some US states only had housing planning and building controls within the city municipality. Outside of this zone people could build anything they wished to (probably off grid services). If true that should make housing costs much cheaper for rural areas

Not quite like that, but close.

What they do is put aside land that they don't want to build on for environmental reasons etc. and then leave it up to supply and demand on when and how (not council) the rest gets developed. This in theory leaves a super supply of land available and makes it virtually impossible for speculators to land bank.

So land can be bought by a developer at close to its rural price, and the developer or individual puts in the infrastructure which the community owns. Just imagine and Body Corporate run as a subdivision. It's simple, cheaper, and more environmentally friendly than the present council methodology.

Dle Smith - no, it isn't. This is an argument we had here 10 years ago. Try reading the link I put up upthread - do you still think like that after reading it?

Not sure what point you are trying to make.

Mine is there are far more cost-effective, less wasteful, more energy-efficient, ways of building houses, which would also make them far more operationally efficient and healthier, and help solve other social issues around health etc. Our present system is very wasteful causing people to have to work harder just for the sake of 'feeding the beast.'

The main issue is if people's needs (real needs) could be meet with half the effort and time, houses using 90% less energy etc, then what are they going to do to full in the other half of their time and money without wasting all the gains made (the devil makes use for idle hands). Most reaction activities/holidays are really wasteful of resources.

GDP is about as a useful measure as claiming Auckland is the most liveable city in the world.

The repeal and replacement of the RMA will actually end up being one of the most important pieces of economic and social legislation in New Zealand's history. If it maintains existing land use restrictions that to throttle housing supply then ultimately the benefits will be very limited.

Will we let there be change?

I really can't see how changing one Act into three is going to make things cheaper though?

This is such a warn out story. Both local and state government need to have a good hard look at themselves with the choking compliance and complexity to actually get to the build stage of a development.

I just did a speaking engagement regarding the 226 page addition of the the building code which forms the third tier to The building Act and Building Regulations. The replacement of the RMA into three new acts Will NOT improve anything. Costs are sky rocketing due to government incompetence in virtually everything they stick there noses into

Don't blame the Government, or legislation.

Blame physics first, chemistry and biology second equal.

And perhaps read up about Entropy? Then apply what you've learned, to what you see unfolding.

Here a long form conversation with Richard Werner.

https://youtu.be/u8j51XZegsk

Lets try local banks lending to local businesses, jobs, incomes, GDP all up.

If the banks are not interested then why not have the MBIE provide lending direct to the SMEs? Give it a go for a few years and see how it pans out. The RBNZ has $100b provisioned for "Funding for Lending" so why not tap into that.

Imagine being able to buy a home for less than a few thousand dollars in a beautiful part of the world and have a property that is aesthetically more charming than the drudgery people endure in NZ.

https://www.vice.com/en/article/88nxkx/japan-abandoned-homes-akiya

Interesting. Quite a shift for Japan, which has been highly resistant to immigration.

Now there is no answer to this puzzle, if labor cannot do it then there is no other party in NZ who even say it loud. The only solution will be self correction or some hard hitting laws. If we face out the second option because our current ruler are full of drumheads and liars.

Than there is only one option left self correction, but it will be painful for lot of people, so the current govt try their best to avoid it. And Govt. can do anything if they really want to deliver, so conclusion this will not go down.. Keep Posting no one is listening.. Keyboard warriors can only throw stones upward, they can never make a hole in the sky...

Its nice to vent a little though isn't is and cause a stir with the members of the property investor association. You know, just to keep them honest so they don't become completely delusional (although probably too late!)

You are right IO but my point is now the price will not go back to pre covid level, even we where saying those (pre covid) prices were high but now it's insane. People (renting & FHB) are nearly crying to see property market rocketed. Current govt is completely delusional about the situation, media have done their part but as I said these thick skin politicians will not be impacted no matter what you do or write. NZ have no political party who give it a shot to clean this mess, so it is what it is, accept it or move on (leave NZ).

Interest will not be raised to the level where it hurt, it will go miniscule up side and than plateaued, IO loan can be stopped but don't know why the action is just postponed, either RBNZ head is corrupt, idiot or hired due to commendation and not experience or potential. Now there is no point, as it is too late, you cannot revert few things in life and this is one of them.

I lived in the US when their property bubble burst and people were saying then that prices could never fall. But fall they did.

I wouldn't lose hope if I were in my 20's. Society is interdependent, so you can't oppress one part of society without experiencing pain in another part.

here's a typical video playing on the property investors website...

hey borrow $850k on interest only....what could go wrong

the moment interest only loans get phased out its over rover my friends

Your comment missed one basic logic. You are comparing apple with bananas, NZ is not US and US is not NZ, there is a sizable difference between 2 nations. I was hopping that things will change but after analyzing it thoroughly, my personnel finding says it will not fall. It may not go up substantially for next 2 to 3 years but it has found the ground, there will be not more than 5% downturn but it will bounce even more substantially.

