By Cameron Preston*

This month marks the 4th anniversary of the February 2011 earthquake and the halfway point in the settlement of residential “over EQC cap” claims held by the private insurance industry.

Back in March 2013 the Insurance Council of New Zealand (ICNZ) was at pains to convince people that there “is no insurance monster out there trying to delay, deny and defend” and such beliefs are urban myth.

Mr Tim Grafton, CEO of the ICNZ stated:

“They are not getting financially better off by delaying claims…Demand surge cost inflation will run to double digits [and will] be far in excess of any money retained by insurers and reinsurers in the bank earning less than 3% after tax on their bank deposits.”

It is no secret that the 20th Century’s most successful investor, Warren Buffett, uses his company - Berkshire Hathaway’s - insurance and reinsurance businesses to generate a significant amount of “float” which he puts to work investing across his other businesses.

Building “float” allows Berkshire Hathaway to effectively operate with zero debt which is key to its extraordinary success.

Mr Buffett writes an annual letter to all his shareholders personally, and in his last letter he explains to his shareholders the idea of “float”:

“Berkshire’s extensive insurance operation again operated at an underwriting profit in 2013 – that makes 11 years in a row – and increased its float. During that 11-year stretch, our float – money that doesn’t belong to us but that we can invest for Berkshire’s benefit – has grown from $41 billion to $77 billion. Concurrently, our underwriting profit has aggregated $22 billion pre-tax, including $3 billion realized in 2013. And all of this all began with our 1967 purchase of National Indemnity for $8.6 million.”

What Mr Buffett is differentiating for his shareholders is two sources of profit from Berkshire’s insurance and reinsurance operations:

(1) Underwriting Profit – That is the traditional profit after deducting the cost of claims made in any one year from the premium revenue earned; and

(2) Investment Profit – As insurers receive premiums (including reinsurance recoveries) upfront and pay claims later, this leaves them with large sums – money called “float” that will eventually go to others. Meanwhile, insurers get to invest this float for their benefit. – It is “free money”.

Mr Buffett goes on to explain:

“If our revolving float is both costless and long-enduring, which I believe it will be, the true value of this liability is dramatically less than the accounting liability…. we would happily pay to purchase an insurance operation possessing float of similar quality to that we have – to be far in excess of its historic carrying value.”

This goes some way to explain why Mr Buffett was interested in AMI when it was put on the block in 2011.

So that brings us back to the ICNZ statement that NZ insurers “are not getting financially better off by delaying claims”.

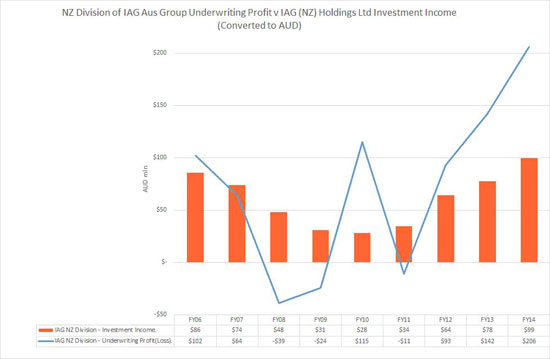

To understand whether that statement is an urban myth, let’s look at insurance giant IAG’s NZ Division results since 2006, separating underwriting profits and losses and investment revenue (in AUD):

You can clearly see the underwriting losses (the blue line) that occurred after the GFC (this is part of the normal insurance cycle – ie people tend to claim on insurance more when the times are tough) was compounded by lower investment returns at the same time as financial markets tanked (the orange bars).

However since the Canterbury earthquakes in 2011, a year in which IAG’s underwriting loss was very small thanks to reinsurance, both underwriting profit and investment income have exploded.

Underwriting profit last year was double what it was in 2006, thanks in large part to substantial premium increases.

However the Canterbury earthquakes instantly boosted IAG’s “float” as an influx of recoveries were made from reinsurers.

By not paying out on claims in a timely fashion, IAG was able to hold on to this increased “float” and use it to earn investment returns. Last year that equated to investment revenue of AUD$100 million attributable to IAG’s NZ Division.

And that is only what IAG are declaring. It would not be a huge surprise to this writer if the AUD$100 million recorded in IAG NZ Holdings Limited’s financial statements is only part of the total investment revenue from the increased float.

Total investment revenue for the Group last year was AUD$360 million, however IAG admitted just before Christmas that their Canterbury earthquake liability has been undercooked for a second time.

Even if IAG’s NZ accounts are taken at face value, you can see that it is in fact a myth that IAG is not currently financially better off by delaying claim settlement.

Whether demand surge kicks into double digits is yet to be seen.

At present most folk seem to be happy to believe the ICNZ’s statement that somehow by insurers holding onto claim payments for 4 years plus, instead of paying them out means “they are aren’t financially better off”.

I think Mr Buffett would disagree.

He has built his empire on that very premise.

Although in Mr Buffett’s defence he does state:

“Unfortunately, the wish of all insurers to achieve this happy result creates intense competition, so vigorous in most years that it causes the P/C industry as a whole to operate at a significant underwriting loss. This loss, in effect, is what the industry pays to hold its float.”

That intense competition is the element we lack here in New Zealand.

The lack of that important element is no urban myth, and it appears that competition or regulation is the only way to tame this particular insurance monster.

No doubt Mr Buffett would admire how this insurance monster is currently staying afloat, trouble is, he knows they have a propensity to sink pretty quickly too.

---------------------------------------

* Cameron Preston is a Christchurch homeowner who has longstanding unresolved quake insurance claims.

