By Bernard Hickey

You know an economic idea or trend has crossed over to the mainstream when a big ratings agency starts talking about it.

The ratings agencies were among the last to realise that much of the sub-prime mortgage debt they had given AAA credit ratings to was turning toxic in the mid 2000s.

They were the last to downgrade Greek and Argentinian bonds before their Governments defaulted and forced restructures.

Eventually they did smell when their debt had gone rotten, but it took a while.

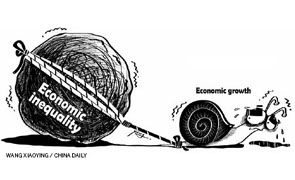

So it's notable when one of them warns that growing income inequality is slowing economic growth.

Up until a few years ago, this was an idea that only those on the more socialist left were saying. It was an issue framed around fairness rather than economic efficiency.

This month Standard and Poor's, one of the two big global ratings agencies, warned that growing income inequality in the United States was slowing growth in the world's biggest economy.

It lowered its growth forecast for the next decade to 2.5% per year from 2.8% because of it.

"Aside from the extreme economic swings, such income imbalances tend to dampen social mobility and produce a less-educated workforce that can't compete in a changing global economy," Standard and Poor's wrote in the detailed report.

"This diminishes future income prospects and potential long-term growth, becoming entrenched as political repercussions extend the problems," it said.

"Our review of the data, as well as a wealth of research on this matter, leads us to conclude that the current level of income inequality in the U.S. is dampening GDP growth, at a time when the world's biggest economy is struggling to recover from the Great Recession and the government is in need of funds to support an aging population."

Standard and Poor's is well aware of what can go wrong when a large group of households see their real incomes fall, as happened in the United States over the last two decades.

To make up for those lower incomes, the households' first instinct was to borrow more in the expectation that they would eventually catch up once their incomes rebounded. But when incomes kept falling for a sustained period and the borrowing kept on at the same rate, those household budgets eventually hit a brick wall.

That's what happened during the Global Financial Crisis. US households defaulted on their mortgages and brought the world's financial system to the brink of collapse.

That has focused the minds of ratings agencies, bond investors and banking regulators globally.

Standard and Poor's suggested various measures to reduce inequality in the United States, including shifting income to those on lower incomes and improving access to education and health-care.

America is, of course, a very different place to New Zealand.

Our education and health-care systems are much more publicly funded and accessible to people across the income spectrums.

Our minimum wage is much higher than America's and over the last 15 years New Zealand has reintroduced a significant amount of income 'shifting' to those on middle to lower incomes, particularly those in working families and the elderly.

Younger, childless people and those out of work have had a much tougher time.

However, the measures that were taken have helped stabilise New Zealand income inequality levels since the late 1990s, but did not improved them at all. Surveys show income inequality is growing as a political issue in New Zealand, but has yet to reach the sort of fever pitch that it is now among economic policy makers and some parts of the political spectrum in the United States and Europe.

New Zealand's relative success in avoiding the blowout in inequality levels seen in America in the last 15 years should not lead to complacency.

The work referred to by Standard and Poor's indicated there are forces of economic gravity at work that naturally push inequality higher. That's because cycles of poverty deepen inequality and the growing political power of the wealthy entrenches and deepens that inequality by introducing tax cuts and protecting special interests.

The work has to be done year after year to reduce inequality or at least stop it from getting worse.

New Zealand's political debate has yet to acknowledge the economic payoffs of reducing inequality. A healthier, better educated and more stable population is much more economically productive.

As Standard and Poor's has forecast, reducing inequality is actually a way to improve economic performance, rather than purely a debate about fairness or 'keeping up with the Joneses'.

Redistributing income and making healthcare and education cheaper for the poor is actually an economic growth strategy.

---------------------------------------------------------------

A version of this article first appeared in the Herald on Sunday. It is here with permission.

18 Comments

... well of course , Bernard , we've all completely forgotten the GFC , and now take S&P seriously .... but never mind their remarkable incompetences of the past .... push on , what !

If you want to cast your mind back through human history , the one era when we had greatest income equality was as nomadic tribesmen ... and tribeswomen ... and tribeskiddies ...

... income inequality has evolved as we've progressed ... the poor havn't been completely left behind , they've made incredible progress too .... colour TV and Lion Red in their caves ... lotto by mammoth-fat-candlelight ..