And believe it or not, it is on cost of young Kiwi's, we don't have any one to blame because shitheads will never take responsibility other than showing concern with fake smile, tilted head, team of 5 million and be kind like gestures.

Don't forget the frown. The furrowed brow is a real crowd pleaser, she's got that one down pat.

As an aside, has anyone actually listened to how she speaks, not the words but her use of inflection, tone, pauses, etc.

With all the talk of her being a good communicator which I always thought was rubbish, one day I actually decided to listen to her speak, not listen to the words because they're utter drivel, but listen to her delivery.

Blow me down, she is as it turns out actually a very skilled, persuasive communicator whose style of speaking is apparently particularly designed to appeal to women along with the ludicrous hand gestures and body language.

So in summary I can see how if you're wanting something to believe in she could seem very sincere and persuasive. Personally though I'd just feel angry with myself if I found myself sucked in by her fakery.

She has at times appeared to be quite genuine in her delivery. I am a woman and I do not overall find her communication to be convincingly sincere, but I completely understand why many do. We do not properly educate people about healthy relationships in all their forms. The cracks are constantly showing through though, especially during questions she clearly does not want to answer and obviously, her actions regularly fail to match her words.

Most people struggle to come across as entirely genuine under pressure, but there are quite a few consistent red flags in her communication. Unfortunately a lot of energy seems to have been focused on maintaining her manufactured outward appearance and utilizing manipulative communication methods/rhetoric, rather than discovering and continually developing an authentic self.

.

Up up and away baby, keep going up I say, 20% 30% a, year go you good thing,

Why not 100%? 1000? 10,000? Don't be such an underachiever. Venezuela is beating us hands down.

Don't want to be too greedy mate, making a million dollars a year on equity is fair enough I reckon.

There is NOTHING wrong with home ownership! What IS wrong is the commodification of housing. What IS wrong is the rise of land leeching as something to aspire to. What IS wrong is the preparedness of some to use their stronger positions to turn their fellow humans into something only a little better than farmyard stock. What IS wrong is the lack of security, the lack of somewhere to really call home for far too many, while a few justify their actions as "securing their retirements". What if those they have fed off!

Soon may it be over!!

What IS wrong is the preparedness of some to use their stronger positions to turn their fellow humans into something only a little better than farmyard stock.

This is neo-feudalism.

Yup

Everyone has a right to the stability and security of a home of their own. It is just shameful, that anyone should struggle or find it entirely impossible to ever enjoy such a simple, yet incredibly important human right. What a world we have created. There is no good reason to justify denying people something as necessary as their own home.

QD - sorry, but if you don't limit population, then there are no 'Rights'.

The world can support a certain number of the human species; that number is dependent on their desired consumption-rate. At good-peasant-level, the world can support perhaps 2 billion. At our level, perhaps 1 billion, but I've seen arguments for 600 million.

At those numbers, there are enough already for several houses each, and well before 2050, our numbers will have fallen enough for this to be the case.

Sorry if reality clashes with your optimism; RNZ are in the same boat and heading rapidly down a Woke rabbit-hole in attempting the reconciliation between their hopes and reality. Watch them in free-fall, and learn.

You mean in your opinion its wrong

No young boy, it IS wrong

Got to say that this was a fantastic article (in my opinion..) - one of the best I've read on here for a while.

Nice work Alison.

It would be interesting to see if we could expand that 'real house price' chart back further....its likely that we see that NZ house prices, like AUS and the US were flat in real terms for the previous 70+ years and that what we've witness in the recent decades, could be the mother of all housing bubbles.

I thought it was average, with nothing particularly insightful.

Not sure who but someone in UK am economist maybe or just a lay person studied housing cycles over hundreds of years and came up with an 18 year property cycle. From 2008 to the next crash in 2026.

This is what most of us have been banging on about for decades. Delusional government after delusional government believing that monetary policy and housing is the economy. It's become the populist mantra and this government is not changing the tune, just singing the song out of key.

One aspect that is not mentioned in this article is probably the biggest piece though - the amount of money "invested" in housing which could have been invested in businesses. With a high cost of entry, it means we have skewed our entire investment options into almost exclusively housing. Barely any money now gets invested into the productive economy in this country which is slowly hollowing out our productive sectors. That effect is likely 2-10 times larger than the 7.7% GDP loss as outlined above, but is near impossible to measure.

There's still room for upward valuation.