8 Comments

Enlightening piece, thanks.

They are better off holding off payouts so long as the total cost remains within its reinsurance limit.

If inflating costs and the resolve of claimants to get their full entitlements pushes the liabilities beyond what is covered by their reinsurance, then any benefit of holding off will be lost.

It is a risky business for an insurer to punt that total insured losses will not grow when most policies have no upper limit on a claims value.

I am uncertain of when reinsurers are required to make payments (when the insurer has paid the claimant or when the claim amount is known? Perhaps Cam, Gareth or Bernard could answer that?)

If it is when the amount of the claim is known, then the insurer has a huge incentive to establish the cost of the claim and then take as long as possible to actually settle the claim...

I think that is an excellent question for IAG - my understanding is that it depends on the reinsurers "layer" and contract.

However a search of the Companies Office website for IAG NZ Holdings certainly shows that their investment balance has risen dramatically since the earthquakes.

One has to wonder what that $3bln is invested in and why it is not going to homeowners?

(Low quality, unsubstantiated comment removed, Ed. See our commenting policy here - http://www.interest.co.nz/news/65027/here-are-results-our-commenting-po…)

THis Article should be brought to Every New Zealanders Attention-- especially the Profitability of the Insurance and Re-Insurance Industry.

In the aftermath of the ChCh Earthquakes ---- AMI was blithely sold off to IAG by Earthquake Minister --Gerry Brownlee --and I presume Prime Minister John Key was advised of the situation, or was he ??

Brownlee --separated off the worst of the Insured Properties and placed them within Southern Response (also called NO RESPONSE) with the NZ Govt picking up the TAB, or maybe what they got for AMI, and was used to fund Southern Response.

But this all made AMI saleable to the Australian Company.

AMI was a Mutual Insurance Company --- and had been built up as a business by hard working New Zealanders over many years.

I wonder what the Australian Insurance company Paid for AMI ??? It has not been revealed.

Brownlee should be Sacked for this Disgraceful decision !!!!

Put the boot on the other foot ---- if there had been a National Disaster in Australia, and one of the Australian Insurance companies failed financially, and was bought for a song by a New Zealand company --- we would hear the Australians whine from here.

>> Journalists should be asking some hard questions of the Government about this.

>> Australia is taking far too much money out of New Zealand already via the main Trading Banks.

AMI was sold for $380m. They sold of the bit that was still worth something, and the government still has to put in $500m to ensure that there is enough to pay claims.

Without doing that there was nothing to sell.

Regretfully Mr Preston has mischaracterised the concept of "float" that so attracts Warren Buffett. The US insurance businesses that he has largely invested in are very different from NZ insurers.

Float is generated when premiums are taken in and held for a period of time before paying out on a claim. As the US has no "ACC" these claims relate to injuries, typically for injured workers. When an insurer has a claim for an injured worker, ie they have a back injury, then they have to put away funds to cover the whole claim for the estimated period they will pay out on. Where this is a serious injury, the cost can be millions. The insurers put away a discounted sum for the whole period, these periods can be up to 30-40 years in some cases.

This is what ACC did some years ago when they were trying to "fully fund" the scheme.

A large US insurer like Berkshire Hathaway can have billions of dollars reserved in this way, and can generate significant returns over a long period.

A major difference in NZ is that you cannot generate a significant float, because you cannot put sums away for the same length of time ie 20-30+ years.

IAG will make some investment return, of course, but not in the same scale

With the earthquake, as with any large event, once the insurer's retention is exceeded it is the reinsurers that are paying, so there really is no significant benefit for insurers to not pay a claim. It really is true that they want to pay the claims.

Reinsurers are involved in the process as well. Surprisingly they want to pay valid claims, but they pay when there is final evidence of the quantum of the loss and the insurer is ready to pay. They are not paying huge sums to the likes of IAG, who then sits on the money.

If you look at insurance accounts they are actually quite complicated. What reinsurers owe insurers is an asset on their books even though they haven't recieved it yet, and the claims are a liability related to what they think they will pay. If you want to see how much they received from reinsurers, look at the income statement. You also have to remember that other non-earthquake claims haven't gone away.

There is no big surprise over investment income, and IAG's income increasing - it has to to help them make a profit. There is no conspiracy theory here, IAG is also 2/3 bigger today than in 2011

Insurance companies, just like all other companies, need to make a profit, otherwise they wont be there to pay claims. IAG today has exactly $1.5b in share capital today - in 2011 it was $0. Somebody - that is IAG Australia, has had to put that money in to ensure IAG NZ is solvent to pay claims. That capital needs a return.

What amazes me is that reinsurers are still willing to risk their capital here to support insurers, and ultimately, allow all of us to insure our houses.

"o there really is no significant benefit for insurers to not pay a claim.

"

Their premiums go up if they make claims.

"What amazes me is that reinsurers are still willing to risk their capital here to support insurers, and ultimately, allow all of us to insure our houses."

there is a reason many people premium portion went up 100-500%

The insurance company does a calculation they like to call "risk assessment" . The re-insurers also don't self-insure - although the risk they pay for is much smaller.

Of course reinsurers are willing to risk capital.

that's what insurance companies do.

And they try to set it up that tomorrows' claim money comes from tomorrows' premiums - very similar to the way NZ Super is funded (last years donors, dont invest, but are ponzi'd from next years pay-ins).

That is what allows them to grow a stable business with the surplus premiums collected. Not unlike how the TAB must pay out a percentage, but never all, of the betting pool.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.