By Gareth Morgan

By Gareth Morgan

In 2007 I said publicly that houses in New Zealand were 30% over-valued.

That comment met with much derision from the real estate industry (funny that) whose state of denial at that time was at its most fervent.

The industry is a little smaller today, but who knows what level of fantasy it’s currently convinced of when it comes to property predictions?

The important issue is how far through the inevitable correction in that market arewe now?

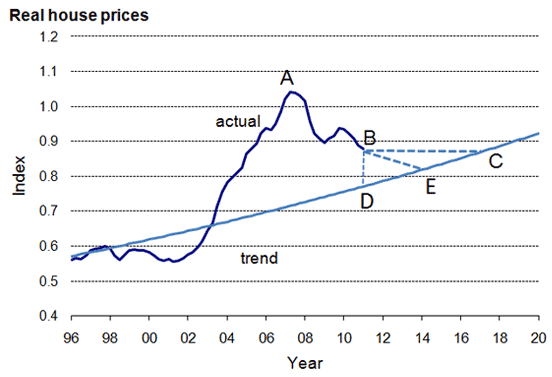

A couple of approaches can give us a feel for where we’re positioned. See first chart below.

At peak, June 2007 (point A on the graph), real house prices were 45% above trend (60 year).

Those 2007 prices would have to fall 31% to be back in line with that indicator.

Since 2007 real house prices have fallen 15.5% (to point B on the graph) comprising a 5% fall in nominal prices while general consumer prices have risen 12.6%.

Meanwhile the long term trend value for housing has risen by 7.8% over the 4 years. This suggests real house prices would need to fall a further 12% to be back on track the long-term trend.

Of course an overnight drop in real prices (to point D on the graph) is just one scenario and most unlikely. The banks’ heroics in avoiding mortgagee sales may prevent a domino tumble in prices.

So let's look at a couple of other possibilities.

If house prices just kept pace with inflation from here on, how long would it take for them to be back in equilibrium (point C on the graph)?

The answer is another 6 years. I doubt the market will have that sort of patience.

A more reasonable scenario would be that house prices stay flat, and inflation erodes their real values, and we’d be back to normal (point E on the graph) in about 3 years.

But a word of caution; it is unusual for house prices to just approach their long term equilibrium value quietly and predictably.

It's actually more common for them to undershoot before they settle – and given the huge size of the overvaluation we have just experienced, you could just as credibly argue for that scenario.

Don't be surprised then if the picture we're painting here ends up being pretty conservative – i.e. things could get considerably worse in the housing market before the markets stabilise.

The ramifications of that for an economy that has been founded for two decades on bloated property values would be very serious.

The reason I’m not backing an overshoot at this time is that immigration is holding up reasonably. Any analysis done simplistically on population demographics and building activity would suggest house prices should have already fired up.

At some stage those factors will come into play, but not until New Zealanders reorganise their finances in a way that reduces their dependence on property speculation.

Now the above is just one type of indicator or analyses many you could deploy.

Here’s another.

Looking at our history, the ratio of average house prices to average household income has varied a bit over the years but averaged about 3.3 – at least up until the orgy of property speculation that began in 2002.

That ratio peaked at around 5.7 times the average income in 2007, but it’s now back to about 4.5, so it looks to be about halfway back to ‘normal’.

This is a slightly more pessimistic message than you get from the real house price trend analysis.

I could go on and talk about the role the ageing babyboomers have played in the speculative orgy, loading themselves with mortgages and multiple homes in their late life quest for riches. Now they have to back out of a weak market and fund their early years of retirement. That will put a further dampener on the sector.

But hey, there’s good news here.

Here we go:

• Houses will become more affordable yet for the younger folk, so keep your powder dry, be patient and work hard to get deals from need-to-sell vendors.

• Agents are too expensive and you don’t need them now with online listings, so don’t accept you have to use one.

• The younger baby boomers – those around 50 years of age – still have time to rebalance their assets, get real, dump a couple of their houses and get a balanced distribution of their wealth.

• The funds freed up from the housing frenzy can be put to investment in New Zealand and increasing our ability to generate genuine income, jobs and wealth – so long as government’s tax and welfare policies and the RBNZ’s directives to the banks on what they should lend on – aren’t dumb enough to thwart that.

Anyway all the messages are the same – the property orgy is correcting, but it’s not over yet.

We’re well into it – and that is very good for New Zealand. Enjoy!

-------------

Dr. Gareth Morgan is a director of Gareth Morgan Investments, where this article originally appeared. It is published here with permission.

135 Comments

Hear hear Gareth.

I seem to remember I said something about a 30% over valuation in early 2008 and haven't heard been able to hear myself thing for the last three years for the noise of complaints about it.

cheers

Bernard

Yes Bernard but you said 30% in 2 years, ie a crash and you didn't even get in the ballpark. At least you manned up and took your humble pie down to the pub.

Vera - the one and only reason why that 30% fall didn't eventuate at the time is hidden (well, not hidden actually - it SCREAMS out at you) in this chart;

http://www.interest.co.nz/charts/interest-rates/ocr

Bernard was robbed by the Reserve Bank Guv.

I think the OCR drop was pretty crucual as well, the rate was un-precidented but well done.

Plus the banks minimalising the mortgagee sales and that includes rural as well as residential.....the OCR allowed them to....ditto a low OCR is seeing ppl sitting on properties because keeping them is not costing them that much....yet.

If we (NZ) or the banks get a credit downgrade (and I think thats fairly likely for the banks because OZ is way over-valued) then rates will have to rise at least for the big 4.....Kiwibank and TSB can probably sit tight....

