This article was first published as a 'Special Topic' in Treasury's July Monthly Economic Indicators report.

-------

The Budget Economic and Fiscal Update discussed a number of risks which might impinge on the outlook for the New Zealand economy. Amongst them were a marked slowdown in China’s economy, possibly sparked by a fall in house prices, and a weaker recovery in the euro area as a result of high levels of sovereign debt and banking sector weakness in peripheral economies. The risk of Greece defaulting on its debt or being unable to reach a further funding agreement with its European partners was seen as a particular risk.1

Both of these risks became elevated in the past month, but the Chinese equity market was the cause for concern rather than the housing market. By the end of the month, the immediate risks appeared to have lessened, but concerns remain about future developments in both economies.

This topic briefly recaps recent developments and then looks at the transmission channels to the New Zealand economy if those risks were to eventuate. It concludes that while they could have a material impact on the NZ economy, it is relatively well placed to adjust to such shocks.

Greek debt crisis to the fore in late June...

The Greek debt crisis came to a head in late June when negotiations between Greece and its European partners broke down, the Greek Prime Minister called a referendum on the latest proposal from its creditors, the existing bailout expired without any extension, and Greece went into arrears in its repayments to the International Monetary Fund (IMF). As a result of these developments, the European Central Bank (ECB) capped its Emergency Liquidity Assistance (ELA) to the Greek banking system; this in turn led to the imposition of capital controls in Greece, with banks closed for three weeks and limited cash withdrawals available from ATMs.

Although Greek voters rejected the latest proposal from their European creditors, negotiations recommenced with Greece submitting fresh proposals for spending reductions, tax reforms and other policy changes. After protracted negotiations over the weekend of 11-12 July, agreement for a third funding arrangement was reached subject to passing of “prior actions” by the Greek parliament and approval of the proposal by other European parliaments (where required). These conditions were met, preparing the way for formal negotiations on a fresh funding arrangement. As a result, Greece’s European creditors arranged a bridging loan from the European Financial Stability Mechanism (EFSM) which allowed Greece to clear its arrears with the IMF and repay the ECB on 20 July.

However, a new funding arrangement still has to be agreed and more reforms be passed by the Greek parliament. In addition, the IMF and European Union Commission consider that Greek debt is unsustainable, and Greece’s economic competitiveness needs to be restored. As a result, risks remain and some commentators still consider that Greece is likely to leave the European Monetary Union in the next few years.

...but limited financial contagion in Europe

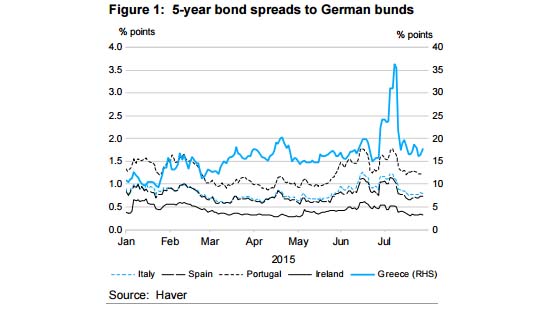

Although Greek bond rates spiked at the height of the debt crisis, spreads to German bunds in other peripheral European bond markets did not spike to the same extent (Figure 1). This could be taken either as an indication that markets considered that an escalation of the Greek debt crisis was unlikely, or that if it did escalate contagion to other financial markets in Europe would be limited. The latter view is supported by the steps that European authorities have taken since the previous Greek bailout in 2012 to strengthen the financial system and support peripheral economies’ bond markets; for example the ECB’s quantitative easing policy whereby it is purchasing government bonds in secondary markets. In addition, most Greek debt is now held publicly and so European banks are less exposed.

Sharp fall in Chinese equity market...

