Today's Top 10 is a guest post from Ryan Greenaway-McGrevy who is a senior lecturer at the University of Auckland. Prior to this he was a research economist in the Office of the Chief Statistician at the Bureau of Economic Analysis (BEA) in Washington DC.

In this week’s Top 10 he looks at China. The recent mini-meltdown in the Shanghai stockmarket is a timely reminder that 30% of our exports go to an economy that often escapes the headlines. But what do we know about the state of the Chinese economy? Chinese economic data is notoriously unreliable. This week’s Top 10 gives us a summary of some of the signals we are receiving.

As always, we welcome your additions in the comment stream below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

1. What is the Government doing to prop up stock prices?

Heather Timmons and Lily Kuo over at Quartz give us a timeline of the interventions that we know of:

Here’s a complete list of the stimulus attempts that have been made public over the past week or so:

June 27: A surprise 25 basis point interest rate cut and lowering of the reserves banks need to keep when they lend to companies.

June 29: Regulators say pension funds can invest 30% of their net assets (equivalent to more than $100 billion) in equities for the first time.

July 1: China’s securities regulator relaxes rules on margin financing, or trading stocks with borrowed money.

July 3: China’s central bank extends a 250 billion RMB ($40 billion), six-month loan to state owned banks to “encourage banks to increase support” to weak parts of the economy.

July 4: 21 brokerages, led by Citic Securities, say they will invest $19.3 billion in a new blue-chip fund to stabilize the market, and vow not to sell any of their own proprietary equity holdings.

July 5: 28 firms planning IPOs on the Shanghai and Shenzhen market say they will postpone them and start refunding investors’ capital.

July 5: China’s central bank says it will inject an undisclosed amount of capital into China Securities Finance Corp (CSF)., a state-owned company that makes margin loans to brokers.

July 6: Executives from mutual funds pledge to support the markets with their own capital.

July 8: Regulators banned company shareholders with stakes of more than 5% from selling for the next six months. China’s central bank said it would further support the margin lending provider CSF through interbank lending, bond issuance, and collateral backed financing and re-lending. China’s securities regulator also said it would increase purchases of small-cap stocks.

July 9: China’s banking regulator, the CBRC, said banks can now loan money to companies using stock as collateral, and ease margin requirements for wealth management customers.

Much of this reads as if the Government is doubling-down on stock prices soaring. In other words, they are trying to fuel a bubble, not slowly deflate it. That last intervention has the potential to be particularly damaging. Let’s take a closer look at it.

2. The Chinese Banking regulator has permitted banks to loan money to companies using their stock as collateral.

This is really is dysfunctional banking. Sigrún Davíðsdóttir over at a Fistful of Euros looks at how this worked out for the Iceland banking sector. Here is my favourite quote:

Asking a foreign banker in London if this was a general practice that banks lent clients to buy the bank’s share with the bank’s own shares as the only collateral he said he knew of this Icelandic practice: “It’s so insane that I don’t even know if it’s legal or not. No bankers in their right mind would consider it.”

You see, I was pulling my punches when I called it “dysfunctional”. This form of collateral can quickly lead to prices spiraling downwards. Sigrún Davíðsdóttir talks us through what happened in Iceland:

Apart from weakening the banks’ equity the lending against own shares turned into a major headache for the Icelandic banks already in 2007 with the drying up of credit markets. The share price of the banks started falling, forcing the banks to make margin calls.

Under normal circumstances the banks would have taken the shares, liquidated them and pocketed the money to cover the losses. But by accepting own shares as collateral the banks had created anything but normal circumstances.

These circumstances were further aggravated with cross-ownership and close connections between holding companies and the banks. Thus, the collateralised shares, banking shares or not, created a highly poisonous circumstances where the banks could not follow normal business practices: by liquidating the shares the price would have fallen further – this really was a spiral straight to hell.

So what do you do when prices begin the downward spiral? Reuters reports that many of the Chinese companies that have had had their stocks suspended from trading borrowed using their own shares as collateral.