Throw in I expect China to throw a paddy field this or next year...which will tumble the market in OZ and hence here...

I still think BH is right...in fact I still think there is a bigger drop possible when you consider an over-correction, we have the financial crisis which is staggering on and getting worse...er have Peak oil and oil at >$100USD a barrel, then we have BBs retiring....all these scream huge problems......so the mean is 3 to 3.5, this suggests a correction to 3 at the least...

regards

It also increased investment in property and firmed prices in many cases, the number of people that purchased additional property and locked in 6.5% long term finance was rather large a couple of years back.

Exactly.

Bernard I don't think anyone disagreed that house prices were over inflated, but there is a big difference between house prices dropping 30% (meaning a lot of people would have been in negative equity and we would have had a lot of mortgagee sales, etc) compared to house prices staying flat for several years. I am pretty sure you predicted the former, not the latter.

Jimbo where have you been? There are heaps of 'gee' sales and no capital gain above inflation is still negative equity if your an investor. Prices are only 'relative' Example: everyone might be asking for 'X' dollars but that does not mean 'X' dollars is the true value at that point in time

Maybe there have been 'heaps' of 'gee' sales, but Bernard's predictions would have meant a hell of a lot more. We haven't had anything like what happened in the states.

You are not in negative equity until you owe more than you own - that can't happen through inflation, only through a drop in $ value. We have only seen about a 5% drop in $ value of housing, not enough to put many into negative equity as even the most loan friendly banks would normally ask for at least 5% deposit.

What's the drop in sales volumes( lowest since records began) worth though Jimbo? Surely it's a good indicator of people not willing to pay the prices wanted?

...... when does supply and demand get mentioned?

well you know the reason why Bernard....

FAR too many vested interestes in property to let your predictions go unchallenged. After all our whole economy has been unsustainably founded on property for so long ,as Gazza states

And quite obviously the "Real estate" (ie. bank) economists did their best to make you sound like a nutter, because ,surprise surprise, they have a massive vested interest in keeping the bubble inflated!

Its pretty hard to battle against arguably the two most powerful institutions in the country, both of whom have extreme vested interests in property - the mainstream media and the banks

Dear anti-property Matt

Stop being so negative! You will not live a happy prosperous life with all the negativity, jealously and anger you have dude (CP). All we are doing is trying to provide for a better future and our own retirements. The mainstream media hardly has a vested interest in property. In fact they rip into it (Mary Holm's columns anyone), NZ Herald vs Chch property manager enforcing tenancies over the weekend etc. The banks are not pro-property. They get advertising from term deposits, share people & companies as well as property companies, clothing companies, retailers and such like. The media have a business to run and this is funded with advertising. They must be open to all in this climate. With your rants over the past couple of weeks anyone would think that you are feeling insecure that you can't live in a better house or suburb in Auckland?

Dear Nikki

Thanks for your concern.

Yes I am bitter about property prices. And so are many of my professional peers. Why shouldn't we feel a bit angry about a system that has made it difficult for professional, middle class households to buy an average house in a good (read GOOD, not high end) suburb????

But I am certainly NOT insecure.

For your information I do have a masterplan. It goes something like this.

1. Continue to rent for next 3 years. This will see my son through Auckland grammar. I could never afford to buy in the grammar zone, but have been more than happy to sacrifice that for my son's education. He is incredibly high achieving and Grammar has been brilliant for him.

We have been more than happy to make this sacrifice.

Everyone has their priorities and for us our son's future is more important than whether we own or rent

2. After 3 years, look to buy a townhouse in a good, but not so central suburb. Maybe somewhere on the North Shore or East Auckland. By then we would have saved a really good deposit, and I doubt prices will be much higher than now, in fact they'll probably be lower.

Matt - You seriously need to stop being jealous, you really just ooze jealousy

Nikki - Some of us own property, and think its rubbish how it is ridiculously over-priced, so much so your average kiwi can't even afford to buy their own home.

very strange comment

On the one hand you are saying I can't feel a bit bitter about housing costs, on the other you acknowledge that housing is way overpriced!

Strange strange strange

I'm not jealous of people who have got insanely in debt to buy some mediocre shack. The worst that could happen is 3 years down the track house prices have increased slightly, and I go from a 15% deposit to a 30% deposit. The best that could happen is house prices are 10% lower and my 30% deposit is equivalent to say a 40% deposit

Either way I am sitting pretty

Cheers

Matt your are a true Hickeyite, and for your devotion you are garanteed a place in Hickey Heaven, where you'll receive your reward...Hickey virgins....enjoy

"The banks are not pro-property." LOL Nikki are you from Mars! Only an RE agent would trying sell such tripe!

Thanks for this article :-)

Feels like a breath of fresh air compared with all the BS merchants out there.

Bernard, didn't you predict an actual fall in prices of 30% from the prices in 2007? And then you back-tracked and said probably 15%- and inflation does the rest?

So, is it an actual fall from the 2007 peak of 30%, not counting any inflation?

Or is it that when you factor in inflation over a period of time, plus some actual decline you make it a a 30% decline?

They are 2 quite different scenarios. Which one are you going for??

It's hard to analyse that graph without knowing what the standardised index on the y axis is. But to me it appears that we are in for an undershoot, like the 7 years between 96 and 03, whichever scenario plays out. That's a fall of far more than 15.5% from here. But whatever it is, it appears to take us well into the 20's before we get back to anything like a trend price. And that's all before this earthquake price destruction is factored in ~ or is that when we shoot past point D ?!

I know, lets all sell our investment properties and invest the money with Gareth Morgan investments. Nice try Gareth but I will stick with my property.