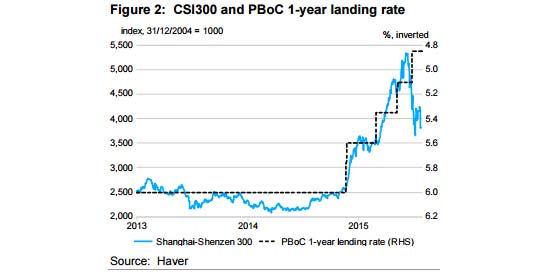

The China Securities Index 300 (CSI300, an index of 300 stocks traded on the Shanghai and Shenzen stock markets) peaked at 5,354 on 8 June 2015, up 145% from a year before (Figure 2). Its ascent had been particularly rapid since late 2014, doubling in value since November.

The rise in the Index was supported by a number of factors: the People’s Bank of China (PBoC) was reducing interest rates (Figure 2) and banks’ reserve requirement ratios at the time in order to offset slowing economic growth and further monetary easing was expected; falling house prices may have encouraged some investors to switch from property to equities; the government was taking steps to liberalise financial markets, for example by connecting the Shanghai and Hong Kong share markets; in addition the government provided funding for margin trading (leveraged borrowing to buy shares); and there was general encouragement for investing in the share market to give firms another source of capital in addition to bank lending.

Prices fell sharply in the second half of June and reached a low of 3,663 on 8 July, down 32% in one month. The immediate trigger for the fall was a clampdown on the use of margin finance in response to concerns about an equity bubble. Concerns that the economy was slowing may also have been a factor (although the market had been rising even as the economy was slowing), as well as prospective monetary tightening in the US and concerns about euro area financial stability.

When equity prices began to fall precipitously, the authorities stepped in to halt the fall. Interest rates were reduced further (Figure 2), trading was halted for selected firms, there was a temporary ban on the sale of selected stocks by major shareholders, initial public offerings were suspended, additional liquidity was provided and a market stabilisation fund established. The market stabilised temporarily in mid July, but then fell by 10% again in late July before steadying.

...but limited impact on other markets...

The fall in Chinese share prices had some effect on other equity markets, especially in Asia, but it is difficult to distinguish that from the impact of the Greek crisis. Exchange rates were also volatile. There was some increased risk aversion in global financial markets, with increased demand for US Treasury bonds, and both the Federal Reserve and Bank of England mentioned global risks as factors which might delay monetary tightening.

There was also some additional weakness in commodity prices; iron ore prices also recorded a 32% fall over the same period as Chinese equity prices, but from an already low base. They have since recovered slightly. How much of the recent decline in dairy prices is attributable to the share market fall is uncertain, as dairy prices continued to fall after the temporary stabilisation of the share market in mid July. Buyer sentiment may have been affected, given China’s importance to NZ’s dairy exports. Weaker economic growth in China and high dairy stocks, along with the imbalance in global dairy supply and demand, are the more important factors in the current weakness. (See discussion of recent dairy prices on p.5 above.)

...and on the Chinese economy...

However, the impact of the share market fall on China’s wider economy, including demand for dairy products, is not expected to be large:

• share values spiked briefly and households had not yet responded to the increase, so any response to the decrease is likely to be limited;

• the total market capitalisation of China’s share market is small relative to the size of the economy (equivalent to around 40% of GDP) compared with most developed economies (around 100% of GDP);

• although retail investors account for around 80% of market turnover, only 8% of households invest in the share market;

• shares account for only 10-15% of household financial assets (compared with around 50% in the US), reducing any wealth effects from the losses, whether realised or potential;

• business investment is unlikely to be adversely affected by the fall because even at the peak equity issuance accounted for only 5% of fundraising, compared with bank loans and corporate bonds at 75% and 10% respectively.

...but it may have other effects...

However, the share market fall may have other less tangible effects on China’s economy. It may have an adverse effect on consumer confidence, but retail sales had been easing despite previous increases in consumer confidence. Another possible impact is that GDP growth in the year to June was boosted by increased activity in the financial sector; to the extent that reflected higher share trading, the fall in the market may contribute to slightly lower growth in the second half of 2015.

The fall in the share market does not appear to pose a threat to financial stability, and may be positive in the long run given that it reverses a rapid increase before it became entrenched. The debt on leveraged share purchases is estimated at only 1.5% of total assets in the banking system.