3. Why is the Government so concerned about the stock market coming back down?

After all, the recent 30% drop occurred after an increase of 150% over the previous year. Evan Osnos at the New Yorker suggests that the regime has to keep the prices high because it urged the public to buy, and keep buying:

On April 21st, People’s Daily, the newspaper that the Chinese Communist Party calls its “throat and tongue,” published an online commentary exhorting the masses to place their trust, and savings, in the stock market. Even though share prices had soared by more than eighty per cent in less than four months, this was “merely the start of a bull market,” since blue-chip stocks remained “undervalued,” the author, Wang Ruoyu, explained. Like a CNBC stock picker, Wang mocked fears of a bubble—“What’s a bubble? Tulips and Bitcoins are bubbles”—and assured readers that continued gains would enjoy the full “support from China’s grand development strategy and economic reforms.”

So this is about the credibility of the regime. This is appears to be an old habit:

The public had reason to believe. Official and quasi-official Chinese pronouncements carry the ring of prophesy. In the heyday of socialism, the Party forecasted the size of the following year’s harvests and the quantity of steel production, and the final numbers were rarely permitted to deviate much from the predictions. More recently, the Party has offered annual targets for economic growth that almost always bear out, no matter what sort of creative policy, or accounting, steps are required.

After the exhortation to buy more stocks, apparently the graphic below started doing the rounds within China’s online community.

"ChineseBullMarket" by http://roll.sohu.com/20150423/n411770788.shtml. Licensed under Fair use via Wikipedia - https://en.wikipedia.org/wiki/File:ChineseBullMarket.jpg#/media/File:ChineseBullMarket.jpg

{kind=link}

4. Debt at the provincial level ballooned to crisis levels in 2015.

The Ministry of Finance and the Bank of China reacted by having state-controlled banks purchase the debt under very unfavorable terms. This is a default by another name. Christopher Balding comments:

Let’s run a simple thought experiment. Assume a government is drowning in debt. They can’t raise the money to pay off the debt coming due. The interest rates are too high and the maturities too short. Revenues are falling and the banks are reluctant to continue extending credit to the government. The situation looks dim.

The government and central bank, however, come up with an idea to solve the problem. The government imposes a debt swap on the banks where they unilaterally turn short term high interest debt into low interest long term debt. Though there is no write down in the face value of the debt, there would be a reasonable case given the coercion and change of terms, to ask whether this was a debt default. There has been no change in asset or borrower quality but rather a unilateral rewriting of the debt contract using coercion. Not wanting to miss out, the central bank offers to accept this troubled debt as collateral should the banks want cash instead, effectively monetizing the bad debt.

This scenario isn’t about Greece but about the debt swap imposed by the Chinese government in partnership with the PBOC on lenders holding local government debt. While no one is saying this is a default, if this same scenario played out in Greece, there would be arguments over whether this constituted a default.

But it seems the bailout was not enough to help local government. Here is Balding again:

Friday night the Chinese central government through the Ministry of Finance, along with the PBOC and CBRC, jointly announced a policy intended to further aid local governments. In the words of the Financial Times, the regulation:

“…told financial institutions to keep lending to local government projects even if borrowers are unable to make principal or interest payments on existing loans….(the regulation)explicitly banned financial institutions from cutting off or delaying funding to any local government projects started before the end of last year and said that any projects that are unable to repay existing loans should have their debt renegotiated and extended.”

Let me say that again just so it sinks in: banks were told to keep lending money even if the borrowers are unable to make principal or interest payments on existing loans and banks are forbidden from cutting, denying, or delaying loans. While country policy makers around the world have unofficially encouraged excessively loose credit policies and lenders may take such policies in individual cases, I have never heard of a similar countrywide or bank wide policy anywhere. (If anyone knows of a comparable case please let me know).

5. Despite capital controls, capital is leaking out of China.

What do you do when the Government won’t let you buy US dollars to invest overseas, but it will let you buy US dollars in order to purchase goods and raw materials?