I agree that E is the "more reasonable" scenario - all other things being "normal", that is.

But then, all other things are not "normal" - are they? - not here, nor globally.

With such tremendous uncertainty, D (and even D-) becomes a real possibility.

E assumes inflation.......if we see deflation and then there will be a panic and its a self re-inforcing cycle from there...then the graph starts to look like D....however those that keep jobs and those on fixed incomes like OAPs should rejoice a wee bit...day to day they have more cash, except the Govn will be too broke to fund their healthcare if they need it....

regards

Gareth is basically saying what I have been predicting for months now. Property in NZ is going to die by a thousand cuts. Other than the central parts of Auckland it is going to drop in value a little month by month for the foreseeable future and when you throw in inflation we are going to see values drop in real terms to levels as Gareth predicts. If and when interest rates increase then the drops will accelerate even more. The average New Zealander is really starting to struggle with the daily costs of living which just seem to be getting worse by the day. Petrol is about to increase in price substantially. I think the oil companies are only holding back because of the earthquake. Food is going up by the day and petrol increases will make it even worse. Insurance will have to increase. There is no way values can go up let alone stabilise in such circumstances. More and more will put their rentals on the market as they tire of supporting the debt they have secured against them. If you thought last year was tough for New Zealand it will be a piece of cake compared to what is happening this year. If you need to sell an asset sell it now as things will not get better for many years.

Good analysis except point 2 that I believe is embarassingly naive. My heart surgeon was expensive according to some. Not to me. If you understand the real meaning of value you seek & find it. If you don't you don't.

The real house price trend in the first chart suggests an (about) 2% increase per year in the long term. If average house prices to average household income in the long term is constant (3.3) then this would mean real household income would increase with about 2% rate.

I'm not convinced this will be the case the next decades.

You can't argue against historical statistics. There's only one way this market can go and that's down. How long that will take is just crystal ball gazing which is why BH got it wrong a few years back. The fact still remains that the historical trends are off and need to recalibrate. Once interest rates go up then this could be accelerated.

All bloggers in denial will be shocked, maybe not today, next year or even in 5 years but at some stage infaltion erosion as well as real price drops will bring this back to where it should be.

I used to believe the house was bloated for years, but not now. After Dr Roof (Ron) invoiced me over $2000.00 for a simple leaking roof repair(one day, two people), now I think the house price is not that expensive.

So you bought a bloated house that needed serious roof repair and didn't knock that off your bid? Or are you saying the roofer ripped you off?

I went to a bayleys auction last week, was very funny. People are still buying houses at these ridiculously inflated prices, so obviously the chumps aren't tapped out yet, they will be soon though. The agents there were excellent sales people, there was this one woman in her mid 50's, an agent, whos property was being bid for, when it came to the bidding war between 2 people when it was the next person's turn to bid, she would stare them down as if to say if you don't buy this property you are poor, and you wouldn't want us to think you're poor would you? It was hilarious. The agents would glare at me and say "You down the back you haven't put a bid in all day, how about it?" I would just shake my head and say "CANT AFFORD IT MATE", but really I was thinking I'm not stupid enough to buy a shack for $500K.

Same in Nelson Muppet. The prices are still ridiculous. I'd even go as far to say $80 grand over for the average priced home. Renting is still the best option for now I feel. We will look at prices in the US in April and compare

The house was built in 1920, the Dr Roof just chnaged few rusty neils and sealed few places. It started leaking from before Xmas.

What I meant is the build and maintenance cosy is sky rocket now.

So predictably, the doom merchants are out in response to this story. Actually I take it as a massive positive that we are halfway back to reality, and the sky still hasn't fallen.

Thanks Gareth, good well researched story.

The Banks and the RBNZ are doing all they can to stop their property lending bubble from folding. This is why BH was abit off with his prediction, He forget about the powers at be and just how far the corrupt will go to pretect their own interests. I believe HP will maybe drop a little more but inflation and a bad economy will do the rest keeping things stagnant for a decade or more depending on anymore natural disasters heading our way.

hey justice...what's your difference between business capitalism and corrupt business?

or is it all corrupt?

Do you believe banks are not corrupt? Do you believe the RBNZ has been totally honest even after Bollards admissions in his book?

How did the global financial crisis take place again and who came out on top regardless Rob?

Capitalism and business is organic and carnivourous by nature..that's understood and a given, when you run on the field and play the game...if you don't like to play that sport then don't ...but don't whinge cos the great money beast don't come to tuck you in at night.

it's always been dog eat dog...always...survival of the fittest.

there's more than enough food to feed the whole planet 6 times over yet we have a commodity boom and prices are rocketing...why?...capitalism !!

so what happened to you, justice , to make you so bitter?

finance companies munch you up for being too greedy and believing that money does actually grow on trees?

ohhh spare me the lecture. Capitalism does not have to equal corruption!

Yet again Bernard we have people like Rob who when they can't argue the facts they have too resort to personal insults. Says alot.

The writing has been sprayed all over the wall....the economy is stuffed...deeply in debt as are too many households and so the level of activity has crashed and will stay dead for years...meanwhile the expected disasters have hit for which there was some level of insurance but not enough...and the rotting building govt business banking farce remains....but wait....China will save us....the commodities revenue will pay for all the stupidity...oh feck no it won't...most will go to the fatter banks which are farming the rural sector and the rest will be invested offshore by smarter farmers who told the banks to go to hell in the bubble. And the word is out that commodity prices will decline.

QED....Gareth is right....recession level activity for a long time as the property values fall and fall, likely below the long running whatsit....because that is the way of the world.