...and raise deeper concerns

Another concern with China’s share market fall is that, rather than leading to weaker demand, it is itself a sign of slower economic growth. Indicators of economic activity have remained relatively robust so far (albeit against a background of slowing growth). However, the Caixin flash manufacturing PMI fell from 49.4 in June to 48.2 in July, indicating below-trend industrial growth. On the other hand, recent movements in the share market were influenced by a range of factors, most of which were not economic (including promotion of the stock market via official state media outlets), so it may not be a good indicator of economic activity. That said, the volatility in the market may discourage some local and foreign investors in the future and set back China’s financial liberalisation and reform agenda.

Impact on New Zealand minimal so far...

So far, the Greek debt crisis and the fall in China’s share market have had limited impact on global financial markets and the world economy, largely because the crises appear to have been temporarily resolved and the risks have declined. However, a more sustainable solution to Greece’s debt still needs to be found and China’s share market may have further to fall. The effect on New Zealand has also been limited so far, but it is worth considering how such risks would impact on the New Zealand economy if they developed further. The risks differ in each case and the effects would also be different.

Direct trade impacts from a financial crisis in Greece would be minimal as Greece accounted for only 0.1% of goods exports in 2014. However, the European Union accounts for around 12% of goods and services exports and a wider European financial crisis would have a larger impact on demand for New Zealand products and services.

In the case of a financial crisis in China which led to a more pronounced slowdown than currently expected, the impact on New Zealand would be more direct. China accounted for 17% of goods exports in the year to June 2015, with 76% of that concentrated in dairy, meat, forestry, wool and seafood exports. The recent fall in the share market is not expected to impact directly on consumer demand in China (for the reasons discussed above), but if it did it would lead to large falls in prices for these commodities. New Zealand could also be impacted by falling demand for services exports from Chinese consumers. China accounts for 10% of New Zealand’s services exports, with 20% growth in the past year, mainly in tourism and education. There could also be an indirect effect via Australia from weaker demand in China, particularly for mineral resources, as lower growth in Australia (our largest export market) would also impact on New Zealand.

There would also be an indirect effect via the rest of east Asia which accounts for 16% of NZ goods exports (excluding Japan).

In addition, a financial crisis, arising from either Greece or China, would lead to higher commercial interest rates and risk premiums, making offshore borrowing more expensive for New Zealand banks. Wealth effects, as asset prices fell, would also be important in such a case, as well as the impact on business and consumer confidence leading to lower investment and consumption.

...but NZ’s policies and frameworks are sound

However, New Zealand is relatively well placed to withstand a global economic or financial shock. The key points of resilience are:

• a floating exchange rate which has already started to adjust to the weakness in commodity prices that has occurred for other reasons;

• flexible monetary policy and room to reduce the policy rate further to offset any increase in offshore funding costs;

• regulatory changes since the global financial crisis have increased the strength and resilience of the banking system, e.g. the core funding ratio and “mis-match ratios” ensure that banks have stable funding and can meet immediate cash needs in the event of a crisis;

• bank capital requirements have been tightened to increase resilience and Basel III capital requirements were introduced in January 2013;

• the Reserve Bank could provide additional liquidity to the banking system, as it did during the global financial crisis;

• the Crown’s fiscal position is relatively strong and net debt is low, providing room for the government to cushion any adverse shock to the economy.

There are currently no signs that a financial crisis is developing from either of these risks, but if one were to develop it would have an effect on a small open economy such as New Zealand’s. However, the policies, frameworks and strength of public finances would buffer its impact on the economy.

1. Risks and Scenarios chapter, pp.54-55, http://www.treasury.govt.nz/budget/forecasts/befu2015/ befu15-5of11.pdf

38 Comments

I haven't even it read it, but let me summarise "everything is coming up roses", if they actually acknowledged the risks, it means they would have to do something other then endlessly pumping out reports on how well things are going, which is not easy when you are a one song band like treasury.