Be quick.

Is the obsession not justified

https://www.oneroof.co.nz/news/nzs-hottest-housing-market-where-prices-…

Promoted by Jacinda Arden and supported by Robertson and Orr

Nz will have the housing ponzi corrected by external events rather than our existing politicians doing anything to lead to a correction. These events could be anything from china embargo on our exports to a surge of interest rates or a significant rise in oil or other energy costs as occurred in the seventies.

True but obviously another different Virus outbreak is not going to "Fix" the NZ housing market, my prediction on that outcome with Covid-19 almost bit me on the bum. We grow food in NZ and thats never going to go out of vogue but I can see that high transportation costs in the future could kill it for exporters. I was thinking the other day we could end up back on sailing ships so that would severely limit the distance goods can travel. An increase in interest rates will only limit house price increases to where they should be.

Enjoyed the article Alison. I don't really see any sign yet that most governments are serious about building, they are treating it like a very peripheral issue.

+1, great article.

Excessive house (LAND) prices are massive unneeded cost to NZ's economy. For those not on the property ladder it means massive mortgages sucking money out of potentially more productive use.

NZ has simply wasted 40+ years (real house price increases started in the 1980') being totally unproductive spending capital bidding up the price of land (of which there is no shortage) & the productivity commission wonders why NZ is so unproductive.

All of it is self inflicted except 1)

1) Fall in worldwide interest rates from the 1980's to worldwide lows in 2020 raising asset prices

2) RBNZ effectively printing money without having DTI tools

3) Immigration rates in excess of ability to build housing supply

4) Inelastic RMA land use rules written by planners who dont bear the costs

5) Failure of successive government to write national environmental standards/policy statements

6) No comprehensive wealth/capital /capital gains/land tax regime

7) Recourse mortgages - these should be banned as they screw investment towards housing rather than towards productive business.

It's a totally ignorant article.

It's from an economist - or from those who teach it. She's had enough put in front of her, to know more, too. Didn't even open it, is my guess.

In reply to your comment - what the ---- do you think the 'productive economy'' is? It's people building houses and filling them with stuff, plus the servicing of those houses. That's it. Period.

But we shouldn't be getting this type of thing from a University, this late in the piece.

Oops, sorry, I forgot the only thing we're allowed to do is "building houses and filling them with stuff, plus the servicing of those houses." :)

Welcome to the real world PDK, that is exactly what the productive economy is now. Success is defined by how much stuff you have in a house thats is as big as possible to fit all that stuff into. To be fair the current system is working really really well, right up to the point the resources we are plundering to sustain it are gone that is. Just face it PDK, humans are dumb and move on. We are the only species on the planet trying to kill the very planet we live on and most of us are all running so fast on that hamster wheel we don't have time to think about it.

Vive la tiny house

A Reality and RBNZ says that housing market is cooling........really

https://thespinoff.co.nz/business/05-06-2021/a-bizarre-afternoon-at-a-c…

How long can Mr Orr lie and manipulate.

The title of the article says it perfectly. No "interested party" (i.e. property owner), has any concern for a return to historically normal interest rates and levels of debt. If the pyramid game stops, their world will tumble.

The only way forward is by personal crusade. I refuse to buy a house due to this debacle (and I dont want to be a mortgage slave). I could, but I wont. Most people I talk to about this look at me like Im an idiot.

I just dont see the point. For the record, Im 50.

I'm 58 and doing the same, Sluggy.

I'm investing in equipment to generate income - to hell with a $1m shitbox in AKL.

This monetary policy is oppressive for those that don't own property....and its oppression caused by a state entity against its own people.

How %@#$'ed.

Can you point to any articles that have come out of academia that discuss (a) the beginnings of our society being splintered into identifiable haves and have nots, and (b) middle session of the continuing plunder of our society, and (c) where society is today, with those who have taken advantage of government policies and now hold multi-million $ wealth versus those who were content with living in their 50 year old one-house with a front lawn and a garden. And (d) those who don't own a house and the afflictions society imposes on them

I havent seen any. Just Silence

Coibion, O., Gorodnichenko, Y., Kueng, L., & Silvia, J. (2017). Innocent Bystanders? Monetary policy and inequality. Journal of Monetary Economics, 88, 70-89.

Mumtaz, H., & Theophilopoulou, A. (2017). The impact of monetary policy on inequality in the UK. An empirical analysis. European Economic Review, 98, 410-423.

Ampudia, M., Georgarakos, D., Slacalek, J., Tristani, O., Vermeulen, P., & Violante, G. (2018). Monetary policy and household inequality.

Domanski, D., Scatigna, M., & Zabai, A. (2016). Wealth inequality and monetary policy. BIS Quarterly Review March.