Meanwhile English is into borrowing big time....with almost no sign that the govt intends cutting the size of the bloated state sector...can't do that before an election can we old chap...might mean Goofy gets to the pig trough first.

And the local govt effort....what a friggin joke....rates raised above the level of inflation...or are we seeing evidence of the real honest bloody rate of inflation.......I think we are!

hey wolly..the yanks and the poms call it quantitive easing...bill calls it borrowing..same difference...inflation will munch it up over time!

I'm pretty sure that the vast majority of property investors don't realize that at any point in time a bank can call in their loan, meaning that they would have to sell their property. This being the case, do they really own their home if someone can take it away from them? I dont think so. They think they are property owners simply because the likelihood of the bank doing that is less than if you were renting and the landlord booted you out. That may be the case now, but we live in very interesting times, and there are tonnes of mortgagees on at the moment and still to come. The banks are the owners sorry guys, not you, the sonner you realize this the better.

Ain't that the truth. i love how many 'homeowners' as they call themselves actually also forget about paying thousands in interest which apparently is not "dead money" (on the premise capital gains will cancel it out)

Interest is not dead money in every instance.

For someone to have aroof over their head they can:

1. Purchase something for the amount of cash they have

2. Purchase something which may need some borrowings as they have cash to put into deal as well

3. Rent off someone else.

With 1 there is no interest or rent to pay so no dead money.

With 2 if interest is less then cost to rent house then interest is not neccessary dead money.

With 3 if cost of renting is less than the the interest you would pay on the loan then this rent is not neccessary dead money.

You an't simply say that everyone who has a mortgage has dead money by way of interest the same way you can't say rent in every instance is dead as well.

I have a house with a small mortgage. Whether I have amortgage or not capital gains or losses will still effect my equity.

Yes you can, paying of interest has no intrinsic value to anyone but the owner of the loan

"I'm pretty sure that the vast majority of property investors don't realize that at any point in time a bank can call in their loan"

Is there a special school somewhere that teaches the conspiratorially vulnerable this kind of crap? Maybe if the mortgage was signed behind a tinny house in South Auckland. Wanna show a clause in a mortgage contract with any major institution operating in the NZ market whereby the mortgagee can arbitrarily call in the loan without the mortgagor first breaching one of the covenants of the contract and then being given time to rectify such breach.

Maybe you should just comment on subjects you have even a slight clue about. How 'bout dem Warriors huh? Bet you seen a bigfoot once, eh?

Poor wee Vera, and all the other RE slaves...Your position just keep getting weaker by the moment and so you resort to ever more desperate means to stave off admitting defeat.

Maaate, 2010 was the best year ever. 100% occupancy and rent increases all round accepted without a flinch. And for those that still have mortgages more good news today. Things have never been better. Used to think this was a kinda risky business, but now sometimes it feels like ya just can't lose with property, maaate.

What defeat are you talking about??????

I don't think he implied "arbitrarily" exactly but I'm pretty sure a bank can call in a 'bank loan demand' at anytime much like they can change the floating interest rate anytime without a covenant breach

Buy yourself a dictionary Justice. "..at any point in time" just "imply" "arbitrarily', it practically defines it. Maybe the Muppet sat next to you at Drongo College.

No need really thanks. Muppet is right. A bank can call a loan at anytime if asked too by it's own creditors

A Bank would need to go into liquidation type administration for this to eventuate. When was the last time a registered bank in NZ was in this state???

Probably the closest we were was in 1990 when the BNZ was close to having its capital wiped out by poor lending in Corporate Sector and Govt had to pump in over $1b to recapitalise it, which by the way the Govt got all of these funds bank plus interest over a period of time.

whatever, point remains

What point, that you know the in's and outs of every loan document of every bank in NZ? I think not?

Yip. My floating part is on call, exactly as if it was an overdraft. The fixed part may be different, but I'm guessing that when push comes to shove, the bank can do what it wants.

Providing its within the term and conditions of the loan contract (and mortgage document).

And they do when pushed. ignore Money Girl and Aloe Vera. They are defending the Titanic ponzi scheme they bought into

You know when someone has run out of logical and rationale argruments when they have to resort to personal attacks.

If you think I don't think property prices can't go down well I do and have seen it on a number of occassions (late 1980's, early 1990's, flat market 1995 to 2000). Have seen it all and yes I still choose to have a property because I what a home "not a house" to have my family in.

A "home"is not an investment, its the choice of either buying or renting.

Yes I have investment in property, small commecial properties between $200k to $250k band, won't touch residential property due to poor yeild after allowing for all cost. These are all cashflow positive and able to retire debt and even have to pay tax due to profits.

PS please don't insult my intelligence by telling me I am some slave to Real Estate agents or some Ponzi scheme.

Overdrafts are generally on demand whereas term loans (like home loans) are over a documented terms.

A loan can become ön demand"if a condition or coveanant has been breached, which in other words means the borrower doesn't keep to their side of the contract and the Bank has to ahve some ability to remidy the default.

Interest rate changes are writen into loan contracts, you choose either floating or fixed. If fixed then simlply Banks can't change the rate within the term without breach of contract.

Which is why a fixed term is "dangerous" in a way...its fixed for say 5 years, but Im not aware the bank is obliged to renew your mortgage at the end of that as its a new mortgage....they can dictate any terms they want, from no find someone else to 30% interest pls....

regards

Two different issues:

1. Term of the loan which is say 25 years.

2. Fixed rate term.

At the end of the fixed rate term almost all loan contracts I have ever seen revert to the floating rate at the time of fixed rate maturity under the terms and condition as per loan contract.