Very bad form to comment on any story without bothering to read it. That is not a 'comment', that is just a rant. Comment facility is looking for 'insight' and 'views', not pre-made-up closed-mind un-thought-through reaction. Low quality contribution.

was he incorrect?

the Crown’s fiscal position is relatively strong and net debt is low, providing room for the government to cushion any adverse shock to the economy.

Is the government's gross debt net asset offset in a condition to be liquidated?- if so, proof is needed. Is seller equity left in farm sales counted as new owner liability in addition to recorded bank debt?

Because let's face it- "The Worldwide Credit Boom Is Over, Now Comes The Tidal Wave Of Global Deflation" Read more

What do you mean by "seller equity left in farm sales"? I would have thought that when a farm, or any other asset, is sold - meaning, the buyer has paid, and the seller has received, the agreed price - then the seller no longer has any equity left in it and neither does the new owner have any further liability. Could you explain further please?

The difference ie loss between the mortgage and the sum received falls to the bank, which will either fall on the banks shareholders, and/or depositors and/or the tax payer if the govn bails the insolvent bank out.

No. Work it out for yourself.

I'm prepared to make any acknowledgement you like as to being stupid, ignorant and ill-informed, but I am afraid I cannot work it out.

Here's an example. Three years ago I bought a house from Fred for $500,000. I used $100,000 of my savings and borrowed $400,000 from a bank, which enabled me to pay Fred the $500,000.

Unless and until I repay $400,000, plus interest, to the bank, the bank has equity in my house, and I have a liability to the bank. This entails some risk to the bank's shareholders and possibly also to the taxpayer generally. That's all clear.

But unless I am misunderstanding something, your original comment suggested that Fred has an ongoing interest, over and above the money he has received, and I have an ongoing liability, over and above my debt to the bank. What? Why? Where?

I think he expects that farm prices will fall and the difference between what the farmer paid originally and what he will get on the mortgagee sale will equal the equity he paid into the farm. So he will lose the farm and lose the equity. This is what happened in the United States when many people were foreclosed upon after the GFC.

Years ago I sold my home. A price was agreed, but the buyer could not come up with the full amount and asked me to "leave $2000 in". He would pay me that 2 years later...

C'mon - dont get your hair in a knot:-

seller equity left in farm sales is or was once a common form of finance when a purchaser of a property has exhausted their ability to raise mortgage finance and comes up short and both parties are keen to do the business, it is not uncommon for the vendor to assist the buyer with "vendor finance" by filling the gap needed, (called leaving it in), as a second or third mortgage - can remember many advertisements "vendor finance available"

Have you never heard of that?

Thank you for your trouble, iconoclast. No, I had not heard of that practice, but now it is clear to me.

In such a case, to go back to Stephen Hulme's original comment, I see no reason why the seller's remaining equity should not be recorded as an ongoing liability for the buyer in such a case.

But what is the analogy with the state of the Government's finances?

My understanding is this:-

The statistics reported by the RBNZ are a summary of mortgage lending provided by the major lenders who in turn notify the RBNZ as a matter of course. Vendor finance is typically registered as a second mortgage but there is no mechanism requiring vendors, or their solicitors, to notify the RBNZ, therefore can be considered to be under the radar and therefore not recorded by RBNZ. Out of sight, out of mind

And, yes, it is a liability for the buyer

It can also be a great option for purchasing residental properties off retirees (especially for family Trusts).

The interest rate can be anything from 0 to whatever is reasonable, and can ensure the sale goes through, and/or provide a steady income for the future without huge risk. And the vendor doesn't need to commit so much of their own capital (or use up so much of their credit)

But what is the analogy with the state of the Government's finances?

Gross government debt offset by an FX and or basis currency swap related NZD valued foreign asset that cannot be liquidated until the swap expires, but thereafter will remain extinguished and non-existent. View D10 section 10

I will not explain further.

Certainly, if you don't want people to understand the points you are attempting to make then using plenty of technical jargon and declining to explain it when questioned is a good way of going about that.