But the rich have outpaced them many times over ... and unless you wanna switch off progress and innovation , this is just a cost we have got to bear ... and these are the prime drivers of GDP growth , not who gets what in the lolly scramble ... technological advancements under-pin our prosperity ...

.. but hey , it makes a change from your regular Sunday attempt to stir up the resident xenophobes ... crack on with the socialists for a change of pace ... you're such a wag , Hickey !

...you're such a wag , Hickey !

You are not wrong GBH - add a tinge of historical revisionisn to the mix and we have a ratings agency tale banishing a little more than incompetence.

The ratings agencies were among the last to realise that much of the sub-prime mortgage debt they had given AAA credit ratings to was turning toxic in the mid 2000s.etc

Reuters reported this:

Between September 2004 and October 2007, as stress in the housing market was starting to emerge, S&P delayed updates to its ratings criteria and analytical models, which weakened its criteria beyond what analysts believed was needed to make them more accurate, the Justice Department said.

During that period, according to the complaint, S&P issued credit ratings on $2.8 trillion worth of mortgage securities and some $1.2 trillion in related structured products.

It charged up to $750,000 per deal it rated, which meant that S&P viewed the investment banks that issued the securities as its main customers, according to the complaint.

In August 2004, the head of S&P's commercial mortgage-backed securities sent an email to her colleagues and said they planned to meet to discuss adjusting criteria "because of the ongoing threat of losing deals." Read more

Its strange isnt it Jamin that people recognise that retailers will try to sell you things that you may not be able to afford, and most people accordingly will run a critical eye over it and most will make sensible decisions based upon their finances as to what they can and can't buy. Why then do some people not understand that banks are in the same business of selling things and equally why don't people not look at their financial situation and based their decisions on that the same as they do in a shop - personal responsibility applies in all cases. At least banks have a credit risk on you and have a vested interest in not creating financial stress but nothing beats the ability to think for yourself and owning a calculator.

I absolutely love the free credit a credit card brings me because I repay it in full each month. You may well know yourselves as well and know you won't have the discipline to do that over time, then its easy, say no.'

@Grant A - Why then do some people not understand that banks are in the same business of selling things and equally why don't people not look at their financial situation and based their decisions on that the same as they do in a shop - personal responsibility applies in all cases.

Collectively the nation has the same inability to manage the books at both a sovereign and personal level.

The government's 2013 budget projected that net core Crown public debt in June 2015 will be $68 billion, up from a low point of $10b in June 2008.

That $58b increase represents about $33,000 per New Zealand household.

Future ministers of finance are saddled with higher ongoing interest costs and future taxpayers are saddled with higher taxes to cover those costs.Read more

Are we in need of better equipped politicians to deal with this vicious circle dilemma?

Or citizens with a deeper understanding of their own collective limitations? Apparently neither can be sourced within our borders if we are to believe Moody's;

In terms of challenges to the country's creditworthiness, these include a continuing reliance on foreign savings to finance relatively large current account deficits, which have been evident for the past four decades, according to the report.

As a result, New Zealand's major vulnerability -- despite the absence of any problems in accessing the global capital markets -- is its dependence on foreign capital inflows, and its negative net international investment position is the largest of any Aaa-rated country.

However, Moody's notes that a large portion of these liabilities belong to the subsidiaries of Australian banks and, given the strength of the parents, these are unlikely to represent a significant risk to the sovereign.

The last comment might soothe some, but not NZ depositors funding the domestic banks post the RBNZ OBR diktat demanding they will re-capitalise any catastrophe with their own funds - they certainly are in need of a higher return than is offered to shoulder this unspoken burden. Read more

Yes exactly my point Steven, our ambitions as a nation are currently not matched by our lack of ability to earn and save for it - the banks need to access offshore funding to finance the public's requirements is a sure sign of that . And yes, it is a real vunerability for NZ but if youre going to borrow more than you save as a nation you're going have vunerabilities. Certainly we could have banks paying deposits insurance (FDIC) type, but who really pays for that, the customer. With regards politicans, I guess you can do comparisons, and since the demise of the Muldoon years the respective Govts have done a better job than most hence our current 26-28% (and about to fall) net debt to GDP ratio compared with say the 56% of Germany, 90% US,France & UK, 143% Japan, and 176% Greece etc. Where we have the major negative comparitive problem is in household debt at 145% in NZ compared to most, but not all, OED countries that are comfortably below 100%. It is that massive vunerablity which was not the case back in the early 90's when it was less than 60% - our ambitions outpaced our ability to afford it in the last 25 years.