The Bank is under no obligation to amend the terms and conditions ob the origional loan contract (and has to adhere to them),

Fixed rates are only "dangerous"if the term of the loan is the same as the term of the fixed rate term, e.g. 5 years fixed with 5 year term, and this normally only relates to business or commercial lending, not John Doe with a generic 25 year housing loan.

Vera, you are right. Banks simply can't call up loans because they think you nose is too big or any other crazy reason. There is a thing called a contract and a thing called a court.

I sometimes wonder whether contributers to this blog actually believe what they write.

Crazy reason, no....however I seem to recall my mortgage contract did have such a statement/clause ( it was a long while ago). The reality is unless you have a terrible credit rating or something pretty bad you can just go to another bank if the one you are with goes toes up...apart from that yes you could fight in the courts....the bank would be onto a PR disaster at that point and would the court allow it? where you have met your side....Anyway I would assume some other bank buys your mortgage debt from the receiver....which I think is what usually happens. Politically such a en mass event just wouldnt fly....

regards

Muppet King wrote "I would just shake my head and say "CANT AFFORD IT MATE", but really I was thinking I'm not stupid enough to buy a shack for $500K."

Should have shouted it out loud! How about this... direct action from interest.co.nz readers who pack auction houses and shout "I wouldn't pay $50K for that POS", placards reading "3x median multiple", "Remember the tulip bubble", "It's always a good time to buy... for the agent", "Suzanne researched this", "Bernard Hickey for Minister of Finance" etc etc.

I have done that on Trade Me a few times with a threat being returned that 'they will take legal action against me" hahahah, based entirely on my OWN personal stated opinion which is all it was!

HaHa...love it..

For some very strange reason prices on the North Shore City are still holding up. If you're interested to have a good laugh, there's a 2bdrm 70sqm house on Nile rd that's has a registered valuation of $515K. Been on the market for months.

Nothing strange about it, Billy. The 'owners' probably have a debt that they don't want to drop below to get out at break-even ( or thier 'promised' profit!). So they'll just try to sit it out - pay the loss in installments week-in, week-out. Lower interest rates will extend that scenario. But sooner or later all property gets sold! It's just a matter of whether people want to add the weekly loses to the ultimtate capital loss.

In Nelson such a home would be rated at around $265k which is still a joke

Billy, you'll find many of Auckland's leaky homes are on the Shore, it's really having an affect on demand / supply..as a result values are holding up.

It's not "values" that are holding up...it's asking prices. Those are two very different things.

Yeah rent is just dead money, interest isn't because its actually going towards something. LOL. You're way better off paying a ridiculous amount of interest whilst waiting 30 years for your debt to inflate away. Trust me, its way better to pay 80% of your wage on a mortgage than 20% on rent. Way,way better.

LOL, let's not forget the 2 year old $30 thou SUV they just financed off the lot which just lost 20% in value as they drove it off AND the maxed out credit card now being used to buy petrol to fill it!

I hope you're not serious? By your own definition one party is thus able to save 60% of their income while the other struggles to get by.

Yeah, right. And those of us who have been paying low rent for high quality places outside the main centres, while earning good money - and saving most of it - are really in the crap, right?

My money earns me interest, and I pay none. No debt here, not a penny owed to anyone for anything.

Meanwhile, the gumbies who thought it wasn't possible to lose with houses, poured every bean they had into "investment property", borrowing huge amounts to pay grossly inflated prices (which they were fuelling by paying them), and now owe everyone a lot of money they will probably never be able to repay.

Chances are these clowns will be in negative equity for the rest of their lives.

"So tell us Mr wise what's it like to finally be 'freehold' after all these years?"

"Aye...what's that you say...speak up young fella....I don't hear so well these days...who are you anyway?"

"I'm from the local paper Mr Wise...I'm here because you are now the owner of a freehold property"

"zzzzzzzzzz...................."

"You'll have to leave now ...Mr Wise needs his rest.....he is 98 you know"

Gareth, while I'm not necesarily saying that house prices aren't over inflated, I can't see how anyone can take the income to house price ratio seriously. Surely you must concede that interest rates play a big part in house prices. If interest rates over the past 10 years had been 10% instead of 7%, I can guarantee that house prices would be lower. So why would you believe that house prices should be 3.5 times annual income regardless of interest rates?

House price will be down In Christchurch by 30%. Not Auckland.

Good arbitrage then? Sell Auckland / Buy Christchurch. That leads to.....Lower prices in Auckalnd and higher in Christchurch as the incentive is normalised. That will lead to a lower market, nationwide. Best to just sell Auckland , then,and move to another asset type.

The RE mob and related sprookers will quickly chop all Chch data from the national porridge so they can keep to the lies about values...expect this announcement any day now. Can't have a wad of stuff cut 30% messing up the planned spin can we!

Be more than 30%..you cant get insurance..and wont for at least 6 months as insurance companies can not get re insurance for Chc as we are now to high a risk and it is not viable..cant even get car insurance. They will be cutting CHC out of any so called national housing data for at least a year or so i would suspect

Who was that poster on here who use to brag last year about all the investment houses he was buying up in ChCh?

Wonder how he's doing?

was it The Man..?

Yes it was The Man.

Gone from being a bass baritone in the website choir to a castrato ?

When we do our national moment of silence at 12.51 pm today... she we also remember The Man ?

I bet your hoping a few bricks landed on his head. Didn't know you disliked him that much.

But Wait !

Just landed in my inbox is a kind and gentle offer from ..ta-room ta-room:

SUPER OLLY !!!!!!!

Last year Olly Newland offered a small number of Empower Education clients a place on his Personal Mentoring programme -- at a greatly reduced rate: HALF PRICE.