Import and export over or under invoicing is another means of disguising flow in the restricted sector to look like flow in the unrestricted sector to move capital between countries. A sample transaction turns a $5m export into $10m to move $5m in capital into China. First, the exporting company issues a $10m invoice, declares $10 export to customs, and ship goods to importing company in another country. Second, the importing company declare $5 of import to customs, pays $5 for the good which is the real value of the goods trade. Third, the capital inflow of $5m will be remitted together with the payment for goods received of $5m, and be accepted by the Chinese company as $10m.

While some capital is also flowing in to the country, it appears that much more is flowing out. How can we tell? Balding again:

The easiest way to know this is happening is to compare official Chinese import and export data to the import and export data of its trade partners. In other words, if China declares $10m in exports to Australia but Australia only reports $5m in imports from China, we consider that a significant discrepancy. Differences are to be expected in trade data but they are typically and should be quite small.

But how much is flowing out?

From 2012-2014 the total export over invoicing discrepancy between China and its top five trade partners was approximately $40billion USD. While that may sound like a lot, give the enormous amount of trade with the top five partners over three years, this is little more than a rounding error averaging about $13b a year. However, import over invoicing, which moves capital out of China, has grown rapidly in the past few years. From 2012 to 2014, the import over invoiced discrepancy amounted to $525 billion rising every year from a low of $148 billion in 2012. Import over invoicing for the top five trade partners of China represents approximately 30% of the value of imports.

So the net outflow of capital is accelerating. It is concerning if Chinese investors increasingly feel their money is better invested overseas. It certainly is not a vote of confidence.

Nor is the outflow economically insignificant: China’s trade surplus for 2014 was $382 billion. Because economists often rely on official trade statistics to estimate Chinese foreign investment, import over-invoicing suggest that these estimates will significantly understate the true amount of Chinese-owned capital sloshing through global asset markets.

But there is perhaps a silver lining: If official net exports are understated, then official GDP is understated.

While these net figures suggest that import over-invoicing is more prevalent than export over-invoicing, the latter is also occurring ...

6. Despite capital controls, capital is leaking into China.

The Shanghai Interbank Rate (SHIBOR) is much higher than US, European or Japanese interest rates. If there were no capital restrictions, money would be flowing in, much like it does to New Zealand to take advantage of our high interest rates.

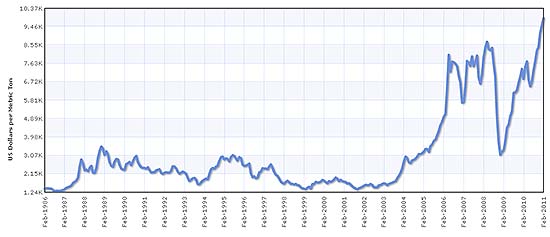

Again, fake invoicing is being used to get around this. The paper by Christopher Balding (you guessed it) and Zhang Xiao outlines how cooper reserves sitting in warehouses are used for this purpose. Balding explains how it works:

To move capital but disguise the FX transaction as trade rather than capital movement, firms have found an enterprising way around this. A firm will enter into a sham transaction to export, for use in our paper copper, a product with a clear market price. The firm will then secure foreign currency trade financing, typically in a currency fixed against the RMB like the USD or HKD with low borrowing rates and potentially additional leverage, convert back into RMB and bring the currency back into the country under the guise of goods trade. They will then invest in typically high credit quality short term products and then unwind the trade and the end of the term for the copper holding.

But is this economically significant? It appears so.

Given that by our official estimates, China now holds nearly 40% of the global copper stock in warehouses, which excludes ongoing consumption, this is not an insignificant finding. It is also worth noting that some estimates, have Chinese copper stock responsible for an even higher share of global copper stock holdings.

And here is the Financial Times reporting:

Some Chinese executives estimate that as much as 70 per cent of China’s imports of refined copper were used to obtain financing rather than for consumption.

