Here's my Top 10 items from around the Internet over the last week or so. As always, we welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must reads are #8 and #9 on productivity. Seriously.

1. Our over-vallued exchange rate (still) - I'm enjoying former Reserve Bank economist Michael Reddell's regular and detailed blogging over at Croaking Cassandra.

I've got a feeling the Reserve Bank may not be enjoying it quite so much, but his blog posts are certainly providing a whole new level of insight into how the bank and the Government operates around economics.

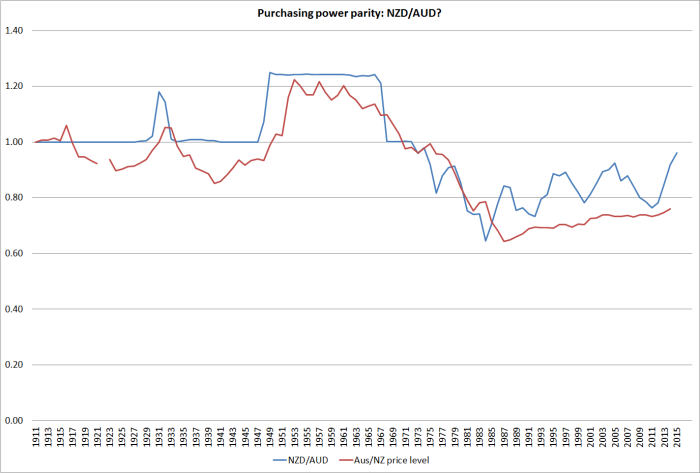

One of his latest (and there are many), is on the New Zealand dollar vs the Australian dollar.

He has compiled a set of very long term charts that are fascinating (note to self: get out more). The chart below is Michael's.

His conclusion is sobering and nuanced:

After spending years reflecting on the issues, I’m convinced there is nothing much wrong with New Zealand’s economy that a real exchange rate averaging 20-30 per cent lower for a few decades could not resolve. Perhaps issues around size, distance, and agglomeration mean we will never again be the richest country in the world, but we can do a great deal better than we have done in recent decades.

Views differ on why the real exchange rate might have been, on average, so strong over the last few decades. My story emphasises the high average real interest rates that have been needed to balance demand and supply (keep inflation near target) in New Zealand relative to those abroad. As just one example, the yield on a 20 year New Zealand government inflation-indexed bond has been around 2.2 per cent this month. The yield on 20 year US government inflation indexed bond has been around 0.7 per cent. Persistent differences in returns like that, which don’t appear to reflect differences in riskiness, have really big (and quite rational) implications for the exchange rate.

But, to be clear, this is not a monetary policy story. Long-term real interest rates reflect the pressures on real resources that result from government and private choices. They are real phenomena, not monetary ones.

Its marketing and many of its practices are based on the idea that consumerism is not sustainable and we need to buy less, not more. Yet it is growing sales at a double digit rate...

3. Ruth, Roger and Me – Over the weekend I was on one of those political talk show panels (TVNZ's Q+A) talking about the Budget, which is all good.

But I got a pleasant surprise when a feature of the show was an interview with Andrew Dean, a New Zealand academic who is currently a Rhodes Scholar and who has written a book about the experience of younger people now, 30 years on from the RuthoRogernomics era.

It was compelling viewing and the book is well worth a read. I'm part of the way through it now. Here's a taste of his thoughts, courtesy of Rob Stock at Fairfax:

Dean is 26, and stressed by an economy that just does not add up for any but a tiny proportion of 20-somethings. They have student loans to pay off. Houses are beyond their reach. They face low wages, high unemployment and a casualised labour market. And they believe that when they get old, there will be no such thing as NZ Super.

All the basic building blocks of a prosperous, stable money life have been stripped from them by the political policies of the generation that was the last to benefit from free education, cheap housing, standard work contracts, and the certainty of NZ Super.

But for all its social media savvy, the 20-somethings are a generation that does not seem to have a voice.

4. Almost doubled – Jing Daily has prepared a report on how much property Chinese are buying globally, and why:

According to the report, Chinese purchases of international real estate in the year to March 2014 equaled $22 billion, up from $12.4 billion the previous year. Within the United States, just under one in four dollars spent on international real estate is from a Chinese person. And the Chinese are making waves in quality, not just quantity.

The median home price for Chinese buyers is $523,148—more than double the median home price across the United States as a whole. Will this surge in international buying continue? All signs point to yes. Compared to prices in Beijing and Shanghai, half a million dollars doesn’t look that expensive to many of China’s more affluent buyers–particularly those interested in having their children educated abroad and diversifying their assets.