That limited offer was quickly snapped up by people keen to take advantage of the chance to work one-to-one with a property Master like Olly -- to really make progress in any area of property investment (residential or commercial).

I've had enquiries about this, and talked it over with Olly. As a result, I'm pleased to announce Olly has agreed to repeat his offer, giving FIVE (just five) Empower Education clients the chance to enrol in his Personal Mentoring programme at a special 50% rate ('six month plus' programme usually $9,750 available for $4,875 incl GST.)

YOU'RE DA MAN , SUPER OLLY ...dial 0800 FREAKS4U

HAHAHAHAHAHAHAHA hope he's offering a free set of steak knives with that fabulous deal so it isn't a total waste of time and money.

This is how Olly is making money now lol, not from property, but simply by saying I'm rich I can show you how, for $5000. Olly is def tryign to squeeze out every cent he can, and good on him, if chumps want to go for it, a fool and his money is soon parted.

Thanks for the article Gareth, as ever you provide the reality of the market (somewhere in the vast space between Olly Newland and Bernard Hickey).

The only thing you've missed in my opinion are the ramifications of the quake on the whole NZ property market.

Key has now projected at least $20 billion - and like with all natural disasters this will continue to be revised upwards. The quake will take a massive chunk of GDP and ensure NZ has no growth in 2011. Without the quake, NZ was likely to have limped through 2011, but now the outlook is bleak.

Immigration, tourism, exports, unemployment will all take a big hit. Add onto take record petrol and food prices that will be here by winter and you have the recipe for disaster.

Like it or not the NZ property bubble is about to change from a slow puncture to a blowout.

Despite Mr Hickey's predictions being premature, I am of the believe he will be proved right - but not based on the factors he outlines. The quake was a horrific event for NZ - but like with all disasters will create winners and losers for years to come.

absolutely

immigration is going to plummet, emmigration is going to surge

Know a number of Wellingtonians and Aucklanders who say this is the last straw for them, they were already thinking of moving to Aus, the economic effects plus the potential for similar scaled disasters to hit the other cities has tipped the balance for them to leave

A big drop off in net migration, plus the other factors you mention (rising costs of living versus minimal wage growth) will pull housing down. What may have been a looming housing shortage will be pushed out by a few years

Hi Matt,

Am concerned about those kind of things too, but then read this today:

http://www.nzherald.co.nz/christchurch-earthquake/news/article.cfm?c_id=1502981&objectid=10709417

"The Viljoens said the earthquake hadn't made them reconsider moving to New Zealand from South Africa. Their granddaughter was born one minute after the September earthquake and has known nothing other than tremors as thousands of aftershocks have since rattled the city.

"I'd rather go through all the shaking than have those other problems back in South Africa," Mrs Viljoen said."

So maybe the outflow will just get replaced with such people and others from countries where governments send LAVs into to fire on the population, rather than help. Had to laugh last night, couldn't get some friends on phone so drove around to them and came across a LAV being used to knock down a dodgy garage before it collapsed into a home. We're getting our monies worth now I thought.

Cheers, Les.

If there is really a big drop in net migration, the bright side is the unemployment rate should go down, not up. If there's enough demand, salaries may even go up, so the cost of living might be less of an issue, especially if house prices drop (more purchasing power). Well, gotta be positive seeing our main customer has lost their premises in the CBD and that there have been no new offers whatsoever on seek in Chch since Tuesday (understandably).

The issue for NZ isn't so much owning property versus not owning property, it's a story of a lack of adequate diversification of the asset base.

Thats it in a nutshell, then they say things like "Oh but our stockmarket is so lousy", to that I reply, THEN DON'T INVEST IN OUR STOCKMARKET, INVEST IN THE ASX,DOW,NASDAQ,FTSE, chumps. Theres a killing to be made on the daq right now.

If a home owner has no mortgage, then prices do not matter? Any agent will tell you "as long as you buy and sell in the same market, you don't lose". Actually, those with no mortgage benefit from a fall in property prices as their purchasing power, the money they have outside the home, buys 'more house' when they swap for a replacemnent property. A lower price of anyhting has to be better for the buyer. Isn't that what we have been taught about any product? - lower prices for the same thing, are better.

Animal Lover, your statement is hyperbole too...NZ has billions of debt sloshing around in property...mountains of it...our private sector is one of the most indebted in the world...to say everything is OK in NZ is wrong.

Home owners that are mortgage free will still be affected when their house drops 15% in value. Maybe retirement gets put off for five years etc etc.

Who's exaggerating?

Have you noted the Current Account? Or Personal debt figures? Seriously, it's not spite or bitterness or envy . It's loathing a group who have absolutely no economic education whatsoever and continually fail to see the connection between cost of living increases and the property/debt bubbles. Living within means has become a nonsense to them.

Garath got one deal right with the Trademe sale but he knows diddlysquat about the property market.

The latest tragic event, plus the other factors ( leaky homes, no new houses etc) will shove up rents and prices whether we like it or not whether it's fair or not. and whether we agree with it or not.

It's already started, and this is only the beginning.http://www.nbr.co.nz/article/opportunists-exploit-extreme-demand-rents-…

And they will rent to whom? Those Cantabrians fleeing New Zealand as they have 'had enough'? Or those immigrants who will flock to the Shaky Isles into a pool of unemployment? Or those workers diplaced onto the dole queue and who look for accommodation with family and friends? Perhaps our young who emmigrate to Australia for chance of a job? Or those foreign students who will come to be educated under an exchange rate twice what it was when they enrolled in Year 1? The supply of tenants just got shorter, and shrinks ,every day!