Balding and Zhang don’t tell us how this may be distorting world copper prices. The global price may have been inflated not because it is being put to good use in building infrastructure, but because Chinese firms need a way to get around the controls.

Copper Price per metric Ton.

Graphic Citiation: "Copper Price History USD" by BonerUploaded by Gonzonator at en.wikipedia - Transferred from en.wikipedia by SreeBotOriginal caption: “Data extracted from http://www.lme.co.uk”. Licensed under Public Domain via Wikimedia Commons - https://commons.wikimedia.org/wiki/File:Copper_Price_History_USD.png#/m…

{kind=link}

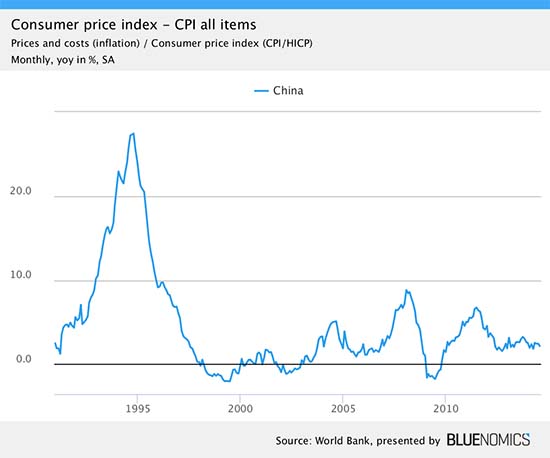

7. Real GDP is almost certainly not growing at 7%, as the official figures indicate.

But you knew that already, and so do the Chinese leaders.

But, how much lower is the real growth rate? Official statistics put nominal growth at 5%, meaning that there is deflation in China, which is not a good sign if you are looking for robust growth. Corporate profits are flat, despite that fact that some companies have been profiting from the stock market boom. Official reports of electricity consumption growth are flat. It is ultimately impossible to tell, but I would guess that it is much below 7%.

Which naturally leads one to consider what the true level of real (i.e. inflation-adjusted) GDP is China may be. Based on discrepancies between different measures of inflation, Christopher Balding puts it at $1 trillion (in purchasing power parity terms), which equates to a reduction of 8-12%.

Official Inflation in China

"China inflation" by Abluher - Own work. Licensed under CC BY-SA 4.0 via Wikimedia Commons - https://commons.wikimedia.org/wiki/File:China_inflation.png#/media/File:China_inflation.png

{kind=link}

8. A huge chunk of labour force is employed in the construction industry.

The IMF reckons 14% of the urban workforce is in construction, while property investment accounts for between 12.5% and 20% of output growth. Or perhaps that should be accounted for between 12.5% and 20% of growth, as these estimates are a year old. Construction is a notoriously volatile sector in any economy.

Gywnn Guilford at Quartz has more:

The beauty of any housing boom is that it needs lots of workers to build it. That employment fillip has served China’s leaders well. After the 2008 financial crisis threatened mass layoffs, they pushed banks to lend to property developers and infrastructure. It worked; by 2011, construction was creating more than half of new migrant worker jobs, according to Capital Economics.

That’s also part of why, even as China’s GDP growth slowed from 14.2% in 2007 to 7.5% last year, employment opportunities abound.

Given that the Chinese property market bubble has burst, one wonders how the huge amount of labour has or will be reallocated. Unfortunately, but perhaps not unsurprisingly, official unemployment data in China offers little insight.

9. Meanwhile, the Government has been cracking down on perceived dissent from its citizens.

Until recently, China’s online community was a vibrant agent of change, and change for the better. Read this excerpt about how an internet campaign lead to the trial of a corrupt official.

It started with a smile. In the summer of 2012 a Chinese government official was pictured grinning at the scene of a bus crash in Shaanxi Province. Web users, annoyed by his cheerful demeanour at the scene of a tragedy, began trawling through other images of the official and found something that many found unsettling. In picture after picture, people noticed that the civil servant was wearing a string of luxury watches, and people demanded to know how he could afford them on his modest salary. The outcry led to a jail sentence for the official, and kick-started a wave of similar scandals, many of which came to light on the Sina Weibo social network.