That's really the issue - too few explanations detailing how seemingly inexplicable liability transformations are employed to distract the citizens from the truth - I had another audience in mind when I wrote the comment causing you so much consternation - they know exactly what I was getting at yet decline to pull back the veil.

So the expectation from the neo-liberals at Treasury is the Govn/tax payer (and their children) bails out the private debt then.

yet more rubbish from zero hedge blaming central banks for trying to keep the economy going while the greed of the gamblers, sharks and thieves knee cap it.

Do you harbour illusions that you are you a traduced ex- central banker or primary dealer employee?

No I harbour no illusions that the likes of me (a tax payer) will be paying if the parasites get tehir way.

If Obama and the Central Bankers had cared about saving the real economy, they would have insisted on bailing out the homeowners who even now are in negative equity in their homes and still struggling to pay off their crushing debts. But Obama's transitional Administration rejected a deal from Hank Paulson to bail out homeowners as well as the banks, even though fellow Democrats had negotiated a provision which made their approval of the Bush bailout conditional upon Federal assistance to homeowners in distress. He promised to provide aid in exchange for fresh bailout funds but reneged on the deal with his Democrat colleagues. Never has a President promised so much yet delivered so little. I reckon he'll go down in history as one of the most incompetent Presidents in history. I can't imagine another black president for many years.

"Frank goes on to explain that Obama rejected the request, saying “we have only one president at a time.” Frank writes, “my frustrated response was that he had overstated the number of presidents currently on duty,” which equally angered both the outgoing and incoming officeholders.

Obama’s unwillingness to take responsibility before holding full authority doesn’t match other decisions made at that time. We know from David Axelrod’s book that the Obama transition did urge the Bush administration to provide TARP loans to GM and Chrysler to keep them in business. So it was OK to help auto companies prior to Inauguration Day, just not homeowners."

http://www.salon.com/2015/03/31/barney_frank_drops_a_bombshell_how_a_sh…

Obama is very much becoming the Canute before the tide. No indication he didn't want to back homeowners, or even give them interest relief, but he is just one person against a sea of self-interested US bureaucrats.

A rather charitable assessment of Obama's leadership, especially considering the fact he allowed his advisory council to be riddled with bank lobbyists.

"First of all, Obama’s economic and financial policy, Cabinet and advisers are largely retreads of the Clinton administration. So from the standpoint of the banking community, and connections to the banking community, there was very much an overlap, if not a complete overlap, of individuals who were all key to the deregulation of the banking industry, and who either came from, or now speak for, large sums of money through the banking industry …"

http://www.salon.com/2014/04/15/we_are_in_great_danger_ex_banker_detail…

Of course they became mega-un-regulated monsters under the previous administration's repeal of much regulation and even non-enforcing of what little there was. On top of that the President is quite constrained in what actions he can do due to politics not least of which was at the least the lower house in the bankers pockets.

You mean the deregulation which happened under the watch of Bill Clinton? Both sides of the "aisle" are utterly compromised by banking interests, and its true in New Zealand too.

The late Bruce Jesson covered it extensively in his book, Only their Purpose is Mad, back in the 1990s.

Certainly Clinton was not without fault, but he certianly didnt leave the economy a basket case.

"both sides" yes certainly the Republicans are, are the democrats clean? no certainly not.

Sure, the dot com bubble being inflated and then bursting had nothing to do with Clinton? Or the recession that followed?

"The seven-member Business Cycle Dating Committee of the Cambridge, Massachusetts-based National Bureau of Economic Research may change its determination that the recession started in March 2001 to reflect recent revisions to government growth statistics, committee members, including Victor Zarnowitz, said."

http://www.bloomberg.com/apps/news?pid=newsarchive&sid=azwhJVa5rWhU

I am talking about the leadership of both parties, there have been several rank and file Senators and Congressmen/women who held various bank heads and regulators over the coals in Congress or the Senate, but nobody was actually held responsible.