5. An Unconditional Basic income – In the wake of the skirmish over NZ Super and the problem/opportunity of universality, it's worth having a look at what Scott Santens writes about the UBI at Medium:

By guaranteeing everyone has at the very least, the minimum amount of voice with which to speak in the marketplace for basic goods and services, we can make sure that the basics needs of life — those specific and universally important to all goods and services like food and shelter — are being created and distributed more efficiently. It makes no sense to make sure 100% of the population gets exactly the same amount of bread.

Some may want more than others, and some may want less. It also doesn’t make sense to only make bread for 70% of the population, thinking that is the true demand for bread, when actually 80% of the population wants it, but 10% have zero means to voice their demand in the market. Bread makers would happily sell more bread and bread eaters would happily buy more bread. It’s a win-win to more accurately determine just the right amount. And that’s basic income. It’s a win-win for the market and those who comprise the market. It’s a way to improve on capitalism and even democracy, by making sure everyone has the minimum amount of voice.

Scott Santens has been thinking a lot about fish lately. Specifically, he’s been reflecting on the aphorism, “If you give a man a fish, he eats for a day. If you teach a man to fish, he eats for life.” What Santens wants to know is this: “If you build a robot to fish, do all men starve, or do all men eat?”

Santens is 37 years old, and he’s a leader in the basic income movement—a worldwide network of thousands of advocates (26,000 on Reddit alone) who believe that governments should provide every citizen with a monthly stipend big enough to cover life’s basic necessities. The idea of a basic income has been around for decades, and it once drew support from leaders as different as Martin Luther King Jr. and Richard Nixon.

But rather than waiting for governments to act, Santens has started crowdfunding his own basic income of $1,000 per month. He’s nearly halfway to his his goal. Santens, for his part, believes that job growth is no longer keeping pace with automation, and he sees a government-provided income as a viable remedy.

“It’s not just a matter of needing basic income in the future; we need it now,” says Santens, who lives in New Orleans. “People don’t see it, but we are already seeing the effects all around us, in the jobs and pay we take, the hours we accept, the extremes inequality is reaching, and in the loss of consumer spending power.”

7. There's too much debt! - So says Goldman Sachs (it would know) in this piece in The Telegraph:

Goldman Sachs worries about how ageing populations will ever repay the stuff. It worries too much. It needs to concentrate on selling and and buying more of the debt, then waiting for the inevitable bailout and money printing (followed by debt cancellation) to solve the problem.

There are fees to be made. Get on with it.

Anyway, here's Goldman wringing its hands. It's well worth a read:

Andrew Wilson, head of Europe, Middle East and Africa (EMEA), said growing debt piles around the world posed one of the biggest threats to the global economy.

"There is too much debt and this represents a risk to economies. Consequently, there is a clear need to generate growth to work that debt off but, as demographics change, new ways of thinking at a policy level are required to do this," he said.

8. But where's the productivity growth - I'm very interested in the 'Second Machine Age' argument that says a wave of computing power is about to break over the services sector of the economy to drive enormous productivity growth and wealth (although the jury is still out on jobs and wages).

However, this big FT piece on the lack of productivity growth in recent years suggest that thesis isn't working out, or at least isn't being measured in the GDP figures. Or is about to happen. A great read.

New data from the Conference Board think-tank show that average labour productivity growth in mature economies slowed to 0.6 per cent in 2014 from 0.8 per cent in 2013, as a result of ebbing performances in the US, Japan and Europe. Productivity, which tracks how efficiently inputs such as labour and capital are used, tends to evolve over long periods. But the Conference Board readings confirm a longer-term trend of sagging growth that is setting off alarm bells around the world.

Marco Annunziata, the chief economist at General Electric, worries there is a structural problem in Europe due to a lack of risk-taking, low R&D spending and inflexible labour markets.

In the US, the most efficient of the major economies, productivity growth began to ebb in 2005. According to Mr Fernald, this was a result of the lapsing of temporary growth dividends from the 1990s IT revolution.

This raises the possibility that the recent, dreary productivity growth in the US is actually a return to an older and weaker trend. Even in emerging economies, where efficiency is catching up, the rate of growth has slowed.