O’Farrell, R., Rawdanowicz, Ł., & Inaba, K. I. (2016). Monetary policy and inequality.

To fix the overwhelming desire to invest in residential real estate, try fixing the NZ superannuation savings process in NZ.

Our poverty-outcome super savings system requires changing from the present TTE system to an EET system like all our western country counterparts (USA, Canada, UK, Australia).

If politicians are truly serious about encouraging everyone to contribute to Kiwisaver and reduce dependence on property for retirement savings, there should be cross party agreement to remove taxation on Kiwisaver funds like most other western countries do. Peoples' savings will grow quicker and larger and can be taxed on pension withdrawal when retirees tax rates are lower. This is way more effective than Capital Gains tax on property which doesn't work per overseas evidence. Remember, peoples' contributions to KS are taxed as part of their wages (unlike overseas where they get a tax deduction for Super savings). Then, exempting Kiwisaver Funds from tax (like US, Canada and others) would help funds grow bigger. This is referred to as an EET system, Exempt-Exempt-Tax. Right now we have the worst system being TTE, Tax-Tax-Exempt, the first two steps ensuring Kiwis' retirement savings can never be as large as our foreign counterparts forcing Kiwis' to invest in property to have any hope of a reasonable retirement. If Govt keeps unfairly taxing KS AND introduces Capital Gains Tax then young NZers are really screwed.

In 1989, the Lange/Caygll Labour government, based on a review carried out by Don Brash, changed New Zealand’s tax settings. Until then, New Zealand was like most other OECD countries including USA, Canada, UK, Australia in that it applied an expenditure tax (saving) treatment on savings placed in sanctioned savings schemes.

The change was that we scrapped NZ’s ‘Exempt Exempt Taxed' tax system (EET), where income was exempt from tax when earned then saved, exempt when it accumulated in a Super Fund and earned interest and dividends, but was taxed at a person’s marginal rate when withdrawn and spent (usually on reaching retirement age).

We replaced that with the current draconian income tax treatment, so it would 'match' other forms of savings, EXCEPT owner-occupied housing. NZ thus adopted the draconian TTE system, leading to significantly smaller retirement nest eggs for NZ retirees. This meant there was a distortion created in our tax settings and hence retirement plans became one of investing in houses. The solution is not to tax capital gains on housing (because politically it won't happen and it certainly won't help) but to move back to an EET Super system to attract Kiwis' money that way, like Canada, USA and most countries still to to this day.

Here are some of the countries that still do in 2019 what New Zealand did up until 1989:

United States, Canada, Mexico, Japan, South Korea, Austria, Belgium, Finland, France, Germany, Greece, Ireland, Iceland, Norway, Netherlands, Portugal, Poland, Spain, Switzerland, Turkey, the United Kingdom. And Hungary has a very similar way. Furthermore, Denmark, Italy and Sweden exempt tax when money is saved and put into a retirement savings account.

So we used to be part of the mainstream OECD approach to expenditure taxes. But the Lange government needed revenue, and the change at the time brought forward revenue into the government’s coffers.

The wise and fair option is to move back to an EET retirement tax system, like the rest of the world. This will provide citizens with a dignified retirement and ultimately reduce dependence on our hopelessly inadequate current NZ Super. It will also remove the incentive to invest in residential real estate.

I'm here from the government to help, yeah right. we continue to look in all the wrong areas and demonise property owners. I have done 368 projects in Auckland to date and the core problem sits primarily with state and local government. Make it less compliant and time constrained and let private investors sort this problem of supply out. Our minister of Housing Megan Woods is an expert in the urbanisation of Maori. What do you expect when you have no experience in an industry that creates massive economic returns and employment.

Let the right people do the job. I'm sure she's pretty good at eating donuts!!!

Simple solution. All those disenfranchised vote for the TOP tax change that would introduce a universal land tax, and reduce income tax. This would promote working/productivity, while punishing lazy debt speculation on land. Unfortunately for young non property owning kiwis - its currently the other way around, hence their departure from our economy as they enter their prime tax generating years.

Land/debt speculation has got to the point that it is holding the rest of the economy hostage. But hay, perhaps we can keep raising and educating young kiwis for the sole purpose of exporting them to Aussie. When there are insufficient nurses and doctors remaining in NZ to operate service, ask yourselves why that is, answer, they simply cant afford to live in NZ. What was their single biggest costs again....oh yeah its Speculators Rent or 9-10 x earnings Mortgage. PS Aussie hospitals are recruiting hard out in NZ right now...Winning!

Every day someone comes with a slightly different angle to write a story on house prices. headline stuff

Well I have news for you , its supply and demand , end of story.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.