Oh I think out of necessity he is an honest politician, he hasn't done what others couldn't, but hasn't had to start much in the way of major laws...things like TPPA aren't coming from his office. It's very Ford-hands-off like...but that just shows who the puppetmasters are (and they're getting bolder and less obfuscated)

self-interested US investors and companies more like.

The classic "old" response was a debt jubilee, Steve keen proposed a similar idea a few years ago. I dont agree on the incompetent bit, with the ACA working I think he'll go down as one of the better ones, certainly far better than GB. Has he been perfect as seen from ppls point of view such as yourself? well I guess not.

I would be very very (yes two verys) upset if the government consider that idea or that private people were banking on the possibility.

That the kids think they can spend it large, because Mum&Dad have not run their credit cards to the maximum and can still bail them out is massively risky.

Then this is not regarded as a shock, therefore excluded from comment

New Zealand’s milk industry shows how commodity-producing countries across the world are struggling after having overestimated demand from China’s fast-growing economy. As with sugar producers in Brazil, rubber farmers in Thailand and iron ore miners in Australia, New Zealand’s milk producers are coming to grips with the reality that Chinese demand didn’t materialize as expected when capacity was put in place many months back.

“It may take several years for Chinese demand to match the levels reached in 2013 and 2014, which suggests that export price recovery, which will make a significant difference in farmgate prices, may be slower than many farmers and commentators are hoping for.”

http://blogs.wsj.com/economics/2015/06/02/how-chinas-taste-for-milk-act…

Needless to say there are other suppliers/producers/exporters trying to race thru that same now smaller opening - aside from now established China owned production facilities in Europe, USA, and Oceania. .

China's dairy consumption volume declined 1% YoY in 2014:

https://doc.research-and-analytics.csfb.com/docView?language=ENG&source…

see page 16: Go vertical to warrant product safety

Then this is regarded as a past event - not a shock, therefore excluded from comment

some wmp buyers are never coming back - to any exporter....

Changes in the domestic production standard in China has meant those producing fresh white milk can only use raw milk rather than reconstituting powder, Mr Chen said. Because of this, large processors have been looking at local farms, rather than imports.

and price has nothing to do with it....

He said China’s biggest processors were opting for strategic relationships with quality domestic suppliers rather than cheaper importers.

http://www.weeklytimesnow.com.au/agribusiness/dairy/waiting-on-china-to…

said so. Chinese policy is that government is there to look after the Chinese Peoples' interests. Same as US. In fact NZ is the only country stupid enough to declare a global open playa field.

Not so, it's intentional by the neocon fleecers.

Indicators of economic activity have remained relatively robust so far (albeit against a background of slowing growth).

Those robust economic indicators being...

Tuesday, August 04, 2015

China Mengniu Dairy (2319) shares plunged as much as 12.7 percent yesterday after Goldman Sachs downgraded the stock to "sell" and slashed its target price by 33 percent to HK$30.10. Shares of the mainland's second-largest dairy producer hit a low of HK$30.50 at noon, but recovered to close at HK$33.55, down 4.28 percent. This chalked up a three-week high turnover of HK$376 million.

Goldman Sachs said in a research report that weak consumption had led to an oversupply in China's dairy market, forcing Mengniu to lower prices in an attempt to move six months' worth of inventories. Mengniu uses raw milk produced in the mainland which is dearer than in Europe and New Zealand, tempering profit growth.

According to the report, Mengniu deployed inefficient marketing strategies while restructuring its distributors and sales team, which had led to a loss of market share. Goldman Sachs also lowered Mengniu's price-to-earnings ratio target to 18.4 times, down from 23 times a 20 percent discount to the average valuation among its peers.

Shares of its peers also performed poorly yesterday, ahead of the release of the New Zealand dairy index today a bimonthly index of dairy prices which has fallen nine times in a row.

Yashili (1230) fell 4 percent to HK$2.16 and China Modern Dairy (1117) lost 2.79 percent. MIRA DING

http://www.thestandard.com.hk/news_detail.asp?pp_cat=1&art_id=159770&si…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.