9. Where's the productivity growth redux - Paul Krugman is also asking where the productivity growth went.

Everyone knows that we live in an era of incredibly rapid technological change, which is changing everything. But what if what everyone knows is wrong? And I’m not being wildly contrarian here. A growing number of economists, looking at the data on productivity and incomes, are wondering if the technological revolution has been greatly overhyped — and some technologists share their concern.

We’ve been here before. “The Hitchhiker’s Guide” was published during the era of the “productivity paradox,” a two-decade-long period during which technology seemed to be advancing rapidly — personal computing, cellphones, local area networks and the early stages of the Internet — yet economic growth was sluggish and incomes stagnant. Many hypotheses were advanced to explain that paradox, with the most popular probably being that inventing a technology and learning to use it effectively aren’t the same thing. Give it time, said economic historians, and computers will eventually deliver the goods (and services).

This optimism seemed vindicated when productivity growth finally took off circa 1995. Progress was back — and so was America, which seemed to be at the cutting edge of the revolution.

But a funny thing happened on the way to the techno-revolution. We did not, it turned out, get a sustained return to rapid economic progress. Instead, it was more of a one-time spurt, which sputtered out around a decade ago. Since then, we’ve been living in an era of iPhones and iPads and iDontKnows, but even if you adjust for the effects of financial crisis, growth and trends in income have reverted to the sluggishness that characterized the 1970s and 1980s.

10. Totally John Oliver covering the end of the world as we know it (not the REM song)

28 Comments

#3 - And then he quickly dismissed any idea of going in to politics himself. Pity. Academia needs to get in the game if there is ever going to be a game-changer. Elizabeth Warren is proving that in the US.

Couldn't agree more. Also: more power handed back to local government, we need to go back to smaller communities, and smaller economies. Maybe then this 'voiceless' generation will get involved again...they can't stay on the fringes forever...

.

Still annoys me when the BBs do the chest beating spiel of "but we had it so hard in our day". gggrrrrr.

.

The power you refer comes from ownership, which is being progressively removed from new zealanders. We have to turn that tide.

A great top 10 Mr Hickey.. some great articles there

"There is too much debt and this represents a risk to economies. Consequently, there is a clear need to generate growth to work that debt"

finite planet meet exponential growth....oopsie.

Debt has nothing to do with the planet.

Debt/credit is a man made fiction.

Debt/credit is created to bring growth forward.

The key thing is that debt/credit is a belief system a fiction in the minds who believe it.

The way I personally look at debt is that I would borrow to expand my business. But I would never borrow money to buy a new car or take a holiday. If i can't afford something that's a luxury i won't buy it. So what I'm saying is it's not debt that's the problem it how we are investing our money. Alot of us are borrowing against the value of our growing asset values to buy a new car (because the banks will let us do it) but have no growth in income. Does the later type of borrowing help growth? We need real wage growth not asset value growth created by easy credit allowing you to borrow more. That's just a debt ponzi.

Tim, boil what you are saying down to basics and hopefully that will provide greater clarity. It isn't the borrowing that causes the problem, it is the interest that causes the demand for exponential growth. When you borrow, you are borrowing previous production (think food), pay interest then you have to pay back that food, and then some. ie: you have to grow more food than you did last year. Lets say you have 100 acres in wheat, do you think you can increase the yield on your 100 acres in perpetuity?

Tim12 it is all very dependent upon the fox in the hen house....you can have identical assets with identical debts....but because they're structured differently two very different outcomes.

if we invest in assets that don't have income growth but are growing in value ( eg capital gain on a booming housing market) then surely this isn't the type of investment the world needs. We need to invest in assets with income growth ( businesses that create sustainable income and jobs). i.e investment where there is potential profit not speculative gain (gambling?) If that asset isn't backed by income is it's value is subjective (like gold). Are assets like property in big cities booming because people see them as a tangible store of wealth at a time where money printing could potentiallly erode the value of currencies? Are there the first signs of cracks in globilization. England having a referendum on belonging to the EU. and tensions between US and China in the South China Sea.

when you say invest, does that include buy with credit?

let people do what they want with their own funds

taking credit that seems underwritten by the rest of us,

where is the fun in that/lets see how this pans out...

ro.

Yes, but clearly the finance sector has effectively become our masters and their own wish is short term gain at our expense.

Really we need to take back control.

"Debt/credit is created to bring growth forward" by "growth" I assume you mean consumption, which of course is related to the planet. We can only consume things made from our environment. If you don't mean consumption could you please expand on what you mean by growth.

"Debt has nothing to do with the planet" This seems to contradict your comment about bringing forward growth.