Corrected link:

http://www.nbr.co.nz/article/opportunists-exploit-extreme-demand-rents-…

Opportunists exploit extreme demand as Christchurch rents and prices skyrocket

Created 01/03/2011 - 9:57am

NBR

Speculators have been quick to take advantage of the damage to commercial premises in Christchurch.

Rents and prices are skyrocketing, according to Colliers director in Christchurch, Hamish Doig.

Colliers has temporarily relocated to Russley on the western outskirts.

Some tenants on short-term tenancies have been told by developers that if they wish to remain in their premises they must buy them. Several transactions are understood to have been completed.

Mr Doig said that while it’s understandable that developers are being opportunistic, the financial effects on firms will be more significant as a result. “Revenues are going to be seriously affected – it will have a huge financial impact on those firms.

Tenants have been scrambling to find space. In one case, Collies signed a deal for space at $130/m2 and another tenant immediately bid $250/m2 for it.

Demand for alternative premises is huge and most available commercial premises had already been leased.

Commercial tenants were accepting whatever they could find, Mr Doig said. In many cases this meant squeezing into much smaller spaces – the notion of private offices was gone. In other cases tenants were moving into apartments or asking staff to work from home

The owner of Knight Frank in Christchurch (formerly Simes), Layne Harwood, said his staff is still assessing the 100 buildings they manage.

The biggest is Clarendon Towers in Oxford Terrace, one of the city’s prime office buildings. Mr Harwood said the damage was mainly around stairwells and fitouts but assessment would have to wait until the security cordon allowed.

His home in the city centre is damaged and offices trashed. He has relocated to the White Heron Hotel near the airport.

“We’re inundated with inquiries from corporate and some people are looking at pretty innovative solutions including portable offices and working from homes. We’ve got about 40 corporates looking for space. Tenants are having to make quick decisions. Most of them want to go to the western side of the city.

“Smaller firms like ours are waiting to see how things develop and continue to operate through electronic communications.”

Mr Harwood said two of his corporate clients were seriously considering the idea of a portacom village on some of the available land in the west of the city.

Instantly take away anybodies/companies support mechanisms and they will scramble; pay whatever it takes, until they get their bearings. Then? They move on. Leaving whatever it was that got them through, behind. No wonder owners of commercial property are trying to 'blackmail' tenants into a purchase agreement. In a few weeks, perhaps months, time, the market will again be awash with empty commercial buildings; that no one wants and no one is left to work in. The people, and the firms they used to work for, have either ceased business or relocated - for good.

So greedy short-sighted landlord parasites kill more genuine productive businesses with their grasping idiocy, and ultimately eliminate their own customers. Great. This'll work out brilliantly for everybody.

Is your rent money more "Dead" than the interest on a mortgage?

Why bother making that comparison while you think about the income from interest you have foregone on the deposit be it 5% or 50% of the purchase price?

Face up to the facts. The whole purchase price has an opportunity value

Conclusion. Owning your house ain't cheap

It is just the satisfaction of being able to exercise a few personal choices on how you live and having some certainty of tenure (bank willing, of course)

I wonder how those valuers are going to do their 'market price guides', today? Err on the side of caution, would be my bet, by making values lower.....just in case!

The only reason they go after the valuers is because the valuers have indemnity insurance and its a nice big fat target for the bank to get some money back when their dodgy lending practices let them down.

This is exactly what happened in NZ when it first hit the fan in late 2008 and 2009. This is the beginning of things to come across the ditch. Somehow I cant see the Aussie tourist market holding up that well in the next few years.

Good plain talking Gareth, just like your kiwisaver scheme.

Too bad it underperformed for 2 years and I left it.

SNAP

House prices falling (in real terms) is an absolute no-brainer, frankly I'm amazed they've held up as long as they have. With the price of pretty much everything going through the roof, the ChCh Earthquake, low GDP and virtually no savings who the hell in NZ has got a spare 500K for a badly made shack?

It all depends where the 500K badly made shack is. If it's in a provincial town no thanks, but if it's in a central Auckland suburb on a full site then yes please.

nobody but dont worry, the bank will lend it to you

If every trademan like Dr Roof is getting more and more expensive. I am sure the house price will not getting cheapper any more.

Now that most of us agree that the massive property bubble is deflating. A note of advice to

1. Property Investors : The party is over - Stop being in denial and looking for reasons other than the fact that the bubble is bursting. Please dont blame the Christchurch earthquake for any further drop in price if there is no other excuse on offer

2. First Home Buyers : The best strategy for potential homebuyers appears to be to wait a year or so. There's a good chance house prices may dip down further, given the current high inventories. That's to the potential buyer's benefit,

If property investers purchased property based on cashflow then the value becomes a non issue as the same amount of cash is coming in. The yeild or cap rate off purchase price remains the same. It only becomes an issue if they need the "value"of ther property for some reason like to support new borrowing etc.

Ask the long term sucessful property investors"cashflow is key".

Neither the article nor the comments seem to mention smart growth zoning - the key driver of urban land prices. Smart growth is really dumb anywhere but in an earthquake zone the herding of people into high rise in the CBD, and elsewhere, is much worse than dumb. Until zoning is relaxed prices for free standing houses and small low rise apartment blocks will hold up very well. If they do show signs of faltering then the government can be relied upon to shore them up with immigration.

i'll tell you what's really dumb and that's your assumption that smart growth exists anywhere in nz

Sue Bradford..where did that come from?..most people on this site think the WWG was great and needs to be implemented to the fullest...we're all mostly of a right wing persuasion on this site with an interest in the fact that NZ property is massively over priced...Sue Bradford, you are making my stomach turn..