But perhaps the online campaigners were too successful. The Government has since cracked down on dissent:

The downward trend may have been helped by a law introduced in 2013 to prevent "rumours" spreading online. It means those posting allegations to Sina Weibo risk being jailed for up to three years if their messages are shared more than 500 times. Rather than leading to a raft of convictions, the effect of the law has been to encourage self censorship, says Tommy Wen, a journalist and blogger based in Beijing.

It appears that the crackdown has affected one of the most vocal critics of the regime: Han Han. If you haven’t heard of Han Han, you’re probably not Chinese. You should know of him. He spoke truth to power. His scathing, angst-ridden critique of modern China Triple Door was a best seller.

Is the crackdown a signal? Does it tell us that things are in far worse state than the leadership is letting on?

Han Han. Photo credit: laihiuyeung ryanne from hong kong derivative work: Stevenliuyi (talk) - Han_Han_at_Hong_Kong_Book_Fair_3.jpg

{kind=link}

10. You can’t understand the economy of China without understanding the geopolitics of China.

Despite being written over three years ago, George Friedman’s account of the Chinese regime’s political strategy is timeless. Friedman believes the maintenance of domestic stability has always been the priority of successive Chinese regimes. The current government is no different. But it is achieving stability be a different means:

The current government has sought a more wealth-friendly means of achieving stability: buying popular loyalty with mass employment. Plans for industrial expansion are implemented with little thought to markets or margins; instead, maximum employment is the driving goal.

As we have seen, the Chinese government certainly appears to prop all markets in order to maintain stability – whether it be stock markets or labour markets. Indeed, it appears that stability is paramount, and this drives much of the ongoing state intervention that we observe. Let’s hope that the Government can keep China prosperous and stable.

27 Comments

So what's the real threat here? China runs out of Yuan?

#2 isnt it common practice for supply dairy farmers to seek and get 100% bank finance for their mandatory Fonterra milk shares? Stand to be corrected.

back when the dividend could cover the cost of finance, since TAF banks then applied their own lending value to shares as part of the deal (usually $5+) but certainly above todays $4.63

maintain stability...

you mean china wmp buyers will pay more for local production (having been told to) in order to maintain stability (Xmas 14 pictures of china farmers spilling milk being the straw)

as credit suisse say China's dairy consumption volume declined 1% YoY in 2014

- H1 & H2 2015 may be no different [we're thinking].

That has been the primary problem with economists and the rest of the population, as the economy that exists in the statistics often bears only passing resemblance to what the rest of America (and the world) finds for itself. Without all the asset inflation, the monetary attempt to rule by “rational expectations”, a great deal of the divergence disappears. In other words, without the asset bubbles the economy begins to look very much like it has been in extended difficulty for more than just this “cycle.” Read more

Great information here. Thanks for the work. Aren't we fortunate to live in a society where information like this is shared and we can comment freely.

Just this morning, as it happens, we have an email from Amnesty International about a recent government crack-down in China targeting over 200 lawyers and their clients (at least of 24 of whom are still missing or detained). Yet this is the set-up with which New Zealand now has a 'Comprehensive Strategic Partnership'.

And what is the political and economic imperative for New Zealand in this relationship? At bottom, to flog them dairy products, no matter the destruction to our environment or the stupidity in seeing this as sustainable. And no matter now, that Chinese money - flooding here through residents as much or more than non-residents - is making vast areas of our largest city unaffordable to ordinary New Zealand wages and salaries.

Jenny Shipley, Don Brash and those others who have accepted window-dressing roles with Chinese banks should hang their heads in shame.

"Jenny Shipley, Don Brash and those others who have accepted window-dressing roles with Chinese banks should hang their heads in shame."

Yes for sure, but don't count on it.

Read this on the net today...Interesting and revealing.

Quote :

Being Chinese

by Chan-Lui Lee, Ph.D.