To my mind public financial education is one of the major priorties for this country, something set up and driven from outside of the schooling system (not skills many teachers necessarily have themselves) but taught through the schools by these outside groups - hopefully within a generation we have raised that level of knowledge that will not only assist people in their private lives but might also assist in being realistic about what they can and can't expect from our Govt.

To my mind public financial education is one of the major priorties for this country

Maybe we could start here - how many of the invited earn a tax paid export dollar to warrant such extravagance?

Luxurious holidays in the south of France or Rarotonga and an internship in New York are among the prizes on offer at an extravagant school fundraiser.

A 41-page catalogue detailing the auction items sets the scene for the opulent evening where guests will "reach for French bubbles under a backdrop of gorgeous crystals, flowers, a fountain and some of the world's finest fabrics".

Organisers say the money raised at the "stellar event" will be spent on arts scholarships, mentoring opportunities and "new acquisitions for our contemporary art collection".

Auction items are either gifted by well-known firms or donated by wealthy and well-connected parents. Read more

I believe all countries are suffering from trying to fund the activities of government more and more from earnings (PAYE) and sales (GST) and excise (cigarettes, petrol etc.) taxes. And there is a double-whammy in this. The large, globalised corporates who are employing all the tax minimisation schemes are at the same time, and with equal fervor, implementing ways to reduce their wages bill - whether it be by opposing unionism, offshoring jobs, casualising local jobs and reducing employee benefits whilst denying pay rises.

It seems pretty simple to me - there is more than plenty 'money' in the world - and not only ain't it not trickling down to the workers, the taps been all but turned off to governments as well. They (governments) were complicit in this - now they don't know how to re-set it without losing the funding of their backers. Dirty politics indeed.

If NZ allowed cheaper new houses to be built through the various policy levers that have been discussed endlessly here and that gradually flowed through the whole housing market. This would reset house prices with respect to income (and therefore GDP) to our historic average of being betweem 3 and 4 household income. Household debt would fall below 100% of GDP. This would allow the country to borrow more for productive/investment purposes. It would also restore some equality to those who are less wealthy. This being the point of a recent Bernard Top 10 where some of the Pickety rising inequality may be explained by rising house costs relative to income. If housing became cheaper it would be a win for economic efficiency and equality.

It's a fact of life that the have nots want what the haves have and unless they have access to credit cards and instant finance type companies they will never get it.So they have a choice ,borrow,steal or go without.

I think you will find that most of the folks who seek out the instant finance type companies do so not for consumer discretionary type spending, but for what all of us would understand to be basic essentials.

The most common of initial debt purchases (and I say initial because once these interest rates get applied to that loan shark loan, many borrow again to fund food and rent because the loan repayment starts to eat into that part of the budget) has to do with private transport expenditure (i.e., something needs fixing in order to get a WoF, can't afford the registration fees, old car dies and new one needed etc.) and most of this transport is needed in order to keep a job (large majority of low paid jobs are shift and split shift hours, places and times not serviced by PT). You might be very surprised how many of the lowest paid jobs require you to have your own transport.

The second most common debt purchase relates to accommodation - landlord decides to sell property and one or two weeks rent in advance + bond needs to be found before one can secure (i.e., sign up before taking up residence in) the new property. And the third most common debt purchase relates to borrowing for travel costs associated with either illness or death of a family member (i.e. parent or sibling, often overseas).

So, it isn't a matter of go without - the loans from these loan shark type loans are predominently taken out to fund what are simple necessities.

I think youre very right in that Kate and its a shame that they're forced to consider Instant Finance type funding to accomodate it. In those proven circumstances it is one where I for one do think there's merit in some form of social assistance (although I thought there was some) at modest rates to get people through that situation, rather than burdening them with a debt many will never be able to extract themselves from. It has to be paid back over a reasonable period but not at usery rates.

I appreciate what you're saying about social assistance - and indeed there are some of these emergency-type grants available via WINZ. But in the main, most of these people are not WINZ beneficiaries - so don't understand that working people too can seek out WINZs help - and their pride too comes into play.