Does any here thinks the mortgage rates in NZ will be very low for a very long time? I see many commentors talked about the rise of mortgage rates, but I am afraid that the NZ OCR may low for long term.

Please advise!

Need advice. I want to buy a property in the central Auckland area (Ponsonby/Herne Bay). How on earth can I work out what to pay? Get the QV and take off 12%? All of this confusion over house price direction is making it very difficult for a genuine buyer who doesn't want to wait three years and who has a partner who likes "a project".

Pay only what YOU think it's worth, not the owner, not the REA, YOU and your partner. Forget everything else! Don't get caught up in QV , GV, rubbish. Bring in a chartered property surveyor IF really concerned

Yeah - you decide what you want to pay 'cos as a buyer what you're willing to pay is what it's worth. Then as you miss out on each place because someone else is willing to pay more just keep reminding youself that they are just idiots for paying too much. Stick to what you think it's worth and remember there is no such thing as supply and demand, only what you as a buyer think it's worth. If your low offers are rejected just keep walking away. If you walk away to the south you'll eventually get a low offer accepted (might be in Manurewa by then, but hey - you'll be the winner)

Private sales are the best way to get a bargain. Check them all out. Funny that Gareth recommends selling privately....he should stick to finance advice.

Take off 12% - you are kidding right? I think in those areas you will need to add 20% to the CV! There are no bargains in Central Auckland at the moment, so unless you are willing to pay top dollar you are wasting your time.

Animal lover, your comments are nonsense.

While we are on about property...spare a thought for the latest exposure in wgtn..Dunne correctly calls for the public to be told the truth about the safety or lack of it regarding the buildings people live and work in...seems it's all secret whether a building is earthquake proof or not...and the council are plodding their way through checking buildings...and the public can find out for a $$$$ to the council but only on pre 1976 structures....

What a friggin joke.

There will be post 76 structures that are as safe as the PGC and CTV buildings in Chch....like standing death traps...but you are not going to know...because the pointy heads think post 76 stuff is safe...that's complete bullshit.

So wgtn gets a wee 4.5 shake last night....the 8.2 which is overdue will flatten the place.

It was a good jolt.....heard/felt it coming.....You cant say how big it will be, some buildings are designed for that 8 but very few....reality is ppl live and work here and are blind to that risk everyday...its known, just ignored just like Chch ppl.

Buildings generally in Wgtn are more earthquake resistant than Chch....mostly wood which will flex and not brick which doesnt.

regards

"resistant"...maybe Steven but factor in the 'Redcliffs' that is much of wgtn...my money is on the data having already been compiled but kept from the public as to which hillside suburbs will be toast in wgtn...the rock is shit every which way you go...so not only is it a secret as to which post 76 structures in the region are poorly designed and nowhere up to modern code..but the info on the hills prone to ending up in the valleys or the sea also remains secret......

Residents in wgtn need to know the Beehive was built to cope with the expected 8.2....bugger all else would come near that.

The data on the slide risks indeed all earthquake risks (sinking, rising, liquidifcation, tsunami etc) was known 12 years ago+ I worked for the structural engineering company that did the work....they had completed that when I joined them...I think its available via WCC....I know the estate agents were p*ssed with its release, but reality most ppl didnt look at it.

So from memory they highlight areas of greatest risk....so for instance some areas have a single risk say on the cliff areas of Vogeltown the risk is slipping....Other areas such as say Kilbernie could sink, rise or get tsunami'd....so they have 2 risks....others could also have the heights above them fall on them and be in danger of a tsunami and sinking....so they have a triple risk....so some could have all 4 as they are on ground that could liquify...Some are right on the motorway which is the fault line.....Ministry of Health is there, but its built for some super high earthquake shocks as a result...8.9 or something, its the highest I know of....Yes the Beehive is high (I dont recall what) its the civil defence centre I think as well as Govn....but its suseptable to tsunami and sinking/rising....lots of other newer buildings have shock pads etc...Te Papa comes to mind....I think the old BNZ building got isolated as well. When a commercial building gets a major upgrade it has to be brought up to the new std....and this has been happening...or it gets re-zoned as residential...now that's a worry but the info is there for ppl to make that decision....

Reality, the differences are fractional....but knowing these I bought where I bought so Im as low as I could get, and with a wood structure...which over time I have improved/fixed where its been a bit marginal IMHO.

regards

Like to see arguments against this... Get on with it.

There are none....

regards

Life is full of risk. That's what makes it most interesting. Dunne needs to get real. You could be anywhere in a large EQ and still get seriously hurt. No building is 100% safe particular old brick ones so people should just assess the risk themselves using (dare i say it) 'commonsense'

Surely Dunne is an advocate of "gods will" anyway? or is he NOW a believer in Mother nature and plate tectonics . Can't have it both ways.........opps sorry you can IF your a hypocrite!

"people should just assess the risk themselves using (dare i say it) 'commonsense'",

... and information.

More than happy to trust the experts... and applaud the high quality of their work, when it is published. There is nothing to hide.

Like they did in the CTV building? No such thing as an expert when Mother Nature comes a calling. Anyway, my initial point was it's a waste of time and money. If Wellington had not already assessed the risks per building decades ago then I guess they felt their was no need or 'point'.

From the lips of an "expert" in today's Herald.

Dr Risatu said it was impossible to predict when the next big one would strike the capital.

"All we can do is basically look through the past historical and geological record. We know that the faults exist, we know that the earthquakes do happen, and we can figure out on average how often they happen and when the last one was. But that's about the best we can do."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.