Honorary Life Member & Past President, AFS-Melbourne, Australia

Why do Chinese people work so hard to succeed in life? Chinese people do not go about bombing, terrorizing others and causing religious hatred. We live peacefully with everyone on Earth.

Here is the plain truth about being Chinese.

#1. There are over 1 billion of us on Earth. We are like photostat copies of each other. You get rid of one, and five magically appear (like ballot boxes). Yes, it is scary, especially for us. We acknowledge that we are replaceable, thus we do not feel that we are particularly 'special'. [Chinese believe that] if you think you are smart, there are thousands more people smarter than you. If you think you are strong, there are thousands more people stronger than you.

#2. We have been crawling all over the Earth for far more centuries than most civilizations. Our DNA is designed for survival. We are like cockroaches. Put us anywhere on Earth and we will make a colony and thrive. We survive on anything around us and make the best of it. Some keep migrating but others will stay and multiply.

#3. NOBODY cares if we succeed as individuals or not. But our families take pride in knowing we have succeeded. Yes, some will fail. We take nothing for granted. We don't expect privileges to fall on our laps. No one owes us anything.

#4. We know we have nothing to lose if we try to succeed. Thus, we have no fear trying. That is why Chinese are addicted to gambling. We thrive on taking risks. All or nothing.

#5. From young we are taught to count every cent. What we take for granted like money management, I have found out recently, is not something other cultures practice at home with their children. It surprised me. But truth is not all societies or cultures teach their young this set of skills because it is rude to them. Yes, most of us can count because we are forced to and the logic of money is pounded into us from the beginning of time (when mama tells us how much she has spent on our milk and diapers).

#6. We acknowledge life cycles. We accept that wealth in a family stays for three generations (urban myth?). Thus, every 4th generation will have to work from scratch. i.e. first generation earns the money from scratch, second generation spends the money on education, third generation gets spoiled and wastes all the inheritance. Then we are back to square one. Some families hang on to their wealth a little longer than most.

#7. It is our culture to push our next generation to do better than the last. Be smarter. Be stronger. Be faster. Be more righteous. Be more pious. Be more innovative. Be more creative. Be richer. Be everything that you can be in this lifetime.

#8. Our society judges us by our achievements...and we have no choice but to do something worthwhile because Chinese New Year comes around every year and Chinese relatives have no qualms about asking you straight in your face...How much are you making? When was your last promotion? How big is your office? What car do you drive? Where do you stay? You have boyfriend? You have girlfriend? When are you getting married? When are you having children? When is the next child? When you getting a boy? Got maid yet? Does your company send you overseas?... etc...etc... etc. It never ends! So, we can't stop chasing the illusive train -- we are damned to a materialistic society. If you are not Chinese, consider yourself lucky!

#9. We have been taught from young that if you have two hands, two feet, two eyes, and a mouth, what are you doing with it? "People with no hands can do better than you !"

#10. Ironically, the Chinese also believe in giving back to save their wretched materialistic souls. Balance is needed. The more their children succeed in life, the more our parents will give back to society as gratitude for the good fortune bestowed on their children. Yes, that is true. And that is why our society progresses forward in all conditions.

Nobody pities us. We accept that.

No one owes us anything. We know that.

There are too many of us for charity to reach all of us. We acknowledge that.

But that does not stop us from making a better life. This lifetime.

Opportunity is as we make of it. So, pardon us if we feel obliged to make a better place for ourselves in any country we call home. It is in our DNA to progress forward for a more comfortable life.

But if history were to be our teacher, look around the globe.

Every country has a Chinatown (seriously) but how many governments or countries have been 'taken over' by the Chinese people? Don't be afraid of us overwhelming your majority, we are not looking to conquer. If we have moved away from China and Chinese governed countries, we are not looking for another country to administer. Our representatives are only there to look after our collective welfare. They are duty bound.

We prefer to blend in and enjoy the fruits of our labor. We enjoy the company of like-minded people of all races. After all, we are only passing through a small period in the history of time... so, use our skills and we can all progress forward together.