What we are seeing are very hard working, simple, family-orientated people - with both adult partners working - getting into financial trouble with these unscrupulous lenders. One could argue for more social assistance, but I'd rather argue for a living wage - as that is what allows the low income families to retain pride and respect within their nuclear family. These are parents who want to raise their children to appreciate an honest days work.

In addition to a living wage - government could change the driver's licensing and registration regimes to make it cheaper to become a full licenced driver (none of these ridiculous graduated steps, each costing a fortune to a low paid family). And where the government recently gave a registration cost break to those of us with late model vehicles .. well, words fail me in terms of targeting to reduce inequality - absolutely the opposite with that one.

We also have Rates Rebate Scheme for low income homeowners but no equivalent for those in private rental housing who most certainly pay for rates as part of the cost of rent indirectly. As opposed to an accommodation supplement, why not instead extend the Rates Rebate Scheme to renters. Point being, the Rates Rebate is just central government funding local government services at a slightly higher rate than they presently do - so not so much a handout as a tax redistribution between layers of government.

Anyway, I could go on about the small things governments could do that could make a huge difference to folks on low incomes but that's probably enough from me :-).

My main point being, when considering more welfare, also consider the effect on people's pride. A more just and equitable society is always far better than greater and greater moves toward middle and working class welfare. Employers need to step up to the plate. Many of the lowest paid jobs (cleaners, rest home/elder care workers, fast food chains etc) are within some of the best performing blue chip corporates. They can afford to pay more - lots and lots more.

Anyone know when jk is doing his speech today? Something on housing to be annouced for fhbs..

https://www.national.org.nz/news/features/first-home-buyers

There ya go. Price caps up and will be able to withdraw ALL kiwisaver for first home deposit....

Cynical stuff from National and John Key. Straight out subsidy of the dsyfunctional housing market. Do they have any creditability left?

National has been telling us for six years the solution is supply side measures. But they failed to implement effective reforms. So the housing bubble re-inflated and the Reserve Bank had to implement loan to value restrictions and interest rate rises. Come the 2014 election campaign the government instead of working with the Reserve Bank just adds fuel to the bubble with a demand side subsidy for new builds, using taxpayers money and the private savings of the young -Kiwisaver.

The end beneficiaries will be land bankers and property developers not first home buyers as they grab the increased subsidy for themselves. John Key is undoing the hard work of the Reserve Bank. Expect further interest rate rises and an over valued NZ$ if National gets re-elected because the Reserve Bank will have a bigger housing bubble to deflate.

Easy credit for home owners is what caused the GFC. Surely the lesson is that economic problems can no be solved by more borrowing.

Deeply cynical politics from a politician fast getting a reputation of saying one thing and acting in another way.

What is contributing to this issue of the middle class going basically nowhere, is this outsourcing of service jobs.

The pace of it seems to be ramping up.

I think a lot of people would be quite surprised how many quite well paid jobs are being lost to Bangalore in India, and now other part of the world like Manila, and China.

Most commonly helpdesk, and other IT jobs, but it seems to be spreading reasonably quickly to other types of office jobs.

Quite often these are reasonably well paid jobs that are going.

Nigel Latta touched on it a little a few weeks back on his program, and he also seemed to be of the impression, that this is definitely something that is ramping up.

It's been happening in the US for a few years, and has also been brought up as one of the reasons why the middle class in the US are struggling.

People in the manufacturing industry probably wouldn't be overly sympathetic, as that industry got decimated, by a similar process.

But I think it's definitely something to be concerned about, given the very high percentage of the country that are in service jobs.

Auckland housing must still be undervalued in what is now an international market since plenty of foreign investors are still buying property here.

I expect that any efforts to make Auckland housing cheaper will be thwarted because as it gets cheaper (or more expensive at a slower pace) it will also become even more affordable and attractive for foreign buyers. As foreign buyers bid on property, their effect on prices will run counter to any efforts to make housing cheaper reducing the efficacy of any efforts to make it cheaper.

National's increased Kiwisaver arrangements for FHBs should increase demand for housing and so should increase prices somewhat but at least it will give kiwi's an advantage (or reduce their disadvantage) over foreign investors who will often have very cheap money.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.