I could simply be missing the point you are trying to make so if you could expand on your ideas it would be much appreciated.

"Long-term real interest rates reflect the pressures on real resources that result from government and private choices."

Would Bernard or other economist be able to point to possible choices that could be taken to change pressures on real resources?

possible choices and permutations

Do you really want to know?

I wrote this back on 14 Feb 2011

http://www.interest.co.nz/opinion/52249/opinion-drain-dragged-down-debt…

Then read BNZ's Senior economist Tony Alexander's Sporadic bulletin 8 of 12 May 2015

http://tonyalexander.co.nz/wp-content/uploads/2015/05/Sporadic-8-May-12…

Even he doesn't know and posits only 8 possible components with a myriad of permutations

Interesting as far as it goes, but is it this what was meant by "Real Resources" in the original article I wonder?

What can be said is, if you listed some of the options you think viable, no one can tell you what the final outcomes will be, and certainly "cannot guarantee" the steps taken will have the desired effect on your intended targets

Who is this Andrew Dean anyway? Bill English has talked to allot of young people and none of them are worried about superannuation. Get with the program.

Bernard produces the best, most interesting and most insightful Top 10's.

#3 Ruth, Roger and Me. Could this be the process of the effects of capitalism, and the free market economy proving that just like the left wing models, they fundamentally do not work? Some level of control is required to limit plutocracies, and oligarchies and remind corporates that they serve, and exist within societies and without the people in those societies they would not, could not exist. Democracies are about people power, not the power of politicians, banks or money.

Yep, haven't heard any Cabinet member or the PM use the phrase, "for the common good", not once in the seven years.

It is gratifying to see an apparently reputable NZ economist such as Reddell explain the long term effects of an overvalued exchange rate, and that the NZD is still overvalued. I had thought NZ economists, perhaps for political reasons, remained in denial on this point. Does he have a view, do we know, whether the Reserve Bank could be more active in encouraging the exchange rate down, other than occasionally attempting to talk it down?

I do have a view. The short answer is "no", The slightly longer version is here. http://croakingcassandra.com/2015/05/28/what-can-the-reserve-bank-do-ab…

Cheers Michael for getting involved. Nice link.

Bernard

Yes indeed. We are certainly getting more than our money's worth reading his OIA stoush with the RBNZ. The later's reaction is revealing in so much as it has in common with the tenets of fascist diktats than that reserved for an open democracy.

Yes, thank you for responding. I'm happy to retract a throwaway implication that most/all NZ economists are somehow in denial about the exchange rate and its effects, even if in my view they do not give it the importance I might do.

Am largely willing to defer to your short answer "no" as presumably that is coventional wisdom for at least some reason.

However I think there is a debate to be had on the cause and effect relationship between the exchange rate on the one hand, and consumption, investment and saving at a national level on the other. The Singaporean approach to monetary and fiscal policies always impresses me; where they have considerable focus on their current account. Given they are resource poor, they have been spectacularly successful. Given their strong Chinese links, if they had NZ's policy settings, they would long ago have had most assets swallowed up by Chinese entities, and through that process an overvalued exchange rate, and a massive current account deficit. But their outcomes have been the opposite. Is that a cultural preference for saving, or a result of policy settings? I would argue the latter. They are small and have a population of 5.5 million. Not a bad model of economic management in my view.

of course, recall that Singapore did have massive current account deficits for a long time when they were growing very rapidly. The high net savings followed their successes rather than initiated them.

Happy to treat Singapore more fully on my blog at some stage. It is intriguing and challenging - and authoritarian! Can't say I'd want to live their and I've heard sensible well-informed Singaporeans arguing that ordinary NZers still have a higher standard of living than ordinary Singaporeans.

Hmmmm - can't say I would like to live in the US.

Five years after the recession ended, many Americans still teeter on the financial brink, barely prepared to handle an emergency expense and aging toward retirements they haven’t saved for, a Federal Reserve report shows.

About 47 percent of 5,896 respondents in the Fed’s 2014 household survey, taken last October and November, wouldn’t be able to cover an emergency $400 expense without selling something or borrowing money. While that marks an improvement from 52 percent last year, the report states that it shows many Americans to be “ill-prepared for a financial disruption.” Read more

One could lay the blame on a strong dollar, but certainly not a high level of interest rates.

Michael,

Have just also read your paper on the last OCR non reduction, (in a link from the link above) and was impressed. Some of us have been making similar points here for a while, but not as well articulated, nor with the ex Reserve Banker gravitas. So all good, well done.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.