Reads like the manifesto of any other culture. Nothing unique really.

Yeah right.

Then, the Chinese culture gets singled out every time.

But that does not stop us from making a better life

Not sure that is correct - it should read

That does not stop us from "seeking" a better life somewhere else and taking over

They've sure done a great job of Beijing, and now that it is classified as an oversized "chinatown" and it's stuffed, so lets go and replicate the same somewhere else where we won't have to wear smog masks - for a little while anyway until it is also too polluted and over-crowded

Mr Lee Ph.D says - We live peacefully with everyone on Earth

Tibet? Uighars? Falun Gong?

Tiananmen Square?

I see Chinese authorities have an issue with Taylor Swift's new album 1989 with her initital TS. You know there has to be a real issue with that.

With respect SmoKey, people everywhere feel like this. You could substitute Italians, Greeks, a host of other cultures, for Chinese in this text with only minor adjustment and it would read as well as it does now.

Nobody except a racist moron has any gripe with someone for being Chinese or any other nationality or ethnic group. (Though other ethnic groups, as pointed out elsewhere here, fare pretty poorly under the Chinese state.)

The problems are with the vastly unequal relationship New Zealand has in its 'Partnership' with China. This inequality is plain in the container loads of unaccountably acquired money being shipped here, piloted by residents as well as non-residents, and distorting the housing market (perhaps other markets too) to the inarguable detriment of those who do not have millions in ready cash are thus unable to own homes in Auckland.

Put simply, where are the primary school teachers, the nurses, the policemen and women, the butcher, the baker, etc, going to live? For many people, a good part of the New Zealand way of life, involving independence and security in one's own home, goes out the window.

Just another piece of ethnic profiling. One man stakes his claim to speak for the character of one billion others, based only on something as superficial as a shared ethnicity. Utter rubbish, and ethically repugnant.

Try to see the character of people. Don't be lazy and rely of ethnic or other stereotypes.

Best Top 10 @ 10 in a very long time, well done.

When China finally blows up it will be interesting to see how much of NZ it takes with it. If you are not factoring it in (at least to some degree) you are not paying attention.

Speaking of which - the Chinese Markit Manufacturing PMI just missed by a mile, at 48.2.

Never could understand how the Markit reading has been saying Chinese manufacturing is contracting for a while yet they still claim 7% GDP growth. Does. Not. Compute.

"A Chinese restaurant in the Kenyan capital does not admit Africans after 5pm..." Coming to a place near us?

There's' disquiet on many front, across the Globe as 'free money' looks for an asset realised home.

http://www.rt.com/news/243273-kenya-bar-africans-restaurant/

To be honest I don't have a problem with the Chinese coming here to invest and live a better life ,it's just that it's always Auckland ,where unfortunately is where all the work is ,

It leaves young people with student debt competing against wealthy foreigners , now if the people coming in chose other towns or if the places of work chose other towns it might work

Invest in what? I for one do not think that any immigrant who thinks investing in housing, becoming a landlord is something this country wants or needs, it is not, we have plenty of that here already

Good top ten

Very good list of articles, thanks.

China has some distinct differences to Iceland, such that it seems likely to me their government can and is likely to keep printing money to solve a number of their issues. They still have a very significant current account surplus, meaning their currency will not collapse, even with extensive printing. Many of their commercial banks, as I understand it, remain under direct government ownership, or under the ownership of party officials. The central bank can always arbitrage away the commercial banks bad debts if it wishes to, with little pain to the government. The fact US$500 billion (and probably a lot more) of this printing has leaked offshore in foreign investments by Chinese is not really a core problem of their government. Apart from catching a few of the most patently corrupt people, their government is unlikely to threaten the domestic money flows necessary for their economy to stop this foreign investment happening. Why would they? Propping up local governments is similarly relatively painless, especially if it is helping build moderately useful infrastructure. That some of this money will be enriching the contractors and leaking off shore in a valid manner; or some local officials are siphoning some to themselves and getting that offshore, may be distasteful, but more of other countries' problem than China's.

Transitioning their workforce from construction into other industries will be harder, but manageable over time you would think.

Their copper mountain is interesting; I assume similar financing mechanisms have explained the reputed milk mountains, and iron ore and coal mountains. It might be best for the world if in fact some of these mountains don't exist in practice, otherwise consuming through them will be both a challenge and very price distortionary. If they are not real, there would then be massive debts to write off presumably, but again the central bank can print them away. Moral hazard everywhere, but I suspect the rest of the world may end up being the fall guys.

Echo KotW: best top 10 for some time.

#10 - George Friedman (StratFor) is always, always worth listening to. His most recent book (Flashpoints http://www.amazon.com/Flashpoints-Emerging-Crisis-George-Friedman/dp/03… ) nails what's stirring in Europe again from the perspective of an insider. It ain't gonna be pretty, especially now that MENA is embroiled in what Spengler characterises as its 'Thirty-Year War', right on the doorstep http://www.atimes.com/atimes/Middle_East/MID-01-120814.html. But then again, he regards America's mis-steps as a comedy of errors...http://www.atimes.com/atimes/China/CHIN-02-101114.html. And Asia will, in his opinion, carry on the mantle of western Civilisation...http://www.atimes.com/atimes/World/WOR-01-300614.html

For much, much more about the Greater Asia Sphere now emerging via a network of Silk Roads, read Pepe Escobar's excellent summary here: http://www.tomdispatch.com/blog/176026/

The subtitle almost says it all: The Eurasian Big Bang: How China and Russia Are Running Rings Around Washington

and yet how does a piece like this fit into the narrative?

Building relationships with China is important and this week I hosted a lunch with a very powerful source, Mr Sun Shoushan, a senior member of the Chinese administration as well as the Communist Party. Malcolm Turnbull would reel at the power Mr Sun has. He's effectively the boss of all state-owned media, including publishing, press, television, radio and film. It was an honour to have Mr Sun join me with a number of colleagues from the Dentsu Aegis Network advertising company, the company to which I sold my advertising interest.

Mr Sun had a very clear message: the Chinese economy will continue to have sustained growth. It's GDP per capita has more than doubled in the past seven years with annual growth rates of around 9 per cent and 10 per cent. Net savings per household is 40 per cent and is proof the Chinese are thrifty and disciplined people. As a percentage of GDP, their debt is running at about 1 per cent, well below Australia. Mr Sun made it very clear that the growth in the Chinese economy would continue but it would moderate by necessity as the economy matured. He made it plain that the growth was managed and that makes all the sense in the world because their economy is changing from one based on building great infrastructure to a new era of output based on the operation and utilisation of those infrastructure assets. And even though they have a rapidly growing and enormous domestic consumer market, they know they need to be involved with the rest of the world and Mr Sun's visit to Melbourne and Sydney indicated just that.

My other invaluable source of information about the Peoples Republic of China is Mr Min Zhu, the deputy managing director of the IMF and formerly a deputy governor of the People's Bank of China. He previously worked at the Royal Bank and taught economics at the John Hopkins University. Mr Zhu's message was exactly the same: China is managing its economy down so that it doesn't become over-heated and exposed to the boom-and-bust syndrome so common in the West. They take a very long-term view and so should we by realising that they are great allies and partners for what we will both want and need for generations to come.

Current negative commentary about China's performance underestimates their intelligence. Mr Min Zhu has a PHD and an MA in economics from John Hopkins University and a Masters from the Woodrow Wilson School. Mr Sun, has a PHD from his Chinese university. They know East and West better than most of us.

It's obvious to me that a lot of our leaders and commentators are getting it wrong. China's going to be a major force for the foreseeable future and Andrew Robb has got us on board. Good on him. So has Barnaby Joyce with his deal this week to send a million live cattle to China. I think my two sources stack up against all the doubters.

Read more: http://www.smh.com.au/business/the-economy/chinas-economy-giving-us-a-f…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.